|

市場調查報告書

商品編碼

1636158

亞太地區先進建築材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)APAC Advanced Building Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

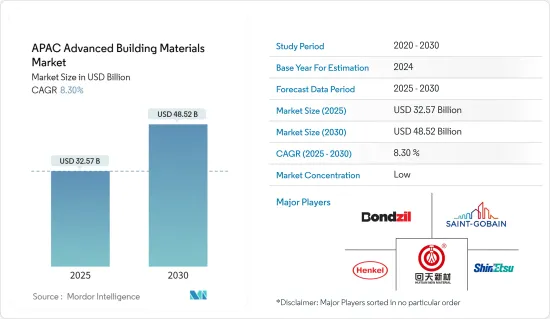

預計2025年亞太地區先進建材市場規模為325.7億美元,預估至2030年將達485.2億美元,預測期間(2025-2030年)複合年成長率為8.3%。

主要亮點

- 疫情影響了建築材料製造並擾亂了供應鏈。此外,疫情導致建設計劃延誤,進一步影響先進建材業。隨著限制的放鬆,市場隨後恢復至疫情前的水平。

- 建築和基礎設施產業的成長是先進建材產業的主要驅動力。這些材料被用於建築計劃,以實現結構強度、能源效率、脫碳目標等。此外,許多開發商有興趣將綠色建築材料納入其開發計劃,以實現國家淨零目標。

- 同時,2023年4月,印度房地產開發商聯合會(Credai)與印度綠色建築委員會(IGBC)合作,決定在未來兩年內在印度各地交付1000多個綠色認證計劃,並決定在2030年交付4000個。

- 此外,對縮短施工時間和提供具有成本效益的產品的日益成長的需求正在推動對先進建築材料的需求。此外,預拌混凝土和預製產品的使用可以節省建設產業的時間。

- 例如,2022年7月,AboitizLand與三井住友建設和SMCC菲律賓公司合作,引進日本預製混凝土技術,創新住宅計劃。因此,建設計劃的增加和基礎設施領域投資的增加預計將推動該地區先進建材行業的需求。

亞太地區先進建材市場趨勢

基礎建設拉動市場需求

- 亞太地區目前基礎設施開發計劃正在顯著成長,這主要是由於投資的增加。投資的激增反過來又增強了這些計劃對先進建築材料的需求。例如,2022年5月,美國、印度、澳洲宣布計畫投資超過500億美元用於亞太地區基礎建設計劃。

- 此外,印度、中國和日本等新興經濟體正在進行大量基礎建設計劃,以進一步提振各自的經濟。 2023年4月,印度政府公佈了價值超過7.4億美元的基礎設施計劃計畫。此外,政府計劃透過國家基礎設施管道撥款超過1.3兆美元用於印度的基礎設施開發計劃。

- 同時,2023年5月,日本承諾向印度提供超過8.6億美元的資金,用於巴特那地鐵建設計劃和拉賈斯坦邦水務部門民生改善計劃等三個基礎建設計劃。此外,2022年中國公共支出與前一年同期比較大幅增加5%以上。因此,全部區域基礎設施開發計劃投資的增加正在創造對先進建築材料的巨大需求。

中國建築業推動市場成長

- 儘管面臨疫情危機,但由於「十四五」規劃(2021-2025)中對基礎設施的大量投資,中國建設產業仍在經歷顯著成長。該計劃由五個類別的 20 個量化目標組成。 2023年,我國政府已撥款超過1.1兆美元用於全國各類基礎建設計劃,進一步推動國內先進建材製造廠的發展。

- 此外,到2022年,中國政府累計超過140億美元用於綠建築計劃,旨在遏制建築相關污染。為了實現淨零碳排放的目標,政府已撥款超過7.8億美元用於減少建築相關污染。

- 此外,為了保護文化遺產,全國各地正在建造許多博物館。例如,北京市文物局計劃到2023年2月在全市建造超過460家博物館,目前已登記的博物館超過215家。由於持續的投資和計劃擴張,該國建築產量年增與前一年同期比較6%,導致對先進建材製造商的需求增加。

亞太地區先進建材產業概況

本報告重點介紹了亞太地區先進建築材料市場的主要企業。該市場競爭激烈且分散,沒有一家公司佔據較大佔有率。為了保持競爭力,主要企業不斷努力加強其產品供應,擴大其地理分佈,並持續進行併購。該市場的主要企業包括匯天、Bondzil、聖戈班集團、漢高巴爾蒂OU和工業。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

