|

市場調查報告書

商品編碼

1550006

資料中心處理器:市場佔有率分析、產業趨勢、成長預測(2024-2029)Data Center Processor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

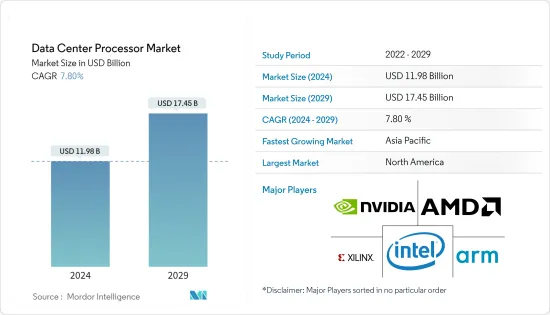

資料中心處理器市場規模預計到 2024 年為 119.8 億美元,預計到 2029 年將達到 174.5 億美元,在預測期內(2024-2029 年)複合年成長率為 7.80%。

主要亮點

- 資料中心處理器是資料中心運算基礎設施的關鍵元件。執行算術處理、邏輯處理、輸入/輸出處理等多種任務的高效能晶片。資料中心依賴伺服器,伺服器是具有大量儲存、記憶體、處理能力和輸入/輸出能力的高效能電腦。這些伺服器使用資料中心處理器來處理計算負載並運行應用程式。資料中心處理器的選擇取決於您的特定任務和要求。雖然通用 CPU 可能適合許多應用,但人工智慧 (AI) 和機器學習 (ML) 等專門任務可能更喜歡針對這些工作負載進行最佳化的處理器。

- CPU 處理器是資料中心中最常見的處理器類型。它用途廣泛且適應性強,可以處理各種任務和應用。 GPU 處理器最初是為圖形密集型應用程式設計的,由於其並行處理能力,它已成為資料中心的必需品。 GPU 執行高度並行運算,使其適用於機器學習、人工智慧和巨量資料分析。配備大量核心,可同時處理大量資料,顯著減少處理時間並提高整體效能。

- FPGA 處理器利用可編程硬體,可針對特定應用進行客製化。此電路可以靈活地重新配置,使其適合需要低延遲和高吞吐量的任務。 FPGA 處理器通常用於即時處理很重要的功能,例如加密、視訊處理和網路封包處理。

- 隨著連網型設備、雲端運算和物聯網的激增,產生的資料量正以前所未有的速度成長。資料的激增需要強大的處理器來滿足資料中心的處理和分析要求。此外,資料中心還負責處理和分析大量即時資料。隨著對資料主導的洞察和複雜運算的越來越依賴,處理器需要提供高效能並有效地處理要求苛刻的工作負載。

- 此外,能源效率是資料中心處理器的關鍵市場促進因素。資料中心消耗大量能源,最佳化電力消耗對於降低營運成本和環境影響至關重要。對具有更高每瓦性能的處理器的需求不斷增加,以實現更有效率的資料中心營運。此外,人工智慧 (AI) 和機器學習 (ML) 技術的日益普及正在推動對具有增強處理人工智慧工作負載能力的處理器的需求。人工智慧和機器學習演算法需要強大的處理器來處理和分析複雜的資料模式並做出準確的預測,從而增加了對人工智慧工作負載進行最佳化的專用處理器的需求。

- GDP 成長是影響資料中心處理器市場的主要宏觀經濟趨勢之一。隨著經濟的擴張,企業往往會增加對資料中心等IT基礎設施的投資。隨著企業需要更多的運算能力來處理不斷成長的資料量,這種投資的增加意味著對資料中心處理器的需求增加。例如,美國是一個重要的資料中心市場。根據經濟分析局(BEA)預測,美國GDP將從2022年的25.7兆美元增加到2023年的約27.36兆美元。

- 然而,資料中心處理器市場面臨著幾個阻礙其成長和潛力的市場限制因素。資料中心處理器的高成本是中小型企業的主要障礙,限制了它們的採用。此外,行業技術的快速進步導致處理器生命週期縮短,使公司難以跟上最新的創新。

資料中心處理器市場趨勢

中央處理器(CPU)領域預計將推動市場成長

- CPU資料中心處理器,也稱為伺服器處理器,是資料中心運作的關鍵元件。這些處理器專為處理資料中心環境的嚴苛工作負載和高效能要求而設計。 CPU資料中心處理器的主要特徵之一是其高核心數量。這些處理器通常具有多個核心,從 8 個到 64 個或更多。這實現了任務並行性,允許資料中心同時處理不同的工作負載。此外,高核心數量可實現高效的資源利用,並最大限度地提高資料中心的整體效能。

