|

市場調查報告書

商品編碼

1631575

光纖陀螺儀 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Fiber Optic Gyroscope - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

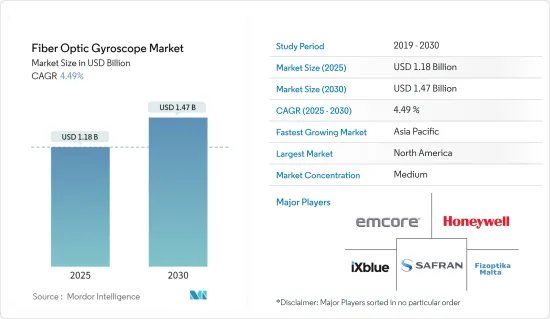

光纖陀螺儀市場規模預計到 2025 年為 11.8 億美元,預計到 2030 年將達到 14.7 億美元,預測期內(2025-2030 年)複合年成長率為 4.49%。

光纖陀螺儀以其高輸出速率和測量各種角度角速度的準確性而聞名,並且正在迅速被採用。這種趨勢在非載人軍用車輛和機載監控系統中尤其明顯,推動了航太和國防領域對陀螺儀的需求。

光纖陀螺儀在航太、國防和工業等各個領域越來越受到關注。背後的原因包括體積小、重量輕、壽命長、可靠性高、功耗低、適合大規模生產。因此,每個細分市場的需求都在增加,這推動了市場的成長。隨著世界各國政府增加軍事開支以增強防禦能力,對光纖陀螺儀的需求正在迅速增加,特別是遠程操作車輛導引等應用。

推動這一市場發展的是無人機和無人機在國防和商業領域的日益普及。根據美國聯邦航空管理局 (FAA) 的報告,2023 年美國約有 516,800 架無人機註冊用於休閒飛行。值得注意的是,這一數字不包括業餘無人機,因為它們不需要註冊。

加強光纖陀螺儀(FOG)市場的主要促進因素包括新興經濟體和成熟經濟體國防支出的增加,以及工業和家庭自動化的快速採用。以色列是軍事應用領域的領先國家,總部位於特拉維夫的 Airobotics 正在展示其實力,在企業自主解決方案方面處於領先地位,推動光纖陀螺儀市場的發展。在石油鑽井過程中使用光纖陀螺儀進行測量以及遠程操作車輛的興起和發展正在進一步推動市場成長。

此外,用於家用電子電器和工業應用的光纖陀螺儀(FOG)小型化趨勢以及降低製造成本的努力也對市場成長做出了重大貢獻。透過縮小光纖陀螺的尺寸和成本,製造商正在將其應用擴展到家用電子電器、汽車、航太和工業自動化等領域。光纖陀螺儀卓越的準確性和可靠性正在刺激其在新市場和現有市場中的採用。由於對小型高性能感測器的需求迅速成長,預計未來幾年光纖陀螺市場將顯著成長。

儘管市場對光纖陀螺儀的需求很大,但其複雜、昂貴且耗時的製造流程是主要限制。這項限制限制了光纖陀螺儀的滲透率,在一定程度上抑制了市場的成長。

宏觀經濟因素,包括地緣政治問題和經濟狀況的變化,對於塑造市場至關重要。例如,經濟強勁的地區將更多預算分配給先進的軍事和國防系統,從而增加了這些解決方案的採用。戰爭等地緣政治挑戰進一步推動市場成長。

光纖陀螺儀市場趨勢

航太航太領域佔市場主導地位

- 航太業是光纖陀螺儀的主要最終用戶,廣泛採用這些設備進行飛行控制、地面探測和動態全球定位系統 (GPS) 追蹤。再加上航空領域的投資趨勢,尤其是亞太地區的投資趨勢,這一趨勢將加強對光纖陀螺儀的需求。

- 例如,印度正迅速成為世界上最大的航空市場之一。過去一年,印度航空、靛藍航空、阿卡薩航空等印度主要航空公司共訂購了1,100多架飛機,成為全球史上最大的民航機訂單。

