|

市場調查報告書

商品編碼

1636426

零廢棄物雜貨店:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Zero-Waste Grocery Stores - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

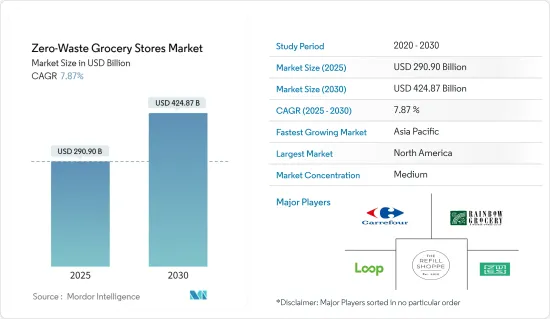

零廢棄雜貨店市場規模預計到 2025 年為 2,909 億美元,到 2030 年預計將達到 4,248.7 億美元,預測期內(2025-2030 年)複合年成長率為 7.87%。

零廢棄物商店正在重塑零售格局,為顧客提供無塑膠和包裝的購物體驗。這些商店主要專注於填充用和散裝食品,鼓勵消費者自備食品、個人護理和清潔產品容器。全球此類商店的數量正在增加,許多商店現在正在透過線上平台尋求群眾集資。除了不使用包裝外,零廢棄物商店通常具有整體和永續的理念,並以各種本地採購的有機產品為特色。這種獨特的方法使我們有別於傳統的零售店,並為我們開闢了一個利基市場。

站在永續購物機芯的最前沿,零廢棄物雜貨店不僅在概念上而且在實踐中做出了聲明。其影響不僅體現在減少廢棄物的努力上,也體現在刺激主要雜貨零售連鎖店的反應。儘管超級市場僅占美國食品店的 10%,但每年的食品浪費卻增加了數十億美元。此外,光是食品包裝就佔所有垃圾掩埋廢棄物的 23%。

零廢棄物雜貨店市場趨勢

零廢棄物雜貨店將在超級市場和大賣場激增,推動成長

以提供多樣化產品而聞名的超級市場和大賣場擴大將零廢棄物雜貨店納入其分銷管道。這些商店提供了一個獨特的機會,透過提供保鮮膜、袋子和吸管等傳統包裝的替代品來對抗一次性塑膠。儘管如此,傳統超級市場和大賣場仍然是受歡迎的購物目的地,尤其是生鮮食品。特別是,隨著超級市場不再使用一次性塑膠包裝,蔬菜銷售量大幅成長。除了環境效益之外,零廢棄物還可以透過減少人事費用、能源和處置成本,為企業節省大量成本。

線上零售通路預計在預測期內成長最快。這一勢頭歸因於全球網路購物的增加,顯示消費行為發生了明顯的轉變。

北美市場領先

隨著環保意識的增強,塑膠廢棄物的影響受到越來越多的關注。美國和加拿大的個人處於永續性運動的最前線。為了支持這項轉變,該地區各國政府正在推出管理環境廢棄物的舉措,為未來幾年的市場大幅成長奠定基礎。雖然商店顯然正在積極減少廢棄物,但大型零售超級市場也擁抱這一趨勢。

光是超級市場就占美國每年排放的食物廢棄物的 10%。此外,食品包裝佔垃圾掩埋廢棄物的 23%。目標是透過由 Care Food、Kroger 和 Walmart 等領先公司主導的 10x20X30 計劃,在未來 10 年內減少食物廢棄物。到 2030 年,這些主要零售商的目標是與至少 20 家供應商合作,進一步減少廢棄物。隨著永續購物的推動勢頭增強,零廢棄物商店可能會成為新常態。

零廢棄雜貨產業概述

零廢棄物雜貨店市場呈現出一種半獨特的情況,目前只有少數幾種選擇。本報告深入研究了主要企業的競爭動態,包括: Rainbow Grocery、Loop、Zero Waste Eco Store、家樂福和 The Refill Shoppe。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態與洞察

- 市場概況

- 市場促進因素

- 環保意識的提高推動市場

- 消費者對環保選擇的需求推動市場成長

- 市場限制因素

- 高昂的初始設置成本阻礙了市場成長

- 維持商店衛生標準的物流問題

- 市場機會

- 與當地生產商和供應商的潛在夥伴關係

- 利用數位平台進行線上銷售

- 價值鏈分析

- 產業吸引力波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

- 洞察產業技術進步

- COVID-19 對市場的影響

第5章市場區隔

- 按分銷管道

- 超級市場/大賣場

- 專賣店

- 網路商店

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 德國

- 法國

- 俄羅斯

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲

- 北美洲

第6章 競爭狀況

- 市場集中度概況

- 公司簡介

- Rainbow Grocery

- Loop

- Zero Waste Eco Store

- Carrefour

- The Refill Shoppe

- Just Gaia

- Zero Muda

- EcoRefill

- ecoTopia

- Lidl*

第7章 未來市場趨勢

第 8 章 免責聲明與出版商訊息

The Zero-Waste Grocery Stores Market size is estimated at USD 290.90 billion in 2025, and is expected to reach USD 424.87 billion by 2030, at a CAGR of 7.87% during the forecast period (2025-2030).

Zero waste stores are reshaping the retail landscape, offering customers a plastic and packaging-free shopping experience. These stores primarily focus on refill and bulk options, encouraging shoppers to bring their containers for food, personal care, and cleaning products. The global count of such stores has surpassed, with many new ones seeking crowdfunding on online platforms. Beyond being packaging-free, zero-waste stores often champion a holistic, sustainable ethos, showcasing a range of local and organic products. This distinctive approach sets them apart from traditional retailers, carving a niche for themselves.

