|

市場調查報告書

商品編碼

1630387

雲端供應鏈管理:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Cloud Supply Chain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

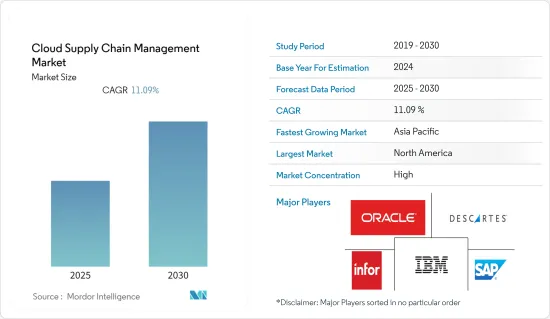

雲端供應鏈管理市場預計在預測期內複合年成長率為11.09%。

主要亮點

- 雲端運算正在迅速擴展,以支援協作運輸管理解決方案(TMS)和運輸管理的其他方面,例如網路容量採購、完整的可視性和事件管理,以及貨運支付和審核等輔助功能。

- 雲端運算現在是一種選擇,它為供應鏈管理人員提供了一種快速、高效地存取和部署透過 SaaS 模型交付的創新解決方案的途徑,從而顯著節省了成本。隨著工業 4.0 的出現,許多供應商正在實施數位技術來改進、自動化和現代化其整個流程。雲端整合變得越來越流行,因為它提供了可擴展性、安全性、成本、控制和速度等顯著優勢。

- COVID-19 大流行凸顯了對可靠且始終可用的供應鏈技術解決方案的需求不斷成長。資訊延遲是透過雲端實現的。為供應鏈提供動力的複雜系統和資料網路,從供應商及其供應商開始,透過入境物流提供者、公司工廠和倉庫、出庫運輸商、經銷商,最終整合到客戶。這就是雲端改變供應鏈的方式。雲端提供了快速、廉價且安全地提高資訊共用標準所需的氛圍和技術。供應鏈合作夥伴之間的無縫整合可輕鬆提供整個供應鏈的近乎即時的可見性。

- 企業在使用雲端基礎的解決方案時最常面臨的問題是資料保護和隱私。資料存取權限應僅授予核准成員,例如值得信賴的供應鏈合作夥伴。雖然雲端基礎的解決方案擁有許多安全通訊協定來防止對個人資料的不必要訪問,但資料安全最終取決於每個公司如何使用其可支配的資源。這對市場來說是一個挑戰。

雲端供應鏈管理市場趨勢

零售業預計將大幅成長

- 隨著大多數主要企業採用雲端基礎的技術,透過從資料中獲得前所未有的可見性和洞察力來轉變其供應鏈,零售業有望實現顯著成長。技術整合的重點是了解客戶旅程並提供實質改進。

- 因此,零售業參與者需要能夠幫助他們更有效地管理紙本文件以及結構化和非結構化資料的工具,以保持競爭力。這就是為什麼大多數主要企業都採用雲端基礎的技術來轉變其供應鏈,並從資料中獲得前所未有的可見性和洞察力。技術整合的重點是了解客戶旅程並提供實質改進。

- 隨著電子商務的發展增加了市場參與者的數量,客戶維繫變得比以往任何時候都更加重要。雲端運算透過擷取和分析來自多個來源的資料、識別模式和預測需求以及提供隨選服務來幫助改善客戶體驗。此外,零售商可以業務線應用程式存取所有業務內容,從而能夠為客戶提供及時的回應和優質的服務,並使自己與競爭對手區分開來。

- 此外,自動化工具透過數位化庫存資訊並使用分析和視覺化報告來改善分銷和庫存管理。這使得零售商能夠實現供應鏈自動化,從透過入境承運商管理和分配庫存到商店層級的匹配。這意味著更低的營運成本、更清晰、更快速的發票核對方式,以及更快的重新訂購時間以提高填充率。

北美佔據主要市場佔有率

- 北美市場正在顯著成長,這主要歸功於 GS1 標準的選擇,該標準旨在提高美國25 個產業的實體和數位通路供應鏈的安全性、效率和可見度。

- 美國的雲端採用率正在增加,這對市場做出了貢獻。根據 Stormforgein 2021 年 4 月發布的報告,18% 的北美受訪者表示,他們的組織每月在雲端使用上的支出在 10 萬至 25 萬美元之間。此外,44% 的受訪者預計他們的雲端支出將在未來 12 個月內略有增加,另外 32% 的受訪者預計他們的組織的雲端支出將在未來 12 個月內大幅增加。

