|

市場調查報告書

商品編碼

1636218

Gears of the World -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Global Gear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

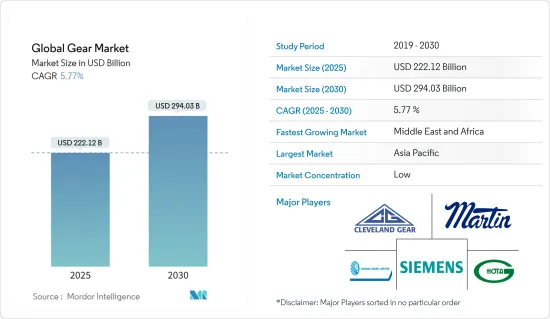

預計2025年全球齒輪市場規模為2,221.2億美元,預估至2030年將達2,940.3億美元,預測期內(2025-2030年)複合年成長率為5.77%。

主要亮點

- 從中期來看,工業自動化的興起和全球風力發電裝置的增加等因素預計將成為預測期內全球齒輪市場的最大驅動力之一。

- 預計在預測期內,齒輪的高生產成本將威脅全球齒輪市場。

- 然而,我們正在不斷努力生產客製化齒輪,以有效滿足客戶的需求。預計這一因素將在未來為市場創造一些機會。

- 預計亞太地區在預測期內將顯著成長,並實現最高的年成長率。這是由於該地區製造業的成長和對風能設施的關注。

全球齒輪市場趨勢

油田設備領域確認成長

- 油田設備領域涵蓋整個石油和天然氣價值鏈的廣泛應用,佔據全球齒輪市場的大部分。在這一領域,齒輪用於鑽孔機、泵浦和壓縮機等關鍵機械,這些機械對於石油和天然氣資源的探勘、開採、加工和運輸至關重要。

- 上游領域,即探勘和生產(E&P)領域,是油田設備領域齒輪的重要消費者。齒輪在鑽孔機、泥漿泵、絞車、井口系統等多種設備中發揮重要作用。上游市場對齒輪的需求主要受到全球石油和天然氣價格、探勘技術進步(如地震探勘和水平鑽井)以及對深海和超深海探勘的日益關注的推動。

- 近年來,由於亞太和非洲經濟擴張對原油的需求增加,原油產量呈現顯著成長。對俄羅斯的製裁也增加了石油產量,以滿足不斷成長的需求。

- 根據能源研究所《世界能源統計回顧》顯示,2022年至2023年原油產量顯著成長2%。同樣,過去10年的複合年成長率也超過1.1%,顯示原油呈現上升趨勢。這種成長推動了對設備的需求並推動了對工業齒輪的需求。

- 中游部門包括管線、卡車車隊、油輪和倉儲設施。齒輪對於該領域使用的泵浦、壓縮機和其他設備至關重要,特別是在管道運作和液化天然氣加工廠中。中游市場齒輪需求的主要促進因素包括管道基礎設施的擴張、液化天然氣(LNG)全球貿易的增加以及對更高效的運輸和儲存解決方案的需求。

- 例如,2024年6月,石油天然氣公司(ONGC)和印度石油公司(IOC)簽署了一項協議,將在中央邦哈塔天然氣田附近建立一個緊湊型液化天然氣(LNG)設施。該工廠將採用先進技術生產液化天然氣,這是一種比傳統石化燃料更環保的替代品。液化天然氣需求的成長預計將推動齒輪市場的成長,因為專用齒輪對於液化天然氣工廠的營運和維護至關重要。這一發展預計將刺激齒輪製造技術的創新和投資。

- 下游領域是油田設備市場齒輪的另一個重要終端使用者。齒輪用於精製和加工廠內的各種設備,包括泵浦、壓縮機、攪拌機和輸送機系統。推動下游領域齒輪需求的因素包括全球對精製石油產品的需求不斷增加、對更有效率、更環保的精製製程的需求以及石化產業的成長。

