|

市場調查報告書

商品編碼

1549711

自動物料輸送(AMH):市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)Automated Material Handling (AMH) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

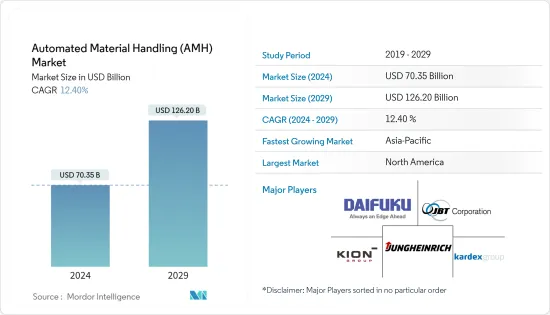

自動化物料輸送市場規模預計到2024年為703.5億美元,預計到2029年將達到1262億美元,在預測期內(2024-2029年)複合年成長率為12.40%。

主要亮點

- 技術進步、對人事費用和安全的擔憂日益增加、製造和倉儲營運效率提高、全球製造業顯著復甦、工業自動化需求增加、製造設備和倉儲設施對機器人的需求不斷成長、新興產業的成長。是推動自動化物料輸送市場的主要因素。至於其他好處,供應鏈業務的數位化將在預測期內擴大,訂單客製化和個人化的增加將進一步提振市場。

- 自動物料輸送(AMH) 系統簡化了各種環境中的物料移動,包括製造設施、倉庫、零售店、機場和物流中心。這些系統有助於材料的無縫移動,無論是在同一區域內、部門之間,甚至在不同建築物之間。 AMH 系統依賴製造執行系統 (MES) 指定的路線。這些系統採用多種技術,包括光學字元辨識 (OCR)、條碼、RFID、超寬頻室內追蹤和近距離通訊。

- 過去 70 年來,物料輸送經歷了重大變革,重塑了產業格局。機器和機器人正在取代體力勞動並刺激各個領域的成長。汽車產業尤其引人注目,成長了 10 倍,令人印象深刻。加拿大在工業 4.0 和尖端製造業方面的進步正在徹底改變不同氣候下產品的設計、交貨和維護。從機器人和自動化到積層製造(3D 列印),這些技術在電子商務、汽車、農業和製藥等廣泛領域中得到了效用。無論是在國內市場還是在競爭激烈的全球舞台上,加拿大的創新者在創造複雜、高價值的產品方面都處於領先地位。他們的工作不僅改善了當地實踐,也為合資企業奠定了基礎,定義了先進自動化技術的發展軌跡。

- 儘管第一台 AGV 於 1953 年首次亮相,但其在生產和倉儲企業中的廣泛採用卻受到多種因素的阻礙。典型的自動導引運輸車成本在 60,000 美元到 100,000 美元之間,但具有導航輔助和感測器等先進功能的系統可能要貴得多。這些高昂的初始成本加上維護挑戰正在抑制市場成長。領先的公司正在努力控制成本,同時不影響創新或研發投資。

- COVID-19 的疫情對跨部門自動化的採用產生了重大影響,重塑了業務規範並帶來了社交距離和非接觸式操作等挑戰。組織面臨需求激增和勞動力萎縮的問題,促使他們實施增強的安全通訊協定。自2020年以來,感染在美國工人中蔓延,迫使企業迅速實施新的安全措施。雖然食品製造等一些行業由於病毒的嚴重性而經歷了停工,但許多其他行業透過採取嚴格的衛生措施來維持營運。

自動物料輸送(AMH) 市場趨勢

工業4.0投資將顯著推動市場成長

- 隨著各國採用工業 4.0 和物聯網技術,市場不斷發展。透過使用機器人技術,工業 4.0 正在徹底改變物料輸送方式。機器人技術在倉庫和配送設施中變得越來越流行。例如,國際機器人聯合會報告稱,美國製造商正在大力投資自動化,到 2023 年,安裝的工業機器人數量將增加 12%,達到 44,303總合。機器人可以用來挑選和包裝訂單、裝卸卡車,甚至清潔倉庫地板。機器人提高了職場的準確性和生產力。機器人還使公司能夠透過減少所需的體力勞動來降低成本。

