|

市場調查報告書

商品編碼

1549899

全球主動光纜 (AOC):市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)Global Active Optical Cables (AOC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

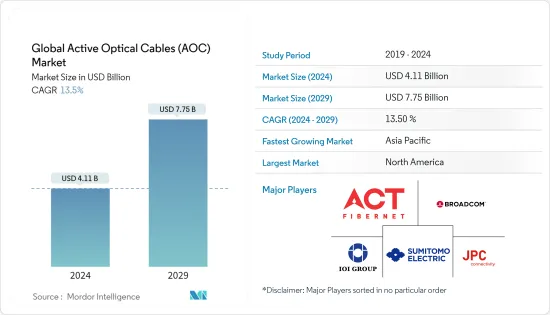

預計2024年全球主動光纜(AOC)市場規模為41.1億美元,2029年預計將達到77.5億美元,複合年成長率預計為13.5%。

主動式光纜市場目前正在經歷強勁成長,由於雲端基礎服務、數位化、5G、資料中心和其他應用的大規模實施,預計將進一步成長。

主要亮點

- 主動式光纜 (AOC) 市場主要是由資料中心、通訊和消費性電子產品等各種應用中對高速資料傳輸的需求不斷成長所推動的。各種應用程式不斷成長的資料需求預計將推動 AOC 市場的需求。

- 由於雲端技術、數位化的大規模應用以及AI/ML需求的不斷增加,資料中心市場正在快速成長。根據通訊服務供應商Cloudscene的數據,截至2023年12月,全球約有10,978個資料中心,且這個數字正在迅速增加。資料中心需要強大且快速的網路連線。因此,資料中心市場的成長預計也將推動AOC市場。

- 5G 的推出旨在滿足對高效通訊不斷成長的需求,這對於推動數位業務至關重要。雖然 5G 的寬頻波長可實現快速資料傳輸,但與 3G 和 4G 相比,訊號範圍有限。因此,強大的 5G 網路需要密集的蜂巢塔,並依靠高速電纜進行訊號傳輸,從而推動 AOC 市場的需求。

- GSMA 預測,到 2029 年,5G 連線將佔所有行動連線的一半以上 (51%),並在 10 年內升至 56%,鞏固 5G 作為主導連線技術的地位。 5G 的部署已經超過了之前所有行動技術,預計到 2023年終將達到超過 16 億個連接,到 2030 年將達到 55 億個連接。因此,隨著5G持續快速擴張,全球主動式光纜市場預計在不久的將來會顯著成長。

- 光纖傳輸安全性和敏感資料應用中潛在漏洞的擔憂可能會阻礙 AOC 的廣泛採用。此外,與傳統銅纜相比,AOC 通常會帶來更大的維護和維修挑戰,特別是在需要快速服務介入的區域。

全球主動光纜(AOC)市場趨勢

資料中心對主動光纜的需求增加推動市場

- 近年來,受全行業高速資料傳輸需求激增的推動,全球主動式光纜(AOC)市場出現了顯著成長。隨著技術的進步,高效、可靠的連接解決方案比以往任何時候都更重要。主動式光纜 (AOC) 作為高速電纜解決方案脫穎而出,它將雷射和光電二極體等主動元件直接整合到電纜組件中。這些組件對於促進光訊號在光纖電纜上的傳輸至關重要。在資料中心領域,術語「200G AOC」是指專門設計用於支援 200Gigabit每秒 (Gbps)資料速率的電纜。

- 此外,在需要大量運算能力的高效能運算 (HPC) 環境中,200G AOC 有助於處理器和儲存單元之間的快速資料交換。企業正在利用高效能運算進行平行處理,以幫助運行人工智慧和資料分析等高階程式。資料中心,特別是那些專注於人工智慧和機器學習的資料中心,可以從 HPC 中受益匪淺。

- 組織內部雲端運算的興起正在顯著推動資料中心市場的發展。根據 Flexera 2023 年雲端狀態報告,72% 的企業已採用混合雲端。然而,這種轉變通常意味著超越傳統的私有雲端或公共雲端基礎架構。

- 主動式光纜 (AOC) 對於連接資料中心纜線架和交換器至關重要,可實現交換器和伺服器之間的無縫通訊。資料中心通常會先安裝交換機,然後再部署結構化佈線,最後選擇合適的互連產品進行網路存取。對於短距離(定義為 10G 為 90 公尺或更短,40G 為 10 公尺或更短),銅纜是最具成本效益的選擇。對於 10G 500 公尺以下和 40G 150 公尺以下的中距離,多模 VCSEL(垂直共振腔面射型雷射)收發器是首選,通常輔以 AOC。

