|

市場調查報告書

商品編碼

1940769

二極體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Diode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

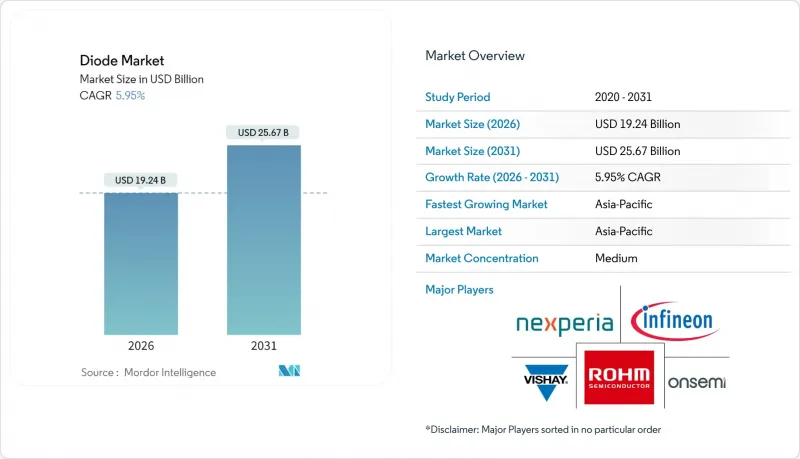

二極體市場預計將從 2025 年的 181.6 億美元成長到 2026 年的 192.4 億美元,預計到 2031 年將達到 256.7 億美元,2026 年至 2031 年的複合年成長率為 5.95%。

儘管家用電子電器仍是二極體的最大終端用戶,市佔率達23.2%,但隨著全球電動車專案的加速推進,汽車應用領域正以6.8%的複合年成長率(CAGR)成為成長最快的領域。亞太地區佔全球營收的58.86%,年增率達6.63%,主要得益於中國、日本和韓國密集的製造群。表面黏著技術封裝佔出貨量的61.2%,而晶片級封裝的年複合成長率也高達7.1%,因為行動電話和物聯網製造商對封裝尺寸的要求越來越小。

全球二極體市場趨勢與洞察

家用電子電器生態系的數位化

智慧型手機、穿戴式裝置和連網家庭設備增加了每個系統中半導體的數量,從而推動了對用於訊號調理、電池保護和數據線保護的分立元件的需求。德克薩斯(TI) 的 ESDS31x 系列等小訊號靜電放電陣列可提供 ±30kV 的保護,資料傳輸速率高達 5Gbps,並支援 USB、HDMI 和乙太網路介面。亞太地區的製造商組裝了全球約 60% 的電子硬體,這支撐了對用於保護高速互連的二極體陣列的強勁需求。

加速電動車生產和車用充電器的普及

電動動力傳動系統的日益普及推動了對汽車半導體的需求。碳化矽和氮化鎵二極體可降低牽引逆變器和800V充電器中的開關損耗。安森美半導體的EliteSiC平台已被大眾汽車用於其下一代電動車。英飛凌的CoolSiC 1200V MOSFET使DC-DC級能夠在900V以上電壓下工作而無需額外的隔離,從而在降低系統成本的同時提高了功率密度。

原料價格波動(矽、砷化鎵、氮化鎵)

中國供應了大部分原生鎵原料,而出口限制導致砷化鎵(GaAs)和氮化鎵(GaN)裝置的晶圓成本飆升。全球僅20%的電子廢棄物妥善回收,造成關鍵金屬的流失,加劇了供應緊張和價格波動。碳化矽(SiC)晶圓的產量比率仍然不穩定,取決於製造技術的成熟度和基板品質。

細分市場分析

到2025年,雷射二極體將成為最大的二極體市場,規模達64.8億美元,年複合成長率(CAGR)為8.25%,主要受汽車頭燈、雷射雷達感測和高速光纖通訊等應用領域需求成長的推動。整流器和肖特基二極體將繼續在功率轉換領域佔據一席之地,但其成長率將處於個位數中段,低於雷射二極體的普及速度。

工業切割、投影機和3D列印將推動對多模雷射二極體的需求,而醫用雷射則需要更嚴格的波長穩定性,從而推高平均售價。在伺服器電源領域,英飛凌的氮化鎵電晶體正與肖特基二極體整合,以減少死區時間損失並提高效率,這為跨領域合作提供了一個良好的範例。

