|

市場調查報告書

商品編碼

1627138

北美玻璃瓶/容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)North America Glass Bottles/Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

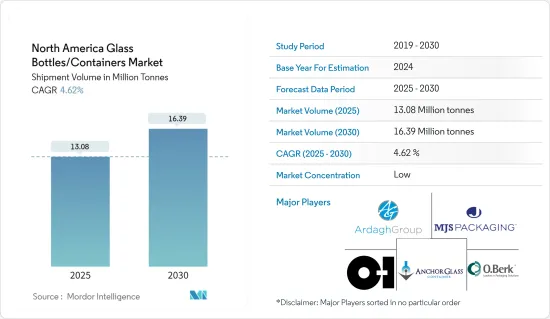

北美玻璃瓶/容器市場規模(以出貨量為準)預計將從2025年的1308萬噸擴大到2030年的1639萬噸,預測期間(2025-2030年)複合年成長率為4.62%。

主要亮點

- 在食品和飲料、化妝品和藥品等領域消費增加的推動下,北美玻璃瓶/容器市場正在成長。隨著消費者越來越重視安全和健康的包裝,玻璃正在進入不同的類別。這種趨勢在飲料領域尤其明顯,奢侈品和工藝飲料通常採用玻璃瓶包裝。

- 此外,壓花、成型和藝術精加工方面的最尖端科技增強了玻璃包裝的吸引力。這些創新不僅可以實現更大的客製化和品牌化,而且還使玻璃容器成為希望使其包裝脫穎而出的公司的可行選擇。該行業對輕質玻璃技術的關注,解決了運輸成本問題和環境影響,進一步推動了市場擴張。

- 在美國,酒精飲料的消費量激增,對包裝的需求不斷增加,尤其是玻璃瓶。這種需求反映了酒精飲料種類的擴大和消費者對優質包裝的偏好。玻璃瓶之所以受到青睞,不僅是因為其可回收性和奢華感,還因為它們能夠保持飲料的品質和風味。精釀啤酒的趨勢和手工烈酒的出現激發了人們對優質玻璃包裝的渴望。

- 2023 年全國藥物濫用與健康調查 (NSDUH) 的資料顯示,2.187 億美國成年人(其中 84.9% 為 18 歲及以上)飲酒。如此龐大的消費群確保了飲料領域對多樣化包裝解決方案的穩定需求。由於其多功能性和吸引力,玻璃瓶仍然是主流,製造商正在不斷創新,以跟上生產商和消費者不斷變化的偏好。

- Glass Global報告稱,北美各行業玻璃瓶/容器產量為8,389,233噸,年產能為9,321,370噸。這凸顯了該地區在玻璃包裝領域的強大影響力。強勁的生產能力和產量顯示了強大的基礎設施以及食品和飲料、藥品和化妝品等行業的強勁需求。

- 此外,根據國際貿易中心的資料,美國出口了約 141,143 噸玻璃包裝。這不僅代表了玻璃包裝領域的新興機遇,也凸顯了國際對北美玻璃產品的需求。大量國內生產和大量出口的結合凸顯了北美玻璃包裝產業的實力和成長軌跡。

- 隨著玻璃瓶/容器被各個領域所採用,回收已成為該地區的重點關注點。食品飲料、藥品和化妝品等行業擴大使用玻璃瓶/容器,產生大量玻璃廢棄物。高效回收對於廢棄物管理、最大限度地減少環境影響和促進永續性至關重要。隨著政府法規傾向於永續包裝,製造商擴大轉向玻璃解決方案。這些動態正在推動北美玻璃包裝市場的成長。

北美玻璃瓶/容器市場趨勢

酒精飲料領域預計將顯著成長

- 酒精飲料製造商正在推出玻璃瓶裝的新產品,此舉預計將對市場產生正面影響。透過採用玻璃包裝,這些製造商旨在提高其產品的吸引力,重塑消費者的觀念,並利用與玻璃相關的奢華形象。玻璃瓶不僅能更有效地保存產品的味道和質量,還能提高可回收性和奢華感。許多消費者將玻璃包裝等同於卓越的飲料品質,通常證明高價是合理的。