- 同樣,全球市場也反映了這一趨勢。領先的民航機製造商波音公司預計,2023 年至 2042 年間,全球將交付約 42,595 架新民航機。光纖陀螺儀 (FOG) 在飛機導航系統、飛機運動監測以及角速度和速度等指標中發揮關鍵作用,預計此類案例將推動市場成長。

- 特別是光纖陀螺在太空火箭及相關系統中扮演重要角色。此外,SpaceX 和 Blue Origin 等私人公司的出現,其願景是讓太空旅行成為現實,進一步擴大了已探索的市場機會。

- 根據《喬納森太空報告》報道,到 2023 年,將有大約 9,115 顆活躍衛星繞地球運行,與前一年同期比較增加 35%。陀螺儀在太空船和運載火箭中發揮著至關重要的作用,使它們能夠偵測方向和角度運動。此功能允許精確控制和追蹤太空船從其初始位置的運動。因此,衛星發射增加,創造了有利於該市場成長的環境。

亞太地區成長率顯著

- 未來幾年,由於幾個新興經濟體國防預算的增加,亞太地區的市場將顯著成長。特別是,中國和日本正在推動該地區光纖陀螺儀的需求。推動這一成長的因素包括航太和國防領域研發活動的活性化、工業化的快速發展以及對增強感測器、無人機和無人海上船舶的大量投資。

- 中國正在成為汽車工業的製造地,再加上無人駕駛汽車的新發展計劃,正在刺雷射纖陀螺儀的採用。中國、日本和韓國等國家更嚴格的監管進一步刺激了企業投資。因此,最終用戶公司正在優先考慮各種監控系統中的方向測量,突顯了不斷成長的市場。

- 近年來,印度已成為軍事和國防產品的主要消費國,這使其成為 FOG 利潤豐厚的市場。例如,2024 年 2 月,美國國務院核准了一項可能價值 39 億美元的交易,向印度購買通用原子公司的 MQ-9B 無人機。該協議強調華盛頓和新德里之間加強國防和安全合作。為印度陸軍提案的一攬子計畫包括31架「天空衛士」無人機、310枚小口徑炸彈和170枚「地獄火」飛彈。該套件還包括專門用於海上運輸的「海洋衛士號」的雷達和反潛設備。

- 印度在航太和國防生產方面取得了重大進展,為已開發市場提供了機會。例如,最近,印度第一家民用無人機製造廠阿達尼-埃爾比特先進系統印度有限公司成功向以色列交付了20多架Hermes 900中中高度(MALE)無人機。印度阿達尼防務與航空航太公司和以色列埃爾比特系統公司位於海得拉巴的合資企業是第一家在以色列境外生產這些無人機的公司。

- 其他國家也出現了類似的趨勢。例如,中國正在積極增強其無人機能力。據中國民航局稱,2023年終,中國註冊無人機將達到127萬架,與前一年同期比較成長32.2%。因此,這些趨勢和進步將在預測期內推動該地區受訪市場的成長。

光纖陀螺儀產業概況

光纖陀螺儀市場競爭溫和,幾個主要企業處於前列。這些參與企業中的少數幾個目前在市場佔有率上佔據主導地位。無人駕駛汽車的快速崛起和持續的技術進步為市場供應商提供了誘人的機會。現有公司之間的競爭仍然溫和,但公司正在利用創新策略來刺激市場需求。然而,複雜且耗時的製造流程、高投資和低成本效益等挑戰正在阻礙光纖陀螺儀製造的新參與企業。主要市場參與企業包括 Emcore、霍尼韋爾和賽峰。

2024年6月,Exail與萊茵金屬公司簽署了一份重要契約,同意為德國陸軍的Caracal 4X4車輛交付1004套Advans Ursa慣性導航系統(INS)。 Advans Ursa 利用 Exile 先進的光纖陀螺儀 (FOG) 技術,成為專為戰術導航而設計的緊湊型、經濟型 INS。即使在惡劣的條件下,該系統也能保證準確可靠的導航資料。因此,即使在沒有 GNSS 訊號的情況下,Caracal 車輛也可以不受任何限制地自信地導航,無論時間或距離如何。

