|

市場調查報告書

商品編碼

1549797

電感器:市場佔有率分析、產業趨勢、成長預測(2024-2029)Inductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

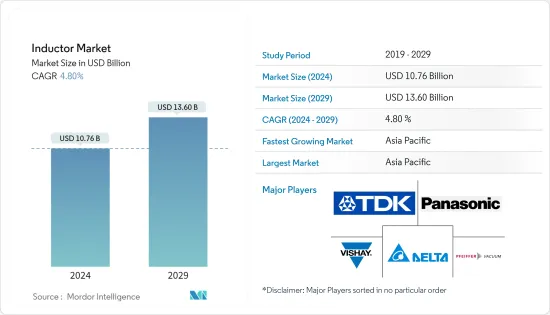

預計2024年電感器市場規模為107.6億美元,預計2029年將達136億美元,在市場預測期間(2024-2029年)複合年成長率為4.80%。

由於技術進步和各行業應用的增加,電感器市場的重要性顯著增加。電感器是電路中的重要元件,主要用於在磁場中能源儲存。它在汽車、航太、通訊、消費性電子等領域的廣泛應用凸顯了其重要角色。市場的發展受到電感器技術創新的影響,特別是為了滿足對節能系統和小型電子產品日益成長的需求。有幾個因素正在影響這個市場的動態,包括供應鏈的複雜性、材料成本和快速的技術進步。

消費性電子科技創新快速成長

主要亮點

- 科技快速進步:家用電子電器科技創新的快速步伐是塑造電感器市場的關鍵因素。隨著設備變得更小、更複雜,對更小、更有效率的電感器的需求也在增加。隨著智慧型手機、平板電腦、穿戴式裝置和其他行動裝置的激增,這種趨勢尤其明顯,所有這些裝置都需要高性能元件才能實現最佳功能。此外,智慧家庭設備和物聯網 (IoT) 應用的興起顯著增加了對先進電感器的需求。將這些組件整合到家用電子電器中可以提高能源效率、改善電源管理並提高整體效能。

- 小型化和效率:更小、更高性能設備的激增導致了電感器設計和製造流程的顯著進步。目前正在開發高頻電感器,以滿足現代電子設備的特定需求,從而在不犧牲性能的情況下實現更緊湊的電路設計。這一趨勢清楚地表明了市場對提供緊湊、高效的組件的關注,以滿足行業對小型化的需求。

- 物聯網和智慧型設備:物聯網設備的激增為感應器製造商帶來了新的機會。這些設備通常以低功耗運行,需要組件來有效管理電源,而電感器在其設計中發揮關鍵作用。不斷擴大的物聯網生態系統繼續推動對節能電感器的需求,這些電感器可以支援這些設備的低功耗要求。

- 能源效率:隨著消費者和監管機構都需要更節能的產品,製造商正在專注於開發有助於降低功耗的感測器。這對於電池供電的設備尤其重要,因為高效的電源管理非常重要。電感器設計中對能源效率的重視是一個重要趨勢,與更廣泛的產業永續性和減少能源使用的趨勢一致。

節能系統的需求不斷成長

主要亮點

- 汽車產業:汽車產業向電動車(EV)的轉變顯著增加了對高效能電感器的需求。這些組件對於電動車內的各種電力電子系統至關重要,例如車載充電器、DC-DC 轉換器和逆變器。電感器在最佳化功率轉換和更有效地管理能源方面發揮關鍵作用。隨著電動車普及率的提高,對能夠滿足汽車應用嚴格的效率要求的先進電感器的需求持續成長。

- 可再生能源系統:太陽能和風力發電等可再生能源系統的擴張也推動了對高效能電感器的需求。這些系統嚴重依賴電力電子設備進行能量轉換和管理,其中電感器作為關鍵組件,以確保高效的能量傳輸並最大限度地減少損失。對可再生能源的推動與該行業對永續性和開發節能技術的關注是一致的。

- 工業自動化:工業環境中向自動化和智慧製造流程的轉變增加了對能夠處理更高功率等級同時保持效率的電感器的需求。隨著工業採用更先進的自動化技術,電感器在確保可靠、高效運作方面的作用變得越來越重要。工業應用對高性能電感器的需求反映了各個領域自動化和數位轉型的更廣泛趨勢。

