|

市場調查報告書

商品編碼

1636227

印度生質能 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)India Biomass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

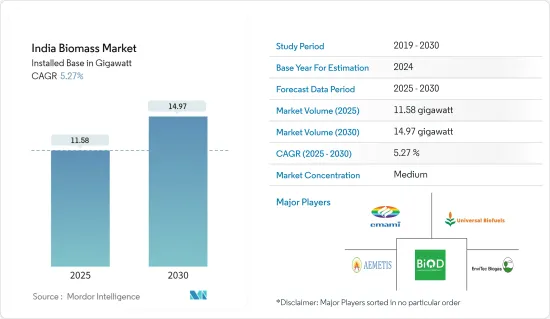

印度生質裝置市場規模預計將從2025年的11.58吉瓦成長到2030年的14.97吉瓦,預測期間(2025-2030年)複合年成長率為5.27%。

主要亮點

- 從中期來看,豐富的原料供應、政府主導的促進生質能生產的舉措以及採取嚴格措施增加可再生資源的使用以盡量減少溫室氣體排放等因素將是推動市場成長的主要因素。

- 同時,可行的替代能源的可用性預計將在預測期內抑製印度生質能市場的成長。

- 然而,印度的混燃機制、遠離燃煤發電廠以及未開發的生質能潛力預計將成為市場成長的重大機會。

印度生質能市場趨勢

發電業預計將主導市場

- 生質能發電是利用林業/農業廢棄物、垃圾、垃圾垃圾掩埋沼氣、沼氣等生質燃料發電的技術。整個過程包括將燃料的化學能轉化為蒸氣、機械能和電力形式的熱勢能。

- 生質能包括植物和動物,例如森林木材、農業和林業加工過程中的殘留物、有機工業廢棄物以及人類和動物廢物。生質能發電是可再生的,二氧化碳排放忽略不計,而且成本低於石化燃料。

- 雖然生質能發電是可再生的,但它會鼓勵森林砍伐,而且並不完全清潔。發電需要大量的空間和水。根據研究,每年約1.5億噸生質殘渣的潛在發電量約為5,000萬千瓦,相當於每年約470吉焦。

- 2023年印度生質能源產能將接近10.75吉瓦。印度也開始了雄心勃勃的能源轉型之旅,目標是到 2030 年實現 50% 的累積發電裝置容量來自非石化燃料燃料能源,並在 2070 年實現淨零發電。為了實現雄心勃勃的可再生能源目標並使國內能源產業自力更生,最佳利用現有可再生能源至關重要。

- 此外,2023 年 6 月,電力部宣布修訂生質能混燒政策,以促進永續能源實踐。該修正案將允許發電廠以標準價格購買生質能顆粒燃料,減少進口依賴並促進生質能作為可再生能源的引入。

- 鑑於上述情況,預計發電業將在預測期內主導印度生質能市場。

政府的有利支持促進市場成長

- 印度憑藉著快速發展的產業、豐富的潛力和強大的政府支持,正成為可再生能源領域的全球領導者。不斷成長的人口以及到 2030 年實現 450 吉瓦可再生能源容量(包括 10 吉瓦生質能源)的目標,為印度的投資和擴張提供了充足的機會。

- 在政府的資助下,Emami Agrotech Ltd、Universal Biofuel 和 Aemetis 等印度生質能市場的公司正在增加投資。此外,剩餘生質能的供應,尤其是來自農業的剩餘生質能,正在推動市場成長。

- 此外,到2023年,印度的沼氣能源容量約為14兆瓦。過去六年產能一直停滯不前,但預計未來幾年將會增加。

- 2024年2月,印度政府將向壓縮沼氣(CBG)生產商提供財政援助,用於採購核准物質聚合機械,以支持2023-2024會計年度至2026-2027會計年度的生質能收集。

- 自 1990 年代以來,新能源和可再生能源部 (MNRE) 一直在實施促進生質能發電和甘蔗渣熱電聯產的計畫。 2018年5月啟動的「生質能汽電共生計畫」旨在開發熱電聯產汽電共生,透過糖廠、碾米廠和造紙廠等其他產業的熱電汽電共生技術來最佳利用。在促進。