2024 年 6 月,慣性實驗室發布了其最新產品 INS-FI。這款 GPS 輔助慣性導航系統 (INS) 採用戰術級光纖陀螺儀 (FOG) 技術,將其定位為市場上最先進、最可靠的 INS 解決方案之一。擁有與所有衛星群相容的多頻段 GNSS 接收器,包括 GPS、GALILEO、GLONASS、QZSS、NAVIC 和 BEIDOU。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

- 宏觀經濟趨勢對光纖陀螺儀市場的影響

第5章市場動態

- 標記驅動程式

- 無人機在國防和民用領域的快速成長

- 擴大全球國防費用

- 市場限制因素

- 複雜性的顯著增加正在挑戰市場需求

- 先進電子機械系統對陀螺儀的需求不斷成長

第6章 市場細分

- 按線圈類型

- 法蘭式

- 輪轂型

- 自主型

- 按檢測軸

- 1軸

- 2軸

- 3軸

- 按設備

- 指南針羅盤

- 慣性測量單元

- 慣性導航系統

- 按最終用戶產業

- 航太

- 機器人技術

- 汽車(自動駕駛汽車)

- 防禦

- 產業

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 澳洲/紐西蘭

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- EMCORE Corporation

- Honeywell International Inc.

- KVH Industries Inc.

- Safran Colibrys SA

- iXBlue SAS

- Northrop Grumman LITEF GmbH

- Cielo inertial Solutions Ltd

- Fizoptika Malta

- NEDAERO

- Optolink LLC

- Advanced Navigation

第8章投資分析

第9章市場的未來

The Fiber Optic Gyroscope Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.47 billion by 2030, at a CAGR of 4.49% during the forecast period (2025-2030).

Fiber optic gyroscopes, known for their high output rates and precision in measuring angular velocity across diverse angles, are witnessing a surge in adoption. This trend is particularly evident in uncrewed military vehicles and airborne surveillance systems, driving up the demand for these gyroscopes in the aerospace and defense sectors.

Various sectors, including aerospace, defense, and industrial domains, are increasingly turning to fiber optic gyroscopes. This is attributed to their compact size, lightweight nature, longevity, reliability, low power consumption, and suitability for mass production. As a result, this heightened demand across sectors propels the market's growth. With governments worldwide ramping up military expenditures to bolster their defense capabilities, there is a corresponding surge in demand for fiber optic gyroscopes, especially in applications like remotely operated vehicle guidance.

The market is driven by the growing adoption of drones and UAVs across defense and commercial sectors. The Federal Aviation Administration (FAA) reported that in 2023, approximately 516.8 thousand drones were registered for recreational flying in the United States. Notably, this count excludes hobbyist drones, which are not required to be registered.

Key drivers bolstering the fiber optics gyroscope (FOG) market include heightened defense spending in both emerging and established economies, alongside a surge in automation adoption across industries and households. Israel, a frontrunner in military application advancements, showcases its prowess with Tel Aviv's Airobotics spearheading autonomous solutions for enterprises, propelling the fiber optic gyroscope market. Using fiber optic gyroscopes for measurement during oil drilling processes and the rising prominence and evolution of remotely operated vehicles further fuel the market's growth.

The market's growth is also being significantly driven by the trend of miniaturizing fiber optic gyroscopes (FOGs) for consumer electronics and industrial applications, alongside efforts to cut manufacturing costs. By reducing the size and cost of FOGs, manufacturers are broadening their applications to sectors like consumer electronics, automotive, aerospace, and industrial automation. This broadened application is spurring greater adoption of FOGs in new and established markets due to their superior precision and reliability. With the surging demand for compact, high-performance sensors, the FOG market is set for substantial growth in the years ahead.