- 因此,鑑於上述幾點,石油和天然氣設備最終用戶產業預計在預測期內將成長。

亞太地區主導市場

- 亞太地區是全球齒輪市場的重要組成部分。隨著人口的快速成長和經濟的強勁,印度、中國、韓國和東協地區國家正在積極加強工業和製造業。這些共同努力正在為齒輪市場創造良好的市場環境。

- 汽車業是亞太地區齒輪的主要最終用戶之一,日本、韓國、中國和印度等國家是主要的汽車製造地。對齒輪的需求涉及廣泛的應用,從變速箱和差速器到轉向機構和引擎零件。

- 根據國際汽車工業協會預測,2022年至2023年亞太地區汽車產量將大幅成長。 2023年,該地區生產汽車55,115,837輛,恢復10%的成長速度。 2019年至2023年的複合年成長率超過12%,顯示該地區對齒輪的需求不斷增加。

- 同樣,該地區的工業領域正在顯著成長,隨著工業領域的擴張,對齒輪的需求也在增加。齒輪在各種應用中都至關重要,包括工具機、物料輸送設備以及建築和採礦中使用的重型機械。亞太地區,特別是中國、印度和東南亞等國家的快速工業化,正在推動對工業齒輪的巨大需求。

- 例如,23會計年度,印度製造業出口創歷史新高,達4,474.6億美元,比上年度(22會計年度)的4,220億美元成長6.03%。製造業佔印度GDP的17%,僱用了超過2,730萬人,對國家經濟至關重要。印度政府的目標是透過各種措施和措施,到2025年將製造業的市場佔有率提高到25%。

- 此外,航太和國防工業是亞太地區齒輪的另一個重要終端用戶。日本、韓國、中國和印度等國家正在擴大航太製造能力。這種擴張推動了對飛機引擎、起落架系統和各種控制機構中精密齒輪的需求。

- 因此,如上所述,亞太地區預計將在預測期內主導市場。

全球齒輪產業概況

全球齒輪市場是細分的。市場的主要參與企業包括(排名不分先後)Cleveland Gear Co、Siemens AG、Martin Sprocket & Gear Inc.、Hota Industrial Mfg. 和 Bharat Gears Ltd。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 工業自動化日益受到關注

- 增加風力發電部署

- 抑制因素

- 製造成本高

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 齒輪類型

- 正齒輪

- 螺旋齒輪

- 行星齒輪

- 齒條和小齒輪

- 蝸輪

- 錐齒輪

- 其他齒輪

- 最終用戶產業

- 油田設備

- 礦山機械

- 工業機械

- 發電廠

- 施工機械

- 其他

- 2029 年之前的市場規模和需求預測(按地區)

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 北歐的

- 俄羅斯

- 土耳其

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 澳洲

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 卡達

- 南非

- 其他中東/非洲

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 北美洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Cleveland Gear Co.

- Siemens AG

- Martin Sprocket & Gear Inc.

- Hota Industrial Mfg. Co. Ltd

- OKUBO GEAR Co. Ltd

- Bharat Gears Ltd

- Elecon Engineering Company Limited

- Precipart

- Kohara Gear Industry Co. Ltd

- Aero Gear Inc.

- 其他知名公司名單

- 市場排名/佔有率(%)分析

第7章 市場機會及未來趨勢

- 客製化服務增加

簡介目錄

Product Code: 50003481

The Global Gear Market size is estimated at USD 222.12 billion in 2025, and is expected to reach USD 294.03 billion by 2030, at a CAGR of 5.77% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising industrial automation and the growing global wind energy installation are expected to be among the most significant drivers for the global gear market during the forecast period.

- High production costs for gears are expected to threaten the global gear market during the forecast period.

- However, continued efforts are being made to manufacture customized gears to effectively meet the client's demand. This factor is expected to create several opportunities for the market in the future.

- Asia-Pacific is expected to grow significantly and register the highest annual growth rate during the forecast period. This is due to the region's growing manufacturing industry and focus on wind energy installations.

