|

市場調查報告書

商品編碼

1537691

汽車煞車皮:市場佔有率分析、產業趨勢、成長預測(2024-2029)Automotive Brake Pad - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

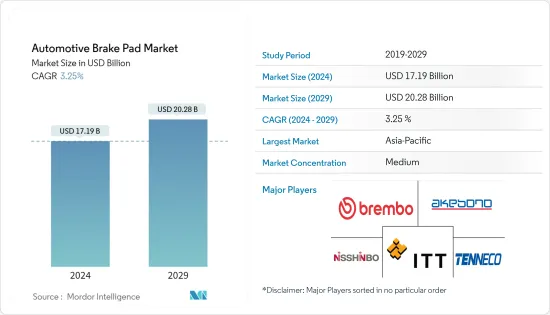

汽車煞車皮市場規模預計到2024年為171.9億美元,預計到2029年將達到202.8億美元,在預測期內(2024-2029年)複合年成長率預計為3.25%。

由於消費者偏好的變化、汽車產量的增加以及對車輛安全性的日益重視等多種因素,汽車煞車皮市場正在經歷動態成長和轉型。市場成長是由對陶瓷和石棉有機複合複合材料等輕質和先進摩擦材料的需求不斷成長、產品推出數量的增加、乘客和行人安全意識的提高以及政府加強安全法規所推動的。

此外,快速的都市化、交通堵塞以及對高性能車輛不斷成長的需求正在推動乘用車和電動車 (EV) 的需求。電動車的普及為煞車皮製造商提供了開發專用解決方案以滿足電動車再生煞車獨特要求的機會。汽車需求的激增正在擴大煞車皮市場。

此外,高階和豪華汽車製造商越來越注重製造功能增強的新產品,以及新興市場乘用車銷售需求的不斷成長,預計將在預測期內增加汽車煞車皮市場,從而進一步推動成長。產業參與者經常推出針對卡車和 SUV 客製化煞車設計的新產品,預計將在預測期內加速市場成長。然而,原料價格上漲和有害物質法規等嚴格法規可能會抑制市場成長。

由於汽車銷售的成長和消費者可支配收入的增加,預計亞太地區將主導市場。此外,在整個預測期內,新興國家廉價勞動力和原料的供應也推動了該市場的發展。中國和印度正在推動該產品的需求增加,並推動該地區的成長。特別是中國,由於嚴重事故的迅速增加和機隊的擴大,預計將成為該行業的主要企業,並有望進一步促進業務成長。

汽車煞車皮市場趨勢

乘用車市場領先的細分市場

乘用車細分市場是汽車煞車皮市場中最大的細分市場,受到乘用車數量增加、消費者對車輛升級偏好的變化以及煞車系統技術進步等因素的推動。

此外,道路上大量的客車直接增加了對煞車皮的需求。 2022年,全球乘用車銷量為5,749萬輛,相較於2021年的5,644萬輛,與前一年同期比較同期成長約1.9%。隨著乘用車產量和銷量的預計成長以及電動車在全球的普及,未來幾年將需要具有更高耐用性和散熱性能的先進汽車煞車皮產品,預計需求將快速成長。

此外,嚴格的安全法規和消費者對車輛安全意識的提高也推動了市場的發展。乘用車是個人和家庭最廣泛使用的交通工具,並且由於容易發生事故而受到嚴格的安全法規的約束。許多地區的政府都推出了有關車輛煞車系統的強制性法規。例如

- 2023 年 7 月,NHTSA提案了新的聯邦機動車輛安全標準,要求輕型車輛配備自動緊急煞車系統,包括行人 AEB。 NHTSA 估計,這項提議的規則每年將挽救至少 360 人的生命並減少至少 24,000 人受傷。

此外,隨著已開發國家對乘用車的需求不斷增加,市場主要參與者正在增加對煞車皮耐用性的投資,因為高階和豪華汽車製造商被迫增加投資來開發具有先進功能的新產品。研發,引進尖端材料與設計,提升性能、安全性和性能。例如

- 2023 年 8 月,日本 Totachi Industrial 開始生產煞車皮,擴大其綜合解決方案產品範圍。煞車皮是該公司產品線的新成員,專為各種品牌的乘用車而設計。這些煞車皮作為OEM(目的地設備製造商)產品精心製造,確保卓越的品質。