- 此外,玻璃可以實現獨特且富有創意的瓶子設計,使品牌能夠在商店脫穎而出。

- 向玻璃包裝的轉變與消費者對永續和環保選擇不斷成長的需求產生了共鳴。

- 例如,2024年9月,帝亞吉歐公司旗下尊尼獲加推出限量版“Blue Label Ultra”,展示了專為蘇格蘭威士忌量身定做的全球最輕的700ml玻璃瓶。這種開創性的包裝標誌著永續威士忌裝瓶的重大飛躍。

- 北美的啤酒包裝行業深受不斷發展的文化趨勢、人口成長、都市化以及年輕人中啤酒受歡迎程度激增的影響。區域啤酒分銷網路的持續投資和擴張可能會維持這些趨勢並重振玻璃瓶/容器市場。

- 2024年3月至2024年5月,美國瓶裝和罐裝啤酒產量在1,041萬桶至1,247萬桶之間波動,支撐了美國對包裝啤酒的需求。市場受到啤酒消費量, 2023 年美國啤酒產量和進口量將減少 5%,精釀啤酒生產商產量將減少 1%。

- 產量和進口量的下降可能是由於消費者偏好、經濟因素或監管變化的變化。然而,啤酒消費量的增加表明該行業尚未開發的成長和創新潛力,這可能是受到新啤酒品種、行銷力度的加大和消費行為變化的刺激。

- 在北美,越來越多的消費者正在採用永續的生活方式,而遏制塑膠廢棄物的努力尤其受歡迎。此舉支持葡萄酒和烈酒市場向玻璃瓶的轉變。許多消費者認為玻璃瓶比塑膠瓶更環保且是優質產品。這種認可引起了具有環保意識的消費者的共鳴,他們往往願意為永續包裝支付溢價。此外,即將訂定的旨在限制塑膠使用的政府法規可能會進一步增加酒精飲料領域對玻璃瓶的需求。

美國預計將佔據主要市場佔有率

- 美國是世界上最大的包裝市場之一,有許多主要企業為食品和飲料、個人護理和藥品等多種行業生產玻璃瓶和容器。該國的經濟成長以及消費者在食品、飲料、藥品和個人保健產品方面支出的增加正在推動對玻璃瓶和包裝解決方案的需求。

- 人們對永續和可回收包裝選擇的日益偏好進一步推動了這一趨勢,玻璃因其環保特性而受到青睞。以啤酒和烈酒為主的精釀飲料行業的成長也促進了特種玻璃包裝需求的增加。由於社會老化和醫療保健的進步,製藥業的擴張也增加了對滿足嚴格安全和儲存標準的高品質玻璃容器的需求。

- 美國擁有強大的經濟、完善的商業移民體系、多元化的消費基礎、創新主導的文化和親商政策,為商業投資提供了良好的環境。這些因素使美國成為對尋求擴張或建立新業務的企業家和公司有吸引力的目的地。強大的基礎設施、先進的技術領域和獲得資本的機會使其對各行業的公司更具吸引力。

- 電子商務平台的發展和消費行為的演變為線上零售商創造了巨大的機會。由於網路普及率、行動裝置使用和購物習慣改變等因素,數位市場正在迅速擴張。這些趨勢為包括玻璃包裝在內的各種行業帶來了潛在機會。

- 隨著消費者的環保意識越來越強並尋求永續的解決方案,玻璃包裝製造商可以利用對可回收和可重複使用容器的需求。此外,利基市場對奢侈品和手工產品日益成長的偏好往往與玻璃包裝的品質和美學吸引力相匹配,為玻璃包裝行業提供了進一步的成長潛力。

