|

市場調查報告書

商品編碼

1687119

銦鎵氧化鋅:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Indium Gallium Zinc Oxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

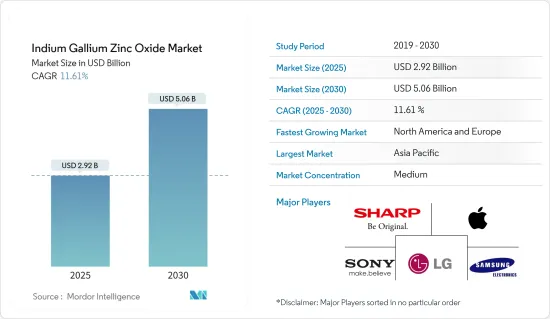

預計 2025 年銦鎵氧化鋅市場規模為 29.2 億美元,到 2030 年將達到 50.6 億美元,預測期間(2025-2030 年)的複合年成長率為 11.61%。

主要亮點

- 由於銦鎵鋅氧化材料 (IGZO) 比傳統矽基材料具有更優異的性能,電子產業擴大採用它。 IGZO 主要用於 LCD 和 OLED 顯示器的薄膜電晶體 (TFT)。 IGZO 的高電子遷移率可實現更快的切換速度和更高的解析度,使其成為高清電視、智慧型手機和平板裝置的首選材料。對先進顯示器的需求不斷成長是 IGZO 市場發展的主要驅動力。

- IGZO 的一大獨特優勢是它能夠以低功耗實現高效能,這對於電池壽命至關重要的攜帶式電子設備來說極為重要。透過降低功耗,IGZO 顯著延長了電池壽命,為製造商和消費者提供了引人注目的價值提案。此外,IGZO的透明度和靈活性使其成為折疊式和旋轉性螢幕等新型顯示類型的理想選擇,使其在市場上越來越受歡迎。

- 此外,小型化趨勢和對更高效電子元件的需求正在塑造 IGZO 市場。 IGZO的高電子遷移率使得能夠製造更小、更有效率的電晶體,從而促進開發更智慧、更輕的電子產品以滿足消費者的偏好。此外,隨著物聯網設備變得越來越普遍並且需要更有效率、更緊湊的組件,對 IGZO 材料的需求預計將會成長。

- IGZO市場面臨生產成本高、需要先進製造流程等挑戰,但正在進行的研究和開發重點是提高效率和降低成本。此外,來自低溫多晶矽(LTPS)和有機半導體等替代品的競爭也是一個問題。然而,IGZO 的獨特特性和不斷擴大的應用範圍使其成為顯示器和電子產品發展的關鍵材料。在技術進步和不斷成長的消費者需求的推動下,IGZO 市場預計將持續成長。

銦鎵氧化鋅市場趨勢

穿戴式裝置市場佔有率將大幅增加

- 銦鎵鋅氧化 (IGZO) 因其獨特的性能滿足現代穿戴式技術的嚴格要求,正在成為穿戴式裝置市場的關鍵組成部分。 IGZO 的高電子遷移率和低功耗對於開發高解析度、節能顯示器至關重要,對於智慧型手錶、健身追蹤器和 AR 眼鏡等設備至關重要。隨著這些設備的進步和對性能的要求越來越高,IGZO 在其發展中變得越來越重要。

- IGZO 能夠支援高解析度顯示,同時保持低功耗,這是穿戴式裝置的關鍵優勢。鑑於穿戴式裝置的電池容量有限,提高能源效率可顯著延長電池壽命。 IGZO 電晶體運轉時耗電量極小,可節省電池壽命,同時不影響顯示品質。對於希望實現高效能穿戴裝置且每次充電可使用較長時間的製造商而言,IGZO 是一個相當吸引人的選擇。

- 除了電源效率之外,IGZO 的靈活性和透明度也為穿戴式裝置帶來了顯著的優勢。穿戴式裝置需要輕巧、耐用且足夠靈活,以適應各種形狀和尺寸。 IGZO 的靈活性使得可以創建可彎曲和折疊的顯示器,從而增強用戶體驗並為穿戴式技術開闢了新的設計可能性。此外,它的透明度可以用來開發創新的顯示解決方案,例如用於 AR 眼鏡的透明螢幕,提供無縫且身臨其境的使用者體驗。

