|

市場調查報告書

商品編碼

1624594

拉丁美洲的藥品包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Latin America Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

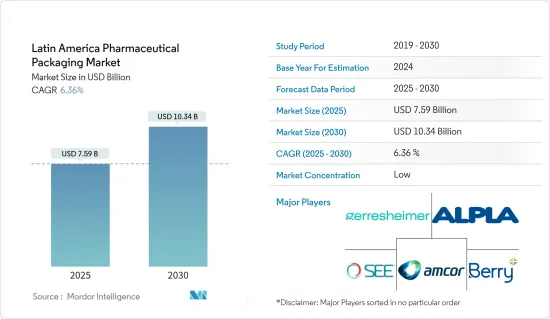

拉丁美洲藥品包裝市場規模預計到2025年為75.9億美元,預計到2030年將達到103.4億美元,預測期內(2025-2030年)年複合成長率為6.36%。

主要亮點

- 藥品包裝對於藥品整個生命週期的展示、保護、識別和遏制至關重要。輕鬆儲存、運輸和展示產品,同時確保在消費前符合監管標準。正確的包裝可以保護藥品免受各種環境因素的影響,包括氣候、生物、物理和化學條件。為了達到最佳效果,藥品包裝必須具有成本效益,並在產品的整個保存期限內提供足夠的穩定性。包裝材料和產品類型的選擇是基於藥品的特定特性,確保所選包裝提供足夠的保護、清晰的標誌並保持封裝藥品的完整性。

- 由於該地區的經濟成長和都市化,對拉丁美洲藥品包裝行業的需求正在增加。需要持續醫療照護的老年人數量不斷增加也推動了這一趨勢。隨著藥品製造業的發展勢頭,該地區的包裝供應商將能夠挖掘市場的巨大潛力。外國投資、本地生產增加和新產品開發正在促進該地區包裝產業的成長。因此,預計拉丁美洲很快將繼續成為藥品包裝的主要市場。

- 拉丁美洲的製藥業是該地區規模最大、資本最密集的產業之一。研究與開發 (R&D) 在創新藥物的開發中發揮關鍵作用,並在過去二十年中為提高拉丁美洲的預期壽命做出了貢獻。這種對研究和開發的關注導致了治療方法和治療方法的重大進步,以解決該地區特有的各種健康挑戰。

- 傳統上,拉丁美洲醫藥市場一直由西歐和美國的大型跨國公司主導。這些老字型大小企業利用其廣泛的資源、全球研究網路和先進的製造能力,在該地區保持強大的影響力。然而,近年來,該行業的新進業者開始改變這一格局。

- 這些新參與企業包括來自中國、印度和韓國的跨國公司,帶來了不同的藥物開發和製造方法。此外,拉丁美洲開發中國家正在興起專門從事學名藥和利基治療領域的本土公司。市場參與企業的多元化可以增加競爭、促進創新並改善拉丁美洲人民獲得藥物的機會。拉丁美洲不斷變化的製藥業格局為老牌公司和新興企業帶來了機會和挑戰。隨著市場的不斷發展,法規環境、智慧財產權、醫療政策等因素將在很大程度上決定該地區產業的未來。

- 拉丁美洲製藥工業協會 (ALIFAR) 是一個獨立於政府和政府間組織運作的非營利國際組織。它代表整個拉丁美洲的國家製藥公司。 ALIFAR 擁有來自 12 個拉丁美洲國家的 400 多名會員,佔該地區醫藥市場 90% 以上。 ALIFAR在維護會員企業利益、促進拉丁美洲醫藥產業發展方面發揮重要作用。 ALIFAR 促進其成員之間的合作,共用最佳實踐,並解決該地區製藥業面臨的通用挑戰。

- 人口成長、預期壽命延長和慢性病增加推動了拉丁美洲藥品需求的成長。製藥業的這些需求和技術進步與對瓶子、安瓿和其他容器等包裝解決方案不斷成長的需求直接相關。因此,拉丁美洲藥品包裝市場經歷了顯著成長。包裝材料和包裝解決方案製造商必須適應行業不斷變化的要求,包括藥品穩定性、安全性和遵守監管標準。

