|

市場調查報告書

商品編碼

1550011

半導體耗材:市場佔有率分析、產業趨勢、成長預測(2024-2029)Semiconductor Consumables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

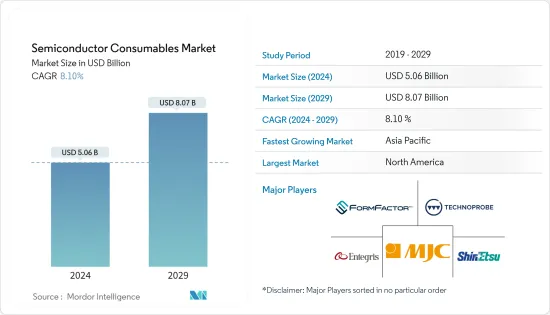

2024年半導體耗材市場規模預估為50.6億美元,預估2029年將達80.7億美元,預測期內(2024-2029年)複合年成長率為8.10%。

主要亮點

- 半導體消耗品是用於半導體製造和檢查過程的材料和零件。這些消耗品對於半導體製造至關重要,並且通常是製造中使用的一次性或可更換零件。它對於確保半導體製造的品質和效率發揮重要作用。半導體廣泛應用於多種產業,包括電腦、行動電話、汽車技術和消費性電子產品。半導體產業對全球經濟至關重要,是經濟整體健康狀況的指標。隨著半導體需求的增加,對可靠、高品質消耗品的需求持續成長。

- 半導體消耗品包括製造過程中使用的各種材料和零件。半導體消耗品的例子包括電極、聚焦環、刀片、墊圈和其他需要經常更換的零件。這些消耗品與機械和設備一起使用,以有效生產半導體。

- 技術進步一直是半導體耗材產業的主要驅動力。隨著對更快、更緊湊、更有效率的電子設備的需求不斷增加,半導體製造商需要先進的耗材來滿足這些不斷變化的要求。新材料、新製造技術的開拓以及人工智慧和機器學習在半導體製造過程中的整合可能會為所研究市場的成長提供利潤豐厚的機會。

- 包括酸、氫氧化物和過氧化物在內的濕化學物質用於清洗和蝕刻半導體產業中的基板表面。這些製程對於半導體製造和濕式剝離至關重要。半導體製造過程需要清潔的環境,而濕化學品在保持這種清潔度方面發揮著重要作用。過氧化氫等化學物質用於蝕刻和清洗積體電路 (IC) 等長期應用。

- 新的半導體製造設施的建設也將刺激對半導體耗材的需求。隨著這些設施產能的提高,所研究市場的需求預計將迅速增加。例如,2024年3月,印度聯合內閣批准了為三座半導體工廠提供1.26兆印度盧比(150.7億印度盧比)的資金,其中包括塔塔集團在古吉拉特邦多萊拉建設印度首個大型晶片製造工廠的提案,核准投資額達1000萬美元。塔塔電子公司與台灣力晶半導體製造公司 (PSMC) 合作在多拉建造的半導體工廠將採用 28 奈米技術製造高性能計算晶片。

- 半導體耗材產業面臨多種市場限制因素,影響其成長和盈利。主要阻礙因素之一是半導體耗材製造所使用的原料高成本。這增加了整體製造成本,並使公司難以保持有競爭力的價格。此外,該產業高度依賴半導體市場,而半導體市場則受週期性需求模式和經濟波動的影響。這種波動可能會導致對消耗品的需求不可預測,並影響收益流。

- 此外,俄羅斯和烏克蘭之間的衝突可能會對半導體產業產生重大影響。這場爭端已經加劇了已經影響半導體產業的半導體供應鏈問題和晶片短缺問題。這種干擾可能導致鎳、鈀、銅、鈦和鋁等關鍵原料的價格波動,進而導致材料短缺。結果,半導體製造可能會受到影響。

半導體耗材市場趨勢

濕化學品領域可望推動市場成長

- 半導體技術在很大程度上依賴半導體材料的精確操縱和製造。半導體製造的重要方面之一是濕化學品用於各種消耗品。這些化學品對於半導體表面的清洗、蝕刻和鈍化非常重要,可確保高品質、無缺陷的裝置。

