|

市場調查報告書

商品編碼

1636257

電動車電池正極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Electric Vehicle Battery Cathode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

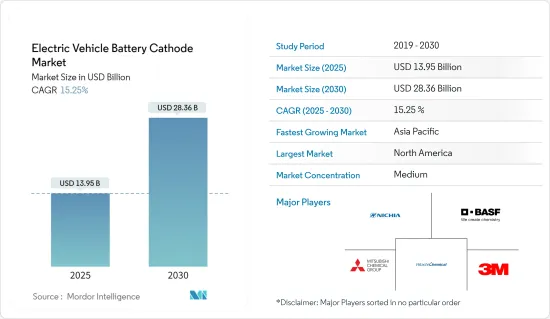

電動車電池負極市場規模預計到2025年為139.5億美元,預計到2030年將達到283.6億美元,預測期內(2025-2030年)複合年成長率為15.25%。

主要亮點

- 從中期來看,電動車滲透率的提高和鋰離子電池價格的下降預計將在預測期內推動市場發展。

- 另一方面,一些國家的壟斷造成的電池材料供應鏈的差異預計將抑制未來市場的成長。

- 然而,陰極材料和高效電解質的持續研究和進步可能會為市場成長提供機會。

- 由於正極材料在汽車產業的應用不斷增加,增加了對正極材料的需求,亞太地區佔據了市場主導地位。

電動車電池正極市場趨勢

鋰離子電池領域佔市場主導地位

- 鋰離子電池已成為電動車中最常用的電池技術。這是因為它具有能量密度高、循環壽命相對較長、效率高等優點。

- 根據國際能源總署(IEA)預測,2023年電動車電池需求量將超過750GWh,較2022年成長40%。這些電池大多數採用鋰離子技術。隨著鋰離子電池在電動車中的使用擴大,鋰離子電池技術對正極材料的需求預計也會增加。

- 根據國際能源總署(IEA)預測,到 2030 年,電動車的銷售佔有率預計將增至 35% 左右。因此,為滿足鋰離子電池的需求,歐盟預計到2030年將鋰離子電池製造能力提高至550GWh。

- 此外,鋰離子電池價格的下降預計將導致該技術在電動車中的使用,從而導致鋰離子技術中正極材料的使用需求增加。 2023年,鋰離子電池組價格年與前一年同期比較14%至139美元/kWh。

- 此外,隨著鎳和鈷以外的正極材料的研究和開發取得進展,鋰離子技術電池正極的需求預計將增加,因為這些材料很稀有並影響供應鏈的可靠性。

- 例如,2023年11月,東芝公司開發出採用無鈷5V級高電位正極材料的新型鋰離子電池。這項技術創新在抑制通常作為副反應發生的劣化性能的氣體的產生方面發揮著重要作用。

- 因此,由於鋰離子電池在電動車中的使用不斷增加以及技術的發展,鋰離子電池正極部分預計在預測期內將大幅成長。

預計北美將佔據很大的市場佔有率

- 北美電動車市場將主要由五家主要公司推動,到2023年將佔據70%以上的市場。這些領先的參與企業包括特斯拉、豐田集團、福特集團、現代和本田。特斯拉是北美國家銷量最多的電動車。隨著電動車需求的增加,這些汽車中電池的使用量也會增加,進而帶動電動車電池負極市場。

- 北美對電動車的需求持續成長。根據美國能源情報署的數據,到 2023 年,美國混合動力汽車、插電式混合動力電動車和純電動車 (BEV) 的總合銷量將升至所有輕型車 (LDV) 新車銷量的 16.3%,而前一年為12.9%。

- 此外,政府的支持措施正在影響電動車電池的需求,進而影響電動車電池正極市場的需求。北美各國政府正在採取措施和獎勵來鼓勵電動車的普及。這些努力包括扣除額、補貼、回扣以及充電基礎設施投資。這種支持增加了消費者對電動車的興趣,並推動了對電池陰極的需求。

- 該地區各國也制定了電動車(EV)的多項目標。例如,美國的目標是到2032年將電動車的佔有率提高到35%左右。同樣,加拿大的目標是到 2035 年實現 100% 零排放車輛。

- 因此,隨著電動車的增加,預計該地區將在預測期內主導市場。

電動汽車電池負極產業概況

電動車電池正極市場一分為二。該市場的主要企業(排名不分先後)包括日亞化學公司、BASF公司、三菱化學集團公司、日立化學有限公司和3M公司。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車的擴張

- 鋰離子電池價格下降

- 抑制因素

- 供應鏈缺口

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 科技

- 鋰離子

- 鉛酸電池

- 其他

- 材料類型

- 磷酸鋰鐵

- 鈷酸鋰

- 錳酸鋰

- 二氧化鉛

- 其他

- 2029 年之前的市場規模和需求預測(按地區)

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 北歐的

- 俄羅斯

- 土耳其

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 澳洲

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 卡達

- 南非

- 其他中東/非洲

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 北美洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- NICHIA CORPORATION

- BASF SE

- Mitsubishi Chemical Group Corporation

- Hitachi Chemical Company Ltd

- 3M Company

- Panasonic Corporation

- Toshiba Corporation

- Umicore

- NEI Corporation

- Johnson Matthey PLC

- 其他知名公司名單

- 市場排名/佔有率(%)分析

第7章 市場機會及未來趨勢

- 正極材料和高效電解質的持續研究和進展

簡介目錄

Product Code: 50003538

The Electric Vehicle Battery Cathode Market size is estimated at USD 13.95 billion in 2025, and is expected to reach USD 28.36 billion by 2030, at a CAGR of 15.25% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, the growing adoption of electric vehicles and the decreasing price of lithium-ion batteries are expected to drive the market during the forecast period.