區域分析

亞太地區預計到2025年將佔全球收入的58.30%,並在2031年之前保持6.45%的複合年成長率,這主要得益於中國、日本和韓國一體化的供應鏈。 2023年,中國在全球晶片銷售中佔據了絕大部分佔有率,這得益於政府激勵措施和國內智慧型手機出口的成長。印尼透過發放98張矽砂開採許可證和提供稅收優惠政策,吸引了外國投資者,旨在實現基板生產的在地化。

預計到2030年,北美市場佔有率將有所成長。 《晶片技術創新法案》(CHIPS Act)的津貼預計將促成5,400億美元的私人晶圓廠投資,其中包括安森美德克薩斯州)在德州新建的8吋碳化矽(SiC)生產線。加拿大正透過清潔技術稅額扣抵來支持氮化鎵(GaN)外延晶圓新興企業,以建立增值流程。墨西哥的電子製造服務(EMS)叢集正在擴大對美國汽車供應鏈的免稅准入,從而促進整流器和突波保護裝置的組裝。

歐洲的目標是到2030年佔據全球20%以上的產量,但審核顯示,由於核准延誤和技術純熟勞工短缺,進度面臨風險。 Nexperia在漢堡投資2億美元將擴大歐洲碳化矽(SiC)產能,而波蘭將設立英特爾後晶圓廠測試中心,創造2,000個工作機會。中東和非洲地區仍處於低度開發狀態,但採用1200V碳化矽二極體的太陽能逆變器試點工廠已在阿拉伯聯合大公國運作。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 家用電子電器生態系的數位化

- 加速電動車(EV)生產和車載充電器的普及

- 5G部署推動射頻和微波二極體的需求

- 資料中心效率要求推動了對功率二極體的需求

- 監理政策利好氮化鎵矽基高壓二極體

- 由於電子廢棄物回收法加強,匯率上漲

- 市場限制

- 原料價格波動(矽、砷化鎵、氮化鎵)

- 高電流封裝中的熱限制

- 寬能能隙半導體製程的專利堵塞

- 區域生產能力不平衡(由於本地化政策)

- 供應鏈分析

- 監管環境

- 技術展望

- 宏觀經濟因素如何影響市場

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 肖特基二極體

- 齊納二極體

- 整流二極體

- 雷射二極體

- 小訊號二極體

- 靜電放電保護二極體

- 瞬態電壓抑制二極體

- 射頻和微波二極體

- 按最終用戶行業分類

- 溝通

- 家用電子電器

- 車

- 國防/航太

- 電腦及周邊設備

- 產業

- 照明

- 其他終端用戶產業

- 透過安裝方式 - 封裝

- 通孔

- 表面黏著技術(SMD)

- 晶片級封裝

- 覆晶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Central Semiconductor Corp.

- Diodes Incorporated

- MinebeaMitsumi Power Semiconductor Device Inc.

- Infineon Technologies AG

- Littelfuse Inc.

- MACOM Technology Solutions Holdings Inc.

- Nexperia BV

- onsemi

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Micross Components Inc.

- Vishay Intertechnology Inc.

- Toshiba Electronic Devices and Storage Corp.

- Mitsubishi Electric Corp.

- Microchip Technology Inc.

- Semikron Danfoss

- Shindengen Electric Manufacturing Co. Ltd.

- STMicroelectronics NV

- Panasonic Holdings Corp.

- Texas Instruments Inc.

- Kyocera AVX Components Corp.

- Skyworks Solutions Inc.

- Cree-Wolfspeed Inc.

- Alpha and Omega Semiconductor Ltd.

- GlobalFoundries Inc.

第7章 市場機會與未來展望

The diode market is expected to grow from USD 18.16 billion in 2025 to USD 19.24 billion in 2026 and is forecast to reach USD 25.67 billion by 2031 at 5.95% CAGR over 2026-2031.

Consumer electronics remains the largest end-user at 23.2% diode market share, while automotive applications show the strongest 6.8% CAGR as electric-vehicle programs accelerate worldwide. Asia-Pacific holds 58.86% of global revenue and grows at a 6.63% pace thanks to dense manufacturing clusters in China, Japan, and South Korea. Surface-mount packaging captures 61.2% of shipments, yet chip-scale packages rise at a 7.1% CAGR because handset and IoT producers need ever-smaller footprints.

Global Diode Market Trends and Insights

Digitization of Consumer Electronics Ecosystems

Smartphones, wearables, and connected-home devices embed higher semiconductor content per system, lifting discrete component volumes for signal conditioning, battery protection, and data-line safeguarding. Small-signal and electrostatic-discharge arrays such as the ESDS31x series from Texas Instruments deliver +-30 kV protection at up to 5 Gbps data rates, supporting USB, HDMI, and Ethernet interfaces.Asia-Pacific manufacturers assemble about 60% of global electronics hardware, feeding clustered demand for diode arrays that secure high-speed interconnects.