- 另一個重要特徵是CPU資料中心處理器的高時脈速度。時脈速度是處理器執行指令的速度。更快的時脈速度意味著更快的資料處理,這對於需要即時處理大量資料的資料中心至關重要。此外,CPU資料中心處理器通常包含 Turbo Boost 技術,該技術允許它們在需要額外效能時暫時提高時脈速度。

- 此外,CPU資料中心處理器旨在支援虛擬。虛擬可讓您在單一實體伺服器上執行多個虛擬機,從而最大限度地提高資源利用率並降低硬體成本。 CPU資料中心處理器包括硬體輔助虛擬等功能,以提高虛擬環境的效能和安全性。

- 市場促進因素之一是行動裝置、社群媒體和物聯網等各種資訊來源產生的資料快速增加。即時處理和分析大量資料需要強大的高效能處理器。隨著資料處理市場的持續成長,資料中心營運商被迫投資先進的 CPU 處理器,以滿足不斷成長的運算需求。

- 雲端處理服務的快速擴張預計也將顯著推動市場成長。雲端平台提供擴充性、靈活性和成本效率,這使得它們對許多企業至關重要。為了滿足對雲端服務不斷成長的需求,資料中心需要部署能夠處理繁重工作負載並提供最佳效能的處理器。因此,始終需要更強大、更節能的 CPU 處理器來滿足雲端處理不斷變化的需求。

- 據 Cloudscene 稱,截至 2024 年 3 月,美國據報道擁有 5,381 個資料中心,比世界上任何其他國家都多。另外 521 個地點位於德國,514 個地點位於英國。幾個地區對資料中心的投資增加似乎正在推動市場成長。例如,2023年10月,Vantage Data Centers完成了對歐洲多個資料中心資產的投資交易。該公司宣布已與 DigitalBridge、Infranity 和 MEAG 領導的投資者聯盟完成投資合作。該投資合作夥伴由六個穩定的歐洲資料中心組成,價值約27億美元,其中包括Vantage的股權。

北美佔最大市場佔有率

- 由於技術進步、資料密集型應用程式的激增以及對高效能運算的需求,美國資料中心處理器市場正在經歷顯著成長。隨著企業轉向雲端基礎的解決方案,北美對強大資料中心的需求不斷增加。這增加了對能夠處理不斷成長的資料量並提供無縫性能的強大處理器的需求。

- 美國擴大採用網際網路、人工智慧、5G、物聯網和高效能運算等先進技術,需要高資料傳輸速度,這正在推動市場成長。根據軟體即服務解決方案公司和線上媒體監控公司 Meltwater 的數據,截至 2023 年 10 月,美國的網路普及率為 91.8%。

- 資料中心消耗大量能源,增加了營運成本和環境問題。因此,人們關注的是能夠在不影響效能的情況下最佳化功耗的節能處理器。

- 資料中心採用異質運算架構來滿足人工智慧和機器學習等新興技術的區域需求。這一趨勢整合了 CPU、GPU 和專用加速器,以提供卓越的效能和靈活性。

- 資料流量的爆炸性成長對開發多個資料中心以支援企業和消費者產生的資料的需求不斷成長。雲端處理服務和應用程式的使用將在美國繼續擴大,從而導致大規模超大規模雲端為基礎的資料中心的發展。

- 多家公司正在該地區投資資料中心擴容,以支持光收發器市場的擴張。例如,亞馬遜在2023年9月宣布將投資35億美元在美國俄亥俄州新奧爾巴尼新建五個資料中心。據悉,這些將於2030年完成。五個資料中心和配套建築的建設計劃於 2025 年開始。這項投資是亞馬遜承諾斥資 78 億美元擴建該州資料中心的第一部分。該協議是在 Google 最近宣布斥資 17 億美元擴建新奧爾巴尼三個資料中心的計劃之後達成的。

資料中心處理器產業概述

在資料中心處理器市場,英特爾公司、NVIDIA公司、Advanced Micro Devices Inc.、Xilinx Inc.和Arm Holdings PLC等主要企業正向半固體過渡。研究市場中的參與者不斷努力創新先進產品,以滿足消費者不斷變化的需求。

2024 年 2 月:Nvidia 宣布提高 GPU 產量,以推動 AI資料中心革命。該公司已開始針對 Google 新發布的 Gemma 系列輕量級模型進行最佳化。兩家公司開發了架構提高在 Nvidia資料中心、雲端和 GPU 支援的 PC 上運行的模型的效能。 Nvidia H200 處理器的首批庫存預計將於 2024 年末出貨。