- 濕化學品廣泛應用於半導體製造的清洗過程。半導體晶圓是晶片製造的主要基板,通常含有先前加工步驟產生的雜質、污染物和殘留物。濕式化學清洗可去除這些雜質,並確保後續製造步驟的原始起點。硫酸、過氧化氫和去離子水等各種化學物質用於去除某些類型的污染物。

- 蝕刻是半導體製造的重要步驟,用於選擇性地從晶圓表面去除材料層。濕蝕刻使用的化學物質可以選擇性地溶解某些材料而不影響其他材料。例如,氫氟酸通常用於蝕刻二氧化矽,而氫氧化鉀和硝酸等其他化學物質則用於不同的材料。蝕刻過程的精確控制對於實現所需的裝置結構和尺寸至關重要。

- 隨著半導體製造中濕化學品的使用增加,適當的化學廢棄物管理變得非常重要。使用過的化學品的處置需要遵守嚴格的環境法規,以盡量減少對生態的影響。採用回收和治療過程從廢棄物中回收有價值的成分,並減少對環境的負面影響和整體生產成本。

- 由於多種因素,包括家用電子電器、計算、5G 和汽車半導體的強勁成長,半導體需求正在上升。半導體需求的成長與製造過程中使用的濕化學品需求的成長直接相關。

- 根據愛立信2023年行動報告,從年終到2029年,全球5G用戶數預計將成長330%以上,從16億成長到53億。預計到 2023年終, 5G 覆蓋率將覆蓋全球人口的 45% 以上,到 2029年終85%。預計到年終,北美和波灣合作理事會的5G滲透率將達到92%,是地區最高的。西歐預計將緊隨其後,滲透率達到 85%。

- 此外,愛立信預計,2022年全球智慧型手機行動網路用戶數量預計將達到約66億,2028年將超過78億人。預計這將進一步推動市場研究。

預計亞太地區市場成長率較高

- 台灣在亞太地區的半導體製造中發揮著重要作用。台灣半導體產業的成功很大程度得益於政府的正面作用。台灣政府實施了各種政策和措施來促進半導體產業的成長。

- 其中之一是“產業進步和轉型計劃”,旨在透過投資研發、人才引進和基礎設施發展來增強台灣半導體產業的競爭力。政府也向國內半導體公司提供稅收優惠、補貼和財政支持,鼓勵它們投資創新和全球企業發展。

- 台灣半導體企業在半導體耗材市場不斷創新先進產品與工藝,引領產業技術進步。台灣企業已成功開發實施7奈米、5奈米等先進晶片製造技術,有利於生產更小、更快、更節能的晶片。這些先進的半導體製造能力使台灣在全球市場上具有競爭優勢。

- 此外,業界在人工智慧、物聯網(IoT)和自動駕駛汽車等新興技術專用晶片的開發方面取得了重大進展,這將進一步支持台灣半導體耗材供應商的成長。

- 台積電(台積電)、聯發科、聯電(聯華)等台灣企業已成為全球半導體供應鏈的重要參與者。特別是,台積電已成為全球最大的合約晶片製造商之一,為全球知名科技公司提供產品。

- 領先半導體公司的存在可能會推動台灣調查市場的擴張。此外,台灣半導體產業也利用其強大的供應鏈來獲得競爭優勢。台灣已經建立了從設計到製造、測試和封裝的垂直整合生態系統。這種整合提高了靈活性和成本效率,使台灣成為對世界各地半導體公司有吸引力的目的地。

- 亞太地區電子設備產量和需求的增加可能會推動研究市場的成長。例如,中國是世界領先的家用電器生產國之一。該國製造業蓬勃發展,並引進了多項製造和通訊技術。

半導體耗材產業概況

半導體耗材市場是一個競爭激烈的市場,有幾家主要公司,包括 FormFactor Inc.、Technoprobe SpA、Micronics Japan、Entegris Inc. 和 Shin-Etsu Polymer。市場參與企業正在透過大量的研發投資、合作和合併來創新新產品,以滿足消費者不斷變化的需求。

