|

市場調查報告書

商品編碼

1630278

5G服務:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)5G Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

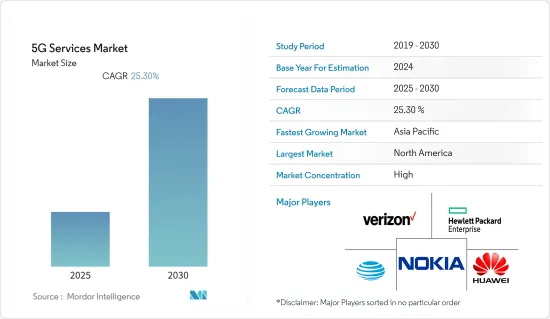

預計5G服務市場在預測期內的複合年成長率為25.3%。

主要亮點

- 5G 服務市場預計將改變各種寬頻服務領域,並增強各個最終用戶垂直領域的連線。推動市場佔有率擴大的主要因素是行動訂閱數量的增加、視訊內容的線上串流媒體、5G基礎設施的加強以及使用5G的各種物聯網應用。

- 工業自動化中的物聯網預計將從 5G 服務中受益最多。在工業 4.0 計劃和 5G-ACIA 等行業協會的影響下,3GPP 目前正在定義支援該細分市場的功能。它可能是特定於 5G 的部分,可用於本地區域使用案例和專用網路部署。

- 更有效地使用依賴低延遲的雲端解決方案將透過更快的寬頻服務下載速度來提高企業效率和創新,這反過來又將有助於行動電話設備製造商和內建分散式天線系統(5G新無線電(5G NR)規則)使通訊業者和目標商標產品製造商 (OEM)(例如 DAS)提供者能夠遵守 5G 新無線電 (5G NR) 規則。

- 考慮到提供不間斷的5G服務所需的高密度BTS單元,安裝必要的5G基礎設施和軟體升級的資本成本相當高。

- 此外,隨著 COVID-19 大流行增加了對虛擬空間的依賴,部署先進 5G 基礎設施的需求也達到了最大。業務轉移到雲端和其他虛擬空間的頻率不斷增加,正在推動對強大連接平台的投資。

5G服務市場趨勢

資料流量的增加和對高速資料連接的需求推動市場成長

- 5G 標準可能支援超高清音頻和影片,以創建依賴語音通訊的新應用,例如遠距臨場系統。 5G的設備密度、低延遲、安全和視訊能力有潛力支援豐富的通訊服務等加值通訊服務,特別是對企業而言。

- 北美擁有全球最高的行動寬頻和智慧型手機普及率。北美通訊業者開始關閉 2G 和 3G 網路以重新調整頻寬。隨著區域通訊業者轉向使用低、中型、高頻段混合的 5G 網路,這一趨勢預計將持續下去。

- 瑞典、阿拉伯聯合大公國等國家正在努力透過不斷的網路演進來增強用戶體驗並提供卓越的效能。隨著更先進的服務和設備的出現,通訊業者可能需要瞄準更高的服務品質水準。

- 此外,隨著對串流媒體服務的依賴程度越來越高,4G網路主要支援串流媒體AR/VR、4k/8k影片和360度影片,而5G影片內容將變得身臨其境型、資料密集。總流量將會增加。

- 5G 訂閱流量的成長將由智慧型手機訂閱數量的增加以及影片內容觀看對每次訂閱平均資料需求的增加所推動。

預計北美將佔據最大佔有率

- 美國對 5G 物聯網連接的需求預計將進一步增加。根據物聯網協會的數據,美國在智慧家庭採用方面處於領先地位,每個家庭擁有智慧家庭設備的比例最高,消費者擁有兩到三個使用案例(安全、能源、電器)的設備的趨勢最為強烈。

- 此外,該國預計將有數十億台設備連接到物聯網、設備和感測器。隨著5G網路的推出,Google和Facebook等公司將利用更寬的頻寬和更快的網路速度,並且很快就會開發出更先進的服務。

- 美國除了推出5G服務外,還需要注重軟體開發。重新利用目前用於軍事和氣象雷達的國家中頻頻譜可以提高網路效率。

- 中國也正在推廣自動駕駛和連網駕駛等技術,以改善道路安全、緩解道路擁塞並減少空氣污染。這些旨在獲得現實駕駛場景經驗的措施也得到了聯邦運輸和數位基礎設施部的支持。

5G服務業概況

5G服務業擁有AT&T、Verizon、諾基亞等主要企業,因此公司之間的競爭非常激烈。如果這些公司能夠持續創新其產品,他們就能超越競爭對手。這些公司透過併購、策略聯盟和研發在市場上佔有重要地位。