- 分析方法

- 調查階段

第3章執行摘要

第4章市場洞察

- 目前的市場狀況

- 洞察技術趨勢

- 產業價值鏈/供應鏈分析

- 與市場相關的政府法規和關鍵舉措

- 市場動態

- 促進因素

- 增加政府基礎建設支出

- 需要縮短工期和具成本效益的產品

- 抑制因素

- 初期投資高

- 機會

- 促進因素

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 對市場的影響

第5章市場區隔

- 按用途

- 建築施工

- 基礎設施

- 按類型

- 綠色材料

- 尖端技術

- 按材質

- 高級水泥/混凝土

- 複合板

- 結構保溫板

- 密封材料

- 其他材料

- 按國家/地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太地區

第6章 競爭狀況

- 市場集中度概況

- 公司簡介

- China National Building Material Group Corporatio

- Henkel Balti OU

- China Lesso

- Huitian

- Zamil Steel Buildings India Private Limited

- Kingspan Jindal

- Bondzil

- Ultratech Cement Limited

- Arto Precast Concrete

- Saint-Gobain Group

- BASF SE

- DuPont

- Sika AG

- Shin-Etsu Chemical Co., Ltd*

第7章 市場機會及未來趨勢

第8章附錄

The APAC Advanced Building Materials Market size is estimated at USD 32.57 billion in 2025, and is expected to reach USD 48.52 billion by 2030, at a CAGR of 8.3% during the forecast period (2025-2030).

Key Highlights

- The pandemic had impacted building materials manufacturing and disrupted the supply chain, further preventing the market from expanding due to restrictions, border closures, etc. Additionally, the pandemic caused delays in construction projects, further affecting the advanced building materials industry. Later, after easing restrictions, the market recovered when compared to pre-pandemic levels.

- The growing building construction and infrastructure sectors are the major drivers of the advanced building materials industry. These materials are employed in construction projects to achieve structural strength, energy efficiency, decarbonization goals, etc. In addition, to meet net-zero goals set by the country, most of the developers are interested in adopting green building materials in development projects.

- Meanwhile, in April 2023, the Confederation of Real Estate Developers Association of India (Credai) partnered with the Indian Green Building Council (IGBC) to build over 1,000 certified green projects across India in the next two years, and 4,000 projects by 2030, these projects, in turn, bolsters the utilization of advanced building materials.

- Furthermore, the increasing need for construction time reduction and utilization of cost-effective products is driving the demand for advanced construction materials. In addition, the utilization of ready-mix concrete and precast products saves time in the building construction industry.

- For instance, in July 2022, AboitizLand partnered with Sumitomo Mitsui Construction Co. Ltd., SMCC Philippines Inc., to innovate its residential projects with the introduction of Japanese precast concrete technology. Thus, the growing construction projects and increasing investments in the infrastructure sector are expected to drive the demand for the advanced building materials industry in the region.

APAC Advanced Building Materials Market Trends

Infrastructure developments driving the market demand

- The Asia-Pacific region is currently experiencing significant growth in infrastructure development projects, primarily driven by increased investments. This surge in investment is, in turn, bolstering the demand for advanced building materials within these projects. For example, in May 2022, the United States, India, and Australia announced plans to invest over USD 50 billion in infrastructure projects across the Asia-Pacific region.

- Moreover, developing countries such as India, China, and Japan are undergoing numerous infrastructure projects, which are further propelling their respective economies. In April 2023, the Indian government revealed plans for infrastructure projects exceeding USD 740 million. Additionally, through the National Infrastructure Pipeline, the government aims to allocate more than USD 1,300 billion to infrastructure development projects in India.

- Meanwhile, in May 2023, Japan committed to funding India with over USD 860 million for three infrastructure projects, including the Patna Metro Rail Construction Project and the Rajasthan Water Sector Livelihood Improvement Project. Furthermore, Chinese public expenditure in 2022 witnessed a substantial growth of over 5% compared to the previous year. Consequently, these increasing investments in infrastructure development projects across the Asia Pacific region are generating a significant demand for advanced building materials.

China construction sector is driving market growth

- The Chinese construction industry is experiencing significant growth despite the pandemic crisis, fueled by substantial investments in infrastructure as outlined in the 14th Five-Year Plan (spanning from 2021 to 2025). This plan comprises 20 quantitative targets across five categories. The Chinese government has allocated over USD 1.1 trillion for diverse infrastructure projects nationwide by 2023, further boosting the development of advanced building materials manufacturing plants in the country.

