|

市場調查報告書

商品編碼

1632021

全球 PE 薄膜 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Global PE Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

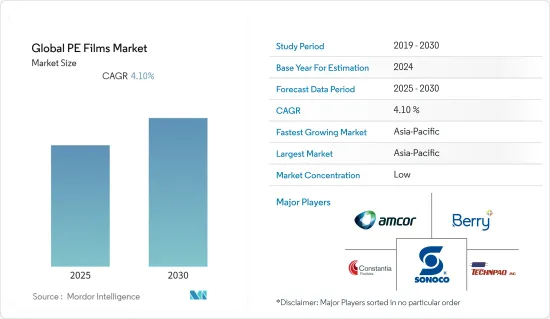

預計全球PE薄膜市場在預測期內複合年成長率為4.1%

主要亮點

- 聚乙烯(PE)薄膜是一種主要成分為碳氫化合物的塑膠薄膜。該薄膜通常用作包裝、混凝土砂漿、害蟲防治和防水等應用中的保護屏障。這些薄膜廣泛用於許多家庭和商業應用,因為它們可重複使用,並且可以承受多年的紫外線劣化。

- 軟包裝產業的成長是研究市場成長的主要動力。例如,截至 2021 年 8 月,軟包裝是美國第二大包裝領域,佔美國1,770 億美元包裝市場的約 19%。 (來源軟包裝協會(FPA))

- 食品和飲料是PE薄膜廣泛使用的另一個主要產業。例如,在食品和飲料行業,聚乙烯薄膜具有低熔點,可用於多種應用,包括店內產品的包裝,例如非冷凍烘焙食品、水果和蔬菜,以及食品和飲料的托盤蓋。

- 包裝食品消費的增加支持了所研究市場的成長。例如,根據美國人口普查局初步估計,2022年4月美國零售和食品服務銷售額為6,777億美元,較上季成長0.9%,比2021年4月成長8.2%。

- 然而,隨著消費者和品牌轉向永續性和環境考慮,對紙張和可回收塑膠薄膜等永續包裝解決方案的需求預計將成長,可能會對成長產生負面影響。

- COVID-19 的影響是巨大的,由於各國政府為遏制病毒傳播而實施的各種法規,聚乙烯薄膜的主要最終用戶(例如包裝、食品和飲料、汽車和建築)受到了不利影響。然而,隨著世界大部分地區取消限制,預計市場將在預測期內再次恢復動力。

PE薄膜市場趨勢

食品飲料產業佔較大市場佔有率

- 基於聚乙烯的軟性薄膜擴大被食品和飲料製造商採用,因為它們具有獨特的阻隔性能,有助於延長保存期限並在儲存和運輸過程中提供保護。此外,食品級塑膠必須遵循政府監控的嚴格製造程序,以確保其可安全用於食品接觸。

- 因此,廠商越來越注重開發滿足上述要求的解決方案。例如,2021年7月,Nova Chemicals推出了高密度聚苯乙烯(HDPE)。該樹脂可透過提高多層軟包裝的防潮阻隔性來開發更可回收的聚乙烯 (PE)。據該公司介紹,新樹脂將多層共擠薄膜的水蒸氣透過性能提高了20%,從而延長了包裝食品的保存期限。

- 食品和飲料的零售對PE薄膜的需求有重大影響。例如,根據美國人口普查局的數據,美國食品和飲料零售額從 2021 年 11 月的 775.21 億美元增加到 12 月的 846.29 億美元。

- 不斷成長的需求也鼓勵供應商推出新產品,以滿足食品和飲料市場不斷變化的需求。例如,2022年5月,Walki集團推出了幾款新產品,包括Lamibel MDO-PE,這是一種用於枕袋的無溶劑薄膜基材,由低密封LDPE和反向印刷MDO薄膜層壓而成。

