|

市場調查報告書

商品編碼

1637742

Memristor -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Memristors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

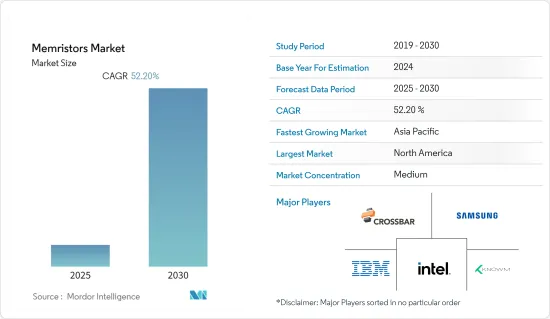

憶阻器市場預計在預測期內複合年成長率為 52.2%

主要亮點

- 過去 50 年來,憶阻器技術一直在不斷發展。在此期間,英特爾、松下、美光等公司在這一領域不斷創新。憑藉節能、高性能、頻寬需求、節省空間和提高資料傳輸速度等前景廣闊的特性,憶阻器預計將在預測期結束時成為主流產品。

- 基於憶阻器的記憶體可實現低功耗、快速寫入速度、良好的可擴展性、 3D整合、低成本以及與CMOS製造製程的兼容性等優越性能,使其成為儲存級記憶體中CMOS的有吸引力的選擇。此外,該技術的商業化將產生一些新的使用案例使用案例,因為許多材料(大致分為2D材料、金屬氧化物、新興材料、有機物等)表現出憶阻效應,可以促進生長。

- 此技術可主要在ReRAM、混合電路、突觸、神經型態形態架構、深度學習和可重構邏輯等領域實現商業化。電阻式 RAM (ReRAM) 是基於憶阻器的技術中最成熟的。多年來,ReRAM 已經推出了許多紙本版本,並已獲得多項專利。

- 然而,這項技術是新技術,面臨許多挑戰,包括與時間相關的狀態保留能力的兼容性問題、與憶阻器框架兼容的新材料的發現、模擬和數位領域的應用、對讀/寫刺激的響應以及功率要求我有一個挑戰。

- 儘管COVID-19的爆發對憶阻器市場的影響很小,但這種流行病顯著提高了消費者對數位和先進技術的認知,這意味著憶阻器將自己定位為一種有前途的下一代技術。

憶阻器市場趨勢

IT/通訊領域佔主要市場佔有率

- 憶阻器有望成為 IT 和電訊領域的突破性技術,因為它們有潛力增強積體電路設計和運算的多個領域。憶阻器可用於伺服器、超級電腦、資料中心、攜帶式電子產品、工業機器人等。考慮到這些優勢,各大半導體和記憶體公司都在投資憶阻器市場,預計將推動市場成長。

- 電子業、IT和通訊業佔據Mimrista很大的市場佔有率。由於在保持成本的同時對高處理能力和記憶體密度的需求不斷增加,IT 領域對高速效能的需求持續成長。此外,更高效能圖形系統的出現進一步增加了對提高處理速度的需求,從而導致對憶阻器的需求增加。

- 憶阻器相對於其他儲存組件的優勢在於易於製造具有神經架構的設備。隨著神經架構搜尋(NAS)等趨勢在資料中心產業中佔據越來越重要的地位,憶阻器是幫助產業實現此類技術潛力的重要一步,它可以成為重要的技術推動者。

- 此外,人們對雲端運算等數位技術的認知和接受度不斷提高,預計將為憶阻器市場的成長創造有利的市場前景。例如,根據歐盟委員會的數據,到 2021 年,歐盟 (EU) 約 41% 的公司將使用雲端運算。此外,根據衡量歐洲創新的各種指標的歐洲創新記分牌,芬蘭在資訊科技領域的創新得分最高。預計這些趨勢將對預測期內所研究市場的成長產生正面影響。

北美佔最大市場佔有率

- 與其他地區相比,北美是憶阻器最重要的市場之一,因為當地參與企業的研發投資率很高,而且憶阻器組件整合商可以獲得大量資訊。許多著名的市場參與企業都位於美國,該國最近也加入了 Mimrista 的大部分應用,包括神經形態運算、汽車、軟性電子產品、物聯網、邊緣運算和工業機器人,它也是最多的國家之一。國。