電感器市場趨勢

汽車產業預計將顯著成長

- 高頻電感快速擴張跡象:全球電感市場預計將顯著成長,尤其是高頻電感領域。隨著通訊、汽車和消費性電子等行業採用 5G、電動車 (EV) 和高級駕駛輔助系統 (ADAS) 等先進技術,對高頻電感器的需求預計將快速成長。這些元件對於確保高速、高效能電子設備的最佳性能至關重要,也是產業參與者的重點關注領域。

- 技術進步推動成長:高頻電感器市場的成長主要是由製造流程和材料的不斷進步所推動的。這些創新提高了電感器的性能、耐用性和可靠性,使其更適合要求嚴格的應用。包括高頻電感器在內的功率電感器領域在各個領域的電源管理應用中尤其重要,進一步推動了市場的成長。

- 電感器設計創新:隨著對緊湊、高效元件的需求增加,供應商越來越注重開發創新的電感器設計。這些進步正在改變競爭格局,主要製造商正在大力投資研發以保持競爭力。小型化趨勢,特別是智慧型手機和無線模組等小型通訊設備中的應用,也正在推動這種技術創新並促進整體市場成長。

- 價格趨勢與市場動態:高頻電感器需求的增加正在影響價格趨勢,原料成本和製造流程的波動也會影響市場。然而,規模經濟和製造技術的改進預計將穩定價格並增加各行業高頻電感器的可用性。高頻電感器的整體市場前景仍然看好,技術進步和不斷成長的需求提供了顯著的成長機會。

亞太地區預計將主導市場

- 蓬勃發展的電子產業:由於電子產業的蓬勃發展,亞太地區預計將實現最高的成長率並主導全球電感器市場。中國、日本和韓國等國家正在透過對半導體製造、家用電子電器和汽車產業的大量投資來推動這一成長。該地區強大的製造基地和主要感應器供應商的存在提供了競爭優勢,使我們能夠有效地滿足不斷成長的全球需求。

- 採用先進技術:5G、物聯網和電動車等先進技術的快速採用正在推動亞太地區對感應器的需求。行業資料顯示,該地區的電感器市場規模正在迅速擴大,其中功率電感器和高頻電感器在支援該地區廣泛的通訊基礎設施和汽車工業方面發揮關鍵作用。該地區電動和混合動力汽車的成長尤其推動了對這些零件的需求。

- 強調創新與永續性:不斷增加的研發投資是推動亞太感應器市場的關鍵因素。當地企業處於開發新感應器類型和應用的前沿,增加了該地區的市場佔有率。對永續製造方法和節能電感器開發的關注符合全球永續性趨勢,進一步提振了市場前景。

- 強勁的市場預測:亞太地區強勁的市場預測得到電子製造和技術創新領先地位的支持。隨著該地區不斷創新和整合先進技術,對電感器的需求預計將增加,從而推動市場成長並鞏固亞太地區作為全球電感器市場領導者的地位。該地區對智慧城市舉措和汽車行業成長的關注進一步促進了這一積極的市場軌跡。

感應器產業概況

市場分散:感應器市場高度分散,許多全球和地區公司構成了競爭格局。市場競爭涉及各種規模的公司,不存在任何一家公司明顯佔據主導地位的情況。Panasonic Corporation、村田製作所等企業集團以及 Coilcraft Inc. 和 Sumida Corporation 等專業公司的出現,體現了市場的多樣性。這種碎片化表明沒有一家公司擁有較大的市場佔有率,從而創造了激烈的競爭和差異化機會。

提供多元化產品的市場領導:TDK Corporation、Vishay Intertechnology Inc. 和 Pulse Electronics(YAGEO 公司的子公司)等主要企業在塑造全球電感器市場方面發揮關鍵作用。這些公司透過廣泛的產品系列、技術創新和策略性收購確立了自己的地位。 TDK 公司和村田製作所以透過大力投資研發來保持競爭力而聞名。同時,Delta電子和太陽誘電等公司利用其技術專長和全球影響力為汽車、消費電子和通訊等廣泛行業提供服務。

未來成功的策略 在競爭激烈的感應器市場中,各公司都專注於創新、品質改進和策略夥伴關係,以獲得優勢。小型化、效率提高以及將電感器整合到複雜的電子系統中等趨勢對於保持相關性至關重要。能夠不斷創新、適應新行業標準並滿足對更小、更高性能電感器不斷成長的需求的公司可能會取得成功。此外,向電感器需求不斷成長的新興市場和產業擴張將是維持成長的重要策略。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 產業價值鏈分析

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 加大家電技術創新力度

- 對節能電氣和電子系統的需求不斷增加

- 市場限制因素

- 原料成本上漲,特別是銅

第6章 市場細分

- 按類型

- 電力

- 按頻率

- 按最終用戶產業

- 車

- 航太/國防

- 通訊

- 消費性電子與計算

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲/紐西蘭

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- TDK Corporation

- Vishay Intertechnology Inc.