- 2023 年11 月領先的自動化測試解決方案供應商泰瑞達(Teradyne) 和領先的探針卡設計商和製造商Techno-Probe 將加速各自發展,為全球帶來更高性能的半導體測試介面,我們已宣布達成一系列戰略協議。作為合作關係的一部分,泰瑞達將向Technoprobe投資約5.16億美元,而Technoprobe將以8,500萬美元收購泰瑞達的設備介面解決方案業務。兩家公司也將致力於聯合開發計劃。

- 2023年8月Technoprobe完成對Harbor Electronics的收購。 Harbour Electronics 於 1980 年代在加利福尼亞州聖克拉拉成立,是一家為著名半導體製造商生產用於測試系統的先進印刷電路基板的著名製造商。 Techno-Probe表示,此次收購將進一步增強技術力,垂直整合探針卡製造程序,並引入內部基板製造專業知識。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 技術進步

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 消費者議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 新進入者的威脅

- COVID-19 後遺症和其他宏觀經濟因素對市場的影響

- 產業供應鏈分析

第5章市場動態

- 市場促進因素

- 對特定類別 IC 的需求增加

- 市場限制因素

- 特定細分市場的需求不確定性與供應鏈不確定性

第6章 市場細分

- 按產品類型

- 濕化學品(包括酸、鹼、相關混合物和有機物)

- 晶圓運輸貨櫃

- 晶圓加工(晶圓盒、FOUP、FOSB 盒等)

- 測試耗材

- 探針卡(垂直、MEMS、懸臂、等特殊產品)

- 插座(老化、測試)

- 末端執行器

- 按地區

- 北美洲

- 台灣

- 中國

- 韓國

- 日本

- 歐洲

- 東南亞

第7章 競爭格局

- 公司簡介

- FormFactor, Inc.

- Technoprobe SpA

- Micronics Japan Co., Ltd.

- Japan Electronic Materials(JEM)

- MPI Corporation

- Entegris, Inc.

- Shin-Etsu Polymer Co., Ltd.

- Miraial Co Ltd

- 3s Korea Co.,Ltd.

- Dainichi Shoji KK

第8章 廠商排名分析

第9章市場的未來

The Semiconductor Consumables Market size is estimated at USD 5.06 billion in 2024, and is expected to reach USD 8.07 billion by 2029, growing at a CAGR of 8.10% during the forecast period (2024-2029).

Key Highlights

- Semiconductor consumables are materials or components used in semiconductors' manufacturing and testing processes. These consumables are essential for producing semiconductors and are often disposable or replaceable parts used in fabrication. They play a crucial role in ensuring the quality and efficiency of semiconductor production. Semiconductors are widely used in various industries, including computers, mobile phones, automotive technologies, and consumer electronics. The semiconductor industry is an essential part of the global economy and serves as an indicator of the economy's overall health. As the demand for semiconductors increases, the need for reliable and high-quality consumables becomes increasingly essential.

- Semiconductor consumables can include various materials and components employed in the manufacturing process. Some examples of semiconductor consumables are electrodes, focus rings, blades, gaskets, and other parts that need frequent replacement. These consumables are used with machinery and equipment to ensure efficient production of semiconductors.

- Technological advancements serve as a key driver for the semiconductor consumables industry. As the demand for faster, compact, and more efficient electronic devices increases, semiconductor manufacturers require advanced consumables to meet these evolving requirements. The development of new materials, novel fabrication techniques, and the integration of artificial intelligence and machine learning in semiconductor manufacturing processes are likely to offer lucrative opportunities for the growth of the market studied.

- Wet chemicals, including acids, hydroxides, and peroxides, are used for cleaning and etching substrate surfaces in the semiconductor industry. These processes are essential for the fabrication and wet stripping of semiconductors. The manufacturing process of semiconductors requires a clean environment, and wet chemicals play a crucial role in maintaining this cleanliness. Chemicals like hydrogen peroxide are used for long-term applications such as etching and cleaning integrated circuits (ICs).

- The establishment of new semiconductor manufacturing facilities also drives the demand for semiconductor consumables. As these facilities increase their production capacity, the demand for the studied market is expected to increase rapidly. For instance, in March 2024, the Union Cabinet of India approved INR 1.26 trillion (USD 15.07 billion) worth of investments in three semiconductor plants, including a Tata Group proposal to build the country's first major chip fabrication facility at Dholera in Gujarat. The semiconductor fabrication unit in Dholera by Tata Electronics, in partnership with Powerchip Semiconductor Manufacturing Corp (PSMC), Taiwan, would manufacture high-performance computing chips with 28 nm technology.