- 消費者對先進穿戴技術的需求不斷成長,推動了 IGZO 市場的發展。隨著消費者要求穿戴式裝置具有更多功能和更好性能,製造商擴大採用 IGZO 來滿足這些期望。更高解析度的顯示器、更靈敏的觸控螢幕和更長的電池壽命等功能正在成為穿戴式裝置的標準,而 IGZO 的特性對於實現這些增強功能至關重要。此外,將健康監測、健身追蹤和連接選項整合到穿戴式裝置中將進一步需要使用像 IGZO 這樣的高效能、高性能材料。

- 物聯網 (IoT) 的普及以及醫療保健、健身和娛樂等各行業中穿戴式裝置的日益普及,預計將推動對 IGZO 的需求。根據國際數據公司 (IDC) 的《印度月度穿戴裝置追蹤報告》,印度穿戴式裝置市場預計將在 2023 年成長 34%,達到創紀錄的 1.342 億台。 2023年第四季(10-12月),銷量較去年同期成長12.7%至2,840萬台。

- 穿戴式裝置不僅用於個人健康管理,也用於醫療監測和工業用途等專業應用。 IGZO 支援先進顯示技術和低功耗操作的能力使其成為下一代穿戴式裝置開發的重要元素。隨著這一趨勢的持續,穿戴式裝置預計將佔據 IGZO 市場的巨大佔有率,從而推動行業創新和成長。

亞太地區將成為成長最快的市場

- 以中國、日本和韓國等國家為主導的亞太地區可能會主導銦鎵鋅氧化 (IGZO) 市場。這些國家擁有強大的電子製造業,並以快速的技術進步而聞名。尤其是,它是世界上一些最大的消費性電子產品和顯示面板生產商的所在地。憑藉強大的工業基礎和對研發 (R&D) 的投入,這些國家成為全球 IGZO 領域的重要參與者。Sharp Corporation、LG 和三星等產業巨頭正在大力投資 IGZO 技術,以完善產品系列確保競爭優勢。

- 中國擁有龐大的電子製造業,成為亞太地區 IGZO 市場的主要企業。中國致力於推動顯示技術的發展,並大規模投資於IGZO生產設施。中國製造商擴大轉向 IGZO,因為他們認知到其在薄膜電晶體 (TFT) 中的卓越性能,而薄膜電晶體 (TFT) 對於高畫質電視、智慧型手機和其他消費性電子產品至關重要。如此廣泛的採用可能會進一步鞏固中國在 IGZO 市場的主導地位。

- 日本以其技術力實力而聞名,是亞太地區 IGZO 市場的主要貢獻者。值得注意的是,Sharp Corporation等公司一直處於 IGZO 技術的前沿,為高效能、節能顯示器樹立了標竿。日本注重研發,加上其生產頂級電子元件的聲譽,使其牢牢確立了其作為 IGZO 市場領導者的地位,推動了國內和全球的需求。

- 韓國是三星和 LG 等科技巨頭的所在地,也是 IGZO 市場的另一個主要參與者。這些公司處於顯示技術的前沿,將IGZO融入其尖端產品中。三星的折疊式和可捲曲顯示器的突破,以及 LG 的 OLED 創新,充分利用了 IGZO 的高電子遷移率和能源效率等特性。韓國對技術創新和嚴格製造標準的承諾進一步鞏固了其在 IGZO 市場的關鍵地位。

- 積極的政府政策鞏固了IGZO在亞太地區的主導地位。中國、日本和韓國等國家正透過研發資金、基礎建設和技術採用補貼等方式積極支持其電子產業。這些舉措不僅刺激了本地製造商對 IGZO 的投資,也鼓勵了其在各種應用中的應用。因此,亞太地區不僅成為IGZO的主要生產地,也成為重要的消費地,鞏固了其全球市場佔有率。

銦鎵氧化鋅產業概況

受使用銦鎵氧化鋅的新技術創新的推動,銦鎵氧化鋅市場呈現中度分散。隨著企業努力開發先進的應用並提高產品性能,這項技術創新正在加劇市場競爭。主要參與者正致力於研究和開發,以提高銦鎵氧化鋅在顯示面板、太陽能電池和感測器等各種應用中的效率和功能。此外,隨著企業尋求加強其市場地位和擴大產品系列,策略聯盟和合作變得越來越普遍。