- 與藥品包裝原料相關的環境問題可能會限制市場,但也為該地區製藥業的包裝創新帶來了機會。人們對永續性的日益關注使得傳統包裝材料受到越來越嚴格的審查,促使製造商尋求環保的替代品。雖然這種轉變帶來了成本和法規遵循挑戰,但它也為開發新的環保包裝解決方案開闢了道路。

- 公司正在投資研發,以開發生物分解性材料、減少塑膠使用並提高藥品包裝的可回收性。這些努力是為了應對環境問題,並符合不斷變化的消費者偏好和監管要求。因此,該行業見證了創新包裝設計的激增,這些設計既保持了產品的完整性,又最大限度地減少了對環境的影響,為具有前瞻性的公司創造了新的細分市場和競爭優勢。

拉丁美洲藥品包裝市場趨勢

塑膠瓶佔較大市場佔有率

- 塑膠因其多功能性、耐用性、靈活性和永續性而廣泛應用於藥品包裝。由多種材料製成的塑膠瓶用於藥品包裝,包括聚氯乙烯、聚乙烯、聚丙烯和聚苯乙烯。該行業依靠透明、耐用且輕質的塑膠來儲存和分配。這些塑膠材質具有難以破碎、易於模製成各種形狀和尺寸、且與多種醫藥產品相容的優點。

- 此外,塑膠包裝有助於保護藥品免受濕氣、光線和污染物的影響,確保產品完整性並延長保存期限。在藥品包裝中使用塑膠也有助於提高製造和運輸的成本效益,因為它通常比玻璃或金屬等替代材料更輕、更經濟。

- 塑膠瓶廣泛用於包裝各種液體和固態藥物,如糖漿、膠囊、錠劑和眼用製劑等。製藥業青睞塑膠包裝,因為它強度大、重量輕且靈活,可以適應各種形狀和尺寸。由於技術進步以及口服固態和液體藥品擴大採用塑膠容器,醫藥塑膠瓶市場正在擴大。

- 用於製藥應用的塑膠必須無毒、非致癌性、生物相容且對生物環境無害。這些嚴格的要求確保了藥品的安全性和有效性。在藥物開發過程中,進行了嚴格的測試,以確保PET包裝材料不會浸出或提取到藥物中。此測試對於防止包裝和藥物內容物之間的污染和交互作用非常重要。 寶特瓶提供有效的防油層,防止運送過程中化學物質溢出。這種阻隔性能對於維持液體藥物的完整性和防止外部污染非常重要。此外,PET 包裝耐用且不易破損,這是可能暴露於各種處理和運輸條件下的藥品容器的基本品質。

- 藥用塑膠瓶的需求不斷增加,影響了拉丁美洲塑膠瓶市場的估值。 2023年,拉丁美洲和加勒比海地區藥品出口總合達到約93億美元,創下分析期間該地區藥品出口額的最高水準。 2022年,墨西哥將在藥品出口方面領先拉丁美洲國家。此外,據預測,擴大採用含營養藥物可能會促進固態包裝的成長。公眾對營養強化以維持人體營養平衡的認知的提高預計將推動該地區營養食品的消費並推動對塑膠瓶的需求。

- 有眼疾的人通常會使用滴管瓶。這些專用容器可以精確計量眼科藥物和溶液。 Gerresheimer 等公司為各種應用提供醫藥塑膠包裝,包括固態、液體和眼科產品。該公司的產品範圍包括用於液體製劑和眼藥水的 寶特瓶。這些瓶子旨在滿足儲存和分配眼科藥物的特定要求,確保正確劑量並保持產品完整性。隨著該地區眼睛相關疾病的盛行率持續上升,滴管瓶在眼科應用中的使用變得越來越重要。

墨西哥預計將經歷顯著成長

- 墨西哥是拉丁美洲醫藥市場佔有率的主要貢獻者。作為該地區製藥業的成熟市場,墨西哥正在經歷許多產品創新,特別是在藥品包裝方面。這項創新由遍布墨西哥的大型供應商提供支援。在強大的醫療保健系統以及對學名藥和品牌藥品不斷成長的需求的支持下,墨西哥的藥品市場正在穩步成長。

- 該國的戰略定位和北美自由貿易組織(NAFTA)貿易協定(現為 USMCA)等貿易協定進一步使其成為該地區製藥領域的重要參與者。最近的趨勢包括墨西哥的藥物研發活動增加,國內外公司投資當地設施。這增加了高品質、具有成本效益的藥品的產量,並進一步鞏固了墨西哥在拉丁美洲藥品市場的地位。