Global Gear Market Trends

The Oilfield Equipment Segment to Witness Growth

- The oilfield equipment segment represents a significant portion of the global gear market, encompassing a wide range of applications across the entire oil and gas value chain. This segment utilizes gears in critical machinery such as drilling rigs, pumps, compressors, and other equipment essential for the exploration, extraction, processing, and transportation of oil and gas resources.

- The upstream segment, or the exploration and production (E&P) segment, is a significant consumer of gears in the oilfield equipment segment. Gears play a crucial role in various equipment such as drilling rigs, mud pumps, drawworks, and wellhead systems. The demand for gears in the upstream segment is primarily driven by global oil and gas prices, technological advancements in exploration techniques (e.g., seismic imaging and horizontal drilling), and the increasing focus on deepwater and ultra-deepwater exploration.

- Crude oil production has witnessed significant growth in recent years due to the rising demand for crude oil due to expanding economies in Asia-Pacific and Africa. Additionally, due to sanctions on Russia, oil production has increased to meet the rising demand.

- According to the Energy Institute Statistical Review of World Energy, crude oil production witnessed a significant growth of 2% between 2022 and 2023. Similarly, the average annual growth rate over the past decade has been more than 1.1%, indicating an increasing growth in crude oil. This growth drives the demand for equipment, which fuels the demand for gear in the industry.

- The midstream segment includes pipelines, trucking fleets, tanker ships, and storage facilities. Gears are essential in pumps, compressors, and other equipment used in this segment, particularly in pipeline operations and LNG processing plants. The primary driving factors for gear demand in the midstream segment include the expansion of pipeline infrastructure, increasing global trade of liquefied natural gas (LNG), and the need for more efficient transportation and storage solutions.

- For instance, in June 2024, India's State-owned Oil and Natural Gas Corporation (ONGC) and Indian Oil Corporation (IOC) inked a deal to establish a compact liquefied natural gas (LNG) facility adjacent to the Hatta gas field in Madhya Pradesh. The plant, leveraging advanced technology, is poised to churn out LNG, heralded as a greener substitute to conventional fossil fuels. This increased demand for LNG will drive growth in the gears market, as specialized gears are essential for operating and maintaining LNG plants. This development is expected to stimulate innovation and investment in gear manufacturing technologies.

- The downstream segment is another critical end user of gears in the oilfield equipment market. Gears are used in various equipment within refineries and processing plants, such as pumps, compressors, mixers, and conveyor systems. The driving factors for gear demand in the downstream segment include the increasing global demand for refined petroleum products, the need for more efficient and environmentally friendly refining processes, and the growth of the petrochemical industry.

- Therefore, as per the above points, the oil and gas equipment end-user industry is expected to grow during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is a pivotal segment in the global gear market. With a burgeoning population and robustly growing economies, nations such as India, China, South Korea, and those in the ASEAN region are actively strengthening their industrial and manufacturing industries. This concerted effort creates a favorable market environment for the gears market.

- The automotive industry is one of the primary end users of gears in Asia-Pacific, with countries like Japan, South Korea, China, and India being major automotive manufacturing hubs. The segment's demand for gears spans a wide range, from transmission systems and differentials to steering mechanisms and engine components.

- According to the International Organization of Motor Vehicle Manufacturers, automobile manufacturing in Asia-Pacific significantly rose between 2022 and 2023. In 2023, the region manufactured 5,51,15,837 automobiles, resuming a 10% growth rate. The annual average growth rate between 2019 and 2023 was over 12%, signifying the rising demand for gears in the region.

- Similarly, the industrial segment is experiencing significant growth in the area, and the demand for gears is increasing with the expanding industrial segment. Gears are crucial in various applications, such as machine tools, material handling equipment, and heavy machinery used in construction and mining. The rapid industrialization across Asia-Pacific, particularly in countries like China, India, and Southeast Asia, has driven substantial demand for industrial gear.

- For instance, in the financial year 2023, India's manufacturing exports hit a record high, reaching USD 447.46 billion, marking a 6.03% growth from the previous year's (FY22) USD 422 billion. The manufacturing industry, contributing to 17% of India's GDP and employing over 27.3 million workers, is pivotal in the nation's economy. With various initiatives and policies, the Indian government aims to elevate manufacturing's market share to 25% by 2025.