- 印度資料中心市場預計將大幅擴張,到 2025 年將達到 46 億美元。這一成長的推動因素包括該國網際網路用戶數量的增加、雲端處理需求的增加、政府促進數位化的舉措以及數位服務提供商向本地化的轉變。值得注意的是,印度資料中心產業無論在市場開拓或營運階段,與新興市場相比都具有顯著的成本優勢。目前,我們主要的資料中心地點主要位於孟買、班加羅爾、清奈、德里 (NCR)、海得拉巴和普納,新資料中心將在加爾各答、喀拉拉邦和艾哈默德巴德建立。隨著資料中心投資的成長,印度各地對包括 IT、電氣、機械和一般建築在內的輔助基礎設施服務的需求也在成長。

北美佔有很大佔有率

- 北美擁有全球最大的資料中心市場,目前超大規模資料中心的建設大幅增加。這一激增的主要驅動力是對雲端服務不斷成長的需求和持續的數位轉型。根據Cloudscene發布的截至2024年3月的最新資料,美國擁有5,381個資料中心,位居全球第一。德國以 521 名緊隨其後,英國以 514 名緊隨其後。從歷史上看,銅纜一直用於伺服器、路由器和交換器之間的網路連結。隨著資料中心的擴張,該地區對有源銅佈線的需求持續成長。

- 美國對新資料中心的需求仍然強勁,每週都會宣布新計劃。 2024年3月,亞馬遜宣布計畫斥資6.5億美元收購伯威克核能發電廠附近的資料中心。這個想法得到了 Talen Energy 的證實,該公司在塞勒姆鎮經營薩斯奎哈納蒸氣發電廠,並將由亞馬遜的網路服務部門牽頭開發新資料中心。

- 美國高速網路的開拓也是推動全球AOC市場的主要因素。美國農業部 (USDA) 已承諾提供總計 9,700 萬美元幫助企業建立人脈。這些網路針對的是未達到美國政府目標的目標(即到 2027 年為所有美國家庭提供 100 Mbps 的下載速度和 20 Mbps 的上傳速度)或缺乏連線的地區。此措施將增強對 11 個州 22,000 名用戶的服務。

- 位於 Green City 的酵母密蘇裡州農村電話公司獲得了 1,370 萬美元的貸款,用於將 6 個交換機從銅纜技術過渡到光纖到戶技術。該計劃將安裝大約 500 路由英里的光纖,以改善對 1,063 個用戶的服務。

- 2023年10月,美國聯邦通訊委員會(FCC)開始大規模投資約182.8億美元,用於加強農村寬頻基礎設施。該資金將分配給從 2024 年 1 月開始的為期 15 年的計劃,目標是在超過 700,000 個地點部署 100/20Mbps 寬頻。它還旨在升級 44 個州約 200 萬個地點的現有服務。這一雄心勃勃的寬頻擴張可能會對 AOC 市場產生重大影響。

全球主動光纜(AOC)產業概況

主動式光纜 (AOC) 市場較為分散。研究市場的主要參與者包括 ACT、Broadcom Inc.、Sumitomo Electric 和 JPC Connectivity。市場上的公司正在採取聯盟、合約、創新和收購等策略來增強服務產品並獲得永續的競爭優勢。

- 2024 年 1 月 領先的光纖解決方案供應商 OFS 宣布其最新創新產品 LaserWave 雙頻 OM4+ 多模光纖。這款多模光纖加入了廣受好評的 OM4 和 OM5 系列,在頻寬、衰減和幾何形狀方面樹立了新標準。 LaserWave 雙頻 OM4+ 是一款專為雙向 (BiDi) 應用精心打造的優質且經濟高效的光纖。此光纖設計用於為高密度、低功耗、多模鏈路供電。它在 850nm 和 910nm 波長的性能也與 OM5 一樣,這使得它對於雙向傳輸至關重要。這可確保一致的 100 公尺覆蓋範圍,這是Terabit BiDi 乙太網路(包括 800G-SR4.2 和 1.6T-SR8.2)等尖端應用的基本指標。

- 2024年1月,澳洲電信國際公司與跨太平洋網路公司(TPN)合作部署Echo電纜系統,這是第一條直接連接美國和新加坡的海底電纜。 Echo 電纜的第一段是關島和美國之間的專用光纖鏈路,計劃於 2024 年中期開通,後續段計劃於 2025 年開通。建成後,它將無縫連接加州、雅加達、新加坡和關島。 Telstra強調,該系統不僅開拓了新的路線,而且還承諾提供低延遲、高速度和強大彈性的網路基礎設施。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 宏觀經濟情境分析(景氣衰退、俄羅斯/烏克蘭危機等)