- 根據國際能源總署統計,2023年印度清潔能源投資達680億美元。 2024年初,新能源和可再生能源部(MNRE)啟動了國家生質能源計劃,第一期投資8.58億印度盧比(約1.029億美元),以促進印度生質能源發展,並通知可能持續五年。從2021年4月到2026年3月。

- 綜上所述,政府支持是印度生質能市場成長的關鍵驅動力。

印度生質產業概況

印度生質能市場較為分散。市場上營運的主要企業包括(排名不分先後)Emami Agrotech Ltd、Universal Biofuels Private Limited、BIOD ENERGY (INDIA) PVT LTD、EnviTec Biogas AG 和 Aemetis Inc。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 至2029年裝置容量及預測(單位:GW)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 政府利好支持帶動市場

- 原料供應充足

- 抑制因素

- 市面上有有效替代品

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔

- 原料

- 農業廢棄物

- 木材/木材殘渣

- 都市固態廢棄物

- 其他原料

- 目的

- 發電

- 加熱

- 其他

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Emami Agrotech Ltd

- Universal Biofuels Private Limited

- BIOD ENERGY (INDIA) PVT. LTD

- EnviTec Biogas AG

- Aemetis Inc.

- Monopoly Innovations Private Limited

- 其他知名企業名單

- 市場排名分析

第7章 市場機會及未來趨勢

- 印度的混燃機制與未開發的生質燃料潛力

簡介目錄

Product Code: 50003495

The India Biomass Market size in terms of installed base is expected to grow from 11.58 gigawatt in 2025 to 14.97 gigawatt by 2030, at a CAGR of 5.27% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as abundant availability of feedstocks, government-led initiatives to boost biomass production, and the introduction of stringent policies to increase the utilization of renewable resources to minimize GHG emissions will be major drivers in the market.

- On the other hand, the availability of viable alternatives is expected to restrain the growth of the Indian biomass market during the forecast period.

- However, the co-firing mechanism, the migration out of coal-fired power plants, and the untapped biomass potential in India are expected to become vital opportunities for the growth of the market.

India Biomass Market Trends

The Power Generation Segment is Expected to Dominate the Market

- Biomass power generation is a technique to generate power with biomass fuel, including forestry and agriculture waste, garbage, landfill gas, and biogas. The complete process involves converting the chemical energy of fuel into the thermal potential energy of steam, mechanical power, and electric power.

- Biomass includes plant and animal material, such as wood from forests, material left over from agricultural and forestry processes, and organic industrial, human, and animal wastes. The power generated from biomass is renewable, with negligible carbon dioxide emission and low cost compared to fossil fuels.

- Biomass power generation is considered renewable but can contribute to deforestation and is not entirely clean. Power production requires a significant amount of space and water. Studies estimate that the electricity generation potential from the approximately 150 million tons of biomass residues produced annually is about 50 GW, equivalent to roughly 470 GJ/per year.

- The bioenergy capacity of India was nearly 10.75 GW in 2023. Also, India has embarked upon an ambitious energy transition journey with a target of 50% cumulative electric power installed electricity capacity from non-fossil fuel-based energy resources by 2030 and achieving net zero by 2070. To achieve the ambitious targets for renewable energy and self-reliance in the domestic energy industry, optimal use of available renewable energy alternatives is a must.

- Moreover, in June 2023, the Ministry of Power announced the revision of the biomass co-firing policy to promote sustainable energy practices. This revision will enable power plants to purchase biomass pellets at benchmark prices, reducing import dependencies and enhancing the adoption of biomass as a renewable energy source.

- Owing to the above points, the power generation segment is expected to dominate the Indian biomass market during the forecast period.

Favorable Government Support to Drive the Growth of the Market

- India emerges as a global leader in renewable energy with a rapidly growing industry, abundant potential, and strong government support. A large and growing population and a target of achieving 450 GW of renewable energy capacity by 2030 (including 10 GW of bioenergy) offer ample opportunities for investments and expansion in India.

- With the help of the government's financial aid, companies in the Indian biomass market, such as Emami Agrotech Ltd, Universal Biofuel, and Aemetis, are increasing their investments. Also, surplus biomass availability, especially from the agricultural industry, drives the growth of the market.

- Moreover, the biogas energy capacity in India was approximately 14 MW in 2023. Though capacity has been stagnant for the last six years, it is expected to increase in the coming years.