Acceleration of EV Production and On-Board Chargers

Automotive semiconductor demand is increasing as electric-powertrain penetration climbs. Silicon-carbide and gallium-nitride diodes deliver lower switching losses for traction inverters and 800 V chargers; onsemi's EliteSiC platform has been adopted by Volkswagen for next-generation EVs.Infineon's CoolSiC 1200 V MOSFETs allow DC-DC stages to operate beyond 900 V without extra insulation, raising power density while trimming system cost.

Raw-Material Price Volatility (Si, GaAs, GaN)

China provides most primary gallium feedstock, and any export curbs rapidly elevate wafer costs for GaAs and GaN devices. Only 20% of global e-waste is properly recycled, causing critical-metal losses that tighten supply and raise pricing swings. SiC wafer yields remain volatile, contingent on manufacturing maturity and substrate quality.

Other drivers and restraints analyzed in the detailed report include:

- 5G Rollout Boosting RF and Microwave Diodes

- Data-Center Efficiency Mandates Raising Power-Diode Demand

- Thermal Limitations in High-Current Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser diodes generated the largest diode market size at USD 6.48 billion in 2025 and are positioned for an 8.25% CAGR, propelled by automotive front-lighting, LiDAR sensing, and high-speed fiber communications. Rectifier and Schottky devices continue to secure power-conversion sockets, though their mid-single-digit growth trails laser adoption.

Industrial cutting, projectors, and 3D printing sustain multimode laser-diode volumes, while medical-grade lasers require tighter wavelength stability that lifts average selling prices. In server power supplies, Infineon's GaN transistors integrate a Schottky diode that curbs dead-time losses and elevates efficiency, showcasing cross-category partnerships.

The Diode Market Report is Segmented by Product Type (Schottky Diodes, Zener Diodes, and More), End-User Industry (Communications, Consumer Electronics, Automotive, Defense and Aerospace, Computer and Peripherals, and More), Mounting-Package (Through-Hole, Surface-Mount, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 58.30% of global revenue in 2025, and continues at a 6.45% CAGR through 2031 on the back of integrated supply chains in China, Japan, and South Korea. China absorbed a significant share of world chip sales in 2023, buoyed by government incentives and domestic smartphone exports. Indonesia courts foreign investors with 98 silica-sand mining licenses and tax holidays, aiming to localize substrate production.

North America's share is set to rise by 2030 as the CHIPS Act grants unlock USD 540 billion of private fab commitments, including onsemi's new 8-inch SiC line in Texas. Canada supports GaN epi-wafer startups through Clean-Tech credits, seeking to anchor value-add processes. Mexico's EMS clusters extend tariff-free access to the U.S. vehicle supply chain, stimulating rectifier and transient-voltage-suppressor assembly.

Europe targets more than 20% global production share by 2030, though audit findings warn of schedule risk given permitting delays and skilled-labor gaps. Nexperia's USD 200 million Hamburg investment broadens European SiC capacity, while Poland secures Intel's post-fab testing center that creates 2,000 roles. The Middle East and Africa remain nascent but see pilot solar-inverter fabs in the UAE that specify 1200 V SiC diodes.

- Central Semiconductor Corp.

- Diodes Incorporated

- MinebeaMitsumi Power Semiconductor Device Inc.

- Infineon Technologies AG

- Littelfuse Inc.

- MACOM Technology Solutions Holdings Inc.

- Nexperia BV

- onsemi

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Micross Components Inc.

- Vishay Intertechnology Inc.

- Toshiba Electronic Devices and Storage Corp.

- Mitsubishi Electric Corp.

- Microchip Technology Inc.

- Semikron Danfoss

- Shindengen Electric Manufacturing Co. Ltd.

- STMicroelectronics NV

- Panasonic Holdings Corp.

- Texas Instruments Inc.

- Kyocera AVX Components Corp.

- Skyworks Solutions Inc.

- Cree - Wolfspeed Inc.

- Alpha and Omega Semiconductor Ltd.