- The semiconductor consumables industry faces several market restraints that impact its growth and profitability. One major restraint is the high cost of raw materials used in the manufacturing of semiconductor consumables. This increases the overall production cost, making it difficult for companies to maintain competitive pricing. Additionally, the industry is highly dependent on the semiconductor market, which is subject to cyclical demand patterns and economic fluctuations. This volatility can lead to unpredictable demand for consumables, affecting revenue streams.

- Further, the conflict between Russia and Ukraine will significantly impact the semiconductor industry. The conflict has already exacerbated the semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may result in volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, and aluminum, resulting in material shortages. This, in turn, could impact the manufacturing of semiconductors.

Semiconductor Consumables Market Trends

The Wet Chemicals Segment is Expected to Drive the Market's Growth

- Semiconductor technology relies heavily on the precise manipulation and fabrication of semiconductor materials. One critical aspect of semiconductor manufacturing is the use of wet chemicals in various consumables. These chemicals are important in cleaning, etching, and passivating semiconductor surfaces, ensuring high-quality, defect-free devices.

- Wet chemicals are extensively used in the cleaning processes of semiconductor manufacturing. Semiconductor wafers, the primary substrates for chip production, often have impurities, contaminants, and residue from previous processing steps. Wet chemical cleaning removes these impurities and ensures a pristine starting point for subsequent fabrication steps. Different chemicals, such as sulfuric acid, hydrogen peroxide, and deionized water, are used to remove specific types of contaminants.

- Etching is an essential step in semiconductor manufacturing, used to remove layers of material from the wafer surface selectively. Wet etching involves using chemicals that can selectively dissolve specific materials without affecting others. For instance, hydrofluoric acid is commonly used to etch silicon dioxide, while other chemicals like potassium hydroxide or nitric acid are used for different materials. Precise control of the etching process is essential to achieve desired device structures and dimensions.

- Proper chemical waste management becomes critical with the increasing use of wet chemicals in semiconductor manufacturing. The disposal of spent chemicals requires adherence to strict environmental regulations to minimize ecological impact. Recycling and treatment processes are employed to recover valuable components from the waste, reducing environmental harm and overall production costs.

- The demand for semiconductors has been on the rise, driven by various factors such as robust growth in consumer electronics, computing, 5G, and automotive semiconductors. This increased demand for semiconductors directly translates into a higher demand for wet chemicals used in their manufacturing processes.

- According to Ericsson Mobility Report 2023, between the end of 2023 and 2029, global 5G subscriptions are forecasted to increase by over 330%, from 1.6 billion to 5.3 billion. 5G coverage was forecasted to be available to more than 45% of the global population by the end of 2023 and 85% by the end of 2029. North America and the Gulf Cooperation Council are anticipated to have the highest regional 5G penetration rates by the end of 2029 at 92%. Western Europe is forecasted to follow at 85% penetration.

- Moreover, according to Ericsson, the global number of smartphone mobile network subscriptions reached nearly 6.6 billion in 2022, and it is expected to exceed 7.8 billion by 2028. This is expected to drive the market studied further.

Asia-Pacific is Expected to Witness a High Market Growth Rate

- Taiwan plays a crucial role in semiconductor manufacturing in Asia-Pacific. Taiwan's semiconductor industry owes much of its success to the proactive role played by the government. The Taiwanese government has implemented a diverse range of policies and initiatives to foster the growth of the industry.

- One such initiative is the Industrial Upgrading and Transformation Plan, which aims to enhance the competitiveness of Taiwan's semiconductor industry through investments in research and development, talent acquisition, and infrastructure development. The government has also provided tax incentives, subsidies, and funding support to domestic semiconductor companies, encouraging them to invest in innovation and expand their global reach.

- Taiwanese semiconductor companies have continuously innovated advanced products and processes in the semiconductor consumables market, driving technological advancements in the industry. Advanced chip manufacturing technologies, such as 7 nm and 5 nm processes, have been successfully developed and deployed by Taiwanese firms, facilitating the production of smaller, faster, and more energy-efficient chips. The ability to manufacture these advanced semiconductors has given Taiwan a competitive edge in the global market.