因此,預計乘用車領域在預測期內將顯著成長。

亞太地區是最有前景的市場

全球整體,亞太地區佔據市場主導地位,其次是歐洲和北美。預計亞太地區的成長率最高,由於安全標準和政府法規的收緊,中國、印度、日本和韓國等國家對全球防鎖死煞車系統收益成長做出了重大貢獻。

作為全球最大的汽車市場,中國預計將成為關鍵地區之一。到2022年,中國將成為全球最大的區域汽車市場,光是汽車銷售就將超過2,360萬輛。這種成長直接影響了對煞車皮的需求,因為每輛車都需要這個重要零件。此外,中國的汽車工業正在不斷發展,煞車皮技術也不斷發展。

降低噪音、延長墊片壽命和提高煞車性能是極為重要的功能。在噪音污染令人擔憂的城市環境中,低噪音煞車皮的需求量很大。中國煞車皮市場競爭激烈,國內外廠商爭奪市場佔有率。幾個主要市場參與者正在大力投資在該國建立新的生產設施。例如

- 2023年6月,美國供應商天納克宣布,其目標是透過專注於本土電動車製造商來提高其在中國煞車零件業務的收益,而這也是中國煞車皮市場的驅動力。

此外,印度汽車產業的生產和銷售正在成長,使其成為煞車皮的潛在市場。售後市場領域在印度煞車皮市場中扮演重要角色。定期更換煞車皮對於道路安全和車輛維護至關重要,從而推動售後市場銷售。在這個市場上,許多公司正在大力投資在國內建立新的生產設施,以滿足不斷成長的國內外需求並提高盈利和市場佔有率。例如

- 2023 年 3 月,印度和全球OEM的一級供應商 Brakes India 推出了 ZAP煞車皮,該煞車片採用專為電動車量身定做的先進摩擦技術。這款專用煞車皮旨在滿足電動車客戶的獨特需求,提供更好的防腐蝕保護和更安靜的運行。

在此類全部區域發展的支持下,汽車煞車皮的需求預計在預測期內將以合理的速度成長。

汽車煞車皮產業概況

汽車煞車皮市場主要分為ITT Inc.、Brembo SpA、ADVICS、北京德爾福萬源引擎管理系統、博格華納上海汽車燃油系統、羅伯特·博世有限公司、德爾福科技、天納克公司、Akebono Brake Company、 主要企業 Brakes等。由於少數製造公司的存在,該市場正在經歷適度的整合。

這些市場領導在研發方面投入大量資金,將尖端技術融入其產品中,並不斷推出升級產品以保持競爭力。

- 例如,2023 年 3 月,Brakes India 推出了 ZAP煞車皮,該煞車片採用專用電動車設計的卓越摩擦技術。除了高度耐腐蝕之外,該墊片還提供安靜的煞車,直接滿足電池供電車輛的需求。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 煞車皮材料和技術的進步

- 市場限制因素

- 煞車皮市場受原物料成本影響

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 依材料類型

- 半金屬

- 無石棉有機

- 低金屬

- 陶瓷製品

- 按職位類型

- 正面

- 後部

- 按銷售管道

- 目的地設備製造商(OEM)

- 售後市場

- 按車型

- 客車

- 商用車

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 韓國

- 日本

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- Brembo SpA

- Nisshinbo Brake Inc

- ITT Inc.

- Robert Bosch GmBH

- Tenneco Inc.

- Akebono Brake Company

- Beijing Delphi Wanyuan Engine Management Systems Co., Ltd.

- ADVICS

- EBC Brakes

- BorgWarner Shanghai Automotive Fuel Systems Co., Ltd.

第7章 市場機會及未來趨勢

- 對環保煞車皮的需求不斷成長

The Automotive Brake Pad Market size is estimated at USD 17.19 billion in 2024, and is expected to reach USD 20.28 billion by 2029, growing at a CAGR of 3.25% during the forecast period (2024-2029).

The automotive brake pad market is experiencing dynamic growth and transformation, driven by a combination of factors, including changing consumer preferences, increasing vehicle production, and the growing focus on vehicle safety. The growth of the market depends on several factors, such as the rise in demand for lightweight and advanced friction materials, such as ceramic and asbestos organic composites, the rising number of product launches, increasing awareness regarding passenger and pedestrian safety and increasing safety regulations by the government.

