|

市場調查報告書

商品編碼

1548913

採購軟體:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Procurement Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

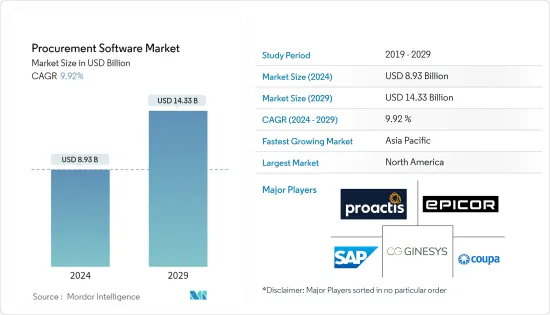

採購軟體市場規模預計到 2024 年為 89.3 億美元,預計到 2029 年將達到 143.3 億美元,在預測期內(2024-2029 年)複合年成長率為 9.92%。

軟體公司越來越關注需求技術,並重新探索為客戶服務的創新方式。推動採購軟體產業的關鍵因素是人工智慧等成熟技術的不斷整合,以支援高品質的報告和保持準確性的功能。

主要亮點

- 隨著對採購程序自動化的需求不斷增加,電子採購技術的成熟預計將為預測期內的市場成長提供新的途徑。此外,防止重複記錄的需求預計將在未來幾年推動採購軟體產業的成長。此外,政府政策的落實將促進市場發展。跨境對外貿易的增加將進一步加快市場發展。供需促進因素之間的市場協同效應預計將影響未來的市場成長。

- 人們越來越希望自動化採購業務以提高效率並縮短時間。它還可以將人員從耗時且不必要的任務中解放出來,從而加快流程。採購流程的自動化變得越來越流行,特別是在採購申請、採購訂單、申請管理、供應商管理和合約核准。

- 電子採購軟體可協助組織整合和自動化整個採購流程。 ERP 透過簡化採購流程、騰出時間專注於其他任務並實現更有效率的業務,讓供應商管理變得更加輕鬆。除此之外,ERP 解決方案可以幫助改善業務報告、改善客戶服務、降低庫存成本、增加現金流量、降低成本、資料和雲端安全、供應鏈管理等等。這些因素正在推動市場擴張。

- 2023 年 9 月,SAP SE、Bristol & Weston NHS 採購聯盟 (BWPC) 宣布已選擇 SAP Ariba 透過雲端上的單一現代採購平台為其數位採購轉型計畫提供支援。

- 此外,2023 年 8 月,全球領先的運輸和物流公司南非 Bidvest International Logistics 與認知採購軟體供應商 Zycus 簽訂了一項多年期協議,使 Zycus 的人工智慧解決方案能夠將從付款到付款目的地的情況。 Bidvest 的關鍵目標是加快申請處理速度並最佳化整個 PR 到 PO 流程,包括降低 PO 處理成本。因此,該公司選擇了具有電子採購功能的申請解決方案以及 Zycus 的人工智慧驅動的應付應付帳款(AP) 自動化解決方案。此解決方案可實現經濟高效的申請處理、與供應商更好的溝通、動態折扣、詐騙偵測,並有助於實現全球合規性。

- 由於許多組織缺乏使用遺留系統所需的基礎設施,預計採購軟體市場在預測期內將面臨挑戰。相反,熟練勞動力的缺乏正在阻礙市場的成長。

- COVID-19 的爆發加速了採購流程的數位轉型,並凸顯了採購軟體對於實現供應鏈管理敏捷性、彈性和效率的重要性。隨著公司不斷適應不斷變化的商業環境,市場需求預計將會成長。 COVID-19 後的情況凸顯了採購軟體在提高公司業務效率、降低風險和創造策略價值方面的重要性。