亞太地區成長顯著

- 包裝、食品和飲料以及建築等領域的快速成長正在推動該地區對 PE 薄膜的需求。該地區城市市場的包裝食品和加工食品的消費量也大幅增加。例如,根據 IBEF 的數據,食品加工產業佔印度食品工業總量的 32%,預計 2025-26 年將達到 5,350 億美元。

- 亞太地區其他國家的食品加工業也出現了類似的趨勢。例如,根據美國農業部的數據,2021年日本食品加工產業的總產值達到2,164億美元。

- PE 薄膜在建築業中也發揮著重要作用,因為它們用於覆蓋特定空間並保護有價值的設備和機械。由於多個地區政府注重升級公共基礎設施,亞太地區的建設活動大幅增加。

- 例如,根據越南統計總局的數據,2021年建築業對越南GDP的貢獻率為5.95%,2020年為6.19%。

PE薄膜產業概況

由於存在多個區域和國際參與企業,全球 PE 薄膜市場競爭非常激烈。市場上的供應商專注於新產品開發並在區域和全球擴大業務。市場上營運的主要企業包括 AmcorFlexibles、BerryGlobalInc、ConstantiaFlexibles 和 SonocoProductsCompany。

- 2022 年 4 月 - 埃克森美孚宣布 Exceed S 高性能聚乙烯 (PE) 樹脂商業化。據該公司稱,它在加工過程中需要的配方更少,可以提供更簡單、更輕的薄膜配方,並且在食品、農業和工業應用中具有相同的耐用性。

- 2021 年 11 月 - 法國領先包裝公司 Reborn Group 宣佈在其位於 Aujou-les-Bains 的工廠推出法國第一條聚乙烯 (PE) 薄膜脫墨生產線。憑藉這條新的脫墨生產線,該公司將解決塑膠薄膜回收過程中印刷油墨的挑戰。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估 COVID-19 對調查市場的影響

第5章市場動態

- 市場促進因素

- 朝著更輕的重量和更小的尺寸發展

- 主要在食品和飲料領域以及 mPE 等技術創新領域擴大最終用戶群

- 市場問題

- 來自 BOPP 薄膜等替代品的激烈競爭

- 向永續替代品過渡

- 市場機會

第6章 市場細分

- 按類型

- LDPE

- 高密度聚苯乙烯

- LLDPE

- 其他

- 按用途

- 包裝膜

- 袋/麻袋

- 用於建築

- 農業

- 醫療保健

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 其他地區(拉丁美洲和中東非洲)

第7章 競爭格局

- 公司簡介

- Amcor Flexibles

- Berry Global Inc

- Constantia Flexibles LLC

- INDEVCO Plastics

- Sonoco Products Company

- Technipaq, Inc.

- Emerald Packaging Inc.

- PPC Flexible Packaging

- ZacrosAmerica Inc.

- ProAmpac Intermediate, Inc.

- American Packaging Corporation

- Polymer Packaging Inc.

第8章投資分析

第9章 市場的未來

The Global PE Films Market is expected to register a CAGR of 4.1% during the forecast period.

Key Highlights

- Polyethylene (PE) film is essentially a plastic film made primarily of hydrocarbons. The films are commonly used as a protective barrier in applications such as packaging, concrete & mortar, exterminating, and even pest control and waterproofing. As these films can be reused and can stand up to UV degradation for several years, they are extensively used for a number of household and commercial applications.

- The growth of the flexible packaging industry is significantly driving the growth of the studied market. For instance, as of August 2021, flexible packaging was the second largest packaging segment in the U.S., garnering about 19% of the USD 177 billion U.S. packaging market. (Source: Flexible Packaging Association (FPA))

- Food and beverage is another major industry wherein PE films are used extensively. For instance, in food & beverage industry, Polyethylene films are used for various applications such as packaging in-store products such as non-frozen baked products, fruits & vegetables, and tray covers for delivery of baked food products due to their low melting point.

- The increasing consumption of packaged food is supporting the growth of the studied market. For instance, according to the U.S. Census Bureau's advance estimates, U.S. retail and food services sales for April 2022 were USD 677.7 billion, an increase of 0.9 percent from the previous month and 8.2 percent above April 2021.