- 與世界其他地區相比,該地區對邊緣運算和先進電子產品等市場的投資明顯較高。根據Linux基金會發布的邊緣現況報告,由於北美在網路和雲端運算產業的主導地位,預計到2028年,全球約20.5%的基礎設施邊緣將部署在北美。

- 北美地區對智慧型手機、電腦和其他智慧家庭產品等先進消費產品也有很高的需求。 Mimrista 的實施是實現強大且廉價的分散式感測和處理解決方案的一步,預計在預測期內,其需求將進一步成長。

- 此外,該地區神經形態運算、物聯網和儲存記憶體市場的新興市場開發,特別是當地公司的技術創新,預計將不僅在該地區而且在全球範圍內促進 Mimrista 技術的市場成長。此外,資料中心和工業應用等各種最終用戶產業的採用預計將擴大,據報道,這些產業在北美地區正在快速成長。

憶阻器產業概況

隨著新參與企業進入憶阻器市場,憶阻器市場的競爭正在加劇。儘管在市場上佔據重要地位的參與企業很少,但隨著技術的進步,預計會有更多的參與企業進入市場,從而加劇市場競爭。為了進一步提高在市場上的影響力,供應商擴大擴大研發足跡,以開發創新的解決方案。市場上一些主要企業包括 Crossbar Inc.、IBM Corporation 和 Knowm Inc.。

2022 年 7 月,由 IIT Jodhpur主導的多機構計劃的研究人員成功創建了一種具有超低功耗的高性能電阻式儲存(憶阻器)裝置。該裝置由硒化鎘(CdSe)量子點(QD)組成,具有高開/關比、優異的RAM性能、快速運行和長保留時間。此元件能夠以高運轉速度執行邏輯運算,適合高密度資料儲存應用。

2022 年 5 月,蘇黎世聯邦理工學院、蘇黎世大學和 Empa 的研究人員開發了一種可用於廣泛應用的電子元件新材料。該組件有助於創建更有效率的電子電路來執行機器學習任務。此外,開發的憶阻器由鹵化物鈣鈦礦結晶製成,這是一種主要用於光伏電池的半導體材料。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 對物聯網、雲端運算和巨量資料的需求不斷成長

- 自動化機器人應用需求快速成長

- 市場限制因素

- 技術應用的複雜性

- 技術簡介

- 分子薄膜和離子薄膜

- 旋轉底座與磁憶阻器

第6章 市場細分

- 按用途

- 非揮發性記憶體

- 神經型態和生物系統

- 可程式邏輯和訊號處理

- 按最終用戶產業

- 消費性電子產品

- 資訊科技和電訊

- 車

- 醫療保健

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 其他

第7章 競爭格局

- 公司簡介

- Crossbar Inc.

- Panasonic Corporation

- 4DS Memory Limited

- Adesto Technology

- Micron Technologies Inc.

- Samsung Group

- Sony Corporation

- Western Digital Corporation

- Knowm Inc.

- Intel Corporation

- IBM Corporation

- SK Hynix Inc.

- Weebit Nano Ltd

- Fujitsu Ltd

- Toshiba Corp.

- Honeywell International Ltd

- Everspin Technologies Inc.

- ST Microelectronics NV

- Avalanche Technology Inc.

第8章投資分析

第9章市場的未來

The Memristors Market is expected to register a CAGR of 52.2% during the forecast period.

Key Highlights

- Memristor technology has seen a series of developments over the last 50 years. During this period, companies like Intel, Panasonic, and Micron, among others, have continued to innovate in this field. Given the promising features to improve power saving, performance, bandwidth requirement, and space-saving augmented with data transfer rate, memristors are expected to become a mainstream product by the end of the forecast period.

- Memristor-based memories are considered the more extensive prospect to replace CMOS in the storage class memory, as they are capable of delivering outstanding performance, such as low power consumption, fast write speed, great scalability, three-dimensional integration, low cost, and compatibility with the CMOS fabrication process. Furthermore, because many materials are showing memristive effects, broadly classified as 2D materials, metal oxides, emerging materials, and organics, commercialization of this technology can open several new use cases, driving the growth of the studied market.