2023 年 12 月:英特爾在紐約舉行的 AI Everywhere 活動上宣布推出第五代 Xeon 可擴充處理器。英特爾於 2023 年 1 月發布了第四代英特爾至強處理器,但為了跟上競爭對手的步伐,它發布了第五代晶片,代號為“Emerald Rapids”。與上一代Xeon 處理器Sapphire Rapids 相比,這些新處理器的運算效能平均提高了21%,記憶體速度平均提高了16%,從而降低了各種客戶工作負載的平均每瓦效能,英特爾聲稱可以提高這些性能。英特爾表示,這使其成為最具永續的資料中心處理器,能夠執行處理器密集任務,同時消耗更少的電力。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 技術簡介

- 深度學習、公共雲端介面和企業介面如何影響資料中心加速器

- 各廠商的技術更新/開發狀況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 消費者議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

- COVID-19 和其他宏觀經濟因素對市場的影響

- 基於設定的市場場景 - 內部部署與雲

第5章市場動態

- 市場促進因素

- HPC資料中心更常採用人工智慧

- 資料中心設施和雲端基礎服務部署的增加

- 市場限制因素

- 有限的人工智慧硬體專業知識和基礎設施問題

第6章 市場細分

- 按處理器

- CPU(中央處理單元)

- GPU(圖形處理單元)

- FPGA(現場可程式化閘陣列)

- ASIC(專用積體電路)- 僅 AI專用加速器

- 網路加速器(SmartNIC、DPU)

- 按用途

- 人工智慧(深度學習、機器學習)

- 資料分析/圖形

- 高效能運算 (HPC)/科學運算

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- Intel Corporation

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Xilinx Inc.

- Arm Holdings PLC

- Super Micro Computer Inc.

- Samsung Electronics Co. Ltd

- Qualcomm Technologies Inc.

- Imagination Technologies Limited

- Advantech Co. Ltd

第8章投資分析

第9章 市場的未來

The Data Center Processor Market size is estimated at USD 11.98 billion in 2024, and is expected to reach USD 17.45 billion by 2029, growing at a CAGR of 7.80% during the forecast period (2024-2029).

Key Highlights

- A data center processor is a critical component of a data center's computing infrastructure. It is a high-performance chip that performs various tasks, including arithmetic, logic, and input/output operations. Data centers rely on servers, which are high-performance computers with large storage space, memory, processing power, and input/output capabilities. These servers use data center processors to handle the computational workload and run applications. The choice of processors in a data center depends on the specific tasks and requirements. General-purpose CPUs may be suitable for many applications, but processors optimized for these workloads may be preferred for specialized tasks like artificial intelligence (AI) and machine learning (ML).

- CPU processors are the most common type of processors found in data centers. They provide the capability to handle various tasks and applications, making them versatile and adaptable. Initially designed for graphics-intensive applications, GPU processors have become indispensable in data centers due to their parallel processing capabilities. GPUs perform highly parallel computations, making them suitable for machine learning, artificial intelligence, and big data analytics. Their massive number of cores enables them to process vast amounts of data simultaneously, significantly reducing processing time and improving overall performance.

- FPGA processors offer the advantage of programmable hardware, allowing customization to specific applications. They provide the flexibility to reconfigure their circuitry, making them suitable for tasks that require low latency and high throughput. FPGA processors are often used for functions such as encryption, video processing, and network packet processing, where real-time processing is crucial.

- With the proliferation of connected devices, cloud computing, and the Internet of Things, the amount of data being generated is increasing at an unprecedented rate. This surge in data necessitates powerful processors that can handle data centers' processing and analysis requirements. Further, data centers are responsible for processing and analyzing vast real-time data. As industries increasingly rely on data-driven insights and complex computations, processors must deliver high performance and efficiently handle demanding workloads.

- Moreover, energy efficiency is a significant market driver for data center processors. Data centers consume enormous amounts of energy, and optimizing power consumption is crucial for reducing operational costs and environmental impact. Processors that offer higher performance per watt are in high demand as they allow for more efficient data center operations. Moreover, the increasing adoption of artificial intelligence (AI) and machine learning (ML) technologies is driving the demand for processors with enhanced capabilities in handling AI workloads. AI and ML algorithms require powerful processors to process and analyze complex data patterns and make accurate predictions, driving the need for specialized processors optimized for AI workloads.