- Panasonic Corporation

- Delta Electronics

- Pulse Electronics(YAGEO Company)

- Sagami Elec Co. Ltd

- Taiyo Yuden Co. Ltd

- TE Connectivity Limited

- Murata Manufacturing Co. Ltd

- Sumida Corporation

- Coilcraft Inc.

第8章投資分析

第9章市場的未來

The Inductor Market size is estimated at USD 10.76 billion in 2024, and is expected to reach USD 13.60 billion by 2029, growing at a CAGR of 4.80% during the forecast period (2024-2029).

The inductor market has seen a significant rise in importance, driven by technological advancements and increasing applications across various industries. Inductors, which are crucial components in electrical circuits, primarily serve the purpose of energy storage within a magnetic field. Their extensive use in sectors such as automotive, aerospace, communications, and consumer electronics highlights their indispensable role. The market's evolution has been shaped by innovations in inductor technology, especially in response to the growing demand for energy-efficient systems and miniaturized electronic devices. Several factors, including supply chain complexities, material costs, and rapid technological advancements, influence the dynamics of this market.

Innovation Surge in Consumer Electronics

Key Highlights

- Rapid Technological Advancements: The swift pace of innovation in consumer electronics is a pivotal factor shaping the inductor market. As devices become more compact and sophisticated, the demand for smaller, more efficient inductors has escalated. This trend is particularly evident in the proliferation of smartphones, tablets, wearables, and other portable devices, all of which require high-performance components for optimal functionality. Furthermore, the rise of smart home devices and IoT (Internet of Things) applications has significantly increased the need for advanced inductors. The integration of these components into consumer electronics ensures improved energy efficiency, better power management, and enhanced overall performance.

- Miniaturization and Efficiency: The push towards smaller, more powerful devices has driven substantial advancements in inductor design and manufacturing processes. High-frequency inductors are now being developed to meet the specific needs of modern electronics, allowing for more compact circuit designs without compromising performance. This trend underscores the market's focus on delivering compact, efficient components that align with the industry's demand for miniaturization.

- IoT and Smart Devices: The increasing adoption of IoT devices presents new opportunities for inductor manufacturers. These devices, which often operate on low power, require components that manage power efficiently, making inductors a critical part of their design. The expanding IoT ecosystem continues to drive the demand for energy-efficient inductors that can support the low-power requirements of these devices.

- Energy Efficiency: As consumers and regulators alike demand more energy-efficient products, manufacturers are focusing on developing inductors that contribute to lower power consumption. This is especially important in battery-powered devices, where efficient power management is crucial. The emphasis on energy efficiency in inductor design is a key trend that aligns with broader industry movements towards sustainability and reduced energy usage.

Growing Demand for Energy-Efficient Systems

Key Highlights

- Automotive Sector: The automotive industry's shift towards electric vehicles (EVs) has significantly increased the demand for high-efficiency inductors. These components are essential in various power electronic systems within EVs, including onboard chargers, DC-DC converters, and inverters. Inductors play a crucial role in optimizing power conversion and managing energy more effectively, which is vital for extending battery life and enhancing vehicle performance. The growing adoption of EVs continues to drive demand for advanced inductors that can meet the stringent efficiency requirements of automotive applications.

- Renewable Energy Systems: The expansion of renewable energy systems, such as solar and wind power, also propels the demand for efficient inductors. These systems rely heavily on power electronics to convert and manage energy, with inductors serving as key components in ensuring efficient energy transfer and minimizing losses. The push towards renewable energy aligns with the industry's focus on sustainability and the development of energy-efficient technologies.