- 例如,倉庫很大,員工必須步行很長的距離才能找到 SKU 並將訂單交付到包裝和運輸區域。每年,倉庫平均浪費 6.9 週在不必要的步行和其他活動上,相當於 2.65 億工時,成本達 43 億美元。協作機器人還可以最大限度地減少分類過程每個階段在功能區域之間長途行走的需要。物料輸送設備訂單的增加可能會顯著推動所研究的市場。

- 此外,機器人、自動化和積層製造(3D 列印)等技術在加拿大電子商務、汽車、農業和製藥等行業有著廣泛的應用。加拿大創新者正在共同為國內和競爭激烈的全球市場生產技術複雜和高價值的產品,並共用改進的實踐並塑造高度自動化技術的未來,我們正在為即將形成的合作關係奠定基礎。

- 德國也重點關注其 2030 年工業 4.0 願景的三個策略行動領域:自主性、互通性和永續性。在這 2030 年願景中,工業 4.0 平台相關人員提出了塑造數位生態系統的整體方法。其目標是根據社會市場經濟的需求建立未來資料經濟的框架,重點是開放的生態系統、多樣性以及德國工業基礎在自動化市場和已建立的具體情況。

- 此外,政府對採購計畫的大力支持使中國能夠邁向工業 4.0。例如,中國工業機器人製造商新松隸屬於中國科學院,同時也與政府合作。各公司採用工業控制系統是該國的一個顯著趨勢。先進的系統有利於工廠生產。這也表明,依賴體力勞動的公司正在逐漸轉向基於先進技術的系統,以實現設備自動化。

- 影響所研究市場的關鍵趨勢是對智慧製造方法的關注。 IBEF資料顯示,印度政府制定了雄心勃勃的目標,到2025年將製造業對國內生產總值(GDP)的貢獻從16%提高到25%。智慧先進製造和快速轉型中心 (SAMARTH) Udyog Bharat 4.0舉措旨在提高印度製造業對工業 4.0 的認知,並使相關人員能夠應對與自動化物料輸送相關的挑戰。

亞太地區預計將成為成長最快的市場

- 中國是亞太地區 AMH 市場成長的主要貢獻者。製造業、汽車和電子商務等行業對 AMH 產品的需求不斷成長,正在推動市場成長。中國人口眾多,正在推行產業政策。過去十年,以購買力平價計算,中國已成為全球最大的經濟體,也是全球最大的出口國和貿易國。中國目前正從製造業和建設業主導經濟轉向消費主導經濟。

- 根據中國國家統計局的數據,2023年中國消費品市場零售總額約為418,605億元人民幣(57,863.1億美元)。中國的網路消費者數量從2006年的不到3,400萬迅速增加到2023年的超過9.15億,促進了中國電子商務業務的激增。因此,隨著電子商務的成長,預計幾年對物料輸送設備的需求可能會增加。

- 日本主要是一個製造業國家。日本製造業對名義GDP的貢獻接近20%,而其他已開發國家則接近10%。據國際貨幣基金組織稱,由於ICT的擴大引進,日本製造業比服務業實現了更大的工業生產力成長。汽車和電子產業是全國生產力最高的製造業。

- 在產業貢獻和「印度製造」宣傳活動的支持下,政府增加的基礎設施投資可能會推動對自動化物料輸送(AMH)系統的需求。鑑於製造業佔印度GDP的17%並僱用了超過2,730萬人,其在該國經濟狀況中的重要性是不可否認的。印度政府的願景是到2025年使製造業佔該國經濟產出的25%,因此正在實施各種措施和政策。因此,製造業正準備擁抱工業 4.0 和其他數位創新,以實現這一雄心勃勃的目標。

- 韓國已經經歷了第四次工業革命。在韓國,智慧工廠將是最重要的領域之一。在韓國,私營和公共部門都致力於增加該國智慧工廠的數量。該公司的目標雄心勃勃:到 2023 年,該公司的目標是在全國運作30,000 家最先進的工廠,配備最新的數位和分析技術。此外,還計劃在2030年建立20個智慧工業,以應對韓國勞動年齡人口的下降。作為該計劃的一部分,我們的目標是到 2030 年建立 2,000 個新的人工智慧驅動的智慧工廠,以適應第四次工業革命特徵的數位化和自動化的快速發展。