- 在美國,千禧世代和X世代正在推動葡萄酒消費的成長。這些消費者群體對葡萄酒的偏好正在提高,這正在影響市場趨勢和產品供應。他們不斷變化的偏好和購買習慣正在對葡萄酒行業的方向產生重大影響。 2023年美國葡萄酒零售總額將達約1,063億美元。這一重要數字反映了美國葡萄酒市場的強勁本質和持續擴張。銷售成長顯示消費增加以及可能轉向優質或更高價格的葡萄酒產品。

- 這一趨勢顯示葡萄酒包裝對高品質玻璃瓶的需求不斷增加。隨著消費者的眼光越來越挑剔,他們更加重視葡萄酒產品的整體呈現和品質。玻璃瓶,尤其是那些品質好的玻璃瓶,在保存葡萄酒的完整性和增加其價值方面發揮著重要作用。包裝產業,尤其是玻璃製造商,將受益於此趨勢,因為釀酒廠力求滿足消費者對優質包裝解決方案的期望。

北美玻璃瓶/容器產業概況

北美玻璃瓶/容器市場細分,許多全球和地區公司爭奪市場佔有率。該領域的主要企業包括 OI Glass, Inc.、Ardagh Group SA、MJS Packaging 和 Anchor Glass Container Corporation。這些和其他市場參與企業促成了多元化和競爭的格局。

隨著市場的發展,技術創新對於維持和擴大永續競爭優勢至關重要。公司投資研發以改進產品、增強製造流程並回應不斷變化的消費者需求。這種對創新的關注正在推動輕質玻璃製造的進步、改進的回收技術以及開發用於增強產品保護的專用塗層。

對永續性和環境的日益關注也是玻璃瓶/容器市場的關鍵促進因素。許多公司正在採用環保方法,並將玻璃的可回收性作為主要賣點。這一趨勢將持續塑造競爭格局並影響市場動態。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 容器玻璃進出口資料

- 容器玻璃市場PESTEL分析

- 包裝玻璃行業標準及法規

- 容器和包裝用玻璃的原料分析和材料考慮

- 容器和包裝玻璃的永續性趨勢

- 北美的容器玻璃熔爐和位置

第5章市場動態

- 市場促進因素

- 食品和飲料產業不斷擴大的需求

- 永續性和可回收性措施推動了最終用戶對玻璃包裝的需求

- 市場限制因素

- 玻璃製造造成的高碳足跡

- 營運和物流問題

- 貿易情景-玻璃瓶/容器產業進出口範式的歷史與現況分析

第6章 市場細分

- 按最終用戶產業

- 飲料

- 酒精飲料(按細分市場定性分析)

- 啤酒/蘋果酒

- 葡萄酒/烈酒

- 其他酒精飲料

- 非酒精類(按細分市場定性分析)

- 碳酸飲料

- 牛奶

- 水/其他非酒精飲料

- 食物

- 化妝品

- 藥品

- 其他行業

- 飲料

- 按國家/地區

- 美國

- 加拿大

第7章 競爭格局

- 公司簡介

- OI Glass, Inc

- Ardagh Group SA

- Gerresheimer AG

- Arksansas Glass Container Corporation

- MJS Packaging

- O.Berk Company, LLC

- Kaufman Container Company

- Burch Bottle & Packaging, Inc.

- Anchor Glass Container Corporation

- West Coast Container Inc.

- PGP Glass Private Limited

第8章 供應北美玻璃瓶/容器廠的主要窯爐製造商分析

第9章 市場未來展望

The North America Glass Bottles/Containers Market size in terms of shipment volume is expected to grow from 13.08 million tonnes in 2025 to 16.39 million tonnes by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

Key Highlights

- Driven by rising consumption in sectors like food and beverage, cosmetics, and pharmaceuticals, the North American container glass market is on an upward trajectory. As consumers increasingly prioritize safe and healthy packaging, glass has found its way into diverse categories. This is especially pronounced in the beverage sector, where premium products and craft beverages often come in glass bottles.