- 墨西哥製藥業的包裝產業尤其充滿活力。該領域的創新重點是提高藥物安全性、延長保存期限和提高患者依從性。這些先進的包裝包括智慧包裝解決方案、環保材料以及滿足不同病患小組需求的設計。儘管面臨監管複雜性和來自其他新興市場的競爭等挑戰,墨西哥製藥業仍在不斷發展和適應。憑藉對創新的承諾和成熟的製造能力,墨西哥在拉丁美洲製藥市場的持續成長和影響力方面處於有利地位。

- 墨西哥的醫療保健產業主要是價格主導的,國內產品在政府銷售上具有價格優勢。公司必須遵守所有衛生註冊標準以確保品質。外國公司應考慮削減成本的措施,並在行銷和促銷材料中強調新技術的好處。 2023年,墨西哥藥品銷售額將達到約108.3億美元,高於2022年的101.2億美元。該地區藥品生產的擴大、非處方藥供應量的增加以及當地公司的大量投資正在促進巴西製藥業的顯著成長。這些趨勢加上出口的增加,預計將導致全國對藥品包裝的需求增加。

- 醫療保健成本的上升以及醫院和製藥製造商等最終用戶日益成長的偏好預計將在預測期內推動墨西哥的產品使用。與其他玻璃容器一樣,管瓶易於回收,並被認為是環保的。隨著最終用戶從傳統容器轉向管瓶,該國的醫療和保健產業對這些產品的需求旺盛。

拉丁美洲藥品包裝產業概況

由於現有公司專注於創新和收購,拉丁美洲藥品包裝市場變得支離破碎。 Amcor Group GmbH、Berry Global Inc. 和 Schott AG 等公司投入大量資源和資金來研發新產品、解決環境問題並確保政府合規。

- 2024 年 5 月 - 德國製藥和保健品包裝專家 Gerresheimer 計劃擴建其在墨西哥克雷塔羅的工廠。此擴建旨在提高RTF(即用型)注射器的產能,並滿足北美市場對優質注射器的需求。這些預充式玻璃注射器專為注射生物製藥而設計,包括用於肥胖管理的Glucagon-Like Peptide-1製劑。擴建工程將於 2023 年 11 月舉行奠基儀式,Gerresheimer 將在該計劃中投資約 1 億歐元(1.06 億美元)。

- 2023 年 11 月 - Amkor 推出單 PE 層壓板來製造可在聚乙烯流中回收的全薄膜醫療包裝。據報道,這項創新減少了包裝的碳排放,同時確保患者安全。該薄膜預計將為 3D 熱成型包裝提供可回收的蓋子,其中包括手術單、保護器、導管、注射和管道系統等。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場動態

- 市場促進因素

- 國內藥品產量增加

- 增加對該地區製藥和包裝行業的直接投資

- 市場限制因素

- 與藥品包裝原料相關的環境問題

- 原物料價格波動

第6章 市場細分

- 按包裝材料分

- 塑膠

- 玻璃

- 金屬

- 紙

- 依產品類型

- 泡殼包裝

- 塑膠瓶

- 預充式注射器

- 管瓶和安瓿

- 密閉容器

- 容器

- 其他產品類型

- 按國家/地區

- 巴西

- 墨西哥

- 哥倫比亞

- 阿根廷

第7章 競爭格局

- 公司簡介

- Amcor Group GmbH

- Sealed Air Corporation

- Berry Global Inc.

- Schott AG

- Gerresheimer AG

- Aptar Group Inc.

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Pretium Packaging

- Silgan Holdings Inc.

- Greiner Packaging International GmbH

第8章投資分析

第9章市場的未來

The Latin America Pharmaceutical Packaging Market size is estimated at USD 7.59 billion in 2025, and is expected to reach USD 10.34 billion by 2030, at a CAGR of 6.36% during the forecast period (2025-2030).

Key Highlights

- Pharmaceutical packaging is crucial in drug product presentation, protection, identification, and containment throughout their lifecycle. It facilitates storage, transport, and display while ensuring compliance with regulatory standards until the product is consumed. Adequate packaging shields the drug from various environmental factors, including climatic, biological, physical, and chemical conditions. To be optimal, pharmaceutical packaging must be cost-effective and provide adequate stability throughout the product's shelf life. The selection of packaging materials and types is based on the specific nature of the drug, ensuring that the chosen packaging offers appropriate protection and clear identification and maintains the integrity of the enclosed pharmaceutical product.