- 美國客戶受益於日益多樣化的交通選擇。物流企業透過供應鏈管理軟體、包裝、物料輸送、倉儲、貨運、退貨管理、經紀等提供資訊流整合。

- 此外,封鎖和旅行限制擾亂了美國經濟的各個部門,在這段動盪時期對供應鏈業務產生了重大影響。在這個不確定的時期,企業越來越依賴雲端運算和儲存來提高其供應網路的靈活性和敏捷性。

- 此外,加拿大政府制定了「雲端優先」策略,該策略在啟動資訊技術投資、措施、策略和計劃時將雲端服務確定為主要交付選項並對其進行評估。雲端還允許加拿大政府利用私人提供者的創新,並使資訊技術更加敏捷。這些措施預計將為雲端供應鏈管理提供充足的機會。

雲端供應鏈管理產業概況

雲端供應鏈管理市場高度集中,由Oracle公司、SAP SE、笛卡爾系統集團公司、Infor公司和IBM公司等主要企業主導。這些擁有重要市場佔有率的主要企業正致力於擴大海外基本客群。這些公司正在利用策略聯合措施來擴大市場佔有率並提高盈利。然而,隨著產品創新和技術進步,中小企業正在透過獲得新契約和開發新市場來增加其在市場中的佔有率。

- 2022 年 5 月 - SAP 與 Apple 合作,建立跨數位供應鏈的協作。作為與 Apple 持續合作關係的一部分,SAP 宣布推出一套新的應用程式,以簡化數位供應鏈,並為員工提供簡單的工具來改變他們在 iPhone 和 iPad 上的工作方式。

- 2021 年 9 月 - 工業雲端供應商 Infor 發布了 Infor Hospitality Management Solutions (HMS) 3.8.4 版,這是 Infor 飯店解決方案套件中完全支援雲端的飯店管理軟體的最新版本。此更新的重點是提供用於最佳化和提供客製化服務的新選項。 Infor 的 HMS 是一種即時、可存取、雲端基礎的技術,可滿足當今客戶繁忙的日程安排,並允許飯店客製化流暢、無摩擦的體驗。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

第5章市場動態

- 市場促進因素

- 中小型企業快速採用雲端基礎的解決方案進行需求管理

- 電子商務領域的成長加速了客戶維繫技術解決方案的採用

- 市場限制因素

- 企業對安全和隱私的擔憂日益增加

第6章 市場細分

- 按解決方案

- 需求規劃與預測

- 庫存/倉庫管理

- 產品生命週期管理

- 運輸與物流管理

- 銷售/營運計劃

- 其他解決方案(採購、產品主資料管理、訂單管理)

- 依部署類型

- 混合雲

- 公有雲

- 私有雲端

- 按組織規模

- 主要企業

- 小型企業

- 按最終用戶產業

- 零售

- 飲食

- 製造業

- 車

- 石油和天然氣

- 衛生保健

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭狀況

- 公司簡介

- SAP SE

- Oracle Corporation

- Infor Inc

- Descartes Systems Group Inc

- IBM Corporation

- JDA Software Group Inc

- Manhattan Associates Inc

- Logility Inc.

- Kinaxis Inc

- HighJump Software Inc

- CloudLogix Inc.

- TECSYS, Inc.

第8章投資分析

第9章市場展望

The Cloud Supply Chain Management Market is expected to register a CAGR of 11.09% during the forecast period.

Key Highlights

- Cloud computing is quickly growing to support collaborative transportation management solutions (TMS) and other aspects of transportation management, such as sourcing of network capacity, complete visibility and event management, and ancillary functions, including freight pay and audit.

- Cloud computing is now perceived as a significant cost-saving alternative, giving a route through which supply chain executives can quickly and efficiently access innovative solutions delivered through a SaaS model and deploy them at scale. With the emergence of industry 4.0, numerous vendors are implementing digital technologies to improve, automate, and modernize the entire process. Integrating the cloud is becoming increasingly popular because it offers substantial advantages such as scalability, security, cost, control, and speed.