- 2024 年 4 月,LTPO(低溫多晶氧化物)背板技術領先的蘋果進一步創新,採用 IGZO(銦鎵鋅氧化物)來驅動薄膜電晶體(TFT)。此策略改進旨在提高 LTPO 顯示器的效率,LTPO 顯示器的特點是節能和可變更新率。

- 2024 年 3 月,優派繼推出 XG272-2K-OLED 之後,又推出了最新遊戲顯示器 VX2781-4K-PRO-6。 XG272-2K-OLED 具有 2.5K 解析度和 240Hz 的有機發光二極體面板。 ViewSonic 聲稱 VX2781-4K-PRO-6 是世界上第一款採用 IGZO(銦鎵鋅氧化)和 IPS 面板的 27 吋 4K 顯示器的創新產品,可提供 165Hz 的更新率。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

- 研究框架

- 二次調查

- 主要研究方法及主要受訪者

- 資料三角測量與洞察生成

第3章執行摘要

第4章 市場動態

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 技術簡介

- 市場促進因素

- 高解析度技術的進步

- 重視節能技術

- 市場限制

- 低溫多晶(LTPS) 等競爭對手

- COVID-19 產業影響評估

第5章 市場區隔

- 按應用

- 智慧型手機

- 穿戴式裝置

- 壁掛式展示架

- 電視機

- 平板電腦、筆記本、筆記型電腦

- 其他用途

- 按最終用戶

- 車

- 家電

- 衛生保健

- 產業

- 其他最終用戶

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第6章 競爭格局

- 公司簡介

- Sharp Corporation

- Apple Inc.

- Sony Corporation

- ASUSTEK Computer Inc.

- LG Electronics

- AU Optronics

- Samsung Electronics Co. Ltd

- Fujitsu Limited

第7章 投資分析及未來趨勢

- 投資分析

- 市場的未來

The Indium Gallium Zinc Oxide Market size is estimated at USD 2.92 billion in 2025, and is expected to reach USD 5.06 billion by 2030, at a CAGR of 11.61% during the forecast period (2025-2030).

Key Highlights

- The electronics industry is increasingly adopting indium gallium zinc oxide (IGZO) over traditional silicon-based materials, driven by its superior performance. IGZO is primarily utilized in thin-film transistors (TFTs) for LCD and OLED displays. With its high electron mobility, IGZO enables faster switching speeds and higher resolutions, making it a preferred choice for HD TVs, smartphones, and tablets. The rising demand for advanced displays is a key driver for the IGZO market.

- One notable advantage of IGZO is its ability to deliver high performance at lower power consumption, which is crucial for portable electronics where battery life is critical. By reducing power usage, IGZO displays a significantly extended battery life, presenting a compelling value proposition for both manufacturers and consumers. Additionally, IGZO's transparency and flexibility are ideal for emerging display types like foldable and rollable screens, which are gaining traction in the market.

- Moreover, the trend toward miniaturization and the need for more efficient electronic components are shaping the IGZO market. Thanks to its high electron mobility, IGZO enables the creation of smaller, more efficient transistors, facilitating the development of sleeker and lighter electronic devices, aligning with consumer preferences. Furthermore, as the adoption of IoT devices increases, demanding efficient and compact components, the demand for IGZO materials is expected to rise.

- While the IGZO market faces challenges such as high production costs and the need for sophisticated manufacturing processes, ongoing R&D efforts are focused on enhancing efficiency and reducing costs. Additionally, competition from alternatives like low-temperature polysilicon (LTPS) and organic semiconductors poses a challenge. However, given its unique properties and expanding applications, IGZO is solidifying its role as a pivotal material in the evolution of displays and electronic devices. With technological advancements and rising consumer demand, the IGZO market is poised for sustained growth.

Indium Gallium Zinc Oxide Market Trends

Wearable Devices to Gain a Significant Market Share

- Indium gallium zinc oxide (IGZO) is emerging as a critical component in the wearable devices market, driven by its unique properties that meet the stringent requirements of contemporary wearable technology. IGZO's high electron mobility and low power consumption make it indispensable for developing high-resolution, energy-efficient displays that are essential for devices such as smartwatches, fitness trackers, and AR glasses. As these devices advance and demand higher performance, IGZO's significance in their development becomes increasingly crucial.