- 評估 COVID-19 大流行的影響和恢復

第5章市場動態

- 市場促進因素

- 電訊領域向更快光纖網路的轉變

- 對寬頻化的需求不斷增加

- 資料中心對主動式光纜的需求增加

- 數位化和5G連接的高滲透率

- 市場挑戰

- 高初始成本和光纖網路安全光纖駭客

- 對電力消耗的擔憂

- 缺乏技術專長

- 價格和技術規格分析

- 關於直連接線(有源和無源)與主動光纜的技術見解

- 世界貿易分析

- 對 AOC 最常見外形規格規格的重要見解

- 深入了解 AOC 中的各種通訊協定類型

第6章 市場細分

- 按用途

- 資料中心

- 通訊

- 高效能運算 (HPC)

- 家用電子產品

- 工業應用

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 亞洲

- 中國

- 印度

- 日本

- 澳洲/紐西蘭

- 拉丁美洲

- 中東/非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- JPC Connectivity

- Shenzhen Sopto Technology Co. Ltd

- Linkreal Co. Ltd

- Broadcom

- Sumitomo Electric Lightwave Inc.

- Black Box

- ACT

- IOI Technology Corporation

- ETU-Link Technology Co. Ltd

- Amphenol Corporation

第8章 市場機會及未來趨勢

The Global Active Optical Cables Market size is estimated at USD 4.11 billion in 2024, and is expected to reach USD 7.75 billion by 2029, growing at a CAGR of 13.5% during the forecast period (2024-2029).

The active optical cables market is currently experiencing robust growth, and it is expected to grow further owing to the large-scale adoption of cloud-based services, digitalization, 5G, data centers, and other applications.

Key Highlights

- The active optical cable (AOC) market is mostly driven by the increasing need for high-speed data transmission in a variety of applications, including data centers, telecommunications, and consumer electronics. The growing need for data through various applications is expected to drive the demand for the AOC Market.

- The data center market is growing rapidly owing to the large-scale application of cloud technologies, digitalization, and growing demand for AI/ML. According to Cloudscene, a telecommunication services provider, there are approximately 10,978 data center locations worldwide as of December 2023, with numbers growing rapidly. Data centers require robust and high-speed internet connectivity. Therefore, the growth in the data center market is anticipated to drive the AOC market as well.

- 5G implementation is poised to meet the escalating demand for efficient communication, which is crucial for enhancing digital operations. While 5G's broader wavelength enables rapid data transmission, its signals are limited in range compared to 3G and 4G. Consequently, a robust 5G network necessitates a dense array of cell towers, each reliant on high-speed cables for signal transmission, thereby bolstering the demand for the AOC market.

- GSMA forecasts that 5G connections will account for over half (51%) of all mobile connections by 2029, climbing to 56% by the decade's end, solidifying 5G as the leading connectivity technology. 5G has outpaced all previous mobile generations in its rollout, exceeding 1.6 billion connections by the end of 2023, and it is projected to reach 5.5 billion by 2030. Consequently, as 5G continues its rapid expansion, the global active optical cables market is poised for significant growth in the near future.

- Concerns over the security of optical transmissions and potential vulnerabilities in sensitive data applications may impede the widespread adoption of AOCs. Additionally, AOCs often pose greater maintenance and repair challenges compared to traditional copper cables, particularly in sectors requiring swift service interventions.

Global Active Optical Cables (AOC) Market Trends

Rising Demand for Active Optical Cable in Data Centers to Drive the Market

- The global active optical cable (AOC) market has witnessed significant growth in recent years, propelled by the surging demand for high-speed data transmission across industries. With technological advancements, the emphasis on efficient and dependable connectivity solutions has never been more critical. Active optical cables (AOCs) stand out as high-speed cabling solutions, incorporating active elements like lasers and photodiodes directly into the cable assembly. These components are pivotal, facilitating the transmission of optical signals through fiber optic cables. In the realm of data centers, the term '200G AOC' specifically denotes cables engineered to support data rates of 200 gigabits per second (Gbps).

- Additionally, in high-performance computing (HPC) settings demanding substantial computational power, the 200G AOC facilitates swift data exchange between processors and storage units. Organizations leverage high-performance computing for parallel processing, empowering them to execute advanced programs like AI and data analytics. Data centers, especially those emphasizing AI and machine learning, stand to gain significantly from HPC.

- The rise of cloud computing within organizations significantly drives the data center market. According to the Flexera State of the Cloud Report 2023, 72% of companies have adopted hybrid clouds. Yet, this transition frequently means moving beyond conventional private and public cloud infrastructures.

