|

市場調查報告書

商品編碼

1549724

PLM 軟體:市場佔有率分析、產業趨勢/統計、成長預測 (2024-2029)PLM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

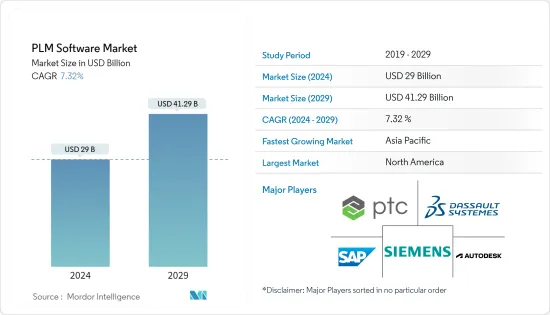

PLM 軟體市場規模預計到 2024 年將達到 290 億美元,預計到 2029 年將達到 412.9 億美元,在預測期內(2024-2029 年)複合年成長率為 7.32%。

預計 2024 年 PLM 軟體市場規模將達 290 億美元。由於產業對強大資料分析軟體平台的需求不斷成長,預計到2029年將達到412.9億美元,預測期內(2024-2029年)複合年成長率為7.32%。此外,整個製造業也擴大採用物聯網也支持了這些趨勢。 PTC 的 Windchill 是 PLM 軟體的一個範例,該軟體具有內建分析功能,適合尋求 IoT 功能的離散製造商。該軟體可以提高 PLM 解決方案的靈活性。

主要亮點

- 各行業的公司越來越注重簡化產品開發流程,以提高效率並加速創新。 PLM 軟體使公司能夠管理整個產品生命週期,從構思到處置再到效率,市場需求量很大。

- 隨著全球營運和團隊分佈在多個地點,對促進通訊和資料共用的協作工具的需求不斷增加。 PLM 軟體提供了一個集中式平台,團隊可以在其中無縫協作,無論其地理位置為何。

- 生產過程中工業IoT(IIoT) 的日益普及正在推動市場對軟體應用程式的需求,預計在預測期內 IIoT 的採用將會激增。例如,根據 GSMA Intelligence 的數據,到 2025 年,IIoT 連線物件的數量預計將達到 137 億個。

- 然而,隨著公司不斷提供不同的產品和產品系列來參與市場競爭,互通性問題就會出現,需要軟體公司不斷最佳化。軟體產品的持續改進使得將軟體實施到公司現有的產品系列中更加精簡、更易於管理,並且更有可能產生更好的結果。

- 許多製造業受到了 COVID-19 大流行的影響,導致供應鏈出現嚴重缺口和延誤。這迫使許多產業加速實施工業4.0和數位轉型,增加了對PLM軟體的需求以提高必要的成長率。疫情後軟體採用的增加也推動了市場的成長。

PLM軟體市場趨勢

自動駕駛汽車產量的增加推動市場成長

- 隨著自動駕駛汽車變得越來越普遍,自動駕駛汽車的開發人員面臨越來越複雜的挑戰。克服這些挑戰需要重新評估現有流程和工具集。因此,對有助於克服這些挑戰的解決方案的需求不斷成長,這推動了市場的指數成長。

- 此外,功能齊全的自動駕駛系統結合了各種資料饋送,包括來自感測器的資訊、來自雲端的交通資料以及來自其他基礎設施和車輛的資料,所有這些都連接到車輛的機械和電子系統以連接組件。

- 此外,整合的ALM(應用程式生命週期管理)和codeBeamer ALM 等產品開發平台可以幫助克服自動駕駛汽車領域產品複雜性增加和對高級軟體應用程式依賴增加的挑戰,將在開發流程現代化方面發揮重要作用。

- 數位化製造使用的增加和自動駕駛汽車需求的增加是預測期內推動汽車 PLM 軟體市場的主要趨勢。

北美佔有很大佔有率

- 北美強大的金融基礎使其能夠進行大規模投資,特別是在先進技術和解決方案方面,使其在市場競爭中具有優勢。此外,該地區還擁有幾家主要的產品生命週期管理軟體供應商,包括 IBM 公司、PTC 公司和 Oracle 公司。因此,市場競爭異常激烈。

- 整個北美汽車工業正在快速成長。 PLM 軟體主要在產品開發階段使用,在汽車產業中,這個階段早在製造開始之前就開始了。 PLM 軟體可確保車輛的先進安全功能、電子設備和內建軟體內容。因此,隨著該地區汽車行業的崛起,預計該市場在整個預測期內將享受各種利潤豐厚的成長機會。

- 其他製造業和市場正在探索實施 PLM 軟體的好處,以增強其製造和生產流程。例如,2023 年 4 月,西門子和微軟將利用生成人工智慧的集體協作力量,幫助工業公司提高其產品的工程、設計、製造和營運生命週期的效率和創新。為了加強跨職能協作,兩家公司還致力於將西門子的 Teamcenter 產品生命週期管理軟體與微軟的 Teams 協作平台、Azure OpenAI 服務的語言模型以及各種其他 Azure AI 功能整合。

