|

市場調查報告書

商品編碼

1629764

AaaS(分析即服務)-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Analytics as a Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

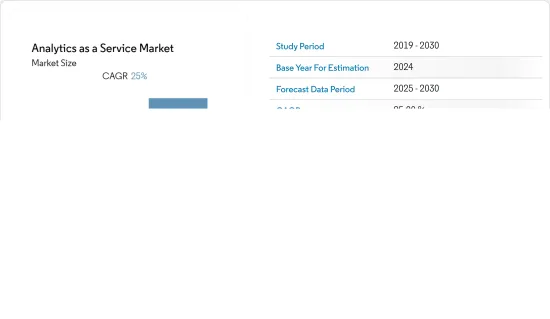

AaaS(分析即服務)市場預計在預測期內複合年成長率為 25%

主要亮點

- 工業 4.0 時代及其在世界上幾乎每個行業的採用正在推動組織轉向雲端。自動化每天都會產生大量資料。對收集的資料進行模式分析並用於預測未來事件。隨著物聯網設備的商業化,這種機會正在增加。

- 分析可以最佳化物流等複雜營運,並降低幾乎每個行業的生產成本。內部資產的績效有助於提高組織的獲利能力。除了歷史資料分析之外,還可以進行預測分析,使製造商能夠安排預測性維護。這使得製造商能夠防止代價高昂的資產故障並避免計劃外停機。

- 這些是推動 AaaS(分析即服務)市場成長的關鍵因素。然而,隨著資料外洩事件的增加,出於隱私方面的考慮,企業不再採用雲端服務。這些服務收益的不確定性也限制了分析即服務 (AaaS) 市場。

- 資料安全問題和複雜分析程序的可用性預計將阻礙 AaaS(分析即服務)市場的成長。同時,企業更了解消費者活動和行為並控制他們創建的資料的需求正在成長,這為分析即服務 (AaaS) 市場創造了巨大的機會。

- 在 COVID-19 大流行期間,公司允許員工在家工作,增加了 Microsoft Teams 和 Zoom 等視訊會議平台的使用,並推動了分析即服務 (AaaS) 行業的成長。此外,對雲端運算技術不斷成長的需求正在推動市場擴張。雲端運算提供存取權限,允許員工在任何地方工作。員工可以使用特定的憑證來存取他們所需的資料和文檔,使在家工作,同時保持安全。這種情況正在推動 AaaS 產業向前發展。

AaaS(分析即服務)市場趨勢

電信和 IT 領域成長顯著

- 電信分析是商業智慧的一種,可以滿足電信業複雜的最佳化需求。電信分析旨在透過增加銷售、減少詐欺和改進風險管理來降低營運成本並最大化利潤。

- 市場成長背後的驅動力之一是人們對物聯網 (IoT) 意識的不斷增強。預計未來幾年對儲存大量待評估資料的需求將會增加。隨著創新性 COVID-19 的傳播以及公眾對資料的使用越來越多,開放原始碼資料和視覺化已經被開發出來以推動市場成長。

- 分析應用於通訊,以提高可見度並深入了解組織的核心業務和內部流程。它還可以幫助您了解市場狀況、預測趨勢並根據您獲得的見解做出預測。巨量資料現在在這方面發揮著重要作用。

- Zoom Video Communications 於 2021 年 3 月進行的一項調查重點關注了冠狀病毒 (COVID-19) 爆發後的現場和虛擬活動出席。活動的例子包括音樂表演、會議和宗教儀式。疫情爆發後,52%的美國受訪者表示他們將親自或透過視訊會議參與活動。在日本,65% 的受訪者表示同意。同時,10%的印度受訪者表示,疫情爆發後只會透過視訊會議參加活動。

- 物聯網設備的日益普及正在推動 AaaS(分析即服務)市場的發展。根據 Appinventiv 進行的一項研究,預計到 2023 年,連網車輛將成為全球 5G 物聯網 (IoT) 端點市場中最大的類別,預計將有 1,900 萬個端點。全球已安裝的 5G IoT 端點數量預計將從 2020 年的 350 萬個增加到 2023 年的約 4,900 萬個。