自動物料輸送(AMH) 產業概述

自動化物料輸送(AMH)市場的特點是半固化且競爭激烈。市場上的主要企業主要依靠產品推出、研發方面的大量投資以及建立合作夥伴關係和收購等策略來在激烈的競爭中生存。

- 2024 年 5 月,林德物料輸送設備的著名製造商凱傲北美公司 (KION NA) 與 Fox Robotics 建立了非排他性策略合作夥伴關係。作為合作夥伴關係的一部分,KION NA 將在其位於南卡羅來納州薩默維爾的最先進工廠製造和組裝FoxBot 的自動拖車裝卸機 (ATL)。

- 2023 年 11 月,物料輸送先驅豐田物料輸送(TMH) 宣布推出三款尖端電動堆高機機型。這些新型號進一步增強了 TMH 廣泛的物料輸送解決方案系列。這三種型號包括側入端騎車、中心騎車堆垛機和工業牽引車。這些車型承諾提高效率、多功能性和一流的性能,並專注於駕駛員的舒適度。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

- COVID-19 大流行對市場的影響

第5章市場動態

- 市場促進因素

- 技術進步不斷推動市場成長

- 工業 4.0 投資推動自動化和物料輸送的需求

- 電商領域快速成長

- 市場挑戰

- 初始設備成本高

- 缺乏技術純熟勞工

第6章 市場細分

- 依產品類型

- 硬體

- 軟體

- 服務

- 依設備類型

- 移動機器人

- 自動導引運輸車(AGV)

- 自主移動機器人(AMR)

- 自動搜尋系統

- 固定通道

- 旋轉木馬

- 垂直升降模組

- 自動輸送機

- 腰帶

- 滾筒

- 調色盤

- 開賣

- 堆垛機

- 傳統的

- 機器人

- 分類系統

- 移動機器人

- 按最終用戶

- 飛機場

- 車

- 食品/飲料

- 零售/倉庫/配送中心/物流中心

- 一般製造業

- 藥品

- 小包裹

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 亞洲

- 中國

- 日本

- 印度

- 澳洲/紐西蘭

- 拉丁美洲

- 巴西

- 墨西哥

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 北美洲

第7章 競爭格局

- 公司簡介

- Daifuku Co. Ltd

- Kardex Group

- KION Group AG

- JBT Corporation

- Jungheinrich AG

- TGW Logistics Group GmbH

- SSI Schaefer AG

- KNAPP AG

- Mecalux SA

- System Logistics SpA

- Viastore Systems GmbH

- BEUMER Group GmbH & Co. KG

- Interroll Holding AG

- WITRON Logistik

- Siemens AG

- KUKA AG

- Honeywell Intelligrated Inc.(Honeywell International Inc.)

- Murata Machinery Ltd

- Toyota Industries Corporation

- Visionnav Robotics

- Dearborn Mid-West Company

第8章投資分析

第9章市場的未來

簡介目錄

Product Code: 53959

The Automated Material Handling Market size is estimated at USD 70.35 billion in 2024, and is expected to reach USD 126.20 billion by 2029, growing at a CAGR of 12.40% during the forecast period (2024-2029).

Key Highlights

- Technological advancements, rising labor costs and safety concerns, improved efficiency in manufacturing and warehouse operations, a significant recovery in global manufacturing, increasing demand for automation in industries, growing need for robots in manufacturing units and warehousing facilities, and the growth of emerging markets are key factors driving the automated material handling market. Additionally, the market will benefit from the expanding digitization of supply chain operations, further supported by increasing order customization and personalization during the forecast period.

- Automated Material Handling (AMH) systems streamline the movement of materials across various settings, including manufacturing facilities, warehouses, retail outlets, airports, and logistics centers. These systems facilitate the seamless transfer of materials, whether within the same area, across departments, or even between distinct buildings. AMH systems rely on routes designated by the manufacturing execution system (MES). These systems employ various technologies, including optical character recognition (OCR), barcodes, RFID, ultra-wideband indoor tracking, and near-field communication.