Furthermore, rapid urbanization, traffic congestion, and the growing demand for high-performance vehicles are propelling the demand for passenger and electric vehicles (EVs). The proliferation of electric vehicles is presenting opportunities for brake pad manufacturers to develop specialized solutions tailored to the unique requirements of regenerative braking in EVs. This surge in demand for automobiles, in turn, augments the brake pad market.

Moreover, the growing focus by the premium and luxury car manufacturers to manufacture new products with enhanced features and growing demand for passenger car sales in developed nations is further expected to drive the automotive brake pads market growth during the forecast period. Industry players are frequently launching new products with customized braking designs for trucks and SUVs is expected to accelerate the market growth during the forecast period. However, increases in the prices of raw materials and stringent regulations such as toxic substances control are likely to restrain the market's growth.

The Asia-Pacific region is projected to dominate the market due to the increasing sales of vehicles, as well as an uptick in disposable income among consumers. This is further bolstered by the availability of inexpensive labor and raw materials in emerging economies throughout the forecast period. China and India serve as catalysts for growth within the region, as they contribute to the rising demand for the product. China, in particular, is anticipated to emerge as a major player in the industry due to a surge in serious accidents and an expanding fleet, which is expected to further contribute to the growth of the business.

Automotive Brake Pad Market Trends

Passenger Car is the Leading Segment in the Market

The passenger car segment is the largest segment in the automotive brake pad market, driven by factors like increasing volume of passenger cars, changing consumer preferences towards vehicle upgradation, technological advancement in braking systems, etc. among others.

Further, the huge volume of passenger cars on the roads contributes directly to the demand for brake pads. In 2022, 57.49 million units of passenger cars were sold globally, as compared to 56.44 million units in 2021, registering an year-on-year growth of about 1.9 percent. With the increase in passenger car production and sales and the anticipation of greater adoption of electric vehicles across the globe, there will be surge in demand for advanced automotive brake pad products with higher durability and greater heat dissipation capability in the coming years.

Additionally, stringent safety regulations and increasing consumer awareness regarding vehicle safety also drives the market. Being the most widely used personal mode of transport for individuals as well as for families, passenger cars are prone to accidents, and thus are subject to strict safety norms. Government in many regions gave introduced mandatory regulations regarding braking system in cars. For instance,

- In July 2023, the NHTSA proposed a new Federal Motor Vehicle Safety Standard to require automatic emergency braking systems including pedestrian AEB on light vehicles. The NHTSA projects that this proposed rule would save at least 360 lives a year and reduce injuries by at least 24,000 annually.

Additionally, the rising investments from premium and luxury car manufacturers to develop new products with advanced features, coupled with the increasing demand for passenger cars in developed nations, are compelling the key market players to invest in research and development to introduce advanced materials and designs that enhance the durability, performance, and safety of brake pads. For instance,

- In August 2023, Totachi Industrial Co. Ltd., based in Japan, expanded its comprehensive solution by initiating the manufacturing of brake pads. The latest addition to their product lineup encompasses brake pads designed for passenger cars across diverse brands. These brake pads are meticulously crafted to serve as original equipment manufacturer (OEM) products, guaranteeing exceptional quality.

Hence, the passenger car segment is expected to witness significant growth during the forecast period.

Asia Pacific to be the most Potential Market

Globally, Asia-Pacific is the most dominant region in the market, followed by Europe and North America. Asia-Pacific is likely to possess the highest growth rate, with countries like China, India, Japan, and South Korea expected to contribute significantly to the growth in terms of revenue in the global anti-lock braking system due to safety norms and firm government regulations.

China is expected to emerge as one of the major regions, owing to its largest automotive market in the world. China was the world's largest regional market for automobiles in 2022, accounting for over 23.6 million units sales alone. This growth directly influences the demand for brake pads, as each vehicle requires this essential component. Also, the automotive industry in China is evolving, and so is the brake pad technology.

Noise reduction, extended pad life, and enhanced braking performance are crucial features. In urban environments where noise pollution is a concern, low-noise brake pads are highly sought after. The brake pad market in China is highly competitive, with both local and international players vying for market share. Multiple key market players are making substantial investments to establish new production facilities within the country. For instance,

- In June 2023, Tenneco, a U.S. supplier, set its sights on boosting revenue from its brake parts business in China by focusing on local manufacturers of electrified vehicles, which also drive the brake pad market in the country.