2022年5月,諾基亞公司宣布推出5G-Advanced,擴大了5G上行訊號的可達範圍。 5G-Advanced 透過利用更好的隨機存取通道覆蓋範圍,首先在初始連接設定期間改善上行鏈路覆蓋範圍,同時支援需要較低資料速率的新型設備,並支援將新的5G 功能引入垂直行業和市場。然後,5G-Advanced 動態變更上行鏈路波形,以在分配的連線預算內最佳化上行鏈路資料速率。當使用者靠近小區邊緣時,網路會動態地優先考慮可改善覆蓋範圍的波形,並在使用者移向小區中心時降低其優先權。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

- 技術簡介

- 按類型

- 增強型行動寬頻(EMBB)

- 超可靠低延遲通訊(URLLC)

- 大規模機器通訊(MMTC)

- 按類型

第5章市場動態

- 市場促進因素

- 對超低延遲連線的需求不斷成長

- 資料流量增加以及對高速資料連接的需求增加

- 市場限制因素

- 實施成本高

- 評估 COVID-19 對產業的影響

第6章 市場細分

- 按最終用戶產業

- 資訊科技與電信

- 媒體與娛樂

- 車

- 能源與公共事業

- 航太/國防

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 北美洲

第7章 競爭格局

- 公司簡介

- Nokia Corporation

- Huawei Technologies Co Ltd.

- AT&T Inc

- Verizon Communications Inc

- HP Enterprise Development LP

- T-Mobile USA, Inc.

- Deutsche Telekom AG

- Telefonaktiebolaget LM Ericsson

- Swisscom AG

- Vodafone Group

- BT Group

- Telstra Corporation Limited

第8章投資分析

第9章 市場機會及未來趨勢

The 5G Services Market is expected to register a CAGR of 25.3% during the forecast period.

Key Highlights

- The market for 5G services is expected to revolutionize the domain of various broadband services and empower connectivity across different end-user verticals. The main drivers responsible for increasing the market share are an increase in mobile subscriptions, online streaming of video content, strengthening 5G infrastructure, and various IoT applications utilizing 5G.

- IoT in industrial automation is expected to derive maximum benefit from 5G services. The functionality to support this segment is currently being defined in 3GPP, influenced by Industry 4.0 initiatives and industry bodies, such as 5G-ACIA. It will likely be a 5G-specific segment, valid for local area use cases and private network deployments.

- The use of more effective cloud solutions that rely on low latency improves firm efficiency and innovation through increased download speeds of broadband services, which also, in turn, leads the carriers and original equipment manufacturers (OEMs), such as cellular device manufacturers and in-building distributed antenna systems (DAS) providers to follow the 5G New Radio (5G NR) rules to enable such offerings.

- The capital costs of installing the required 5G infrastructure and software upgrades are considerably high, considering the high density of BTS units needed to provide uninterrupted 5G services.

- Moreover, with extensive reliance on virtual space increasing during the COVID-19 pandemic, the need to deploy advanced 5G infrastructure has become paramount. Increased migration frequency of business operations to the cloud and other virtual spaces has prompted investments in robust connectivity platforms.

5G Services Market Trends

Increasing Data Traffic and Demand for High Speed Data Connectivity will Drive the Market Growth

- 5G standards are likely to support ultra-HD voice and video to produce new applications that rely on voice communication, for instance, telepresence. The 5G's device density, low latency, security, and video capabilities may support added value communications offerings, like Rich Communication Services, especially for enterprises.

- North America has the highest levels of mobile broadband and smartphone adoption globally. The operators in North America have begun to shut down 2G and 3G networks to reframe the spectrum. This trend is expected to continue as regional operators switch to 5G networks using a mix of low, medium, and high-band spectrums.

- Countries such as Sweden and the United Arab Emirates strive to offer superior performance by strengthening user experience through continuous network evolution. As more advanced services and devices emerge, the operators may need to raise their targeted service quality levels even higher.

- Moreover, with increased dependence on streaming services, 4G networks supported majorly, streaming with AR/VR, 4k/8k video, and 360-degree videos, the 5G video content is expected to be immersive and consume a higher proportion of the overall data traffic.

- The 5G subscription traffic growth is driven by both the rising number of smartphone subscriptions and a need for increasing average data volume per subscription due to video content viewing.

North America is Expected to Hold the Largest Share

- 5G-enabled IoT connections are expected to witness a further increase in demand in the United States. As per the IoT Association, the United States leads, in terms of smart home adoption, with the highest smart home device ratio per household and the greatest consumer propensity to own devices across two or three use cases (security, energy, and appliances).