採購軟體市場趨勢

零售業預計將佔據主要市場佔有率

- 預計零售業將佔據很大佔有率。競爭的加劇、利潤率的下降和品牌忠誠度的下降迫使零售商尋找新的方法來保持盈利和競爭力。零售企業領導者越來越依賴採購團隊來降低成本、降低供應風險並創造更多價值。因此,零售業擴大採用採購軟體。

- 採購軟體可協助零售商整合其業務流程並提高整體業務價值。它還促進了從申請到付款完成的金融供應鏈透明度和合約細節。根據印度品牌資產基金會預測,到2025年,印度零售市場規模預計將達到1兆美元。因此,採購服務預計將成為推動預測期內成長的巨大需求。

- 隨著業務流程變得數位化,許多零售公司正在採用電子採購解決方案來自動化和簡化採購流程。電子採購平台促進線上採購、電子帳單以及與供應商的協作,提高效率並節省成本。

- 此外,採購軟體工具可讓零售商實現採購業務自動化,並從供應商獲得最佳競標價格,這對於採購大量商品的零售商來說至關重要。採購軟體解決方案使公司能夠與供應商協作、追蹤事件、獲取警報並分析商業智慧資料,以深入了解採購流程以進行預測和規劃。

- 此外,該技術透過整合供應鏈和促進庫存管理,簡化了圍繞需求和銷售額預測的決策流程。它還具有營運成本最低、營運效率高等優勢,預計在未來幾年加快零售業的市場成長速度。

預計北美將佔據較大市場佔有率

- 由於對採購流程集中化的需求不斷成長,北美在全球佔據主導地位。此外,該地區成立的公司的整合預計將推動未來市場的成長。

- 美國力求透過重點改善該國工業部門整個供應鏈的活動來提高生產力並加強製造業。北美零售市場的電子零售商正在努力透過納入當日送達來改善客戶體驗,這可以透過有效的供應鏈管理來有效實現。

- 北美採購軟體供應商不斷創新,以保持競爭力並滿足不斷變化的客戶需求。創新的關鍵領域包括人工智慧(AI)、機器學習、預測分析、機器人流程自動化(RPA)、區塊鏈和高階資料分析,以提高採購效率、決策和風險管理。

- GDPR 等監管合規要求和特定產業法規正在推動採購軟體在該地區的採用。採購軟體供應商提供的功能和特性可協助組織遵守法規、管理風險並確保採購流程的透明度和課責。

採購軟體行業概況

採購軟體市場較為分散,既有跨國公司,也有中小企業。市場主要參與者包括 SAP SE、Proactis Holdings PLC、Epicor Software Corporation、Ginesys (Ginni Systems Limited)、Coupa Software Inc. 等。市場上的公司正在採取聯盟和收購等策略來增強其軟體產品並獲得永續的競爭優勢。

- 2024 年 4 月:Iris Software Group 與 Amazon Business 合作,最佳化英國學校的採購。此次合作將使 Iris 的 5,254 名客戶能夠使用 Iris Financials(該集團基於雲端基礎的學校財務軟體)有效地從 Amazon Business 購買設備。

- 2023 年 10 月 Maximus UK 推出採購軟體 Atamis。 Atamis 提供的採購軟體可以最佳化 Maximus UK 的採購流程、提高效率並降低成本。透過實施 Atamis 的採購軟體,Maximus UK 進入了一個注重業務和提高效率的新採購階段。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估 COVID-19 對全球採購軟體市場的影響

第5章市場動態

- 市場促進因素

- 採購流程自動化的需求不斷增加

- 電子採購應用程式和 ERP 解決方案的整合

- 零售業預計將佔據主要市場佔有率

- 市場挑戰

- 與現有系統整合和供應商入職的複雜性

第6章 市場細分

- 按配置

- 本地

- 雲

- 按最終用戶產業

- 零售

- 製造業

- 運輸/物流

- 衛生保健

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲/紐西蘭

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- SAP SE

- Proactis Holdings PLC

- Epicor Software Corporation

- Ginesys(Ginni Systems Limited)

- Coupa Software Inc.