- Technology commercialization is possible, mainly in areas like ReRAM, hybrid circuits, synapses, neuromorphic architectures, deep learning, and reconfigurable logic. Resistive RAM, or ReRAM, has been the most developed among all the memristor-based technologies. ReRAM has had many papers published and several patents granted over the years.

- However, the technology is new and poses many challenges like state retention capacity concerning time, finding new material which fits into memristive framework, applications in analog and digital domains, response to reading/write stimulus, and compatibility issues in terms of power requirement, among others.

- Although the outbreak of COVID-19 had a minimal impact on the memristors market, the fact that the pandemic has significantly increased consumers' awareness about digital and advanced technologies is expected to have a long-term effect on the growth of the studied market as memristor presents itself as promising next-generation technology, which is expected to have a high impact on the future trends of the electronics and related industries.

Memristors Market Trends

IT and Telecom Sector to Hold a Significant Market Share

- Memristors are expected to be a breakthrough technology for the IT and Telecom sector as they have the potential to enhance several areas of integrated circuit design and computing. Memristors can be used in servers, supercomputers, data centers, portable electronics, and industrial robotics. Considering the benefits, leading semiconductor and memory companies are investing in the memristor market, which is expected to boost the market's growth.

- The electronic, IT, and telecommunications industries hold significant market shares for memristors. The requirements for high-speed performance are continuously increasing in the IT sector, owing to the rising need for high processing power and memory density while maintaining the cost. Additionally, the arrival of higher graphics systems further drives the need for better processing speeds, thus driving the demand for memristors.

- Memristors' advantage over other memory components is that they make it easier to produce devices with neural architecture. With trends such as Neural Architecture Search (NAS) increasingly making space in the data center industry, memristors can be a key technology enabler to help the industry realize the potential of such technologies.

- Furthermore, the increasing awareness and acceptance of digital technologies, such as cloud computing, are expected to create a good market scenario for the growth of the memristors market. For instance, according to the European Commission, about 41% of enterprises in the European Union used cloud computing in 2021. Furthermore, according to the European innovation scoreboard, which measures innovation in Europe through various indicators, Finland had the highest innovation scores in information technologies. Such trends will positively impact the growth of the studied market during the forecast period.

North America to Hold the Largest Market Share

- North America is one of the most significant markets for memristors, owing to the high rate of investment in R&D by local players and the highly informed integrator base of memristor components compared to other regions. Many of the prominent market players are US-based, and the country is also one of the most prominent contributors to a majority of the applications of memristors, including neuromorphic computing, automotive, flexible electronics, IoT, edge computing, and industrial robotics in the recent past.

- The region's investment in markets like edge computing and advanced electronics is significantly higher compared to other parts of the world. According to The State of Edge report published by the Linux Foundation, it is estimated that about 20.5% of the global Infrastructure Edge will be deployed in North America by 2028, owing to its dominance in the internet and cloud computing industry.

- The North American region also highly demands advanced consumer products such as smartphones, computers, and other intelligent home gadgets. As the implementation of memristors takes a step further to creating powerful and cheap distributed solutions for sensing and processing, their demand is expected to grow further during the forecast period.

- Furthermore, the developments and innovations in the regional neuromorphic computing, IoT, and storage memory market, especially by local players, are anticipated to augment the market growth for the memristor technology not only in the region but also globally. Also, it will expand its adoption across various end-user industries, including data centers and industrial, which are also reporting rapid growth in the North American region.

Memristors Industry Overview

The memristors market is growing in competition as new players are inclining toward it. Few players hold a significant presence in the market; however, with technological advancements, more and more players are expected to enter the market, driving the market's competition. To further consolidate their market presence, the vendors are increasingly focusing on expanding their R&D footprint into developing innovative solutions. Some major players in the market include Crossbar Inc., IBM Corporation, and Knowm Inc.