- 例如,PTC 宣布推出 Onshape-Arena Connection,這是一項新功能,可連接其主要雲端原生的 Onshape 產品開發解決方案和 Arena 產品生命週期管理解決方案。這種連接使公司只需單擊按鈕即可在 Arena 和 Onshape 解決方案之間即時共用產品資料,從而幫助公司增強產品開發流程並簡化與供應鏈合作夥伴的協作。

- 此類合作強化了整體市場格局,並激勵其他競爭對手和供應商啟用 PLM 軟體,從而塑造了龐大的 PLM 實施的整個北美市場。因此,透過產品供應鏈多個方面的徹底實施,正在積極支持北美企業不斷發展的工業4.0趨勢。

PLM 軟體市場產業概況

產品生命週期管理 (PLM) 軟體市場高度分散且競爭激烈,這主要是由於存在許多全球參與者。各市場參與者充分利用最新的軟體技術進行研發,在市場上建立了較高的競爭力。主要參與者包括 Dassault Systemes Deutschland GmbH、Siemens、Autodesk Inc.、ANSYS Inc. 和 Infor Inc.。公司透過建立各種合作夥伴關係、投資計劃以及向市場推出新產品來最大化市場佔有率。

- 2023 年 2 月,Hexagon 旗下公司、全球協作和設計解決方案提供商 Bricsys 宣布與 MechWorks(ITI Technegroup 旗下子公司,WIPRO 旗下子公司)建立合作夥伴關係,提供西門子 Teamcenter 軟體與 BricsCAD 的整合。此解決方案主要提供一流的功能,以更快地連接 BricsCAD 流程,並使設計人員能夠專注於產品開發。

- 2023 年 10 月,主要企業PTC 宣布收購專門從事產品和軟體變體管理的德國軟體公司 Pure-systems。正如 Pure-systems 網站上的免責聲明所述,收購已經發生。此次收購為 PTC 的產品組合增添了 pure::variants,這是一種幫助工程師和產品設計師管理產品和軟體變化的工具。 PTC 和 pure-systems 先前合作將 pure::variants 整合到 PTC 的應用程式生命週期管理 (ALM) 軟體 Codebeamer 中。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- COVID-19 對產品生命週期管理軟體市場的影響

第5章市場動態

- 市場促進因素

- 引入數位化以提高生產力

- 資訊集中雲端技術簡介

- 市場限制因素

- 不同產品版本之間缺乏互通性

第6章 市場細分

- 依部署類型

- 本地

- 雲

- 專業服務

- 按最終用戶產業

- 電子、工業設備、高科技

- 航太/國防

- 車

- 架構、工程與施工 (AEC)

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 其他亞太地區

- 拉丁美洲

- 中東/非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- Siemens AG

- Dassault Systems Deutschland GmbH

- Autodesk Inc.

- PTC Inc.

- SAP SE

- ANSYS Germany GmbH

- Oracle Corporation

- Aras Corporation

- Arena Solutions

- Infor Inc.

第8章投資分析

第9章市場的未來

The PLM Software Market size is estimated at USD 29 billion in 2024, and is expected to reach USD 41.29 billion by 2029, growing at a CAGR of 7.32% during the forecast period (2024-2029).

The PLM software market size is estimated to account for USD 29 billion in 2024. It is expected to reach USD 41.29 billion by 2029, registering a CAGR of 7.32% during the forecast period (2024-2029), owing to the growing demand for robust data analytics software platforms in the industry. Moreover, the increasing adoption of IoT across the manufacturing industry has augmented these trends. PTC's Windchill is an instance of the PLM software embedded with analytics for discrete manufacturers looking for IoT capabilities. This software can boost the PLM solution to sprint with flexibility.

Key Highlights

- Companies across industries are increasingly focused on streamlining their product development processes to improve efficiency and accelerate innovation. PLM software enables organizations to manage the entire product lifestyle, from ideation to disposal and efficiency, thereby increasing the demand in the market.

- With businesses operating on a global scale and teams dispersed across various locations, there is a growing need for collaboration tools that facilitate communication and data sharing. PLM software provides a centralized platform for teams to collaborate seamlessly regardless of geographic location.

- The increased adoption of Industrial IoT (IIoT) in the production process is aiding the market demand for software applications, and IIoT adoption is expected to skyrocket during the forecast period. For instance, according to GSMA Intelligence, the number of IIoT-connected objects is expected to reach 13.7 billion by 2025.

- However, as the companies continue to provide different products and product ranges to tackle market competitiveness, it creates interoperability issues, a matter of constant optimization for the software companies. As continuous improvements continue in the software products, the software implementation in a company's existing product line-up becomes streamlined and manageable, facilitating better results.

- Many manufacturing industries were affected by the COVID-19 pandemic, creating significant supply chain gaps and leading to delays. This forced many industries to hasten the adoption of Industry 4.0 and digital transformation initiatives, boosting the demand for PLM software to bolster the required growth rates. The increased software penetration after the pandemic has boosted market growth.