北美地區佔比最大

- 北美佔據最大的市場佔有率,主要是因為存在眾多市場參與企業以及對分析平台不斷成長的需求。美國是全球最大的雲端解決方案市場之一。

- 大多數主要設備製造商在全球範圍內營運和部署設備,因此在每個地區持有資料中心以滿足其運算需求。因此,製造商需要分析解決方案來追蹤他們的設備。

- 此外,Twitter、Instagram、Facebook 和 YouTube 等社群媒體應用程式會產生大量資料。企業出於專業目的分析社群媒體資料的需求不斷成長,這是推動分析即服務 (AaaS) 市場擴張的因素之一。例如,IBM公司提供基於Twitter資料的特定行業市場分析,北美地區的公司正在增加研發投資,以提供先進的分析解決方案。

- 北美地區的公司正在建立策略夥伴關係並開發分析服務。例如,2022 年 2 月, 資料和 Microsoft 建立了連接 Teradata Vantage資料平台和 Microsoft Azure 的全球夥伴關係關係。此次合作將使希望提升資料分析工作負載安全性、可靠性和靈活性的公司能夠大規模利用兩家公司的技術。

- 加拿大的電子商務產業也伸出了援助之手,推動了對巨量資料解決方案的需求。據Worldpay稱,2018年加拿大電子商務銷售額超過500億美元,預計到2022年將達到800億美元。

AaaS(分析即服務)產業概述

分析服務是分散的,有可能改變競爭對手並為差異化和附加價值服務開闢許多新途徑。此外,分析技術能力的大幅擴展迫使公司跟上競爭對手的步伐,並超額提供改進的產品效能。這種環境增加了成本並降低了行業盈利。領先的分析解決方案供應商與各種公司和技術合作,以支援他們的整體產品供應。

- 2022 年 5 月 - Wipro 和 Informatica 合作,透過 Wipro Fullstride 雲端服務資料平台將雲端基礎的資料和分析推向市場。 Informatica 和 Wipro 創造了一個一站式市場,透過將雲端超大規模產品與 Wipro 的平台、IP、人才和合作夥伴主導的解決方案相結合,創造業務價值和客戶成果。 Wipro 眾所周知的資料、分析和人工智慧 (AI) 技能,與 Informatica 完整的人工智慧驅動的資料管理解決方案相結合,可實現雲端基礎的大規模轉型。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 提高雲端採用率並增加產生的資料量

- 提高組織內部效率的需求不斷增加

- 市場限制因素

- 資料安全問題

第6章 市場細分

- 按公司規模

- 小型企業

- 主要企業

- 按最終用戶產業

- 資訊科技/通訊

- 能源/電力

- BFSI

- 醫療保健

- 零售

- 製造業

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Hewlett-Packard Enterprise Company

- SAS Institute

- Accenture PLC

- Google Inc.

- Amazon Web Services Inc.

- Opera Solutions LLC

- Atos SE

- Host Analytics Inc.

第8章投資分析

第9章市場的未來

The Analytics as a Service Market is expected to register a CAGR of 25% during the forecast period.

Key Highlights

- The era of industry 4.0 and its adoption by almost all the sectors globally are driving the organization to move to the cloud. The automation is creating a massive amount of data on day to day basis. The collected data is then analyzed for the pattern and is used for predicting future incidences. This opportunity is increasing with the commercialization of IoT-enabled Devices.

- The analytics optimizes complex operations like logistics for almost all industries to reduce production costs. The performance of the internal assets helps increase the organization's profit margin. In addition to enabling historical data analysis, predictive analytics, which manufacturers can use to schedule predictive maintenance. This allows manufacturers to prevent costly asset breakdowns and avoid unexpected downtime.

- These are the major factors driving the growth of analytics as a service market. However, the increasing data breach incidences restrict organizations from adopting cloud services due to privacy concerns. Also, the uncertainty of the return on investment for these services limits the analytics as a service market.