- Over the past seven decades, material handling has undergone significant transformations, reshaping the industry's landscape. Machines and robots have largely supplanted manual labor, catalyzing growth across sectors. Notably, the automotive industry stands out, boasting a remarkable tenfold expansion. Canada's advancements in Industry 4.0 and cutting-edge manufacturing are revolutionizing product design, delivery, and maintenance, even in diverse climates. From robotics and automation to additive manufacturing (3D printing), these technologies find broad utility in sectors spanning e-commerce, automotive, agriculture, and pharmaceuticals. Canadian innovators are spearheading the creation of sophisticated, high-value products, not only for domestic markets but also for a fiercely competitive global arena. Their initiatives not only elevate local practices but also set the stage for collaborative ventures that will define the trajectory of advanced automation technologies.

- While the first AGV debuted in 1953, widespread adoption across production and warehousing firms has been hindered by various factors, with cost being a primary concern. A typical guided vehicle is priced between USD 60,000 and 100,000, but systems with advanced features like navigation aids and sensors can be considerably pricier. These high upfront costs, coupled with maintenance challenges, are dampening the market's growth. Leading firms are striving to control costs without compromising on innovation or R&D investments.

- The COVID-19 pandemic has significantly impacted the adoption of automation across sectors, reshaping operational norms and introducing challenges such as social distancing and contactless operations. Organizations faced surging demands and reduced workforces, prompting the implementation of enhanced safety protocols. Since 2020, the outbreak affected the US workers, compelling companies to adopt new safety measures swiftly. While some industries, like food production, experienced shutdowns due to the virus's severity, many others adapted by incorporating stringent health measures to sustain operations.

Automated Material Handling (AMH) Market Trends

Industry 4.0 Investments Significantly Drive the Market's Growth

- The market is driven by the developments occurring due to countries adopting Industry 4.0 and IOT technologies. Through the use of robotics, industry 4.0 is revolutionizing how material handling is done. In warehouses and distribution facilities, robotics is becoming more and more prevalent. For instance, the International Federation of Robotics reported that US manufacturers heavily invested in automation, leading to a 12% increase in industrial robot installations, totaling 44,303 units in 2023. In addition to picking and packaging orders, loading and unloading trucks, and even cleaning the warehouse floor, they can also be employed for these activities. Workplace accuracy and productivity can both be enhanced by robotics. Robots can also enable company save money by lowering the quantity of necessary manual work.

- For instance, as warehouses are huge, associates must walk considerable distances to locate SKUs and deliver orders to the packing and shipping regions. Every year, an average warehouse wastes 6.9 weeks on unnecessary walking and other movements, equating to 265 million hours of work at the cost of USD 4.3 billion. During each stage of the selection process, collaborative robots also minimize the need for extended walks between functional areas. The rise in material handling equipment orders will significantly drive the studied market.

- Moreover, robotics, automation, and technologies like additive manufacturing (3D printing) have a wide range of applications in Canadian industries such as e-commerce, automotive, agriculture, and pharmaceuticals. Canadian innovators are producing a comprehensive range of technologically complex, increased-value products for domestic and competitive global markets, sharing enhanced practices and laying the groundwork for collaborations that shape the future of advanced automation technologies.

- Germany is also focused on the 2030 vision for Industry 4.0 in three strategic fields of action: autonomy, interoperability, and sustainability. In this 2030 vision, the stakeholders of the platform Industry 4.0 present a holistic approach to shaping the digital ecosystem. The goal is to create a framework for a future data economy that is by the demands of a social market economy, emphasizing open ecosystems, diversity, and supporting competition between all market stakeholders based on the specific situation and established strengths of the German industry base for the automation market.

- Furthermore, the government's strong support in the acquisition program has enabled China to move toward Industry 4.0. For instance, Siasun, a China-based industrial robot maker, is affiliated with the Chinese Academy of Sciences, which is further linked to the government. The country's adoption of industrial control systems by various companies is a notable trend. The advanced systems allow ease of production in factories. This also points to the gradual shift of companies from depending on manual labor to advanced technology-based systems that will enable the facility's automation.

- A significant trend impacting the market studied is the focus on smart manufacturing practices. According to the data from IBEF, the Government of India set an ambitious target of increasing manufacturing output contribution to 25% of the gross domestic product (GDP) by 2025 from 16%. The Smart Advanced Manufacturing and Rapid Transformation Hub (SAMARTH) Udyog Bharat 4.0 initiative aims to enhance awareness about Industry 4.0 within the Indian manufacturing industry and enable stakeholders to address challenges related to automation material handling.