- In February 2024, the Government of India approved the scheme for providing financial assistance to compressed biogas (CBG) producers for procurement of biomass aggregation machinery to support the collection of biomass with a total financial outlay of INR 564.75 crore (~USD 67.7 million) for the period from FY 2023-2024 to FY 2026-2027.

- The Ministry of New and Renewable Energy (MNRE) has been running a program to promote Biomass Power and Bagasse Cogeneration in the country since the 1990s. The Biomass-based Cogeneration Program, launched in May 2018, aims to promote cogeneration for the optimal use of the country's biomass resources through cogeneration technology in sugar mills and other industries such as rice and paper mills.

- According to the International Energy Agency, clean energy investments in India reached USD 68 billion in 2023. At the beginning of 2024, the Ministry of New and Renewable Energy (MNRE) notified the National Bioenergy Programme may continue for five years from April 2021 to March 2026 with an outlay of INR 858 crore (~USD 102.9 million) under Phase-I to boost bio-energy in India.

- Owing to the above points, favorable government support in the country will drive the growth of the Indian biomass market.

India Biomass Industry Overview

The Indian biomass market is semi-fragmented. Some of the major players operating in the market (in no particular order) include Emami Agrotech Ltd, Universal Biofuels Private Limited, BIOD ENERGY (INDIA) PVT LTD, EnviTec Biogas AG, and Aemetis Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast, in GW, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Favorable Government Support to Drive the Market

- 4.5.1.2 Abundant Availability of Feedstocks

- 4.5.2 Restraints

- 4.5.2.1 Availability of Viable Alternatives in the Market

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Feedstock

- 5.1.1 Agriculture Waste

- 5.1.2 Wood and Woody Residue

- 5.1.3 Solid Municipal Waste

- 5.1.4 Other Feedstocks

- 5.2 Application

- 5.2.1 Power Generation

- 5.2.2 Heating

- 5.2.3 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1

Emami Agrotech Ltd

- 6.3.2

Universal Biofuels Private Limited

- 6.3.3 BIOD ENERGY (INDIA) PVT. LTD

- 6.3.4 EnviTec Biogas AG

- 6.3.5 Aemetis Inc.

- 6.3.6 Monopoly Innovations Private Limited

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Co-firing Mechanism and Untapped Biofuel Potential in India

02-2729-4219

+886-2-2729-4219

生物塑膠市場按產品、形式、應用和最終用途產業分類 - 2025-2030 年全球預測

生物塑膠市場按產品、形式、應用和最終用途產業分類 - 2025-2030 年全球預測 生質能顆粒燃料市場報告:2031 年趨勢、預測與競爭分析固態生質能原料市場:按類型、來源、轉換技術、最終用途分類 - 2025-2030 年全球預測

生質能顆粒燃料市場報告:2031 年趨勢、預測與競爭分析固態生質能原料市場:按類型、來源、轉換技術、最終用途分類 - 2025-2030 年全球預測 生質能顆粒燃料市場規模、佔有率、成長分析,按原料、類型、最終用戶、地區分類 - 產業預測,2024-2031 年

生質能顆粒燃料市場規模、佔有率、成長分析,按原料、類型、最終用戶、地區分類 - 產業預測,2024-2031 年 固體生質能原料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、最終用戶、地區和競爭細分,2019-2029F

固體生質能原料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、最終用戶、地區和競爭細分,2019-2029F 固體生質能原料市場 - 全球和區域分析:按應用、按最終用戶、按來源、按類型、按地區 - 分析和預測(2024-2034)

固體生質能原料市場 - 全球和區域分析:按應用、按最終用戶、按來源、按類型、按地區 - 分析和預測(2024-2034) 全球生質能顆粒燃料市場

全球生質能顆粒燃料市場 全球固體生質能原料市場規模研究,按來源、類型、應用、最終用戶和區域預測 2022-2032全球固體生質能原料市場 2024-2031

全球固體生質能原料市場規模研究,按來源、類型、應用、最終用戶和區域預測 2022-2032全球固體生質能原料市場 2024-2031 全球固體生質能原料市場:按來源、類型、應用、最終用戶、地區 - 預測(至 2029 年)

全球固體生質能原料市場:按來源、類型、應用、最終用戶、地區 - 預測(至 2029 年)

▼