- The pharmaceutical packaging industry in Latin America is experiencing increased demand driven by the region's expanding economies and urbanising population. The growing elderly demographic requiring continuous medical care further fuels this trend. As the pharmaceutical manufacturing sector gains momentum, packaging vendors in the region can capitalise on the market's significant potential. Foreign investments, rising local production, and new product development contribute to the growth of the regional packaging industry. Consequently, Latin America is expected to remain a key market for pharmaceutical packaging shortly.

- The pharmaceutical industry in Latin America stands as one of the region's largest and most capital-intensive sectors. Research and development (R&D) plays a crucial role in developing innovative drugs, contributing to increased life expectancy in Latin America over the past two decades, albeit at a high cost. This focus on R&D has led to significant advancements in medical treatments and therapies, addressing various health challenges specific to the region.

- Traditionally, large multinational companies from Western Europe and the United States have dominated the pharmaceutical market in Latin America. These established firms have leveraged their extensive resources, global research networks, and advanced manufacturing capabilities to maintain a strong regional presence. However, in recent years, the landscape has begun to shift with the entry of new players into the industry.

- These new entrants include multinational companies from China, India, and South Korea, bringing different drug development and manufacturing approaches. Additionally, local firms from several developing countries within Latin America have emerged, often focusing on generic drugs or niche therapeutic areas. This diversification of market participants has led to increased competition, potentially driving innovation and improving access to medicines for Latin American populations.The evolving pharmaceutical landscape in Latin America presents opportunities and challenges for established and emerging companies. As the market continues to develop, factors such as regulatory environments, intellectual property rights, and healthcare policies will significantly shape the industry's future in the region.

- ALIFAR, the Latin American Association of Pharmaceutical Industries, is a non-profit international organisation operating independently from governmental and intergovernmental bodies. It represents nationally owned pharmaceutical companies across Latin America. ALIFAR's membership encompasses over 400 companies from 12 Latin American countries, accounting for over 90% of the region's pharmaceutical market. The organization plays a crucial role in advocating for the interests of its member companies and promoting the development of the pharmaceutical industry in Latin America. ALIFAR works to foster collaboration among its members, share best practices, and address common challenges faced by the industry in the region.

- The growing demand for pharmaceutical drugs and medicines in Latin America has been driven by population growth, increasing life expectancy, and a rising prevalence of chronic diseases. This demand and technological advancements in the pharmaceutical industry have directly led to an increased need for packaging solutions such as bottles, ampules, and other containers. The pharmaceutical packaging market in Latin America has consequently experienced significant growth. Manufacturers of packaging materials and solutions have had to adapt to meet the industry's evolving requirements, including considerations for drug stability, safety, and compliance with regulatory standards.

- Environmental concerns related to pharmaceutical packaging raw materials may limit the market but also provide opportunities for innovation in packaging within the pharmaceutical industry in the region. The increasing focus on sustainability has heightened scrutiny of traditional packaging materials, prompting manufacturers to explore eco-friendly alternatives. This shift presents cost and regulatory compliance challenges but also opens avenues for developing novel, environmentally responsible packaging solutions.

- Companies are investing in research and development to create biodegradable materials, reduce plastic usage, and improve the recyclability of pharmaceutical packaging. These efforts address environmental concerns and align with changing consumer preferences and regulatory requirements. As a result, the industry is witnessing a surge in innovative packaging designs that maintain product integrity while minimising environmental impact, potentially creating new market segments and competitive advantages for forward-thinking companies.

Latin America Pharmaceutical Packaging Market Trends

Plastic Bottles to Hold Significant Market Share

- Plastic is widely used in pharmaceutical packaging due to its versatility, durability, flexibility, and sustainability. Pharmaceutical packaging employs plastic bottles made from various materials, including polyvinyl chloride, polyethene, polypropylene, and polystyrene. The industry utilises transparent, durable, lightweight plastic for storage and distribution. These plastic materials offer several advantages, such as resistance to breakage, ease of moulding into various shapes and sizes, and compatibility with a wide range of pharmaceutical products.