PLM Software Market Trends

Increasing Production of Autonomous Vehicles to Drive Market Growth

- As the use of autonomous vehicles becomes more widespread, the developers working on these vehicles are encountering increasingly complex challenges. To overcome these challenges, they need to re-evaluate their existing processes and toolsets. This has led to a rising demand for solutions that can help them overcome these challenges, which is fueling the market's growth exponentially.

- Moreover, the fully functional autonomous driving systems need some of the most complex and sophisticated software implementations that carmakers have ever faced for combining a variety of data feeds, like information from sensors, traffic data from the cloud, data coming from other infrastructure or vehicles, and tying it all into the automobiles's mechanical and electronic components to create a vast network of onboard systems that all work together reliably without the need for user input or correction.

- Furthermore, integrated ALM (application lifecycle management) and product development platforms, such as codeBeamer ALM, will play a significant role in modernizing development processes to overcome the challenges posed by the growing complexity of products and the increasing dependence on sophisticated software applications in the autonomous vehicle sector.

- The rising usage of digital manufacturing and the increasing demand for autonomous cars are key trends that are expected to drive the PLM software market in the automotive sector during the forecast period.

North America to Account for a Significant Share

- North America's strong financial position allows it to invest massively, especially in advanced technologies and solutions that have offered a strong competitive edge within the market. Moreover, the region has a robust presence of several significant product lifecycle management software vendors like IBM Corp., PTC Inc., and Oracle Corporation. Hence, there lies intense competition among the market players.

- The entire automotive industry in North America is growing at a rapid pace. PLM software is primarily utilized in the product development stage, which starts long before manufacturing begins in the automotive industry. It ensures the vehicles' advanced safety features, electronics, and embedded software content. Hence, with the rise in the automotive industry within the region, the market is expected to have various lucrative growth opportunities throughout the forecast period.

- Other manufacturing industries and markets explore the benefits of deploying PLM software to augment manufacturing and production processes. For instance, in April 2023, Siemens and Microsoft harnessed the overall collaborative power of generative artificial intelligence mainly to help industrial companies drive efficiency and innovation across the engineering, design, manufacturing, and operational lifecycle of the products. Also, to enhance cross-functional collaboration, the companies are focused on integrating Siemens' Teamcenter software for product lifecycle management with Microsoft's collaboration platform, Teams, and its language models in Azure OpenAI Service, as well as various other Azure AI capabilities.

- For instance, PTC declared the availability of the Onshape-Arena Connection, a new functionality that mainly connected its cloud-native Onshape product development and Arena product lifecycle management solutions. The connection allowed the product data to be shared instantly between the Arena and Onshape solutions with the single click of a button, assisting the companies in augmenting the product development process and simplifying collaboration with the supply chain partners.

- Such collaborations enhance the entire market scenario, stimulating other competitors and vendors to enable PLM software and shaping the whole North American market for vast PLM implementation. Hence, the in-depth implementation throughout several aspects of the product supply chain is actively helping North American businesses with the evolving Industry 4.0 trends.

PLM Software Market Industry Overview

The product lifecycle management (PLM) software market is highly fragmented and competitive, mainly due to the presence of numerous global players. Various market players are moving in R&D with the latest software techniques, building a high level of competitiveness throughout the market. The key players include Dassault Systemes Deutschland GmbH, Siemens, Autodesk Inc., ANSYS Inc., and Infor Inc. The companies are thus maximizing their market share by forming various partnerships, investing in projects, and introducing new products in the market.

- In February 2023, global provider of collaboration and design solutions Bricsys, part of Hexagon, declared its partnership with MechWorks, part of ITI Technegroup, a WIPRO company, to offer an integration between Siemens' Teamcenter software and BricsCAD. The solution primarily provides industry-best features to connect BricsCAD's processes faster and enable designers to focus on its product development.

- In October 2023, PTC, a leading engineering software and PLM provider, announced its acquisition of pure-systems, a German software company that specializes in product and software variant management. The acquisition had already taken place, as indicated by the disclaimer on pure-systems' website. The acquisition will bring pure::variants, a tool designed to help engineers and product designers manage product and software variation, to PTC's portfolio. PTC and pure-systems had previously partnered to integrate pure::variants into PTC's Codebeamer application lifecycle management (ALM) software.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Product Lifecycle Management Software Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Digitalization to Improve Production

- 5.1.2 Introduction of Cloud Technology to Consolidate the Information

- 5.2 Market Restraints

- 5.2.1 Lack of Interoperability among Dissimilar Product Versions

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.1.3 Professional Services

- 6.2 By End-user Industry

- 6.2.1 Electronics, Industrial Equipment, and High-tech

- 6.2.2 Aerospace and Defense

- 6.2.3 Automotive

- 6.2.4 Architecture, Engineering, and Construction (AEC)

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Dassault Systems Deutschland GmbH

- 7.1.3 Autodesk Inc.

- 7.1.4 PTC Inc.

- 7.1.5 SAP SE

- 7.1.6 ANSYS Germany GmbH

- 7.1.7 Oracle Corporation

- 7.1.8 Aras Corporation

- 7.1.9 Arena Solutions

- 7.1.10 Infor Inc.