- IGZO's ability to support high-resolution displays while maintaining low power consumption is a key advantage for wearable devices. Given the limited battery capacity of wearables, improvements in energy efficiency can significantly extend battery life. IGZO transistors operate with minimal power, conserving battery life without compromising display quality. This makes IGZO an attractive option for manufacturers aiming to deliver high-performance wearables with longer operational periods between charges.

- In addition to power efficiency, IGZO's flexibility and transparency offer substantial benefits for wearable devices. Wearables need to be lightweight, durable, and often flexible to conform to various shapes and sizes. IGZO's flexibility allows for the creation of bendable and foldable displays, enhancing user experience and opening new design possibilities for wearable technology. Moreover, its transparency can be utilized in developing innovative display solutions, such as transparent screens in AR glasses, providing a seamless and immersive user experience.

- Increasing consumer demand for advanced wearable technology is driving the IGZO market. As consumers seek more functionality and better performance from their wearable devices, manufacturers are increasingly adopting IGZO to meet these expectations. Features such as high-definition displays, responsive touchscreens, and extended battery life are becoming standard in wearables, with IGZO's properties being crucial in achieving these enhancements. Additionally, the integration of health monitoring, fitness tracking, and connectivity options in wearables further necessitates the use of efficient and high-performing materials like IGZO.

- The proliferation of the Internet of Things (IoT) and the growing adoption of wearables across various industries, including healthcare, fitness, and entertainment, are expected to boost demand for IGZOs. International Data Corporation's (IDC) India Monthly Wearable Device Tracker reported that the Indian wearable market experienced a 34% growth in 2023, reaching a record 134.2 million units. In the fourth quarter of 2023 (October-December), the market recorded 28.4 million units, reflecting a 12.7% Y-o-Y increase.

- Wearable devices are not only used for personal health tracking but also for professional applications in medical monitoring and industrial use. IGZO's capability to support advanced display technologies and low-power operations makes it a vital component in developing the next generation of wearables. As this trend continues, wearable devices are set to capture a significant share of the IGZO market, driving innovation and growth in the industry.

Asia-Pacific to Witness the Fastest Market Growth

- The Asia-Pacific regional segment, led by countries such as China, Japan, and South Korea, is poised to dominate the indium gallium zinc oxide (IGZO) market. These nations boast robust electronic manufacturing industries and are renowned for their rapid technological advancements. Notably, they house some of the world's largest producers of consumer electronics and display panels. With strong industrial bases and a keen focus on research and development (R&D), these countries are pivotal players in the global IGZO landscape. Major industry players like Sharp, LG, and Samsung are channeling significant investments into IGZO technology to elevate their product portfolios and secure a competitive advantage.

- With its mammoth electronics manufacturing industry, China stands out as a key player in the Asia-Pacific IGZO market. The nation's commitment to advancing display technology has translated into substantial investments in IGZO production facilities. Chinese manufacturers increasingly turn to IGZO, recognizing its superior performance in thin-film transistors (TFTs) - crucial components in high-definition televisions, smartphones, and other consumer electronics. This widespread adoption is poised to further solidify China's dominance in the IGZO market.

- Japan, renowned for its technological prowess, is a significant contributor to the Asia-Pacific IGZO market. Notably, companies like Sharp have been at the forefront of IGZO technology, setting benchmarks for high-performance, energy-efficient displays. Japan's emphasis on R&D, coupled with its reputation for producing top-tier electronic components, cements its position as an IGZO market leader, driving both local and global demand.

- South Korea, home to tech giants like Samsung and LG, is another linchpin in the IGZO market. These companies are at the vanguard of display technology, integrating IGZO into their cutting-edge products. Samsung's strides in foldable and rollable displays, alongside LG's OLED innovations, heavily leverage IGZO's attributes, such as high electron mobility and energy efficiency. South Korea's commitment to innovation and stringent manufacturing standards further solidify its significant role in the IGZO market.