- The COVID-19 pandemic has highlighted the growing demand for dependable, anytime-accessible supply chain technology solutions. Through the cloud, information latency is achieved. It integrates the intricate web of systems and data that serves up the supply chain, starting with suppliers and their suppliers and moving on to inbound logistics providers, a company's factories and warehouses, outbound carriers, distributors, and eventually customers. Thereby making the cloud transformative for supply chains. It provides the atmosphere and technology required to quickly, inexpensively, and securely raise the bar for information sharing. Near-real-time visibility across the whole supply chain is easily provided by seamless integration among supply chain partners.

- The most frequent problem businesses have with cloud-based solutions is data protection and privacy. Data access should only be permitted for approved members, such as reputable supply chain partners. Data security ultimately depends on how each firm uses the resources at their disposal, even while cloud-based solutions have numerous security protocols in place to prevent unwanted access to personal data. This acts as a challenge to the market.

Cloud Supply Chain Management Market Trends

Retail Industry is Expected to Register a Significant Growth

- The retail industry is expected to register significant growth as most key players are adopting cloud-based technologies to transform their supply chains with unprecedented visibility and insights from data. Technology integrations focus on understanding the customer journey and providing substantive improvement.

- With the growing retail sector, the adoption of advanced technologies is significantly growing; therefore, the retail industry players require tools that enable organizations to manage paper documents and structured and unstructured data more effectively to remain competitive. Hence, most key players are adopting cloud-based technologies to transform their supply chains with unprecedented visibility and insights from data. Technology integrations focus on understanding the customer journey and providing substantive improvement.

- Customer retention has become more important than before due to increased players in the market with the growth of e-commerce. Cloud computing helps enhance customer experiences as it captures and analyzes data from many sources, identifies patterns and predicts needs, and offers on-demand services. It also provides retailers access to all business content from the core line-of-business applications to provide timely responses and exceptional service to the customers, separating them from their competition.

- Additionally, automation tools improve distribution and inventory management by digitizing inventory information and using analytics and visual reporting. Therefore, it enables retailers to automate the supply chain from the inbound carrier to manage and distribute inventory to store-level reconciliation. It leads to lower operational costs, a more straightforward, faster way to reconcile invoices, and improved fill rates by shrinking reorder time.

North America Hold Significant Market Share

- North America may experience notable market growth, principally driven by the selection of GS1 standards designed to promote the safety, efficiency, and visibility of supply chains across physical and digital channels in 25 sectors in the United States.

- The growing adoption of cloud in the US is contributing to the market. According to a report published by Stormforgein in April 2021, 18% of respondents from North America state that their organization has a monthly cloud spend of between USD 100,000 and USD 250,000. Further, 44% of respondents expect cloud spending to increase somewhat over the next 12 months, while another 32% indicate that they expect their organization's cloud spending to increase significantly over the next 12 months.

- Customers in the United States are profiting from the diversity of transport modes in their increasingly connected environment. Logistics businesses offer the integration of information flow through supply chain management software, packaging, material handling, warehousing, forwarding, returned goods management, and brokerage.

- Further, Lockdowns and travel restrictions have disrupted different sectors of the US economy and considerably influenced supply chain operations during these periods of fast upheaval. Businesses increasingly rely on cloud computing and storage in these uncertain times to increase the flexibility and agility of their supply networks.

- Moreover, the Government of Canada has a "cloud-first" strategy whereby cloud services are identified and evaluated as the principal delivery option when initiating information technology investments, initiatives, strategies, and projects. The cloud will also allow the Government of Canada to harness the innovation of private-sector providers to make its information technology more agile. Such initiatives are expected to provide ample opportunities to the cloud supply chain management.

Cloud Supply Chain Management Industry Overview

The cloud supply chain management market is highly concentrated and controlled by dominant players, like Oracle Corporation, SAP SE, Descartes Systems Group Inc., Infor Inc., and IBM Corporation. With a notable share in the market, these principal players are concentrating on expanding their customer bases across foreign countries. These businesses are leveraging strategic collaborative initiatives to strengthen their market shares and enhance their profitability. However, with product innovations and technological advancements, midsize to smaller firms are growing their market presence by securing new contracts and tapping new markets. Some of the recent developments in the market are:

- May 2022- SAP has partnered with Apple to build collaborations throughout the digital supply chain. SAP has unveiled a new suite of apps that streamline the digital supply chain and equip workers with simple tools as part of its ongoing relationship with Apple to transform how people operate on iPhones and iPads.