- However, with consumers and brands shifting more towards sustainability and environmental friendliness, the demand for sustainable packaging solutions such as paper and recyclable plastic films is expected to grow, which in turn will negatively impact the growth of the studied market.

- A significant impact of COVID-19 has been observed on the studied market, as the major end-users of polyethylene films such as packaging, food & beverages, automotive, and construction were negatively impacted due to various restrictions imposed by the governments to curb the spread of the virus. However, with the restrictions being lifted almost across every part of the world, the market is expected to regain traction during the forecast period.

PE Films Market Trends

Food & Beverage Industry to Hold Significant Market Share

- Food and beverage product manufacturers are increasingly adopting polyethylene-based flexible films because they offer distinct barrier properties that help with longer shelf life and better protection during the storage and transportation phase. Additionally, food-grade plastics must follow stringent, government-monitored manufacturing processes to ensure they are safe for food contact.

- Hence, the vendors are increasingly focusing on developing solutions to fulfill the above requirements. For instance, in July 2021, a high-density polyethylene (HDPE) was introduced by Nova Chemicals. The resin enables the development of more recyclable polyethylene (PE) by offering an improved moisture barrier for multilayer flexible packaging. According to the company, the new resin delivers up to a 20% increase in water-vapor transmission performance in multilayer coextruded films, which increases the shelf life of packaged foods.

- The retail sales of food and beverage products have significantly impacted the demand for PE films. For instance, according to the US Census Bureau, the retail sales of food and beverage stores in the United States increased from USD 77,521 million in November 2021 to USD 84,629 million in December 2021.

- The growing demand also encourages the vendors to launch new products to serve the changing need of the food & beverage market. For instance, in May 2022, Walki Group launched several new products, including Lamibel MDO-PE, a film-based material for pillow pouches made of solvent-free laminated with low sealing LDPE and reverse printed MDO-film.

Asia Pacific to Register Significant Growth

- The rapid growth of sectors such as packaging, food & beverage, and construction is driving the demand for PE films in the region. The consumption of packaged and processed food has also increased significantly in the urban markets of the area. For instance, the food processing sector accounts for 32% of the entire food industry in India and is expected to reach USD 535 billion by 2025-26, according to IBEF.

- A similar trend has been observed in the food processing industry of other countries in the APAC region. For instance, according to the United States Department of Agriculture, the total production value of the Japanese food-processing sector amounted to USD 216.4 billion in 2021.

- PE films also play an essential role in the construction industry as they are used to cover specific spaces and protect valuable equipment and machinery. As the Asia Pacific region is witnessing a significant rise in construction activities with several regional governments focusing on upgrading their public infrastructure, the sector is expected to drive the growth of the studied market.

- For instance, according to the General Statistics Office of Vietnam, the construction sector's contribution to Vietnam's GDP amounted to 5.95 percent and 6.19 percent for 2021 and 2020, respectively.

PE Films Industry Overview

The Global PE Films Market is competitive, owing to the presence of several players operating their businesses within regional and international boundaries. Vendors operating in the market are broadly focusing on new product development and on expanding their footprint both on a local as well as a global scale. Some of the major players operating in the market include Amcor Flexibles, Berry Global Inc, Constantia Flexibles, and Sonoco Products Company.

- April 2022 - ExxonMobil announced the commercialization of its Exceed S performance polyethylene (PE) resins, which according to the company, requires less blending during processing and can offer simpler and lighter film formulations with the same durability for food, agricultural, and industrial applications.