- The Asia-Pacific's IGZO dominance is bolstered by proactive government policies. Nations like China, Japan, and South Korea are actively supporting the electronics industry through R&D funding, infrastructure development, and technology adoption incentives. These initiatives not only spur local manufacturers to invest in IGZO but also drive its adoption across diverse applications. Consequently, the Asia-Pacific regional segment emerges not just as a major IGZO producer but also as a substantial consumer, underlining its global market share.

Indium Gallium Zinc Oxide Industry Overview

The indium gallium zinc oxide market exhibits moderate fragmentation, driven by players innovating with new technologies using indium gallium zinc oxide. This innovation is intensifying market competition as companies strive to develop advanced applications and improve product performance. Key players are focusing on research and development to enhance the efficiency and functionality of indium gallium zinc oxide in various applications, including display panels, solar cells, and sensors. Additionally, strategic partnerships and collaborations are becoming common as companies aim to strengthen their market position and expand their product portfolios.

- In April 2024, Apple, a leader in LTPO (low-temperature polycrystalline oxide) backplane technology, further innovated by incorporating IGZO (indium gallium zinc oxide) into driving thin-film transistors (TFTs). This strategic enhancement aims to improve the efficiency of LTPO displays, which are distinguished by their energy-saving features and variable refresh rates.

- In March 2024, ViewSonic launched its latest gaming monitor, the VX2781-4K-PRO-6, following the introduction of the XG272-2K-OLED. The XG272-2K-OLED features a 2.5K resolution and a 240 Hz OLED panel. ViewSonic claimed the VX2781-4K-PRO-6 to be a world-first innovation with its 27-inch, 4K display utilizing an IGZO (indium gallium zinc oxide) and IPS panel, offering a 165 Hz refresh rate.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research Approach and Key Respondents

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Market Drivers

- 4.4.1 Advancements in High Resolution Technologies

- 4.4.2 Emphasis on Energy-saving Technology

- 4.5 Market Restraints

- 4.5.1 Competitors, Such as Low-temperature Polycrystalline Silicon (LTPS)

- 4.6 Assessment of the Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Smartphones

- 5.1.2 Wearable Devices

- 5.1.3 Wall-mounted Displays

- 5.1.4 Televisions

- 5.1.5 Tablets, Notebooks, and Laptops

- 5.1.6 Other Appplications

- 5.2 By End User

- 5.2.1 Automotive

- 5.2.2 Consumer Electronics

- 5.2.3 Healthcare

- 5.2.4 Industrial

- 5.2.5 Other End Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Sharp Corporation

- 6.1.2 Apple Inc.

- 6.1.3 Sony Corporation

- 6.1.4 ASUSTEK Computer Inc.

- 6.1.5 LG Electronics

- 6.1.6 AU Optronics

- 6.1.7 Samsung Electronics Co. Ltd

- 6.1.8 Fujitsu Limited

7 INVESTMENT ANALYSIS AND FUTURE TRENDS

- 7.1 Investment Analysis

- 7.2 Future of the Market

2025年全球超快雷射圖形化顯示器市場報告

2025年全球超快雷射圖形化顯示器市場報告 採用量子點薄膜的新型顯示器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

採用量子點薄膜的新型顯示器:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 鈣鈦礦量子點顯示應用市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)銦鎵鋅氧化物(IGZO):全球市場佔有率和排名、總收入和需求預測(2025-2031年)

鈣鈦礦量子點顯示應用市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)銦鎵鋅氧化物(IGZO):全球市場佔有率和排名、總收入和需求預測(2025-2031年) IGZO市場按應用、裝置類型、終端用戶產業、沉澱方法、基材、厚度和遷移率範圍分類-全球預測,2025-2032年下一代顯示材料市場按應用和材料類型分類 - 全球預測(2025-2032)

IGZO市場按應用、裝置類型、終端用戶產業、沉澱方法、基材、厚度和遷移率範圍分類-全球預測,2025-2032年下一代顯示材料市場按應用和材料類型分類 - 全球預測(2025-2032) 全球顯示材料市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年)

全球顯示材料市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年) 透明電極的全球市場顯示材料市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

透明電極的全球市場顯示材料市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 IGZO 輪調目標市場報告:到 2030 年的趨勢、預測和競爭分析

IGZO 輪調目標市場報告:到 2030 年的趨勢、預測和競爭分析