- One of the key macroeconomic trends that can affect the data center processors market is GDP growth. As the economy expands, companies are inclined to increase their investments in IT infrastructure, such as data centers. This increased investment leads to a higher demand for data center processors, as businesses require more computing power to handle the growing volume of data. For instance, the United States is a prominent data center market. According to the Bureau of Economic Analysis (BEA), the US GDP increased from USD 25.7 trillion in 2022 to about USD 27.36 trillion in 2023.

- However, the data center processor market faces several market restraints that can hinder its growth and potential. The high cost of data center processors is a significant barrier for small and medium-sized businesses, limiting their adoption. Additionally, the rapid technological advancements in the industry lead to a shorter lifecycle of processors, making it challenging for businesses to keep up with the latest innovations.

Data Center Processor Market Trends

The Central Processing Unit (CPU) Segment is Expected to Drive the Growth of the Market

- CPU data center processors, also known as server processors, are a crucial component in the functioning of data centers. These processors are specifically devised to handle the demanding workload and high-performance requirements of data center environments. One of the primary features of CPU data center processors is their high core count. These processors often have multiple cores, ranging from 8 to 64 or more. This allows for parallel processing of tasks, enabling data centers to handle various workloads simultaneously. The high core count also ensures efficient resource utilization, maximizing the data center's overall performance.

- Another essential feature is the high clock speed of CPU data center processors. Clock speed refers to how fast a processor can execute instructions. Higher clock speeds result in faster data processing, which is crucial for data centers that need to handle large amounts of data in real time. Additionally, CPU data center processors often have turbo boost technology, temporarily increasing the clock speed when additional performance is required.

- Also, CPU data center processors are designed to support virtualization. Virtualization facilitates multiple virtual machines to run on a single physical server, maximizing resource utilization and reducing hardware costs. CPU data center processors include features like hardware-assisted virtualization, improving virtualized environments' performance and security.

- One of the primary market drivers is the exponential growth of data generated by various sources like mobile devices, social media, and the Internet of Things. This vast amount of data must be processed and analyzed in real time, requiring powerful, high-performance processors. As the market for data processing continues to grow, data center operators are compelled to invest in advanced CPU processors to meet the increasing computational requirements.

- The rapid expansion of cloud computing services is also anticipated to drive market growth significantly. Cloud platforms have become essential to many businesses, offering scalability, flexibility, and cost-efficiency. To support the growing demand for cloud services, data centers must deploy processors that can handle the heavy workloads and provide optimal performance. As a result, there is a constant need for more robust and energy-efficient CPU processors to cater to the evolving requirements of cloud computing.

- According to Cloudscene, as of March 2024, there were a reported 5,381 data centers in the United States, the most of any country worldwide. A further 521 were in Germany, while 514 were in the United Kingdom. The increasing investments in data centers in several regions are likely to aid the growth of the market. For instance, in October 2023, Vantage Data Centers closed an investment deal for several European data center assets. The company announced it had completed an investment partnership with DigitalBridge and a consortium of investors led by Infranity and MEAG. The investment partnership initially comprises six stabilized European data centers and is valued at approximately USD 2.7 billion, including Vantage's stake.

North America Holds the Largest Market Share

- The American data center processor market has experienced substantial growth due to technological advancements, the proliferation of data-intensive applications, and the need for high-performance computing. The migration of businesses to cloud-based solutions has fueled the demand for robust data centers in North America. This has driven the need for powerful processors that can handle the increasing volume of data and provide seamless performance.

- The high adoption of the Internet and advanced technologies like AI, 5G, IoT, and high-performance computing in the United States is driving the need for a high data transmission rate, which drives the market's growth. According to Meltwater, a software-as-a-service solution company and an online media monitoring company, as of October 2023, the internet penetration rate in the United States was 91.8%.

- Data centers consume large amounts of energy, resulting in heightened operational costs and environmental concerns. As a result, there is a rising emphasis on energy-efficient processors that can optimize power consumption without compromising performance.

- Data centers are embracing heterogeneous computing architectures to meet the region's requirements of emerging technologies like AI and machine learning. This trend has led to the integration of CPUs, GPUs, and specialized accelerators, offering superior performance and flexibility.

- The upsurge in data traffic has created elevated demand for developing several data centers that support data generated by businesses and consumers. The use of cloud-computing services and applications will continue to grow in the US, leading to the development of large hyperscale cloud-based data centers.

- Several companies are investing in data center capacity expansions in the region, thereby driving the expansion of the optical transceiver market. For instance, in September 2023, Amazon announced it would invest USD 3.5 billion in five new data centers in New Albany, Ohio, United States. It is reported that they will be finished by 2030. The construction is set to commence in 2025 on the five data centers and supporting buildings. The investment is claimed to be an initial part of Amazon's USD 7.8 billion commitment to expand data centers in the state. The agreement follows Google's recent announcement of a planned USD 1.7 billion expansion of its three data centers in New Albany.