- Additionally, plastic packaging helps protect medications from moisture, light, and contaminants, ensuring product integrity and extending shelf life. The use of plastic in pharmaceutical packaging also contributes to cost-effectiveness in manufacturing and transportation, as it is generally lighter and more economical than alternative materials like glass or metal.

- Plastic bottles are extensively utilised for packaging various liquid and solid medicines, including syrups, capsules, tablets, and ophthalmic preparations. The pharmaceutical industry favours plastic packaging due to its strength, lightweight nature, and flexibility, allowing for diverse forms and sizes. The market for pharmaceutical plastic bottles has expanded, driven by technological advancements and the increased adoption of plastic containers for oral solid and liquid medications.

- Plastics in pharmaceutical applications must be non-toxic, non-carcinogenic, biocompatible, and harmless to the biological environment. These stringent requirements ensure the safety and efficacy of pharmaceutical products. The drug development process includes rigorous testing of PET packaging for leaching and extractability in conjunction with the drug. This testing is crucial to prevent contamination or interaction between the packaging and the pharmaceutical contents. PET bottles provide an effective oil barrier, helping to resist chemical spills during transport. This barrier property is significant for maintaining the integrity of liquid medications and preventing contamination from external sources. Additionally, PET packaging offers durability and resistance to breakage, essential qualities for pharmaceutical containers that may be subject to various handling and transportation conditions.

- The demand for pharmaceutical plastic bottles has increased, impacting the market valuation of plastic bottles in Latin America. In 2023, the combined value of pharmaceutical exports from Latin America and the Caribbean reached approximately USD 9.3 billion, marking the region's highest level of pharmaceutical exports during the analyzed period. In 2022, Mexico led Latin American countries in pharmaceutical export value.Further, it is anticipated that the growth of solid containers may be aided due to the increased adoption of medicines containing nutrients. The increasing awareness of nutritional enrichment among working professionals for maintaining balanced nutrition in the human body is anticipated to promote the consumption of dietary supplements and drive demand for plastic bottles in the region.

- Individuals with eye conditions commonly use dropper bottles. These specialised containers allow for the precise administration of eye medications and solutions. Companies like Gerresheimer provide pharmaceutical plastic packaging for various applications, including solid, liquid, and ophthalmic products. Their product range includes PET bottles for liquid dosage forms and ophthalmic solutions. These bottles are engineered to meet specific requirements for preserving and dispensing eye medications, ensuring proper dosage and maintaining product integrity. The use of dropper bottles in ophthalmic applications has become increasingly important as the prevalence of eye-related disorders continues to rise in the region.

Mwxico is Expected to Witness Significant Growth

- Mexico is a significant contributor to the pharmaceutical market share in Latin America. As a mature market in the region's pharmaceutical industry, Mexico has experienced numerous product innovations, particularly in pharmaceutical packaging. This innovation is driven by the presence of significant vendors throughout the country. The Mexican pharmaceutical market has grown steadily, supported by a robust healthcare system and increasing demand for generic and branded medications.

- The country's strategic location and trade agreements, such as NAFTA (now USMCA), have further enhanced its position as a critical player in the regional pharmaceutical landscape. In recent years, Mexico has seen a rise in pharmaceutical research and development activities, with domestic and international companies investing in local facilities. This has increased the production of high-quality, cost-effective medications, further solidifying Mexico's position in the Latin American pharmaceutical market.

- The packaging sector within Mexico's pharmaceutical industry has been particularly dynamic. Innovations in this area have focused on improving drug safety, extending shelf life, and enhancing patient compliance. These advancements include intelligent packaging solutions, eco-friendly materials, and designs catering to different patient groups' needs. Despite challenges such as regulatory complexities and competition from other emerging markets, Mexico's pharmaceutical industry continues to evolve and adapt. The country's commitment to innovation and established manufacturing capabilities position it well for continued growth and influence in the Latin American pharmaceutical market.

- The Mexican healthcare industry is primarily price-driven, with domestically produced goods having a pricing advantage in government sales. Businesses must comply with all sanitary registration standards to ensure quality. Foreign companies should consider cost-cutting measures and highlight the benefits of new technology in their marketing and promotional materials. In 2023, Mexico's pharmaceutical product sales reached approximately USD 10.83 billion, an increase from USD 10.12 billion in 2022. The region's expanding pharmaceutical production, increased availability of over-the-counter medicines, and significant investments by local businesses contribute to the substantial growth of the Brazilian pharmaceutical sector. These trends are expected to lead to an increase in pharmaceutical packaging demand nationwide, along with growing exports.