Despite significant demand for fiber optic gyroscopes in the market, their complicated, costly, and time-consuming manufacturing process poses a considerable constraint. This limitation restricts the widespread adoption of fiber optic gyroscopes and curtails the market's growth to some degree.

Macroeconomic factors, including shifting geopolitical issues and economic conditions, are pivotal in shaping the market. For example, regions enjoying robust economic health typically allocate greater budgets to advanced military and defense systems, thereby broadening the adoption of these solutions. Geopolitical challenges, such as wars, further drive the growth of the market studied.

Fiber Optic Gyroscope Market Trends

Aerospace and Aviation Segment to Dominate the Market

- The aerospace and aviation industry, a major end-user of fiber optic gyroscopes, extensively employs these devices in flight control, ground detection, and dynamic global positioning system (GPS) tracking. Coupled with rising investments in the aviation sector, particularly in the Asia-Pacific region, this trend is set to bolster the demand for fiber optic gyroscopes.

- For instance, India is rapidly establishing itself as one of the world's largest aviation markets. Over the past year, leading Indian airlines, including Air India, Indigo, and Akasa Air, collectively placed orders for more than 1,100 aircraft, marking one of the largest commercial aircraft orders in global history.

- Similarly, the global market mirrors this trend. Boeing, a leading name in commercial aircraft manufacturing, projects that from 2023 to 2042, the global commercial fleet will welcome approximately 42,595 new aircraft deliveries. Given the prominent role of fiber optic gyroscopes (FOGs) in aircraft navigation systems, monitoring motion in aviation, and capturing metrics like angular velocity and speed, such instances are poised to propel the growth of the market.

- As countries like India ramp up their space missions, the growing activities in the space exploration sector are set to boost the market studied, especially since FOGs play a crucial role in space rockets and related systems. Moreover, the emergence of private companies like SpaceX and Blue Origin, with their vision of making space travel a reality, further amplifies the opportunities in the market studied.

- As reported by Jonathan Space Report, 2023 witnessed approximately 9,115 active satellites orbiting Earth, marking a 35% surge from the prior year's count. Gyroscopes play a pivotal role in space vehicles and launch rockets, enabling them to detect orientation and angular motion. This capability allows precise control and tracking of the craft's movement from its initial position. Consequently, the uptick in satellite launches fosters a conducive environment for the growth of the market studied.

Asia-Pacific to Witness a Significant Growth Rate

- In the coming years, the Asia-Pacific is set to witness significant market growth, driven by rising defense budgets in several emerging economies. Notably, China and Japan are leading the demand for fiber optic gyroscopes in the region. Contributing to this growth are factors such as heightened R&D activities in the aerospace and defense segment, swift industrialization, and substantial investments to enhance sensors, drones, and unmanned maritime vessels.

- China's emergence as a manufacturing hub for the automobile industry, coupled with its new development plans for driverless vehicles, is spurring the adoption of fiber optic gyroscopes. The tightening of regulations in countries like China, Japan, and South Korea has further incentivized corporate investments. As a result, end-user companies increasingly prioritize orientation measurement in various monitoring systems, underscoring the market's expansion.

- In recent years, India has emerged as a leading spender on military and defense products, making it a lucrative market for FOGs. For example, in February 2024, the US State Department approved a potential USD 3.9 billion deal for General Atomics MQ-9B drones to India. This deal underscores the strengthening of defense and security cooperation between Washington and New Delhi. The proposed package for the Indian military encompasses 31 SkyGuardian unmanned aerial vehicles, 310 Small Diameter Bombs, and 170 Hellfire missiles. The package includes radars and anti-submarine equipment for the maritime-focused SeaGuardian variant.

- India is making notable strides in aerospace and defense production, driving opportunities in the studied market. For instance, recently, Adani-Elbit Advanced Systems India Ltd, India's inaugural private UAV manufacturing facility, successfully delivered over 20 Hermes 900 medium-altitude, long-endurance (MALE) UAVs to Israel. This joint venture, based in Hyderabad and formed between India's Adani Defence and Aerospace and Israel's Elbit Systems, proudly stands as the first entity to produce these UAVs outside of Israel.