Data Center Processor Industry Overview

The data center processor market is semi-consolidated with significant players like Intel Corporation, NVIDIA Corporation, Advanced Micro Devices Inc., Xilinx Inc., and Arm Holdings PLC. The players in the studied market are striving to constantly innovate advanced products to cater to the evolving needs of consumers.

February 2024: Nvidia announced that it ramped up GPU production to fuel the AI data center revolution. The company launched optimizations for Google's newly released Gemma family of lightweight models. The two companies developed architecture to accelerate the model's performance running in Nvidia data centers, in the cloud, and on GPU-enhanced PCs. The initial stock of Nvidia's H200 processors is set to ship in the second half of 2024.

December 2023: Intel launched its 5th-generation Xeon Scalable processors at the AI Everywhere event in New York. Intel released the fourth generation of its Intel Xeon processors in January 2023, but to keep pace with its competitors, it has unveiled the fifth generation of the chips, also known by its code name Emerald Rapids. These new processors offer a 21% average compute performance gain and 16% better memory speeds than the previous generation of Xeon processors, Sapphire Rapids, enabling 36% higher average performance per watt across a diverse range of customer workloads - Intel claims. This would facilitate users' undertaking processor-intensive tasks while utilizing less overall power, with Intel describing them as their most sustainable data center processors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technology Snapshot

- 4.2.1 Impact of Deep Learning, Public Cloud Interface, and Enterprise Interface on Data Center Accelerators

- 4.2.2 Technological Updates/Developments by Various Vendors

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.6 Market Scenario Based on the Setup - On-premise vs Cloud

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Deployment of AI in HPC Data Centers

- 5.1.2 Increasing Deployment of Data Center Facilities and Cloud-based Services

- 5.2 Market Restraints

- 5.2.1 Limited AI Hardware Experts and Infrastructural Concerns

6 MARKET SEGMENTATION

- 6.1 By Processor

- 6.1.1 CPU (Central Processing Unit)

- 6.1.2 GPU (Graphics Processing Unit)

- 6.1.3 FPGA (Field-programmable Gate Array)

- 6.1.4 ASIC (Application-specific Integrated Circuit) - Only AI-dedicated Accelerators

- 6.1.5 Networking Accelerators (SmartNIC and DPUs)

- 6.2 By Application

- 6.2.1 Artificial Intelligence (Deep Learning and Machine Learning)

- 6.2.2 Data Analytics/Graphics

- 6.2.3 High-performance Computing (HPC)/Scientific Computing

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 NVIDIA Corporation

- 7.1.3 Advanced Micro Devices Inc.

- 7.1.4 Xilinx Inc.

- 7.1.5 Arm Holdings PLC

- 7.1.6 Super Micro Computer Inc.

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 Qualcomm Technologies Inc.

- 7.1.9 Imagination Technologies Limited

- 7.1.10 Advantech Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年深度學習晶片組全球市場報告2025 年深度學習全球市場報告

2025年深度學習晶片組全球市場報告2025 年深度學習全球市場報告 全球交通號誌辨識市場深度學習市場規模、佔有率、趨勢分析報告:按解決方案、應用、最終用途、地區和細分市場預測,2025 年至 2030 年

全球交通號誌辨識市場深度學習市場規模、佔有率、趨勢分析報告:按解決方案、應用、最終用途、地區和細分市場預測,2025 年至 2030 年 深度學習:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

深度學習:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 深度學習市場規模、佔有率、成長分析,按產品、按應用、按最終用戶行業、按地區 - 行業預測,2024-2031 年藥物研發·診斷的Deep學習市場:各治療領域,各主要地區:到2035年前的產業趨勢與全球預測

深度學習市場規模、佔有率、成長分析,按產品、按應用、按最終用戶行業、按地區 - 行業預測,2024-2031 年藥物研發·診斷的Deep學習市場:各治療領域,各主要地區:到2035年前的產業趨勢與全球預測 Deep學習的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

Deep學習的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年) 深度學習市場:按類型、最終用戶、應用分類 - 2025-2030 年全球預測深度學習晶片組市場:按類型、最終用戶分類 - 2025-2030 年全球預測

深度學習市場:按類型、最終用戶、應用分類 - 2025-2030 年全球預測深度學習晶片組市場:按類型、最終用戶分類 - 2025-2030 年全球預測