- GlobalFoundries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digitization of consumer electronics ecosystems

- 4.2.2 Acceleration of EV production and on-board chargers

- 4.2.3 5G rollout driving demand for RF and microwave diodes

- 4.2.4 Data-center efficiency mandates boosting power diodes

- 4.2.5 Regulatory tailwinds for GaN-on-Si high-voltage diodes

- 4.2.6 E-waste recycling laws increasing replacement rates

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility (Si, GaAs, GaN)

- 4.3.2 Thermal limitations in high-current packages

- 4.3.3 Patent congestion in WBG semiconductor processes

- 4.3.4 Regional capacity imbalance from localization policies

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Schottky Diodes

- 5.1.2 Zener Diodes

- 5.1.3 Rectifier Diodes

- 5.1.4 Laser Diodes

- 5.1.5 Small-Signal Diodes

- 5.1.6 Electrostatic Discharge Protection Diodes

- 5.1.7 Transient Voltage Suppressor Diodes

- 5.1.8 RF and Microwave Diodes

- 5.2 By End-User Industry

- 5.2.1 Communications

- 5.2.2 Consumer Electronics

- 5.2.3 Automotive

- 5.2.4 Defense and Aerospace

- 5.2.5 Computer and Peripherals

- 5.2.6 Industrial

- 5.2.7 Lighting

- 5.2.8 Other End-User Industries

- 5.3 By Mounting - Package

- 5.3.1 Through-Hole

- 5.3.2 Surface-Mount (SMD)

- 5.3.3 Chip-Scale Package

- 5.3.4 Flip-Chip

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank - Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Central Semiconductor Corp.

- 6.4.2 Diodes Incorporated

- 6.4.3 MinebeaMitsumi Power Semiconductor Device Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Littelfuse Inc.

- 6.4.6 MACOM Technology Solutions Holdings Inc.

- 6.4.7 Nexperia BV

- 6.4.8 onsemi

- 6.4.9 Renesas Electronics Corp.

- 6.4.10 ROHM Co. Ltd.

- 6.4.11 Micross Components Inc.

- 6.4.12 Vishay Intertechnology Inc.

- 6.4.13 Toshiba Electronic Devices and Storage Corp.

- 6.4.14 Mitsubishi Electric Corp.

- 6.4.15 Microchip Technology Inc.

- 6.4.16 Semikron Danfoss

- 6.4.17 Shindengen Electric Manufacturing Co. Ltd.

- 6.4.18 STMicroelectronics NV

- 6.4.19 Panasonic Holdings Corp.

- 6.4.20 Texas Instruments Inc.

- 6.4.21 Kyocera AVX Components Corp.

- 6.4.22 Skyworks Solutions Inc.

- 6.4.23 Cree - Wolfspeed Inc.

- 6.4.24 Alpha and Omega Semiconductor Ltd.

- 6.4.25 GlobalFoundries Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年可見光通訊(VLC)室內導航顯示器全球市場報告

2026年可見光通訊(VLC)室內導航顯示器全球市場報告 LED智慧燈帶市場按類型、類別、顏色、長度、連接方式、分銷管道、應用和最終用途分類,全球預測,2026-2032年LED直升機場泛光燈市場按應用程式、安裝類型、最終用戶產業、功耗範圍和分銷管道分類,全球預測,2026-2032年

LED智慧燈帶市場按類型、類別、顏色、長度、連接方式、分銷管道、應用和最終用途分類,全球預測,2026-2032年LED直升機場泛光燈市場按應用程式、安裝類型、最終用戶產業、功耗範圍和分銷管道分類,全球預測,2026-2032年 LED磷光體市場分析及預測(至2035年):依類型、產品、應用、技術、最終用戶、組件、材料類型、功能、安裝類型及解決方案分類線性LED燈帶照明燈具市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、安裝方式、最終用戶、功能及解決方案分類2026年全球發光二極體(LED)市場報告全球背光LED市場報告(2026年)7段LED市場依技術、安裝方式、類型、應用及通路分類,全球預測(2026-2032年)AH-IPS發光二極體顯示器市場:按產品類型、螢幕大小、解析度、應用和最終用戶分類的全球預測(2026-2032年)LED SEG框架市場按產品類型、安裝類型、最終用戶和分銷管道分類,全球預測,2026-2032年

LED磷光體市場分析及預測(至2035年):依類型、產品、應用、技術、最終用戶、組件、材料類型、功能、安裝類型及解決方案分類線性LED燈帶照明燈具市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、安裝方式、最終用戶、功能及解決方案分類2026年全球發光二極體(LED)市場報告全球背光LED市場報告(2026年)7段LED市場依技術、安裝方式、類型、應用及通路分類,全球預測(2026-2032年)AH-IPS發光二極體顯示器市場:按產品類型、螢幕大小、解析度、應用和最終用戶分類的全球預測(2026-2032年)LED SEG框架市場按產品類型、安裝類型、最終用戶和分銷管道分類,全球預測,2026-2032年