Moreover, the growing vehicle production and sales in the automotive sector in India makes it a potential market for brake pads. The aftermarket segment plays a substantial role in the Indian brake pad market. Regular brake pad replacement is essential for road safety and vehicle maintenance, which fuels aftermarket sales. Numerous players in the market are investing heavily in setting up new production units in the country to meet the rising demands for local and international markets and enhance their profitability and market share. For instance,

- In March 2023, Brakes India, a Tier-1 supplier to both Indian and global OEMs, introduced ZAP brake pads featuring advanced friction technology tailored for electric vehicles. These specialized brake pads are designed to meet the unique needs of electric vehicle customers, providing improved corrosion protection and ensuring quieter braking.

On the back of such development across the region, the demand for automotive brake pads is likely to grow at a decent rate during the forecast period.

Automotive Brake Pad Industry Overview

The automotive brake pad market is primarily dominated by key players such as ITT Inc., Brembo S.p.A., ADVICS, Beijing Delphi Wanyuan Engine Management Systems Co., Ltd., BorgWarner Shanghai Automotive Fuel Systems Co., Ltd., Robert Bosch GmBH, Delphi Technologies, Tenneco Inc., Akebono Brake Company, and EBC Brakes, among others. This market exhibits moderate consolidation due to the presence of a select few manufacturing companies.

These market leaders are heavily investing in research and development to integrate state-of-the-art technology into their products, consistently introducing upgraded offerings to maintain their competitive edge.

- For instance, in March 2023, Brakes India introduced ZAP brake pads, leveraging superior friction technology specifically designed for electric vehicles. These pads not only offer better corrosion protection but also ensure silent braking, catering directly to the needs of battery-powered

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Advancements in Brake Pad Materials and Technologies

- 4.2 Market Restraints

- 4.2.1 The Brake Pad Market is Influenced by the Cost of Raw Materials

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Material Type

- 5.1.1 Semi-Metallic

- 5.1.2 Non-Asbestos Organic

- 5.1.3 Low-Metallic

- 5.1.4 Ceramic

- 5.2 By Position Type

- 5.2.1 Front

- 5.2.2 Rear

- 5.3 By Sales Channel Type

- 5.3.1 Original Equipment Manufacturers (OEMs)

- 5.3.2 Aftermarket

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 South Korea

- 5.5.3.4 Japan

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the world

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Brembo S.p.A.

- 6.2.2 Nisshinbo Brake Inc

- 6.2.3 ITT Inc.

- 6.2.4 Robert Bosch GmBH

- 6.2.5 Tenneco Inc.

- 6.2.6 Akebono Brake Company

- 6.2.7 Beijing Delphi Wanyuan Engine Management Systems Co., Ltd.

- 6.2.8 ADVICS

- 6.2.9 EBC Brakes

- 6.2.10 BorgWarner Shanghai Automotive Fuel Systems Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand For Environmentally Friendly Brake Pads

全球燒結煞車片市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球燒結煞車片市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年全球汽車煞車皮市場報告

2025 年全球汽車煞車皮市場報告 汽車煞車皮市場規模、佔有率和成長分析(按材料、位置、車型、銷售管道和地區)- 2025-2032 年產業預測

汽車煞車皮市場規模、佔有率和成長分析(按材料、位置、車型、銷售管道和地區)- 2025-2032 年產業預測 燒結煞車片市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料成分、車輛類型、配銷通路、地區和競爭細分,2020-2030F

燒結煞車片市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料成分、車輛類型、配銷通路、地區和競爭細分,2020-2030F 燒結煞車皮的全球市場:2024年

燒結煞車皮的全球市場:2024年 NAO 煞車片的全球市場:~2030 年

NAO 煞車片的全球市場:~2030 年 全球煞車皮市場:按材料、零件、分銷管道和車型分類 - 2025-2030 年預測

全球煞車皮市場:按材料、零件、分銷管道和車型分類 - 2025-2030 年預測 電動汽車煞車皮市場:按類型、銷售管道、車型分類 - 2025-2030 年全球預測

電動汽車煞車皮市場:按類型、銷售管道、車型分類 - 2025-2030 年全球預測 全球煞車片市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測

全球煞車片市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測 2024-2028年全球汽車煞車皮市場

2024-2028年全球汽車煞車皮市場