- Industrial Automation: The move towards automation and smart manufacturing processes in industrial settings has led to an increased need for inductors capable of handling higher power levels while maintaining efficiency. As industries adopt more sophisticated automation technologies, the role of inductors in ensuring reliable and efficient operation becomes increasingly critical. The demand for high-performance inductors in industrial applications reflects the broader trend of automation and digital transformation across various sectors.

Inductor Market Trends

Automotive Industry Segment is Expected to Register Significant Growth

- High-Frequency Inductors Poised for Rapid Expansion: The global inductor market is poised for substantial growth, particularly in the high-frequency inductor segment. As industries such as telecommunications, automotive, and consumer electronics increasingly adopt advanced technologies like 5G, electric vehicles (EVs), and advanced driver-assistance systems (ADAS), the demand for high-frequency inductors is expected to surge. These components are essential for ensuring optimal performance in high-speed, high-efficiency electronic devices, making them a critical focus area for industry players.

- Technological Advancements Driving Growth: The growth in the high-frequency inductor market is significantly driven by ongoing advancements in manufacturing processes and materials. These innovations enhance the performance, durability, and reliability of inductors, making them more suitable for demanding applications. The power inductor segment, which includes high-frequency inductors, is particularly crucial in power management applications across various sectors, further driving market growth.

- Innovations in Inductor Design: As demand for compact and efficient components rises, suppliers are increasingly focused on developing innovative inductor designs. These advancements are reshaping the competitive landscape, with key players investing heavily in research and development to maintain a competitive edge. The trend towards miniaturization, particularly for applications in small communication devices like smartphones and wireless modules, is also driving this innovation, contributing to the overall growth of the market.

- Price Trends and Market Dynamics: The rising demand for high-frequency inductors is influencing price trends, with fluctuations in raw material costs and manufacturing processes potentially impacting the market. However, economies of scale and improvements in manufacturing technologies are expected to help stabilize prices, making these inductors more accessible across various industries. The overall market outlook for high-frequency inductors remains positive, with significant growth opportunities driven by technological advancements and increasing demand.

Asia-Pacific Region is Expected to Dominate the Market

- Booming Electronics Industry: The Asia-Pacific region is expected to dominate the global inductor market, registering the highest growth rate due to its thriving electronics industry. Countries such as China, Japan, and South Korea are leading this growth, driven by substantial investments in semiconductor manufacturing, consumer electronics, and the automotive sector. The region's strong manufacturing base and the presence of key inductor suppliers provide a competitive advantage, enabling it to meet growing global demand efficiently.

- Adoption of Advanced Technologies: The rapid adoption of advanced technologies such as 5G, IoT, and electric vehicles is fueling demand for inductors in the Asia-Pacific region. Industry data indicates that the market size for inductors in this region is expanding rapidly, with power and high-frequency inductors playing a critical role in supporting the region's extensive telecommunications infrastructure and automotive industry. The growth of electric and hybrid vehicles in the region is particularly driving the demand for these components.

- Focus on Innovation and Sustainability: Increased investment in research and development is a key factor driving the inductor market in Asia-Pacific. Local companies are at the forefront of developing new inductor types and applications, enhancing the region's market share. The focus on sustainable manufacturing practices and the development of energy-efficient inductors aligns with global trends towards sustainability, further boosting the market outlook.

- Strong Market Forecast: The Asia-Pacific region's strong market forecast is supported by its leadership in electronics manufacturing and technological innovation. As the region continues to innovate and integrate advanced technologies, the demand for inductors is expected to rise, driving market growth and solidifying Asia-Pacific's position as a global leader in the inductor market. The region's focus on smart city initiatives and the growing automotive sector further contribute to this positive market trajectory.

Inductor Industry Overview

Highly Fragmented Market: The inductor market is highly fragmented, with numerous global and regional players contributing to a competitive landscape. The market lacks clear dominance by any single company, with competition spread across multiple firms, both large and small. The presence of conglomerates such as Panasonic Corporation and Murata Manufacturing Co., Ltd., alongside specialized companies like Coilcraft Inc. and Sumida Corporation, illustrates the diverse nature of the market. This fragmentation suggests that no single company holds a substantial market share, leading to intense competition and opportunities for differentiation.