- Data security issues and the availability of complicated analytical procedures are expected to hamper the growth of the Analytics as a Service Market. With this, the expanding company requirement to better understand consumer activities and behavior and manage created data will present significant opportunities for the Analytics as a Service Market.

- Companies have allowed their employees to work from home during the Covid-19 pandemic, which has increased the usage of video conferencing platforms like Microsoft Teams and Zoom, significantly increasing the growth of the analytics-as-a-service industry. Furthermore, the growing need for cloud computing technologies drives the market's expansion. By giving access, cloud computing enables employees to operate from any place. Employees may access the necessary data and documents by utilizing specific credentials, ensuring security while allowing them to work from home. This circumstance is propelling the AaaS industry forward.

Analytics as a Service Market Trends

Telecom and IT Segment to Grow Significantly

- The telecom analytics type of business intelligence satisfies the optimization of the complex needs of the telecom industry. Telecom analytics aims to decrease operational costs and maximize profits by increasing sales, reducing fraud, and improving risk management.

- One of the reasons driving the market growth is increased awareness of the Internet of Things (IoT). The requirement for storing large amounts of data that must be evaluated is expected to increase in the coming years. The proliferation of innovative COVID-19 and the public's growing data utilization have resulted in the development of open-source data sets and visualizations, driving the market growth.

- Analytics is applied to telecommunications to improve visibility and gain insight into the organization's core operations and internal processes. It also helps in gaining knowledge of market conditions, spotting trends before they emerge, and then establishing forecasts based on the insights gained. Big data is now playing a significant role in this.

- According to the survey conducted by Zoom Video Communications, in March 2021, the study focused on event participation in person and virtually after the coronavirus (COVID-19) epidemic. Music performances, conferences, and religious services were examples of events. After the pendamic, 52 percent of respondents in the United States said they would attend events both in person and via video conferencing. In Japan, 65 percent of respondents agreed. Meanwhile, 10 percent of Indian respondents said they would only attend events through video conferencing after the epidemic.

- The increased use of IoT devices propels Analytics as a Services Market. According to a survey conducted by Appinventiv, with an estimated 19 million endpoints by 2023, connected automobiles are expected to be the largest category of the worldwide 5G Internet of Things (IoT) endpoint market. The global installed base of 5G IoT endpoints is expected to expand from 3.5 million in 2020 to approximately 49 million in 2023.

North America Region to Hold the Largest Share

- North America occupies the largest market share, mainly owing to the presence of many market players and the rising demand for the analytics platform. The growth of machine-to-machine communication (M2M) has also opened doors for cloud solutions in the region, with the United States being one of the largest cloud solutions markets in the world.

- Most large equipment manufacturers have local data centers for computing needs, as they operate and deploy their equipment globally. Thus, the manufacturers require analytics solutions to help maintain track of the facilities.

- Furthermore, social media apps such as Twitter, Instagram, Facebook, and YouTube generate massive amounts of data. The growing demand among businesses to analyze social media data for their specialized purposes is one element driving the expansion of the Analytics as a Service Market. For instance, IBM Corporation provides market analytics for sectors based on Twitter data, and the companies in the North American region are spending more investment in R&D to provide advanced analytics solutions.

- The companies in the North American region are making strategic partnerships and developing Analytics services. For instance, in February 2022, Teradata and Microsoft established a global partnership to connect the Teradata Vantage data platform with Microsoft Azure. With this partnership, organizations looking to upgrade their data analytics workloads with security, dependability, and flexibility - even on a large scale - can use both organizations' technologies.

- The Canadian e-commerce industry also offers a helping hand in boosting the demand for big data solutions. According to Worldpay, Canadian e-commerce sales crossed the mark of USD 50 billion in 2018, and it is expected to reach USD 80 billion by 2022.