- On the other hand, the supply chain gap in battery materials created by the monopoly of some countries is expected to restrain market growth in the future.

- However, the ongoing research and advancement in cathode material and efficient electrolytes may offer opportunities for market growth.

- Asia-Pacific dominates the market, owing to the growing application of cathode material in the automotive industry, which augments the demand for cathode material.

Electric Vehicle Battery Cathode Market Trends

The Lithium-ion Battery Segment to Dominate the Market

- Lithium-ion batteries have emerged as the most commonly used battery technology in electric vehicles. This is due to their advantages, such as high energy density, relatively long cycle life, and efficiency.

- According to the International Energy Agency, demand for EV batteries reached more than 750 GWh in 2023, up 40% relative to 2022. Most of these batteries use lithium-ion technology. As the use of lithium-ion batteries in electric vehicles expands, the demand for cathode materials for lithium-ion battery technology is also expected to increase.

- According to the International Energy Agency, the share of electric vehicle sales is expected to increase to around 35% by 2030. Hence, in order to meet lithium-ion battery demand, the European Union is expected to increase its lithium-ion battery manufacturing capacity to 550 GWh by 2030.

- Additionally, the decreasing price of lithium-ion batteries is expected to drive the use of this technology in electric vehicles, which, in turn, will boost the demand for the use of cathode material of lithium-ion technology. In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh.

- Further, in the future, as research and development continue to use materials other than nickel and cobalt in cathode material, as they are rare and affect supply chain reliability, the demand for battery cathodes of lithium-ion technology is expected to increase.

- For instance, in November 2023, Toshiba Corporation developed a new lithium-ion battery featuring a cobalt-free 5V-class high-potential cathode material. This innovation plays a crucial role in suppressing the production of performance-degrading gases typically generated as side reactions.

- Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and technological developments, the lithium-ion battery cathode segment is expected to grow significantly during the forecast period.

North America is Expected to Have a Significant Share in the Market

- The North American electric vehicle market is majorly driven by the five major players, accounting for more than 70% of the market in 2023. These prominent players include Tesla, Toyota Group, Ford Group, Hyundai, and Honda. Tesla is the highest seller of electric vehicles in North American countries. As the demand for electric vehicles increases, the use of batteries in these vehicles will also increase, thereby driving the electric vehicle battery cathode market.

- The demand for electric vehicles is increasing continuously in North America. According to the Energy Information Administration, the combined sales of hybrid vehicles, plug-in hybrid electric vehicles, and battery electric vehicles (BEV) in the United States rose to 16.3% of total new light-duty vehicle (LDV) sales in 2023, which was 12.9% in the previous year.

- Further, supportive government policies are affecting the demand for electric vehicle batteries, thereby affecting the demand for the electric vehicle battery cathode market. Governments across North America have been rolling out policies and incentives to spur EV adoption. These initiatives encompass tax credits, grants, rebates, and investments in charging infrastructure. Such support has bolstered consumer interest in EVs, driving the demand for battery cathode.

- Also, the countries in the region have set multiple targets for electric vehicles (EVs). For instance, the United States aims to have an electric vehicle share of around 35% by 2032. Similarly, Canada aims to have 100% zero-emissions cars by 2035.

- Thus, with the growing number of electric vehicles, the region is expected to dominate the market during the forecast period.

Electric Vehicle Battery Cathode Industry Overview

The electric vehicle battery cathode market is semi-fragmented. Some of the major players in the market (in no particular order) include Nichia Corporation, BASF SE, Mitsubishi Chemical Group Corporation, Hitachi Chemical Company Ltd, and 3M Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Decreasing Price of Lithium-ion Batteries

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Other Technologies

- 5.2 Material Type

- 5.2.1 Lithium Iron Phosphate

- 5.2.2 Lithium Cobalt Oxide

- 5.2.3 Lithium Manganese Oxide

- 5.2.4 Lead Dioxide

- 5.2.5 Other Materials

- 5.3 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 NORDIC

- 5.3.2.7 Russia

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 South Korea

- 5.3.3.6 Malaysia

- 5.3.3.7 Thailand

- 5.3.3.8 Indonesia

- 5.3.3.9 Vietnam

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 Nigeria

- 5.3.4.4 Egypt

- 5.3.4.5 Qatar

- 5.3.4.6 South Africa

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 NICHIA CORPORATION

- 6.3.2 BASF SE

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Hitachi Chemical Company Ltd

- 6.3.5 3M Company

- 6.3.6 Panasonic Corporation

- 6.3.7 Toshiba Corporation

- 6.3.8 Umicore

- 6.3.9 NEI Corporation

- 6.3.10 Johnson Matthey PLC

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research and Advancement in Cathode Material and Efficient Electrolytes