Market Leaders with Diverse Offerings: Leading companies like TDK Corporation, Vishay Intertechnology Inc., and Pulse Electronics (a subsidiary of YAGEO Company) play pivotal roles in shaping the global inductor market. These firms have established themselves through extensive product portfolios, innovation, and strategic acquisitions. TDK Corporation and Murata Manufacturing Co. Ltd. are known for their significant R&D investments, allowing them to maintain a competitive edge. Meanwhile, companies like Delta Electronics and Taiyo Yuden Co., Ltd. leverage their technological expertise and global presence to cater to a broad range of industries, including automotive, consumer electronics, and telecommunications.

Strategies for Future Success: In the highly competitive inductor market, companies are focusing on innovation, quality enhancement, and strategic partnerships to stay ahead. Trends such as miniaturization, increased efficiency, and the integration of inductors into complex electronic systems are crucial for maintaining relevance. Companies that can continuously innovate, adapt to new industry standards, and meet the growing demand for compact, high-performance inductors are likely to thrive. Additionally, expanding into emerging markets and industries with growing inductor demand will be a key strategy for sustaining growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Innovations in Consumer Electronics Products

- 5.1.2 Growing Demand for Energy Efficient Electrical and Electronic Systems

- 5.2 Market Restraints

- 5.2.1 Rising Cost of Raw Materials, Especially Copper

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Power

- 6.1.2 Frequency

- 6.2 By End-User Industry

- 6.2.1 Automotive

- 6.2.2 Aerospace and Defense

- 6.2.3 Communications

- 6.2.4 Consumer Electronics and Computing

- 6.2.5 Other End-User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TDK Corporation

- 7.1.2 Vishay Intertechnology Inc.

- 7.1.3 Panasonic Corporation

- 7.1.4 Delta Electronics

- 7.1.5 Pulse Electronics (YAGEO Company)

- 7.1.6 Sagami Elec Co. Ltd

- 7.1.7 Taiyo Yuden Co. Ltd

- 7.1.8 TE Connectivity Limited

- 7.1.9 Murata Manufacturing Co. Ltd

- 7.1.10 Sumida Corporation

- 7.1.11 Coilcraft Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

AI伺服器電感器市場:依產品類型、磁芯材料、安裝類型、額定電流、製造流程、屏蔽、冷卻方式、應用子系統和最終用戶分類,全球預測,2026-2032年高功率交流逆變器電感器市場:按應用、輸出容量、磁芯材料、頻率範圍、電感範圍、冷卻方式、繞線方式和封裝類型分類,全球預測,2026-2032年

AI伺服器電感器市場:依產品類型、磁芯材料、安裝類型、額定電流、製造流程、屏蔽、冷卻方式、應用子系統和最終用戶分類,全球預測,2026-2032年高功率交流逆變器電感器市場:按應用、輸出容量、磁芯材料、頻率範圍、電感範圍、冷卻方式、繞線方式和封裝類型分類,全球預測,2026-2032年 全球可調式電感器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球可調式電感器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球金屬動力傳動鏈市場報告全球環形變壓器市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)多層功率電感器市場:按類型、電感範圍、額定電流、封裝、銷售管道和應用分類-全球預測,2026-2032年多層電感器市場:按電感類型、安裝類型、材質類型、電感範圍和應用分類 - 全球預測(2026-2032年)大電流鐵氧體輪胎邊緣晶片市場(按安裝類型、額定電流、電阻範圍、材料配置和最終用戶分類),全球預測(2026-2032年)按產品類型、電感範圍、銷售管道、屏蔽類型、應用程式和最終用戶產業分類的線繞高頻電感器市場-2026-2032年全球預測晶片多層電感器市場:按材料、安裝類型、頻率範圍、額定功率、應用和分銷管道分類,全球預測(2026-2032年)

2026年全球金屬動力傳動鏈市場報告全球環形變壓器市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)多層功率電感器市場:按類型、電感範圍、額定電流、封裝、銷售管道和應用分類-全球預測,2026-2032年多層電感器市場:按電感類型、安裝類型、材質類型、電感範圍和應用分類 - 全球預測(2026-2032年)大電流鐵氧體輪胎邊緣晶片市場(按安裝類型、額定電流、電阻範圍、材料配置和最終用戶分類),全球預測(2026-2032年)按產品類型、電感範圍、銷售管道、屏蔽類型、應用程式和最終用戶產業分類的線繞高頻電感器市場-2026-2032年全球預測晶片多層電感器市場:按材料、安裝類型、頻率範圍、額定功率、應用和分銷管道分類,全球預測(2026-2032年)