In July 2022, researchers working on a multi-institutional project led by IIT Jodhpur successfully fabricated high-performance resistive memory (memristor) devices with ultralow power consumption. The fabricated device comprises cadmium selenide (CdSe) quantum dots (QDs) with a high on/off ratio, good RAM performance, fast operation speed, and long retention time. This device is suitable for high-density data storage applications as it can perform logical operations with fast operation speed.

In May 2022, a new material for an electronic component that can be used in broad applications ranges was developed by researchers from ETH Zurich, the University of Zurich, and Empa. These components will help create more efficient electronic circuits to perform machine-learning tasks. Furthermore, the memristors developed are made of halide perovskite nanocrystals, a semiconductor material known primarily for its use in photovoltaic cells.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for IoT, Cloud Computing, and Big Data

- 5.1.2 Surging Demand for Application of Automation Robots

- 5.2 Market Restraints

- 5.2.1 Complexity in Technological Application

- 5.3 Technology Snapshot

- 5.3.1 Molecular and Ionic Thin Film

- 5.3.2 Spin-based and Magnetic Memristor

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Non-volatile Memory

- 6.1.2 Neuromorphic and Biological System

- 6.1.3 Programmable Logic and Signal Processing

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 IT and Telecom

- 6.2.3 Automotive

- 6.2.4 Healthcare

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Crossbar Inc.

- 7.1.2 Panasonic Corporation

- 7.1.3 4DS Memory Limited

- 7.1.4 Adesto Technology

- 7.1.5 Micron Technologies Inc.

- 7.1.6 Samsung Group

- 7.1.7 Sony Corporation

- 7.1.8 Western Digital Corporation

- 7.1.9 Knowm Inc.

- 7.1.10 Intel Corporation

- 7.1.11 IBM Corporation

- 7.1.12 SK Hynix Inc.

- 7.1.13 Weebit Nano Ltd

- 7.1.14 Fujitsu Ltd

- 7.1.15 Toshiba Corp.

- 7.1.16 Honeywell International Ltd

- 7.1.17 Everspin Technologies Inc.

- 7.1.18 ST Microelectronics NV

- 7.1.19 Avalanche Technology Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

憶阻器市場機會、成長促進因素、產業趨勢分析與 2024 年至 2032 年預測

憶阻器市場機會、成長促進因素、產業趨勢分析與 2024 年至 2032 年預測 憶阻器市場報告:2030 年趨勢、預測與競爭分析

憶阻器市場報告:2030 年趨勢、預測與競爭分析 全球憶阻器市場規模研究(按最終用戶產業應用和 2022-2032 年區域預測)

全球憶阻器市場規模研究(按最終用戶產業應用和 2022-2032 年區域預測) 憶阻器市場報告(按類型(分子和離子膜憶阻器、自旋和磁性憶阻器)、垂直產業(電子、IT 和電信、工業、航太和國防、汽車、醫療保健)和地區2024 -2032

憶阻器市場報告(按類型(分子和離子膜憶阻器、自旋和磁性憶阻器)、垂直產業(電子、IT 和電信、工業、航太和國防、汽車、醫療保健)和地區2024 -2032 憶阻器市場-2024年至2029年預測

憶阻器市場-2024年至2029年預測 憶阻器全球市場規模、佔有率、趨勢分析報告:按類型、產業、地區分類的展望與預測,2024-2031憶阻器市場:按類型、產業:2024-2032 年全球機會分析與產業預測憶阻器市場,按類型、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測

憶阻器全球市場規模、佔有率、趨勢分析報告:按類型、產業、地區分類的展望與預測,2024-2031憶阻器市場:按類型、產業:2024-2032 年全球機會分析與產業預測憶阻器市場,按類型、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測 憶阻器市場 - 全球產業規模、佔有率、趨勢、機會和預測。按類型、按應用、垂直產業、地區、公司和地理位置細分,2018-2028 年預測和機會離子膜憶阻器市場報告:2030 年趨勢、預測與競爭分析

憶阻器市場 - 全球產業規模、佔有率、趨勢、機會和預測。按類型、按應用、垂直產業、地區、公司和地理位置細分,2018-2028 年預測和機會離子膜憶阻器市場報告:2030 年趨勢、預測與競爭分析