- Additionally, the industry has witnessed substantial progress in the development of specialized chips for emerging technologies like artificial intelligence, the Internet of Things (IoT), and autonomous vehicles, which are further driving the growth of Taiwanese semiconductor consumables vendors.

- Taiwanese companies, such as TSMC (Taiwan Semiconductor Manufacturing Company), MediaTek, and UMC (United Microelectronics Corporation), have become critical players in the global semiconductor supply chain. TSMC, in particular, has emerged as one of the world's largest contract chipmakers, catering to prominent global technology companies.

- The presence of major semiconductor companies is likely to aid the expansion of the market studied in the country. Moreover, Taiwan's semiconductor industry has leveraged its robust supply chain to gain a competitive advantage. The country has developed a vertically integrated ecosystem, encompassing everything from design and manufacturing to testing and packaging. This integration allows for greater flexibility and cost-effectiveness, making Taiwan an attractive destination for semiconductor companies worldwide.

- The increasing electronics production and demand in Asia-Pacific are likely to drive the growth of the market studied. For instance, China is one of the prominent consumer electronics producers worldwide. The manufacturing industry is growing quickly in the country and is witnessing the deployment of several manufacturing and telecommunications technologies, which is likely to aid in the market's growth.

Semiconductor Consumables Industry Overview

The semiconductor consumables market is a competitive market with the presence of several major players like FormFactor Inc., Technoprobe SpA, Micronics Japan Co. Ltd, Entegris Inc., and Shin-Etsu Polymer Co. Ltd. The market players are striving to innovate new products by way of extensive investments in R&D, collaborations, and mergers to cater to the evolving demands of consumers.

- November 2023: Teradyne Inc., a prominent supplier of automated test solutions, and Technoprobe SpA, a significant company in the design and production of probe cards, announced a series of agreements establishing a strategic partnership that is anticipated to accelerate growth for both companies and allow them to deliver higher performance semiconductor test interfaces to their global customers. As part of the partnership, Teradyne will make nearly USD 516 million in equity investment in Technoprobe, and Technoprobe will acquire Teradyne's Device Interface Solutions business for USD 85 million. The companies also claimed to engage in joint development projects.

- August 2023: Technoprobe finalized its acquisition of Harbor Electronics Inc. Harbor Electronics, a company founded in the '80s in Santa Clara, California, is a prominent manufacturer of advanced printed circuit boards for testing systems for prominent semiconductor manufacturers. As per Technoprobe, the acquisition is claimed to allow it further to strengthen its technological skills in the testing field and vertically integrate the probe card production process, bringing PCB production expertise in-house.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Advancements

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.3.6 Threat of New Entrants

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.5 Industry Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Certain Class of ICs

- 5.2 Market Restraints

- 5.2.1 Uncertainties in Demand for Certain Segments and Supply Chain Uncertainties

6 MARKET SEGMENTATION

- 6.1 By Product Category

- 6.1.1 Wet Chemicals (includes acids, basis, associated mixtures, and organics)

- 6.1.2 Wafer Shipping Containers

- 6.1.3 Wafer Processing (Cassettes, FOUP, FOSB Boxes etc.)

- 6.1.4 Test Consumables

- 6.1.4.1 Probe Card (Vertical, MEMS, Cantilever, and Other Speciality)

- 6.1.4.2 Sockets (Burn-in, and Test)

- 6.1.5 End Effectors

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Taiwan

- 6.2.3 China

- 6.2.4 South Korea

- 6.2.5 Japan

- 6.2.6 Europe

- 6.2.7 South East Asia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 FormFactor, Inc.

- 7.1.2 Technoprobe S.p.A.

- 7.1.3 Micronics Japan Co., Ltd.

- 7.1.4 Japan Electronic Materials (JEM)

- 7.1.5 MPI Corporation

- 7.1.6 Entegris, Inc.

- 7.1.7 Shin-Etsu Polymer Co., Ltd.

- 7.1.8 Miraial Co Ltd

- 7.1.9 3s Korea Co.,Ltd.

- 7.1.10 Dainichi Shoji K.K.