- September 2021- Infor, the industrial cloud provider, has released the latest edition of the fully cloud-enabled hotel management software in the Infor Hospitality suite of solutions, Infor Hospitality Management Solution (HMS) version 3.8.4. This update focuses on giving new choices for optimizing and delivering customised services. Infor HMS is cloud-based technology accessible in real time, keeping up with modern customers' hectic schedules and allowing hotels to customize a smooth and frictionless experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Adoption of Cloud -based Solution for Demand Management by SMEs

- 5.1.2 Increasing Growth of E - commerce Sector Has Fueled the Adoption of Technological Solutions to Retain Customers

- 5.2 Market Restraints

- 5.2.1 Increasing Security and Privacy Concerns Among Enterprises

6 MARKET SEGMENTATION

- 6.1 By Solution

- 6.1.1 Demand Planning and Forecasting

- 6.1.2 Inventory and Warehouse Management

- 6.1.3 Product Life-Cycle Management

- 6.1.4 Transportation & Logistics Management

- 6.1.5 Sales and Operations Planning

- 6.1.6 Other Solutions (Procurement and Sourcing, Product Master Data Management, and Order Management)

- 6.2 By Deployment Type

- 6.2.1 Hybrid Cloud

- 6.2.2 Public Cloud

- 6.2.3 Private Cloud

- 6.3 By Organization Size

- 6.3.1 Large Enterprises

- 6.3.2 Small and Medium Enterprises

- 6.4 By End-user Industries

- 6.4.1 Retail

- 6.4.2 Food & Beverage

- 6.4.3 Manufacturing

- 6.4.4 Automotive

- 6.4.5 Oil & Gas

- 6.4.6 Healthcare

- 6.4.7 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 SAP SE

- 7.1.2 Oracle Corporation

- 7.1.3 Infor Inc

- 7.1.4 Descartes Systems Group Inc

- 7.1.5 IBM Corporation

- 7.1.6 JDA Software Group Inc

- 7.1.7 Manhattan Associates Inc

- 7.1.8 Logility Inc.

- 7.1.9 Kinaxis Inc

- 7.1.10 HighJump Software Inc

- 7.1.11 CloudLogix Inc.

- 7.1.12 TECSYS, Inc.

8 INVESTMENT ANALYSIS

9 MARKET OUTLOOK

2025年認知供應鏈全球市場報告

2025年認知供應鏈全球市場報告 供應鏈管理及物流的季報:2025年第一季

供應鏈管理及物流的季報:2025年第一季 2025 年機場供應鏈管理全球市場報告

2025 年機場供應鏈管理全球市場報告 智慧和行動供應鏈解決方案市場(按組件、應用和地區分類)

智慧和行動供應鏈解決方案市場(按組件、應用和地區分類) 供應鏈風險管理市場:依組件、部署、最終用途產業和地區

供應鏈風險管理市場:依組件、部署、最終用途產業和地區 2025 年智慧與行動供應鏈解決方案全球市場報告

2025 年智慧與行動供應鏈解決方案全球市場報告 供應鏈管理市場評估:依解決方案類型、部署模式、垂直、公司規模、地區、機會、預測,2018-2032 年

供應鏈管理市場評估:依解決方案類型、部署模式、垂直、公司規模、地區、機會、預測,2018-2032 年 印度的供應鏈管理市場評估:各解決方案類型,各部署模式,各業界,不同企業規模,各地區,機會,預測,2018年~2032年

印度的供應鏈管理市場評估:各解決方案類型,各部署模式,各業界,不同企業規模,各地區,機會,預測,2018年~2032年 2025 年至 2033 年基於 SaaS 的 SCM 市場報告(按解決方案、部署模式、最終用戶、應用程式、垂直行業和地區分類)

2025 年至 2033 年基於 SaaS 的 SCM 市場報告(按解決方案、部署模式、最終用戶、應用程式、垂直行業和地區分類) 2025 年醫療保健供應鏈管理全球市場報告

2025 年醫療保健供應鏈管理全球市場報告