- Other countries are witnessing similar trends. For example, China is actively bolstering its UAV capabilities. According to the Civil Aviation Administration of China (CAAC), by the end of 2023, China boasted 1.27 million registered drones, marking a 32.2% increase from the prior year. Consequently, these trends and advancements are poised to fuel the growth of the market studied in the region during the forecast period.

Fiber Optic Gyroscope Industry Overview

The fiber optic gyroscope market features a moderate level of competition, with several key players at the forefront. A select few of these players currently hold a dominant position in terms of market share. The swift ascent of unmanned vehicles, coupled with ongoing technological advancements, presents enticing opportunities for market vendors. While the competitive rivalry among established players remains moderate, companies are leveraging innovation strategies to drive market demand. However, challenges such as intricate and time-intensive manufacturing processes, substantial investments, and a low cost-benefit ratio have deterred new entrants from producing fiber optic gyroscopes. Some key market players include Emcore, Honeywell, and Safran.

June 2024: Exail clinched a significant deal with Rheinmetall, agreeing to deliver 1004 units of its Advans Ursa inertial navigation systems (INS) for the German Army's Caracal 4X4 vehicles. Leveraging Exail's advanced Fiber-Optic Gyroscope (FOG) technology, the Advans Ursa stands out as a compact and budget-friendly INS specifically designed for tactical navigation. This system ensures accurate and dependable navigation data, even in challenging conditions. As a result, Caracal vehicles can confidently navigate without any constraints, regardless of time or distance, even in scenarios where GNSS signals are entirely absent.

June 2024: Inertial Labs has unveiled its newest offering, the INS-FI. This GPS-assisted Inertial Navigation System (INS) leverages Tactical-grade Fiber Optic Gyroscope (FOG) technology, positioning it as one of the market's most sophisticated and dependable INS solutions. It boasts a multi-band GNSS receiver compatible with all constellations, including GPS, GALILEO, GLONASS, QZSS, NAVIC, and BEIDOU.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macroeconomic Trends on the Fiber Optic Gyroscope Market

5 MARKET DYNAMICS

- 5.1 Marker Drivers

- 5.1.1 Rapid Growth of Unmanned Vehicle in Defense and Civilian Applications

- 5.1.2 Expanding Defense Expenditure Globally

- 5.2 Market Restraints

- 5.2.1 Substantial Rise in Complexity Challenging the Market Demand

- 5.2.2 Increasing Demand for Advanced Microelectromechanical Systems Gyroscopes

6 MARKET SEGMENTATION

- 6.1 By Coil Type

- 6.1.1 Flanged

- 6.1.2 Hubbed

- 6.1.3 Freestanding

- 6.2 By Sensing Axis

- 6.2.1 1-axis

- 6.2.2 2-axis

- 6.2.3 3-axis

- 6.3 By Device

- 6.3.1 Gyrocompass

- 6.3.2 Inertial Measurement Unit

- 6.3.3 Inertial Navigation System

- 6.4 By End-user Industry

- 6.4.1 Aerospace and Aviation

- 6.4.2 Robotics

- 6.4.3 Automotive (Autonomous Vehicles)

- 6.4.4 Defense

- 6.4.5 Industrial

- 6.4.6 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 EMCORE Corporation

- 7.1.2 Honeywell International Inc.

- 7.1.3 KVH Industries Inc.

- 7.1.4 Safran Colibrys SA

- 7.1.5 iXBlue SAS

- 7.1.6 Northrop Grumman LITEF GmbH

- 7.1.7 Cielo inertial Solutions Ltd

- 7.1.8 Fizoptika Malta

- 7.1.9 NEDAERO

- 7.1.10 Optolink LLC

- 7.1.11 Advanced Navigation