- Zycus Inc.

- GT Nexus(Infor Inc.)

- Ivalua Inc.

- Microsoft Corporation

- Oracle Corporation

- Basware AS

- Mercateo AG

- GEP Corporation

- Jaggaer Inc.

第8章投資分析

第9章 市場機會及未來趨勢

The Procurement Software Market size is estimated at USD 8.93 billion in 2024, and is expected to reach USD 14.33 billion by 2029, growing at a CAGR of 9.92% during the forecast period (2024-2029).

Software companies are increasing their focus on in-demand technologies and re-exploring innovative ways to serve their clients. The primary factor driving the procurement software industry is the increased integration of developing technologies, such as artificial intelligence, which assists in high-quality reports and features to maintain accuracy.

Key Highlights

- With the growing requirement to automate procurement procedures, the maturation of e-procurement technology is expected to offer new avenues for market growth during the forecast period. Furthermore, the need to prevent duplicate records is projected to drive the growth of the procurement software industry in the future. Moreover, the implementation of government policies encourages market development. The increase in the flow of foreign transactions across borders fuels the market's progress even further. The market synergy between supply and demand drivers is predicted to affect future market growth.

- There is a growing desire to automate procurement operations to improve efficiency and reduce time. It also expedites the process by relieving personnel of time-consuming and unneeded tasks. Procurement process automation is becoming increasingly popular, especially in buy requests, purchase orders, invoice management, vendor management, and contract approval.

- E-procurement software helps an organization integrate and automate its whole procurement process. ERP assists in easing supplier management by facilitating the procurement processes, freeing time to concentrate on other tasks, and enabling a more effective business, which is made possible when e-procurement tools are connected with ERP solutions. Among other things, ERP solutions support improved business reporting, better customer service, lower inventory costs, increased cash flow, cost reductions, data and cloud security, and supply chain management. These factors encourage market expansion.

- In September 2023, SAP SE, Bristol & Weston NHS Purchasing Consortium (BWPC) announced it had selected SAP Ariba to drive its digital procurement transformation program as it embraces a single modern procurement platform in the cloud.

- Further, in August 2023, one of South Africa's leading global transport and logistics companies, Bidvest International Logistics, signed a multi-year agreement with Zycus, a cognitive procurement software provider, to transform its source-to-pay landscape with Zycus' AI-powered solutions. A key goal for Bidvest was to enable faster invoice processing and optimize the entire PR to PO process, including lowering PO processing costs. The organization has hence selected the invoicing solution with e-procurement alongside Zycus' AI-led accounts payable (AP) automation solution, which would also enable cost-efficient invoice processing, better supplier communications, dynamic discounting, and fraud detection, as well as help in achieving global compliance.

- The market for procurement software is expected to have challenges during the forecast period because many organizations lack the infrastructure necessary to work with traditional systems. On the contrary, the lack of skilled personnel impedes the market's growth.

- The COVID-19 pandemic has accelerated the digital transformation of the procurement process and highlighted the importance of procurement software in enabling agility, resilience, and efficiency in supply chain management. As businesses continue to adapt to the evolving business landscape, the demand in the market is expected to grow. The post-COVID-19 landscape has reinforced the importance of procurement software in driving operational efficiency, risk mitigation, and strategic value creation for businesses.

Procurement Software Market Trends

Retail Industry is Expected to Hold Significant Market Share

- The retail industry is anticipated to cater to a significant share. The growing competition, falling margins, and diminishing brand loyalty have made retailers look for new ways to remain profitable and competitive. Business leaders at retail enterprises are increasingly turning to their procurement teams to reduce costs, mitigate supply risks, and create more value. This has enabled the adoption of procurement software in the retail industry.

- Procurement software helps retailers to integrate business processes and improve the overall value of businesses. It facilitates transparency in financial supply chains and contract details for generating invoices to complete payments. According to the India Brand Equity Foundation, the Indian retail market size is expected to account for USD 1 trillion by 2025. Therefore, procurement services are expected to be a huge requirement that drives growth during the forecast period.