- Moreover, cutting-edge technologies in embossing, shaping, and artistic finishes are elevating the allure of glass packaging. Such innovations not only offer enhanced customization and branding but also make glass containers a go-to choice for companies aiming for standout packaging. The industry's push towards lightweight glass technologies addresses transportation cost concerns and environmental implications, further fueling market expansion.

- In the U.S., a surge in alcoholic beverage consumption is driving a robust demand for packaging, especially glass bottles. This demand mirrors the expanding range of alcoholic offerings and a consumer tilt towards premium packaging. Glass bottles are preferred not just for their recyclability and premium look, but also for their prowess in preserving beverage quality and taste. The craft beer trend and the emergence of artisanal spirits have amplified the appetite for top-tier glass packaging.

- Data from the 2023 National Survey on Drug Use and Health (NSDUH) reveals that 218.7 million U.S. adults (84.9% of those 18 and older) have consumed alcohol at some point. Such a significant consumer base ensures a steady demand for varied packaging solutions in the beverage sector. Glass bottles, with their versatility and appeal, remain dominant, and manufacturers are innovating to cater to the changing preferences of both producers and consumers.

- Glass Global reports that North America produced 8,389,233 tonnes of glass bottles and containers across sectors, with an annual capacity of 9,321,370 tonnes. This underscores the region's formidable presence in the glass packaging arena. The robust production capacity and volume signal not just a strong infrastructure but also a thriving demand, spanning industries like food and beverage, pharmaceuticals, and cosmetics.

- Additionally, data from the International Trade Centre highlights the U.S. exported around 141,143 tonnes of glass packaging. This not only points to a burgeoning opportunity in the glass packaging realm but also underscores the international demand for North American glass products, likely attributed to their quality and the region's manufacturing prowess. The blend of substantial domestic production and significant export figures accentuates the North American glass packaging industry's strength and growth trajectory.

- As container glass finds increasing adoption across sectors in the region, recycling has emerged as a critical focus. Industries like food and beverage, pharmaceuticals, and cosmetics are generating substantial glass waste due to their heightened use of container glass. Efficient recycling is vital for waste management, minimizing environmental impact, and championing sustainability. With government regulations leaning towards sustainable packaging, manufacturers are increasingly turning to glass solutions. Collectively, these dynamics are propelling the growth of North America's glass packaging market.

North America Glass Bottles/Containers Market Trends

Alcoholic Beverage Segment is Expected to Witness Significant Growth

- Alcohol manufacturers are rolling out new versions of their products in glass bottles, a move anticipated to positively influence the market. By adopting glass packaging, these manufacturers aim to boost product appeal and reshape consumer perceptions, capitalizing on the premium image associated with glass. Glass bottles not only preserve the product's taste and quality more effectively but also offer heightened recyclability and an upscale feel. Many consumers equate glass packaging with superior beverage quality, often justifying a premium price tag.

- Moreover, glass facilitates unique and creative bottle designs, allowing brands to differentiate themselves on store shelves.

- This pivot to glass packaging resonates with the rising consumer demand for sustainable and eco-friendly options, given that glass is entirely recyclable and boasts multiple reuse capabilities.

- For example, in September 2024, Diageo-owned Johnnie Walker unveiled a limited edition Blue Label Ultra, showcasing the world's lightest 700ml glass bottle tailored for Scotch whisky. This pioneering packaging marks a notable leap in sustainable whisky bottling.

- The North American beer packaging sector is largely influenced by evolving cultural trends, a growing population, urbanization, and a surge in beer's popularity among younger demographics. Continued investments and a broadening beer distribution network across regions are likely to uphold these trends, potentially invigorating the market for glass bottles and containers.

- From March to May 2024, U.S. beer production in bottles and cans fluctuated between 10.41 million and 12.47 million barrels, underscoring the nation's demand for packaged beer. Even though the U.S. witnessed a 5% dip in beer production and imports in 2023, and craft brewer volume sales fell by 1%, the market remains buoyed by a rising beer consumption trend.