- Additionally, the country expects billions of devices to be connected to the internet, devices, and sensors of the Internet of Things. With the onset of 5G networks, the extensive bandwidth and faster internet speeds can be utilized by Google and Facebook; for instance, to develop more advanced services shortly.

- Apart from the launch of 5G services, the United States also needs to focus on software development. Repurposing the country's mid-band spectrums currently being used by the military or weather radars may make networks more efficient.

- Moreover, the country is promoting technologies, such as automated and connected driving, to enhance road safety, reduce road congestion, and decrease air pollution. Such initiatives to gain experience in actual driving scenarios are also supported by the Federal Ministry of Transport and Digital Infrastructure.

5G Services Industry Overview

The competitive rivalry among the 5G services industry players is high because of the presence of several significant players, including AT&T, Verizon, Nokia, and others. They could outperform rivals if they could consistently innovate their product offers. These businesses have established a substantial presence in the market through mergers and acquisitions, strategic alliances, and research and development.

In May 2022, Nokia Corporation announced its 5G-Advanced to widen the area that 5G uplink signals can reach. While 5G-Advanced will improve uplink coverage first with the initial connection setup by leveraging more excellent random access channel coverage, it will support new types of devices with low data-rate requirements and introduce 5G capabilities to new vertical sectors and markets. The uplink data rate will then be optimized within the allocated connection budget by 5G-Advanced dynamically altering the uplink waveform. When the user is close to the cell edge, the network will dynamically favor coverage-enhancing waveforms, and as the user travels into the cell center, it will deprioritize them.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.3.1 By Type

- 4.3.1.1 Enhanced Mobile Broadband (EMBB)

- 4.3.1.2 Ultra-reliable Low Latency Communications (URLLC)

- 4.3.1.3 Massive Machine Communications (MMTC)

- 4.3.1 By Type

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Ultra-Low Latency Connectivity

- 5.1.2 Increasing Data Traffic and Demand for High Speed Data Connectivity

- 5.2 Market Restraints

- 5.2.1 High Deployment Cost

- 5.3 Assessment of Impact of COVID-19 on the Industry

6 MARKET SEGMENTATION

- 6.1 End-user Industry

- 6.1.1 IT & Telecom

- 6.1.2 Media & Entertainment

- 6.1.3 Automotive

- 6.1.4 Energy & Utility

- 6.1.5 Aerospace & Defense

- 6.1.6 Other End-user Industries

- 6.2 Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 South Korea

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Rest of the World

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nokia Corporation

- 7.1.2 Huawei Technologies Co Ltd.

- 7.1.3 AT&T Inc

- 7.1.4 Verizon Communications Inc

- 7.1.5 HP Enterprise Development LP

- 7.1.6 T-Mobile USA, Inc.

- 7.1.7 Deutsche Telekom AG

- 7.1.8 Telefonaktiebolaget LM Ericsson

- 7.1.9 Swisscom AG

- 7.1.10 Vodafone Group

- 7.1.11 BT Group

- 7.1.12 Telstra Corporation Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNTIES AND FUTURE TRENDS

2025年5G服務全球市場報告

2025年5G服務全球市場報告 5G 服務市場:按通訊類型、應用程式和最終用戶分類 - 2025-2030 年全球預測

5G 服務市場:按通訊類型、應用程式和最終用戶分類 - 2025-2030 年全球預測 5G服務的全球市場的評估:各類型,各終端用戶,各產業,各地區,機會,預測(2017年~2031年)

5G服務的全球市場的評估:各類型,各終端用戶,各產業,各地區,機會,預測(2017年~2031年) 5G 服務市場報告:2030 年趨勢、預測與競爭分析

5G 服務市場報告:2030 年趨勢、預測與競爭分析 全球 5G 服務市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球 5G 服務市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 2024 年至 2028 年全球 5G 服務市場

2024 年至 2028 年全球 5G 服務市場 5G 服務市場規模、佔有率和成長分析:按應用程式、按最終用戶、按通訊、按地區 - 行業預測,2024-2031 年2024-2031 年全球 5G 服務市場

5G 服務市場規模、佔有率和成長分析:按應用程式、按最終用戶、按通訊、按地區 - 行業預測,2024-2031 年2024-2031 年全球 5G 服務市場 5G 服務市場規模和預測(2021 - 2031)、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、最終用戶和地理位置

5G 服務市場規模和預測(2021 - 2031)、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、最終用戶和地理位置 全球5G服務市場:2023年至2028年預測

全球5G服務市場:2023年至2028年預測