- With the increasing digitization of business processes, many retailers are adopting e-procurement solutions to automate and streamline their procurement processes. E-procurement platforms facilitate online purchasing, electronic invoicing, and supplier collaboration, driving efficiency and cost-saving.

- Further, procurement software tools enable retail companies to automate procurement tasks and procure the best rates from vendors for their tender, making it essential for retail companies to procure a large volume of goods. With the implementation of procurement software solutions, companies can collaborate with suppliers, track events, get alerts, and analyze business intelligence data to gain insights into the procurement process for forecasting and planning purposes.

- Moreover, this technology simplifies the decision-making process that concerns demand and sales forecast by consolidating the supply chain and facilitating inventory management. It also offers advantages such as minimum operational cost and higher operational efficiency, which are presumed to increase the growth pace of the market in the retail industry in the coming years.

North America is Expected to Hold Significant Market Share

- North America dominates globally due to the rising demand for centralized procurement processes. Also, consolidating companies incorporated in the region is expected to provide an impetus to market growth in the future.

- The United States is rigorously looking to strengthen its manufacturing industry by enhancing its productivity by emphasizing improving activities across the supply chain within the country's industrial sector. E-retailers in the North American retail market are rigorously trying to enhance the customer experience by incorporating same-day delivery, which can be achieved effectively through effective supply chain management.

- Procurement software vendors in North America continually innovate to stay competitive and address evolving customer needs. Key areas of innovation include artificial intelligence (AI), machine learning, predictive analytics, robotic process automation (RPA), blockchain, and advanced data analytics to enhance procurement efficiency, decision-making, and risk management.

- Regulatory compliance requirements, such as GDPR and industry-specific regulations, drive the adoption of procurement software in the region. Procurement software vendors offer features and functionalities to assist organizations in complying with regulatory mandates, managing risk, and ensuring transparency and accountability in procurement processes.

Procurement Software Industry Overview

The procurement software market is fragmented, with the presence of global players and small and medium-sized enterprises. Some of the major players in the market are SAP SE, Proactis Holdings PLC, Epicor Software Corporation, Ginesys (Ginni Systems Limited), and Coupa Software Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their software offerings and gain sustainable competitive advantage.

- April 2024: Iris Software Group formed a partnership with Amazon Business to optimize procurement for UK schools. This collaboration allows 5,254 Iris customers to efficiently purchase supplies from Amazon Business using Iris Financials, the group's cloud-based school finance software.

- October 2023: Maximus UK launched the Atamis procurement software. Atamis will provide procurement software to optimize Maximus UK's sourcing processes, enhance efficiency, and reduce costs. By implementing Atamis's procurement software, Maximus UK entered a new procurement phase, focusing on streamlining operations and driving efficiencies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Global Procurement Software Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand to Automate the Procurement Processes

- 5.1.2 Integration between E-procurement Applications and ERP Solutions

- 5.1.3 Retail Industry is Expected to Hold Significant Market Share

- 5.2 Market Challenges

- 5.2.1 Complexity Regarding Integration with Existing System and Supplier Onboarding

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Manufacturing

- 6.2.3 Transportation and Logistics

- 6.2.4 Healthcare

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 SAP SE

- 7.1.2 Proactis Holdings PLC

- 7.1.3 Epicor Software Corporation

- 7.1.4 Ginesys (Ginni Systems Limited)

- 7.1.5 Coupa Software Inc.

- 7.1.6 Zycus Inc.

- 7.1.7 GT Nexus (Infor Inc.)

- 7.1.8 Ivalua Inc.

- 7.1.9 Microsoft Corporation

- 7.1.10 Oracle Corporation

- 7.1.11 Basware AS

- 7.1.12 Mercateo AG

- 7.1.13 GEP Corporation

- 7.1.14 Jaggaer Inc.