- Active optical cables (AOCs) are pivotal in connecting data center cabling racks and switches, enabling seamless communication between switches and servers. Typically, data centers first install switches, then implement structured cabling, and finally, select the appropriate interconnect products for network access. Copper cables are the most cost-effective choice for short distances, defined as under 90 meters for 10G and under 10 meters for 40G. For medium distances spanning under 500 meters for 10G and 150 meters for 40G, multimode VCSEL (vertical cavity surface emitting laser) transceivers are favored, often complemented by AOCs.

- India's data center market is set for a significant uptick, with forecasts pointing to a climb to USD 4.6 billion by 2025. This growth is fueled by several factors: a growing domestic internet user base, rising demands for cloud computing, government initiatives driving digitalization, and a shift toward localization by digital service providers. Notably, India's data center sector boasts a significant cost advantage, both in its development and operational phases, compared to more mature markets. Currently, key data center hubs are primarily located in Mumbai, Bengaluru, Chennai, Delhi (NCR), Hyderabad, and Pune, with emerging centers in Calcutta, Kerala, and Ahmedabad. As investments in data centers expand, so does the demand for ancillary infrastructure services covering IT, electrical, mechanical, and general construction throughout India.

North America to Hold a Major Share

- North America boasts the world's largest data center market, currently experiencing a notable rise in hyperscale data center construction. This surge is primarily fueled by the escalating demand for cloud services and the ongoing digital transformation. Recent data from Cloudscene, as of March 2024, highlights the United States as the global leader, housing 5,381 reported data centers. Germany and the United Kingdom follow closely, with 521 and 514 centers, respectively. Historically, copper cables have been the go-to for networking links between servers, routers, and switches. With the expanding data center landscape, the demand for active copper cables in the region is set to rise.

- The demand for new data centers in the United States remains strong, with fresh projects unveiled almost weekly. In March 2024, Amazon disclosed its plan to invest a hefty USD 650 million in acquiring a data center adjacent to the Berwick nuclear power plant. This initiative, confirmed by Talen Energy, the operator of the Susquehanna Steam Electric Station in Salem Township, will see Amazon's web services arm spearhead the development of the new data center.

- The development of high-speed internet in the United States is also a major factor driving the global AOC market. The US Department of Agriculture (USDA) has pledged a total of USD 97 million to assist operators in establishing networks. These networks are aimed at areas lacking connectivity or falling below the US government's set target of 100 Mbps download and 20 Mbps upload speeds for all American households by 2027. This initiative is set to enhance services for 22,000 subscribers across 11 states.

- Green City's Northeast Missouri Rural Telephone Company secured a USD 13.7 million loan to transition six exchanges from copper to fiber-to-the-premises technology. This initiative involves laying down approximately 500 route miles of fiber, with the aim of enhancing services for 1,063 subscribers.

- In October 2023, the US Federal Communications Commission (FCC) initiated a significant investment of approximately USD 18.28 billion to strengthen rural broadband infrastructure. This funding, allocated for a 15-year program commencing in January 2024, targets the deployment of 100/20 Mbps broadband to over 700,000 locations. Furthermore, it aims to upgrade existing services for approximately 2 million locations spread across 44 states. This ambitious broadband expansion is set to have a profound impact on the AOC market.

Global Active Optical Cables (AOC) Industry Overview

The active optical cables (AOC) market is fragmented in nature. Some major players in the market studied are ACT, Broadcom Inc., Sumitomo Electric, JPC Connectivity, etc. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- January 2024: OFS, a prominent figure in the fiber optic solutions realm, unveiled its latest innovation: the LaserWave Dual-Band OM4+ Multimode Optical Fiber. This addition to the lineup, alongside the already esteemed OM4 and OM5 offerings, sets new benchmarks in bandwidth, attenuation, and geometry. The LaserWave Dual-Band OM4+ stands out as a premium yet cost-effective fiber, meticulously crafted for bidirectional (BiDi) applications. It is tailored to bolster the upcoming wave of high-density, low-power multimode links. Its capability to deliver performance akin to OM5 at both 850 nm and 910 nm wavelengths is also noteworthy, which is crucial for bidirectional transmissions. This ensures a consistent 100-meter reach, a vital metric for cutting-edge applications like Terabit BiDi Ethernet, including 800G-SR4.2 and 1.6T-SR8.2.