- Additionally, the aerospace and defense industry represents another significant end user of gears in Asia-Pacific. Countries such as Japan, South Korea, China, and India are expanding their aerospace manufacturing capabilities. This expansion drives the demand for high-precision gears in aircraft engines, landing gear systems, and various control mechanisms.

- Therefore, as mentioned above, Asia-Pacific is expected to dominate the market during the forecast period.

Global Gear Industry Overview

The global gear market is fragmented. Some key players in this market (in no particular order) are Cleveland Gear Co., Siemens AG, Martin Sprocket & Gear Inc., Hota Industrial Mfg. Co. Ltd, and Bharat Gears Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Focus on Industrial Automation

- 4.5.1.2 Growing Wind Energy Installation

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Gear Type

- 5.1.1 Spur Gear

- 5.1.2 Helical Gear

- 5.1.3 Planetary Gear

- 5.1.4 Rack and Pinion Gear

- 5.1.5 Worm Gear

- 5.1.6 Bevel Gear

- 5.1.7 Other Gear Types

- 5.2 End-user Industry

- 5.2.1 Oilfield Equipment

- 5.2.2 Mining Equipment

- 5.2.3 Industrial Machinery

- 5.2.4 Power Plants

- 5.2.5 Construction Machinery

- 5.2.6 Other End-user Industries

- 5.3 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 NORDIC

- 5.3.2.7 Russia

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 South Korea

- 5.3.3.6 Malaysia

- 5.3.3.7 Thailand

- 5.3.3.8 Indonesia

- 5.3.3.9 Vietnam

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 Nigeria

- 5.3.4.4 Egypt

- 5.3.4.5 Qatar

- 5.3.4.6 South Africa

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Cleveland Gear Co.

- 6.3.2 Siemens AG

- 6.3.3 Martin Sprocket & Gear Inc.

- 6.3.4 Hota Industrial Mfg. Co. Ltd

- 6.3.5 OKUBO GEAR Co. Ltd

- 6.3.6 Bharat Gears Ltd

- 6.3.7 Elecon Engineering Company Limited

- 6.3.8 Precipart

- 6.3.9 Kohara Gear Industry Co. Ltd

- 6.3.10 Aero Gear Inc.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Customization Offerings

02-2729-4219

+886-2-2729-4219

2025年全球汽車正齒輪市場報告

2025年全球汽車正齒輪市場報告 齒輪製造市場按產品(蝸輪、錐齒輪等)、最終用戶(石油和天然氣工業、電力工業、汽車等)和地區分類 2025-2033 年

齒輪製造市場按產品(蝸輪、錐齒輪等)、最終用戶(石油和天然氣工業、電力工業、汽車等)和地區分類 2025-2033 年 全球錐齒輪市場,2025-2029

全球錐齒輪市場,2025-2029 全球工業大齒輪市場全球齒輪製造市場

全球工業大齒輪市場全球齒輪製造市場 全球齒輪製造市場 2024-2028

全球齒輪製造市場 2024-2028 塑膠齒輪材料市場報告:2030 年趨勢、預測與競爭分析

塑膠齒輪材料市場報告:2030 年趨勢、預測與競爭分析 亞太地區蝸輪傳動市場預測至 2030 年 - 區域分析 - 按操作類型、產品類型和材料類型

亞太地區蝸輪傳動市場預測至 2030 年 - 區域分析 - 按操作類型、產品類型和材料類型 北美蝸輪傳動市場預測至 2030 年 - 區域分析 - 按操作類型、產品類型和材料類型

北美蝸輪傳動市場預測至 2030 年 - 區域分析 - 按操作類型、產品類型和材料類型 歐洲蝸輪傳動市場預測至 2030 年 - 區域分析 - 按操作類型、產品類型和材料類型

歐洲蝸輪傳動市場預測至 2030 年 - 區域分析 - 按操作類型、產品類型和材料類型

▼