Asia-Pacific is Expected to be the Fastest Growing Market

- China has been a prominent contributor to the growth of the Asia-Pacific AMH market. The increasing demand for AMH products across industries, such as manufacturing, automotive, and e-commerce, boosts the market's growth. China has a vast population and pursues an industrial policy. Measured on the PPP basis, the country became the largest global economy and the largest global exporter and trader during the current decade. The country is currently transitioning from a manufacturing and construction-led economy to a consumer-led economy.

- According to China's National Bureau of Statistics, total retail sales in China's consumer products market were around CNY 41,860.5 billion (USD 5786.31 billion) in 2023. The number of Chinese online buyers has risen rapidly from under 34 million in 2006 to over 915 million in 2023, enabling China's e-commerce business to proliferate. Hence, with growing e-commerce, the demand for material-handling equipment will likely rise in the forecasted years.

- Japan is predominantly a manufacturing nation. Its manufacturing industry contributes close to 20% to the nominal GDP, whereas it is close to 10% for other developed countries. According to the IMF, the country's manufacturing sector has achieved significant industrial productivity gains over the services sector, owing to the increased adoption of ICT. The automotive and electronics sectors are the most productive manufacturing sectors in the country.

- The government's heightened infrastructure investments, bolstered by industry contributions and the 'Make in India' campaign, are set to propel the demand for automated material handling (AMH) systems. Given that the manufacturing sector accounts for 17% of India's GDP and employs over 27.3 million individuals, its significance in the nation's economic landscape is undeniable. With a vision to derive 25% of the economy's output from manufacturing by 2025, the Indian government is rolling out various initiatives and policies. Consequently, manufacturers are gearing up to embrace Industry 4.0 and other digital innovations to meet this ambitious goal.

- South Korea adopted the 4th Industrial Revolution. In Korea, smart factories will be one of the most important fields. Both the private and public sectors in Korea have committed to ramping up the number of domestic smart factories. Their target is ambitious: they aim to have 30,000 such cutting-edge factories equipped with the latest digital and analytical technologies up and running across the nation by 2023. Furthermore, in a bid to counteract Korea's shrinking working-age population, there are plans to establish 20 smart industrial zones by 2030. As part of this initiative, the goal is to set up 2,000 new AI-powered smart factories by 2030, aligning with the rapid pace of digitalization and automation characteristic of the fourth industrial revolution.

Automated Material Handling (AMH) Industry Overview

The automated material handling (AMH) market is characterized by semi-consolidation and high competitiveness. Key players in the market primarily rely on strategies like product launches, significant investments in R&D, and forming partnerships or making acquisitions to navigate the fierce competition.

- In May 2024, KION North America (KION NA), a prominent manufacturer of Linde Material Handling equipment, and Fox Robotics entered into a strategic non-exclusive partnership. As part of this collaboration, KION NA is expected to manufacture and assemble FoxBot autonomous trailer loader/unloaders (ATLs) at its state-of-the-art facilities in Summerville, South Carolina.

- In November 2023, Toyota Material Handling (TMH), a pioneer in material handling, unveiled three cutting-edge electric forklift models. These additions bolster TMH's already extensive range of material handling solutions. The trio includes a Side-Entry End Rider, a Center Rider Stacker, and an Industrial Tow Tractor. These models promise heightened efficiency, versatility, and top-tier performance, all while emphasizing operator comfort.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Incremental Technological Advancements aiding the Market's Growth

- 5.1.2 Industry 4.0 Investments driving the Demand for Automation and Material Handling

- 5.1.3 Rapid Growth of the E-commerce Sector

- 5.2 Market Challenges

- 5.2.1 High Initial Equipment Costs

- 5.2.2 Unavailability for Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 By Equipment Type

- 6.2.1 Mobile Robots

- 6.2.1.1 Automated Guided Vehicle (AGV)

- 6.2.1.2 Autonomous Mobile Robot (AMR)