Zero-waste grocery stores, at the forefront of the sustainable shopping movement, are making a statement not just in concept but also in practice. Their impact is evident, not only in their waste reduction efforts but also in catalyzing responses from major retail grocery chains. Despite accounting for just 10% of food outlets, US supermarkets add massive billions of dollars to the total yearly food waste. Furthermore, food packaging alone constitutes 23% of all landfill waste.

Zero-Waste Grocery Stores Market Trends

Zero-Waste Grocery Stores Proliferate in Supermarkets and Hypermarkets, Propelling Growth

Supermarkets and hypermarkets, known for their diverse product offerings, have seen a surge in the inclusion of zero-waste grocery stores within their distribution channels. These stores present a unique opportunity to combat single-use plastic by offering alternatives to traditional packaging, such as plastic wraps, bags, and straws. Despite this, traditional supermarkets and hypermarkets remain popular shopping destinations, especially for fresh produce. Notably, supermarkets that transitioned away from single-use plastic packaging witnessed a remarkable surge in vegetable sales. Beyond the environmental benefits, going zero-waste also translates to significant cost savings for businesses, cutting down on labor, energy, and disposal expenses.

The online retail channel is poised for the swiftest growth during the forecast period. This momentum is fueled by the global uptick in online shopping, indicating a clear shift in consumer behavior.

North America Leading the Market

As environmental consciousness rises, so does the scrutiny of the repercussions of plastic waste. Individuals in the United States and Canada are spearheading the movement toward sustainability. Bolstering this shift, governments in the region have rolled out initiatives to manage environmental waste, setting the stage for significant market growth in the coming years. While it's evident that stores are actively reducing waste in their operations, major retail supermarket chains are also embracing this trend.

Supermarkets alone contribute to 10% of food waste produced annually in the United States. Additionally, food packaging constitutes a significant 23% of landfill waste. Through the "10x20X30 Initiative," spearheaded by major players like Kea Food, Kroger, and Walmart, the goal is to slash food waste over the next decade. By 2030, these leading retailers aim to collaborate with at least 20 suppliers each, furthering their waste reduction efforts. As the push for sustainable shopping gains momentum, zero-waste stores are set to become the new norm.

Zero-Waste Grocery Stores Industry Overview

The zero-waste grocery store market exhibits a semi-consolidated landscape, with only a handful of options available presently. The report delves into the competitive dynamics, highlighting key players such as Rainbow Grocery, Loop, Zero Waste Eco Store, Carrefour, and The Refill Shoppe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Environmental Consciousness Driving the Market

- 4.2.2 Consumer Demand for Eco-friendly Options Fuels Growth of the Market

- 4.3 Market Restraints

- 4.3.1 Higher Initial Setup Costs Hinder Growth of the Market

- 4.3.2 Logistical Challenges in Maintaining Hygiene Standards in Stores

- 4.4 Market Opportunities

- 4.4.1 Potential Partnerships with Local Producers and Suppliers

- 4.4.2 Leveraging Digital Platforms for Online Sales

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness: Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Advancements in the Industry

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Distribution Channel

- 5.1.1 Supermarkets/Hypermarkets

- 5.1.2 Speciality Stores

- 5.1.3 Online Stores

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Italy

- 5.2.2.6 Spain

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Rainbow Grocery

- 6.2.2 Loop

- 6.2.3 Zero Waste Eco Store

- 6.2.4 Carrefour

- 6.2.5 The Refill Shoppe

- 6.2.6 Just Gaia

- 6.2.7 Zero Muda

- 6.2.8 EcoRefill

- 6.2.9 ecoTopia

- 6.2.10 Lidl*

7 FUTURE MARKET TRENDS

8 DISCLAIMER AND ABOUT US

紙袋市場按材料類型、樣式、數量、最終用戶和分銷管道分類 - 2025-2030 年全球預測

紙袋市場按材料類型、樣式、數量、最終用戶和分銷管道分類 - 2025-2030 年全球預測 紙袋包裝市場預測至 2030 年:按產品類型、材料類型、密封和手柄類型、最終用戶和地區進行全球分析

紙袋包裝市場預測至 2030 年:按產品類型、材料類型、密封和手柄類型、最終用戶和地區進行全球分析 2025 年全球多層袋市場報告購物袋市場規模、佔有率和成長分析(按材料類型、袋子類型、應用、最終用戶和地區)- 產業預測 2025-2032

2025 年全球多層袋市場報告購物袋市場規模、佔有率和成長分析(按材料類型、袋子類型、應用、最終用戶和地區)- 產業預測 2025-2032 紙袋市場按產品類型、厚度、材料、最終用途和地區分類 - 預測至 2029 年

紙袋市場按產品類型、厚度、材料、最終用途和地區分類 - 預測至 2029 年 中東和非洲紙袋:市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)麻紙:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)全球雜貨店紙袋市場:按產品類型、材料、尺寸(小、中、大)、應用和地區預測到 2032 年

中東和非洲紙袋:市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)麻紙:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)全球雜貨店紙袋市場:按產品類型、材料、尺寸(小、中、大)、應用和地區預測到 2032 年 全球紙袋牛皮紙市場規模:依等級、包裝類型、最終用途行業、區域範圍和預測

全球紙袋牛皮紙市場規模:依等級、包裝類型、最終用途行業、區域範圍和預測 牛皮紙袋市場規模、佔有率和趨勢分析報告:2025-2030 年按紙張、產品、厚度、最終用途、地區和細分市場進行的預測

牛皮紙袋市場規模、佔有率和趨勢分析報告:2025-2030 年按紙張、產品、厚度、最終用途、地區和細分市場進行的預測