- January 2024: Telstra International teamed up with Trans Pacific Networks (TPN) to introduce the Echo cable system, marking the inaugural subsea cable directly linking the United States and Singapore. The initial segment of the Echo cable, a dedicated fiber-optic line linking Guam and the United States, is set for a mid-2024 debut, with subsequent segments slated for 2025. Upon completion, the cable will seamlessly link California, Jakarta, Singapore, and Guam. Telstra emphasizes that this system will not only forge a new route but also promise a network infrastructure characterized by low latency, high speeds, and robust resilience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Macro-economic Scenarios (Recession, Russia-Ukraine Crisis, etc.)

- 4.3 An Assessment of the Impact of and Recovery from COVID-19 Pandemic

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Change in the Telecom Sector Toward Faster Optical Networks

- 5.1.2 Increased Need for Higher Bandwidth

- 5.1.3 Rising Demand for Active Optical Cable in Data Centers

- 5.1.4 Digitalization and High Adoption of 5G Connectivity

- 5.2 Market Challenges

- 5.2.1 Significant Initial Cost and Optical Network Security Fiber Hacking

- 5.2.2 Significant Power Consumption Concerns

- 5.2.3 Lack of Technical Expertise

- 5.3 Analysis of Pricing and Technical Specifications

- 5.4 Technology Insights on Direct Attach Cables (Active and Passive) vs. Active Optical Cable

- 5.5 Global Trade Analysis

- 5.6 Key Insights into Most Common Form Factor Specifications of AOC

- 5.7 Key Insights into Various Protocol Types of AOC

6 MARKET SEGMENTATION

- 6.1 By Application Area

- 6.1.1 Data Center

- 6.1.2 Telecommunication

- 6.1.3 High-Performance Computing (HPC)

- 6.1.4 Consumer Electronics

- 6.1.5 Industrial Applications

- 6.1.6 Other Applications

- 6.2 By Region

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Australia and New Zealand

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 JPC Connectivity

- 7.1.2 Shenzhen Sopto Technology Co. Ltd

- 7.1.3 Linkreal Co. Ltd

- 7.1.4 Broadcom

- 7.1.5 Sumitomo Electric Lightwave Inc.

- 7.1.6 Black Box

- 7.1.7 ACT

- 7.1.8 IOI Technology Corporation

- 7.1.9 ETU-Link Technology Co. Ltd

- 7.1.10 Amphenol Corporation

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

主動光纜市場 - 全球產業規模、佔有率、趨勢、機會及預測(按通訊協定、外形規格尺寸、最終用戶應用、地區和競爭格局分類,2021-2031年)

主動光纜市場 - 全球產業規模、佔有率、趨勢、機會及預測(按通訊協定、外形規格尺寸、最終用戶應用、地區和競爭格局分類,2021-2031年) 室內光纜市場按產品類型、光纖數量、光纜結構、安裝類型和應用分類-全球預測,2026-2032年

室內光纜市場按產品類型、光纖數量、光纜結構、安裝類型和應用分類-全球預測,2026-2032年 主動式光纜市場-2026-2031年預測

主動式光纜市場-2026-2031年預測 主動光纜市場規模、佔有率及成長分析(依產品類型、通訊協定、外形規格、傳輸距離、材料類型、應用及地區分類)-產業預測,2026-2033年按傳輸距離、纜線類型、應用、資料速率和連接器類型分類的主動光纜市場-2025-2032年全球預測球透鏡擴束光纖連接器市場(依傳輸模式、連接器介面、應用和銷售管道)——2025-2030 年全球預測

主動光纜市場規模、佔有率及成長分析(依產品類型、通訊協定、外形規格、傳輸距離、材料類型、應用及地區分類)-產業預測,2026-2033年按傳輸距離、纜線類型、應用、資料速率和連接器類型分類的主動光纜市場-2025-2032年全球預測球透鏡擴束光纖連接器市場(依傳輸模式、連接器介面、應用和銷售管道)——2025-2030 年全球預測 主動式光纖 (AOC) 的全球市場:類型·尺寸規格·用途·終端用戶·各地區 (~2030年)

主動式光纖 (AOC) 的全球市場:類型·尺寸規格·用途·終端用戶·各地區 (~2030年) 2025 年至 2033 年主動式光纜市場規模、佔有率、趨勢及預測(按連接器類型、技術、應用和地區)

2025 年至 2033 年主動式光纜市場規模、佔有率、趨勢及預測(按連接器類型、技術、應用和地區) AOC電纜的全球市場:市場佔有率與排行榜,整體銷售額與需求預測(2025年~2031年)全球主動光纜市場規模:依連接器類型、應用程式、最終用戶、地區、範圍和預測

AOC電纜的全球市場:市場佔有率與排行榜,整體銷售額與需求預測(2025年~2031年)全球主動光纜市場規模:依連接器類型、應用程式、最終用戶、地區、範圍和預測