- The dip in production and imports could stem from shifts in consumer preferences, economic factors, or regulatory changes. Yet, the uptick in beer consumption hints at untapped growth and innovation avenues in the industry, possibly spurred by new beer varieties, intensified marketing, or evolving consumer behaviors.

- In North America, a growing segment of consumers is embracing sustainable lifestyles, notably in their efforts to curb plastic waste. This movement is propelling the wine and spirits market's shift towards glass bottles. Many consumers view glass bottles as more eco-friendly than their plastic counterparts and associate them with premium product quality. This perception resonates with environmentally-conscious consumers, often willing to pay a premium for sustainable packaging. Furthermore, looming government regulations aimed at curbing plastic usage could further amplify the demand for glass bottles in the alcoholic beverage sector.

United States is Expected to Account for Major Market Share

- The United States represents one of the world's largest packaging markets, featuring numerous key players producing glass bottles and containers for various industries, including food and beverage, personal care, and pharmaceuticals. The country's economic growth and rising consumer expenditure on food, drinks, pharmaceuticals, and personal care products drive the demand for glass bottle and container packaging solutions.

- This trend is further supported by the increasing preference for sustainable and recyclable packaging options, with glass being favored due to its eco-friendly properties. The growing craft beverage industry, particularly in beer and spirits, has also contributed to the increased demand for specialized glass packaging. The pharmaceutical sector's expansion, driven by an aging population and advancements in healthcare, has also bolstered the need for high-quality glass containers that meet stringent safety and preservation standards.

- The United States offers a favorable environment for business ventures due to its strong economy, comprehensive business immigration system, diverse consumer base, innovation-driven culture, and business-friendly policies. These factors make the USA an attractive destination for entrepreneurs and companies looking to expand or establish new operations. The country's robust infrastructure, advanced technology sector, and access to capital further enhance its appeal for businesses across various industries.

- The growth of e-commerce platforms and evolving consumer behaviors present significant opportunities for online retailers. The digital marketplace has experienced rapid expansion, driven by increased internet penetration, mobile device usage, and changing shopping habits. This shift has created a fertile ground for businesses to reach a wider audience and implement innovative sales strategies.These trends create potential opportunities for various industries, including glass packaging.

- As consumers become more environmentally conscious and seek sustainable solutions, glass packaging manufacturers can capitalize on the demand for recyclable and reusable containers. Additionally, the growing preference for premium and artisanal products in niche markets often aligns well with the perceived quality and aesthetic appeal of glass packaging, presenting further growth prospects for the industry.

- In the United States, Millennial and Gen X consumers have been driving the growth in wine consumption. These demographic groups have shown an increasing preference for wine, influencing market trends and product offerings. Their evolving tastes and purchasing habits have significantly impacted the wine industry's direction. The total retail value of wine sales in the US reached approximately USD 106.3 billion in 2023. This substantial figure reflects the robust nature of the American wine market and its continued expansion. The sales value growth indicates increased consumption and a potential shift towards premium or higher-priced wine products.

- This trend indicates an increasing demand for high-quality glass bottles in wine packaging. As consumers become more discerning, there is a growing emphasis on the overall presentation and quality of wine products. Glass bottles, particularly those of superior quality, play a crucial role in preserving the wine's integrity and enhancing its perceived value. The packaging industry, especially glass manufacturers, will likely benefit from this trend as wineries seek to meet consumer expectations for premium packaging solutions.

North America Glass Bottles/Containers Industry Overview

The North America container glass market is fragmented, with numerous global and regional players competing for market share. Key companies in this space include O-I Glass, Inc., Ardagh Group S.A., MJS Packaging, and Anchor Glass Container Corporation. These firms and other market participants contribute to a diverse and competitive landscape.

