|

市場調查報告書

商品編碼

1637776

石油和天然氣產業的氣體壓縮機:市場佔有率分析、產業趨勢、成長預測(2025-2030)Oil And Gas Industry Gas Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

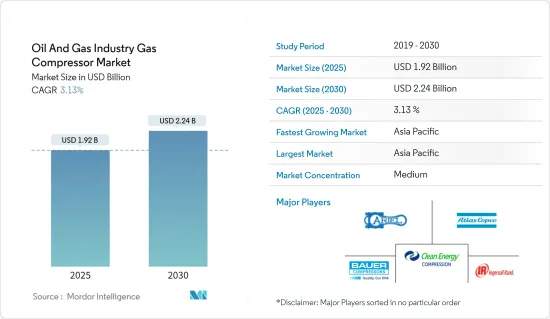

石油和天然氣工業氣體壓縮機市場規模預計到2025年為19.2億美元,預計到2030年將達到22.4億美元,預測期內(2025-2030年)複合年成長率為3.13%。

主要亮點

- 從長遠來看,各種應用的天然氣消費量成長將極大地推動市場,天然氣生產和供應計劃的增加以及當前情況下合理的天然氣價格對上游行業產生積極影響。

- 另一方面,可再生能源在能源領域的日益滲透為天然氣消費帶來了激烈的競爭,從而阻礙了許多應用中氣體壓縮機部署的成長。

- 天然氣探明蘊藏量的增加,特別是最近影像中的海上天然氣田,正在為氣體壓縮機市場創造重大機會。最近的一個例子是俄羅斯盧克石油公司在墨西哥海岸發現的石油和天然氣田。據認為,未來將生產的新油田將導致集輸管線氣體壓縮機的部署擴大。

油氣壓縮機市場趨勢

中游產業預計將主導市場

- 石油和天然氣產業中游使用的氣體壓縮機部署在天然氣輸送管網或壓縮氣體儲存單元。管道中流動的氣體會經歷壓力降,隨著流速和管道長度的增加而增加。因此,每 50 至 100 英里需要一個壓縮機站來重新壓縮氣體並補償壓力損失。

- 過去10年天然氣消費量呈現持續成長趨勢,2022年消費量量約39,413億立方公尺。隨著許多國家政府推廣清潔能源產出方法,預計未來幾年需求將會成長。未來幾年,許多管道和液化天然氣計劃將被添加到許多中游公司已完成的計劃清單中。

- 例如,Adelphia Gateway計劃獲得了美國聯邦能源管理委員會(FERC)的第二階段計劃建設核准。該計劃包括將現有 84 英里長的石油管線改造成天然氣分配管道,以便在費城地區發行。開發商 Adelphia Gateway LLC 預計將於 2023年終從管道輸送第一批天然氣。

- 此外,2023 年 2 月,印度國營碳氫化合物巨頭石油和天然氣公司啟動了一項大型管道更換計劃,計劃對其西海岸主要油田的生產至關重要。這個耗資4.46億美元的計劃將確保ONGC西海岸4萬平方公里油田的石油和天然氣穩定供應。由於壓縮機通過增加天然氣壓力並使其能夠從生產現場運輸,在石油和天然氣行業中發揮著至關重要的作用,因此此類計劃反過來將增加整個行業壓縮機的使用。

- 這些發展必將對預測期內的石油和天然氣工業氣體壓縮機市場產生正面影響。

亞太地區預計將主導市場成長

- 由於運輸和工業部門消費的增加,亞太地區在不久的將來可能佔天然氣需求成長的一半。為了滿足發電業和其他用途對天然氣的需求,該地區正在擴大管道網路,主要是在印度和中國等國家。

- 2022年中國液化天然氣和管道天然氣進口量將達到創紀錄水平,過去十年液化天然氣進口量增加超過16.6%。進口激增將導致國內管道基礎設施的擴建。此外,印度計劃在 2023 年之前有 34,384 公里的新管道運作。

- 2023年3月,阿美公司與合資夥伴盤錦新城工業集團和北方工業集團宣布計畫在中國東北地區開始建造大型煉油化工綜合體。該綜合體將包括日產30萬桶煉油廠和石化廠,每年生產165萬噸乙烯和200萬噸對二甲苯。計劃獲得行政批准後,預計將於 2023 年第二季開工。計劃於 2026 年全面運作。

- 此外,CNG加氣站網路的快速擴張也帶動了亞太地區氣體壓縮機市場的發展。例如,2023年4月,印度政府宣布訂定目標,到2030年在全國安裝約17,700個CNG加氣站。

- 由於這些新興市場的開發,預計在研究期間,亞太地區的氣體壓縮機市場將最為繁榮。

油氣壓縮機產業概況

石油和天然氣產業的氣體壓縮機市場正變成半固體。主要企業(排名不分先後)包括 Atlas Copco AB、Ariel Corporation、Bauer 壓縮機公司、Clean Energy Fuels Corp. 和 Ingersoll Rand PLC。

阿特拉斯·科普柯公司採取了多項策略,包括注重研發、擴大市場開發、提高業務效率、開發可提供更高價值的新永續產品和解決方案以及提高能源效率。例如,阿特拉斯科普柯於 2023 年 2 月推出了新一代 GA 和 GA+ 定速智慧工業空氣壓縮機。這些創新使我們能夠透過多樣化的產品系列來更好地滿足工業客戶不斷變化的需求。這些新型壓縮機也可用於天然氣加工和氫氣生產等清潔能源應用。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 2028年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 各種用途的天然氣消耗量成長

- 抑制因素

- 擴大可再生能源在能源領域的應用

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 類型

- 往復式

- 擰緊

- 目的

- 上游

- 下游

- 中產階級

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 西班牙

- 英國

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 馬來西亞

- 印尼

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 南非

- 其他中東/非洲

- 北美洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Ariel Corporation

- Atlas Corporation AB

- Bauer Compressors Inc.