Analytics as a Service Industry Overview

Analytics service is fragmented and has the potential to shift rivalry, opening up numerous new avenues for differentiation and value-added services. The huge expansion of capabilities in analytics technology also pushes the companies to keep up with rivals and gives away too much of the improved product performance. This environment escalates costs and erodes industry profitability. The major Analytics solution providers are partnering with various companies and technologies that support their overall product offerings.

- May 2022 - Wipro and Informatica have partnered to offer cloud-based data and analytics to market through the Wipro Fullstride cloud services data platform. By combining the offers of cloud hyperscalers with Wipro's platforms, IP, talent, and partner-led solutions, Informatica and Wipro have created a one-stop marketplace that creates business value and customer outcomes. Wipro's well-known data, analytics, and artificial intelligence (AI) skills, combined with Informatica's complete AI-powered data management solution, will enable cloud-based transformations to scale.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Cloud Adoption and Rise in the Data Volume Generated

- 5.1.2 Increasing Demand for Improving Organizations Internal Efficiency

- 5.2 Market Restraints

- 5.2.1 Data Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Enterprise Size

- 6.1.1 Small and Medium Enterprises

- 6.1.2 Large Enterprises

- 6.2 By End-User Industry

- 6.2.1 IT and Telecommunication

- 6.2.2 Energy and Power

- 6.2.3 BFSI

- 6.2.4 Healthcare

- 6.2.5 Retail

- 6.2.6 Manufacturing

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Microsoft Corporation

- 7.1.3 Oracle Corporation

- 7.1.4 SAP SE

- 7.1.5 Hewlett-Packard Enterprise Company

- 7.1.6 SAS Institute

- 7.1.7 Accenture PLC

- 7.1.8 Google Inc.

- 7.1.9 Amazon Web Services Inc.

- 7.1.10 Opera Solutions LLC

- 7.1.11 Atos SE

- 7.1.12 Host Analytics Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

分析即服務市場報告(按類型、組件、部署類型、企業規模、行業垂直和地區分類)2025 年至 2033 年

分析即服務市場報告(按類型、組件、部署類型、企業規模、行業垂直和地區分類)2025 年至 2033 年 全球分析即服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球分析即服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 分析即服務市場規模、佔有率和成長分析(按組件、分析類型、企業類型、部署類型、最終用途產業和地區)- 產業預測 2025-2032可視性即服務市場成長機會(2025-2031)分析即服務市場:按服務、類型、解決方案、部署、產業分類 - 2025-2030 年全球預測

分析即服務市場規模、佔有率和成長分析(按組件、分析類型、企業類型、部署類型、最終用途產業和地區)- 產業預測 2025-2032可視性即服務市場成長機會(2025-2031)分析即服務市場:按服務、類型、解決方案、部署、產業分類 - 2025-2030 年全球預測 AaaS(分析即服務)市場規模、佔有率、趨勢分析報告:按類型、公司規模、最終用途、地區、細分市場預測,2025-2030 年

AaaS(分析即服務)市場規模、佔有率、趨勢分析報告:按類型、公司規模、最終用途、地區、細分市場預測,2025-2030 年 分析即服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、部署模式、組件、應用程式、地區和競爭細分,2019-2029F

分析即服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、部署模式、組件、應用程式、地區和競爭細分,2019-2029F AaaS(Analytics as a Service)市場,各規模,佔有率,趨勢,產業分析報告:各零件,各提供,數據類型,各資料處理,各分析類型,各類型企業,各業界,各地區 - 市場預測,2024年~2032年

AaaS(Analytics as a Service)市場,各規模,佔有率,趨勢,產業分析報告:各零件,各提供,數據類型,各資料處理,各分析類型,各類型企業,各業界,各地區 - 市場預測,2024年~2032年 全球分析即服務市場:按產品、資料類型、資料處理、分析類型、產業、地區分類 - 到 2029 年的預測

全球分析即服務市場:按產品、資料類型、資料處理、分析類型、產業、地區分類 - 到 2029 年的預測 2023-2027分析即服務的全球市場

2023-2027分析即服務的全球市場