- The increasing cost of healthcare and the growing preference among end-users such as hospitals and pharmaceutical manufacturers are expected to drive product usage in Mexico during the forecast period. Vials, like other glass containers, are easily recyclable and considered environmentally friendly. The medical and healthcare sectors in the country are experiencing a lucrative demand for these products due to end-users' shift from conventional containers to vials.

Latin America Pharmaceutical Packaging Industry Overview

The pharmaceutical packaging market in Latin America is fragmented, as established companies focus on innovation and acquisition. Companies like Amcor Group GmbH, Berry Global Inc., Schott AG. invest a lot of their resources and money in Research and development to innovate new products, meet with the environment, and ensure government compliance.

- May 2024 - Gerresheimer, a Germany-based company specialising in pharmaceutical and healthcare packaging, is set to expand its facility in Queretaro, Mexico. This expansion aims to boost production capacities for ready-to-fill (RTF) syringes, addressing the North American market's demand for premium syringes. These prefillable glass syringes are designed for injectable biopharmaceuticals, including glucagon-like peptide-1 drugs for obesity management. The expansion started with a ground-breaking ceremony in November 2023, and Gerresheimer is channelling an investment of around EUR 100 million (USD 106 million) into the project.

- November 2023 - Amcor has introduced a mono-PE laminate to create all-film medical packaging recyclable in the polyethylene stream. This innovation reportedly reduces the package's carbon footprint while ensuring patient safety. The film is expected to enable recycle-ready lidding for 3D thermoformed packages, which house items like drapes, protective materials, catheters, and injection and tubing systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Domestic Pharmaceuticals Production

- 5.1.2 Growing FDI In regional pharmaceutical and packaging sector

- 5.2 Market Restraints

- 5.2.1 Environmental Concerns related to Pharmaceutical Packaging Raw Materials

- 5.2.2 Fluctuations In Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Packaging Material

- 6.1.1 Plastic

- 6.1.2 Glass

- 6.1.3 Metal

- 6.1.4 Paper

- 6.2 By Product Type

- 6.2.1 Blister Packs

- 6.2.2 Plastic Bottles

- 6.2.3 Prefillable Syringes

- 6.2.4 Vials and Ampuls

- 6.2.5 Closures

- 6.2.6 Containers

- 6.2.7 Other Product Types

- 6.3 By Country

- 6.3.1 Brazil

- 6.3.2 Mexico

- 6.3.3 Columbia

- 6.3.4 Argentina

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Sealed Air Corporation

- 7.1.3 Berry Global Inc.

- 7.1.4 Schott AG

- 7.1.5 Gerresheimer AG

- 7.1.6 Aptar Group Inc.

- 7.1.7 ALPLA Werke Alwin Lehner GmbH & Co KG

- 7.1.8 Pretium Packaging

- 7.1.9 Silgan Holdings Inc.

- 7.1.10 Greiner Packaging International GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球藥品單劑量包裝市場報告

2026年全球藥品單劑量包裝市場報告 醫藥包裝市場分析及預測(至2035年):依類型、產品類型、材質、技術、應用、組件、最終用戶、功能、製程及解決方案分類

醫藥包裝市場分析及預測(至2035年):依類型、產品類型、材質、技術、應用、組件、最終用戶、功能、製程及解決方案分類 亞太地區醫藥包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區醫藥包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本生物製藥包裝市場規模、佔有率、趨勢及預測(依材料、包裝類型、應用及地區分類),2026-2034年2026年全球微型離心管盒市場報告2026年全球益生菌包裝市場報告2026年全球藥品包裝檢測設備市場報告2026年全球藥局包裝機械市場報告

日本生物製藥包裝市場規模、佔有率、趨勢及預測(依材料、包裝類型、應用及地區分類),2026-2034年2026年全球微型離心管盒市場報告2026年全球益生菌包裝市場報告2026年全球藥品包裝檢測設備市場報告2026年全球藥局包裝機械市場報告 2025-2029年全球溫控藥品包裝解決方案市場

2025-2029年全球溫控藥品包裝解決方案市場 按應用、技術和地區分類的防偽藥品包裝市場

按應用、技術和地區分類的防偽藥品包裝市場