- November 2021 - Reborn group, one of the leading packaging firm in France, announced that it is set to launch France's first film de-inking line for polyethylene (PE) films at its site in Ogeu-les-Bains. With its new de-inking line, the company will seek to address the challenge of printing inks in the plastic film recycling process.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Studied Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Move Towards Light Weighting & Downgauging

- 5.1.2 Growing End-User Base Specifically in the Food & Beverage Segment, and Innovations Such as mPE

- 5.2 Market Challenges

- 5.2.1 High Competition from Alternatives Such as BOPP Film

- 5.2.2 Move Towards Sustainable Alternatives

- 5.3 Market Opportunities

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 LDPE

- 6.1.2 HDPE

- 6.1.3 LLDPE

- 6.1.4 Other Types

- 6.2 By Application

- 6.2.1 Packaging Films

- 6.2.2 Bags & Sacks

- 6.2.3 Construction

- 6.2.4 Agriculture

- 6.2.5 Healthcare

- 6.2.6 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World (Latin America and Middle East & Africa)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Flexibles

- 7.1.2 Berry Global Inc

- 7.1.3 Constantia Flexibles LLC

- 7.1.4 INDEVCO Plastics

- 7.1.5 Sonoco Products Company

- 7.1.6 Technipaq, Inc.

- 7.1.7 Emerald Packaging Inc.

- 7.1.8 PPC Flexible Packaging

- 7.1.9 ZacrosAmerica Inc.

- 7.1.10 ProAmpac Intermediate, Inc.

- 7.1.11 American Packaging Corporation

- 7.1.12 Polymer Packaging Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025 年至 2033 年機器方向取向薄膜市場(依材料類型、製造流程、應用、最終用途產業及地區分類)

2025 年至 2033 年機器方向取向薄膜市場(依材料類型、製造流程、應用、最終用途產業及地區分類) 聚乙烯層壓膜全球市場報告 2025

聚乙烯層壓膜全球市場報告 2025 全球板下聚乙烯蒸氣膜市場:市場規模、佔有率、趨勢分析(按厚度、產品、應用、最終用途、等級和地區)、細分市場預測(2025-2030 年)

全球板下聚乙烯蒸氣膜市場:市場規模、佔有率、趨勢分析(按厚度、產品、應用、最終用途、等級和地區)、細分市場預測(2025-2030 年) 聚乙烯薄膜市場規模、佔有率、成長分析,按技術、按類型、按材料、按厚度、按應用、按最終用途、按地區 - 行業預測,2025-2032 年美國聚對苯二甲酸乙二醇酯薄膜市場規模、佔有率、趨勢分析報告:按類型、應用和細分市場預測,2025-2030 年

聚乙烯薄膜市場規模、佔有率、成長分析,按技術、按類型、按材料、按厚度、按應用、按最終用途、按地區 - 行業預測,2025-2032 年美國聚對苯二甲酸乙二醇酯薄膜市場規模、佔有率、趨勢分析報告:按類型、應用和細分市場預測,2025-2030 年 全球MDO薄膜市場(至2034年):依薄膜類型、應用、最終用戶產業、厚度、透明度和地區

全球MDO薄膜市場(至2034年):依薄膜類型、應用、最終用戶產業、厚度、透明度和地區 MDO-PE 薄膜市場,全球 2025-2029機器方向薄膜市場:按材料、透明度、製造流程、應用和最終用戶分類 - 全球預測 2025-2030按材料、厚度和最終用途分類的層壓薄膜市場 - 全球產業分析、規模、佔有率、成長、趨勢和預測,2024-2032 年聚對苯二甲酸乙二醇酯薄膜的全球市場:市場規模、佔有率和趨勢分析 - 按類型、最終用途、地區、細分市場預測,2024-2030 年

MDO-PE 薄膜市場,全球 2025-2029機器方向薄膜市場:按材料、透明度、製造流程、應用和最終用戶分類 - 全球預測 2025-2030按材料、厚度和最終用途分類的層壓薄膜市場 - 全球產業分析、規模、佔有率、成長、趨勢和預測,2024-2032 年聚對苯二甲酸乙二醇酯薄膜的全球市場:市場規模、佔有率和趨勢分析 - 按類型、最終用途、地區、細分市場預測,2024-2030 年