- Additionally, in 2022, the Chinese government earmarked more than USD 14 billion for green construction projects aimed at curbing pollution associated with buildings. To achieve net-zero carbon emission goals, the government allocated over USD 780 million specifically to mitigate building-related pollution.

- Furthermore, efforts to preserve cultural heritage involve the construction of numerous museums nationwide. For example, the Beijing Municipal Cultural Heritage Bureau planned to build over 460 museums in the city by February 2023, with more than 215 museums already registered. These continuous investments and expanding projects have driven the country's construction output to grow by over 6% compared to the previous year, thereby generating increased demand for manufacturers of advanced construction materials.

APAC Advanced Building Materials Industry Overview

The report covers prominent players operating in the Asia-Pacific advanced building material market. The market is highly competitive and fragmented, with no players occupying a significant share. To remain competitive, the major players are constantly working to enhance their product offerings, expanding their geographical presence, and constantly being involved in mergers and acquisitions. Some of the major players in the market include Huitian, Bondzil, Saint-Gobain Group, Henkel Balti OU, Shin-Etsu Chemical Co., Ltd, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Insights on Technological Trends

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Spotlight on Government Regulations and Key Initiatives in the Market

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increase in government expenditures for infrastructural development

- 4.5.1.2 Need for reduced construction time and cost-effective products

- 4.5.2 Restraints

- 4.5.2.1 High initial investments

- 4.5.3 Opportunities

- 4.5.1 Drivers

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Building Construction

- 5.1.2 Infrastructure

- 5.2 By Type

- 5.2.1 Green Materials

- 5.2.2 Technically Advanced

- 5.3 By Material

- 5.3.1 Advanced Cement And Concrete

- 5.3.2 Cross-Laminated Timber

- 5.3.3 Structural Insulated Panel

- 5.3.4 Sealants

- 5.3.5 Other Materials

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 China National Building Material Group Corporatio

- 6.2.2 Henkel Balti OU

- 6.2.3 China Lesso

- 6.2.4 Huitian

- 6.2.5 Zamil Steel Buildings India Private Limited

- 6.2.6 Kingspan Jindal

- 6.2.7 Bondzil

- 6.2.8 Ultratech Cement Limited

- 6.2.9 Arto Precast Concrete

- 6.2.10 Saint-Gobain Group

- 6.2.11 BASF SE

- 6.2.12 DuPont

- 6.2.13 Sika AG

- 6.2.14 Shin-Etsu Chemical Co., Ltd*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

樓梯踏板市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(低流量、中等流量和高流量)、按應用(住宅、商業和工業)、按地區和競爭細分,2020-2030 年預測建築安全網市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、位置、最終用戶、地區、競爭進行細分,2020-2030 年預測

樓梯踏板市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(低流量、中等流量和高流量)、按應用(住宅、商業和工業)、按地區和競爭細分,2020-2030 年預測建築安全網市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、位置、最終用戶、地區、競爭進行細分,2020-2030 年預測 2025-2029 年全球先進建築材料市場先進建築材料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、應用、地區、競爭細分,2020-2030F

2025-2029 年全球先進建築材料市場先進建築材料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、應用、地區、競爭細分,2020-2030F 建築材料市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測

建築材料市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測 吸放濕建材市場評估:產品類型·用途·終端用戶·各地區的機會及預測 (2018-2032年)

吸放濕建材市場評估:產品類型·用途·終端用戶·各地區的機會及預測 (2018-2032年) 吸濕性建築材料市場:按類型、吸附過程、最終用戶分類 - 2025-2030 年全球預測建築和建材市場:按材料、功能、建築類型、分銷管道分類 - 全球預測 2025-2030節能建築材料市場:按材料類型、按應用分類 - 全球預測 2025-2030

吸濕性建築材料市場:按類型、吸附過程、最終用戶分類 - 2025-2030 年全球預測建築和建材市場:按材料、功能、建築類型、分銷管道分類 - 全球預測 2025-2030節能建築材料市場:按材料類型、按應用分類 - 全球預測 2025-2030 反應燒結碳化矽陶瓷梁市場報告:2030 年趨勢、預測與競爭分析

反應燒結碳化矽陶瓷梁市場報告:2030 年趨勢、預測與競爭分析