- 6.2.2 Automated Storage and Retrieval System

- 6.2.2.1 Fixed Aisle

- 6.2.2.2 Carousel

- 6.2.2.3 Vertical Lift Module

- 6.2.3 Automated Conveyor

- 6.2.3.1 Belt

- 6.2.3.2 Roller

- 6.2.3.3 Pallet

- 6.2.3.4 Overhead

- 6.2.4 Palletizer

- 6.2.4.1 Conventional

- 6.2.4.2 Robotic

- 6.2.5 Sortation System

- 6.2.1 Mobile Robots

- 6.3 By End User

- 6.3.1 Airport

- 6.3.2 Automotive

- 6.3.3 Food And Beverages

- 6.3.4 Retail/Warehousing/Distribution Centers/Logistic Centers

- 6.3.5 General Manufacturing

- 6.3.6 Pharmaceuticals

- 6.3.7 Post and Parcel

- 6.3.8 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 France

- 6.4.2.3 Italy

- 6.4.2.4 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Mexico

- 6.4.6 Middle East and Africa

- 6.4.6.1 United Arab Emirates

- 6.4.6.2 Saudi Arabia

- 6.4.6.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daifuku Co. Ltd

- 7.1.2 Kardex Group

- 7.1.3 KION Group AG

- 7.1.4 JBT Corporation

- 7.1.5 Jungheinrich AG

- 7.1.6 TGW Logistics Group GmbH

- 7.1.7 SSI Schaefer AG

- 7.1.8 KNAPP AG

- 7.1.9 Mecalux SA

- 7.1.10 System Logistics SpA

- 7.1.11 Viastore Systems GmbH

- 7.1.12 BEUMER Group GmbH & Co. KG

- 7.1.13 Interroll Holding AG

- 7.1.14 WITRON Logistik

- 7.1.15 Siemens AG

- 7.1.16 KUKA AG

- 7.1.17 Honeywell Intelligrated Inc. (Honeywell International Inc.)

- 7.1.18 Murata Machinery Ltd

- 7.1.19 Toyota Industries Corporation

- 7.1.20 Visionnav Robotics

- 7.1.21 Dearborn Mid-West Company

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

到 2030 年自動物料輸送設備市場預測:按產品類型、系統類型、最終用戶、分銷管道和地區進行的全球分析

到 2030 年自動物料輸送設備市場預測:按產品類型、系統類型、最終用戶、分銷管道和地區進行的全球分析 自動化物料輸送市場:按組件、操作、設備類型、應用分類 - 2025-2030 年全球預測

自動化物料輸送市場:按組件、操作、設備類型、應用分類 - 2025-2030 年全球預測 自動物料輸送設備市場:按產品、應用和最終用戶分類 - 全球預測 2025-2030

自動物料輸送設備市場:按產品、應用和最終用戶分類 - 全球預測 2025-2030 歐洲資源回收設施 (MRF) 的成長機會

歐洲資源回收設施 (MRF) 的成長機會 自動化物料輸送市場 – 2024 年至 2029 年預測

自動化物料輸送市場 – 2024 年至 2029 年預測 全球自動化物料輸送(AMH) 市場,2024-2028

全球自動化物料輸送(AMH) 市場,2024-2028 2024-2032 年按組件、產品、功能、系統類型、最終用途產業和地區分類的自動化物料搬運設備市場

2024-2032 年按組件、產品、功能、系統類型、最終用途產業和地區分類的自動化物料搬運設備市場 自動物料輸送設備市場規模、佔有率和趨勢分析報告:按產品、系統類型、產業、地區和細分市場預測,2024-2030

自動物料輸送設備市場規模、佔有率和趨勢分析報告:按產品、系統類型、產業、地區和細分市場預測,2024-2030 自動物料搬運設備市場規模 - 按產品(自動導引車、機器人、自動儲存和檢索系統、輸送機和分類系統)、應用、最終用途和預測,2024 - 2032

自動物料搬運設備市場規模 - 按產品(自動導引車、機器人、自動儲存和檢索系統、輸送機和分類系統)、應用、最終用途和預測,2024 - 2032 自動物料輸送設備 (AMHE) 的全球市場:按產品(AMR、協作堆垛機、AS/RS、輸送機系統、倉庫管理系統、AGV)和地區 - 預測(截至 2029 年)

自動物料輸送設備 (AMHE) 的全球市場:按產品(AMR、協作堆垛機、AS/RS、輸送機系統、倉庫管理系統、AGV)和地區 - 預測(截至 2029 年)

▼