As the market evolves, innovation has become crucial in maintaining and growing sustainable competitive advantage. Companies invest in research and development to improve product offerings, enhance manufacturing processes, and meet changing consumer demands. This focus on innovation drives advancements in lightweight glass production, improved recycling techniques, and the development of specialized coatings for enhanced product protection.

The increasing emphasis on sustainability and environmental concerns has also become a significant driver in the glass bottles and containers market. Many companies are adopting eco-friendly practices and promoting the recyclability of glass as a key selling point. This trend will likely continue shaping the competitive landscape and influencing market dynamics in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL Analysis of Container Glass Market

- 4.4 Industry Standard and Regulation For Container Glass Use For Packaging

- 4.5 Raw Material Analysis and Material Consideration For Packaging

- 4.6 Sustainability Trends For Glass Packaging

- 4.7 Container Glass Furnace and Location in North American Region

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from Food and Beverage Industry

- 5.1.2 Sustainability and Recyclability Initiatives Are Expanding End-Users Demand For Glass Packaging

- 5.2 Market Restraints

- 5.2.1 High Carbon Footprint due to Glass Manufacturing

- 5.2.2 Operation and Logistical Concerns

- 5.3 Trade Scenario - Analysis of the Historical and Current Export-Import Paradigm For Container Glass Industry

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical

- 6.1.5 Other End-user Verticals

- 6.1.1 Bevarages

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 O-I Glass, Inc

- 7.1.2 Ardagh Group S.A.

- 7.1.3 Gerresheimer AG

- 7.1.4 Arksansas Glass Container Corporation

- 7.1.5 MJS Packaging

- 7.1.6 O.Berk Company, L.L.C.

- 7.1.7 Kaufman Container Company

- 7.1.8 Burch Bottle & Packaging, Inc.

- 7.1.9 Anchor Glass Container Corporation

- 7.1.10 West Coast Container Inc.

- 7.1.11 PGP Glass Private Limited

8 ANALYSIS OF MAJOR FURNACE SUPPLIERS TO THE CONTAINER GLASS PLANTS ACROSS NORTH AMERICA

9 FUTURE OUTLOOK OF THE MARKET

德國容器玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南容器玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

德國容器玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南容器玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本玻璃容器市場規模、佔有率、趨勢和預測:按產品、最終用途行業和地區分類,2026-2034年

日本玻璃容器市場規模、佔有率、趨勢和預測:按產品、最終用途行業和地區分類,2026-2034年 2026年全球容器玻璃市場報告2026年全球運動水壺市場報告

2026年全球容器玻璃市場報告2026年全球運動水壺市場報告 容器玻璃市場 - 全球產業規模、佔有率、趨勢、機會及預測(按玻璃類型、容器類型、成型方法、終端用戶產業、地區和競爭格局分類,2021-2031年)廣口瓶市場-全球產業規模、佔有率、趨勢、機會和預測(按材料、產能、應用、分銷管道、地區和競爭格局分類),2021-2031年酒瓶市場-全球產業規模、佔有率、趨勢、機會、預測:按玻璃類型、應用、容量、地區和競爭格局分類,2021-2031年

容器玻璃市場 - 全球產業規模、佔有率、趨勢、機會及預測(按玻璃類型、容器類型、成型方法、終端用戶產業、地區和競爭格局分類,2021-2031年)廣口瓶市場-全球產業規模、佔有率、趨勢、機會和預測(按材料、產能、應用、分銷管道、地區和競爭格局分類),2021-2031年酒瓶市場-全球產業規模、佔有率、趨勢、機會、預測:按玻璃類型、應用、容量、地區和競爭格局分類,2021-2031年 全球臥螺離心機市場(2026-2030 年)印度容器玻璃市場-佔有率分析、產業趨勢與統計、成長預測(2026-2031)

全球臥螺離心機市場(2026-2030 年)印度容器玻璃市場-佔有率分析、產業趨勢與統計、成長預測(2026-2031)