- Burckhardt Compression Holding AG

- Clean Energy Fuels Corp.

- General Electric Company

- HMS Group

- Howden Group Ltd

- Ingersoll Rand PLC

- Siemens AG

第7章 市場機會及未來趨勢

- 天然氣探明蘊藏量增加,特別是海上天然氣田

The Oil And Gas Industry Gas Compressor Market size is estimated at USD 1.92 billion in 2025, and is expected to reach USD 2.24 billion by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the market is largely driven by the growth in natural gas consumption for various applications, which has led to more gas production and transmission projects and reasonable natural gas prices in the current scenario, which has a positive impact on the upstream sector.

- On the other hand, the growing penetration of renewables in the energy sector offers stiff competition to natural gas consumption and thus impedes the growth of gas compressor deployment in numerous applications.

- Nevertheless, the increase in natural gas proved reserves, particularly offshore gas fields in the recent picture, places a tremendous opportunity for the gas compressor market. The very recent Russian group's Lukoil's oil and gas field discovery off the coast of Mexico is an example of the same. The new upcoming producing fields will lead to a greater deployment of gas compressors for gathering lines.

Oil and Gas Compressor Market Trends

Midstream Sector Expected to Dominate the Market

- The gas compressors used in the midstream oil and gas industry are deployed either within the gas transmission pipeline network or at the compressed gas storage units. Gas flowing in pipelines suffers from pressure losses that increase with flow velocity and the length of the pipe. Therefore, every 50 to 100 miles, a compressor station is necessary to recompress the gas and compensate for the pressure losses.

- Natural gas consumption continuously showed an advancing trend over the last 10 years, with around 3941.3 billion cubic meters of consumption in 2022. The demand is expected to grow in the coming years due to the government's push for cleaner methods of energy generation in many countries. A number of pipeline and LNG projects are about to be added to the list of accomplished projects of many midstream companies in the coming years.

- For instance, the Adelphia Gateway Project received approval for the construction of the second phase of the project from the Federal Energy Regulatory Commission (FERC), United States. The project includes the conversion of an existing 84-mile oil pipeline to a gas supply pipeline for distribution in the Philadelphia region. The developer, Adelphia Gateway LLC, is expected to be able to supply the first gas from the pipeline by the end of 2023.

- Furthermore, in February 2023, Oil and Natural Gas Corporation, India's state-owned hydrocarbon giant, initiated a big-buck pipeline replacement project, a crucial project for the company's production from key west coast fields. The USD 446 million project will ensure a stable supply of oil and gas from ONGC wells covering an area of 40,000 square kilometers along the western coast. Since compressors play a crucial role in the oil and gas industry in increasing the pressure of natural gas and allowing natural gas transportation from the production site, this kind of project will, in turn, promote the usage of compressors across the industry.

- Such developments will inevitably have a positive impact on the gas compressor market in the oil and gas industry during the forecast period.

Asia-Pacific Expected to Dominate Market Growth

- Asia-Pacific can account for half of the incremental gas demand in the near future due to increased consumption in the transport and industrial sectors. To serve the natural gas demand for the power generation industry and other applications, the region has witnessed an expansion in the pipeline network, mainly in countries like India and China.

- China's LNG and pipeline imports of natural gas reached record levels in 2022, with an increment of more than 16.6% in LNG imports during the last decade, whereas the gas pipeline monthly imports approached a peak level of 4 million metric tons. The surge in imports will lead to an expansion of the supporting pipeline infrastructure in the country. Moreover, India is expected to bring 34,384 km of new pipelines online by 2023.

- In March 2023, Aramco and joint venture partners Panjin Xincheng Industrial Group and NORINCO Group announced plans to start the construction of a significant integrated refinery and petrochemical complex in northeast China. The complex is going to have combination of a 300,000 barrels per day refinery and a petrochemical plant with an annual production capacity of 1.65 million tons of ethylene and 2 million metric tons of paraxylene. Construction is expected to start in the second quarter of 2023 after the project has secured administrative approvals. It is expected to be fully operational by 2026.

- Also, the rapidly growing network of CNG fueling stations has led to the development of the gas compressor market in the Asia-Pacific region. For example, in April 2023, the government of India announced the target has been fixed to establish around 17,700 CNG stations across the country by 2030.

- Owing to such developments, the gas compressor market is expected to flourish to the greatest extent in the Asia-Pacific region during the study period.

Oil and Gas Compressor Industry Overview

The oil and gas industry's gas compressor market is semi-consolidated. Some of the major companies (in no particular order) include Atlas Copco AB, Ariel Corporation, Bauer Compressor Inc., Clean Energy Fuels Corp., and Ingersoll Rand PLC, among others.

Atlas Copco AB has adopted many strategies like focus on research and development, increase market coverage, increase operational efficiency, develop new sustainable products and solutions offering better value and improved energy efficiency. As an example, in February 2023, the company launched its next generation GA and GA+fixed speed smart industrial air compressors,. Such technological innovations would enable the company to better respond to the changing needs of the industrial customers with diversified product portfolio. These new type of compressors can also be used for clean energy applications like natural gas processing, and hydrogen production.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Natural Gas Consumption for Various Applications

- 4.5.2 Restraints

- 4.5.2.1 Growing Penetration of Renewables in the Energy Sector

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Reciprocating

- 5.1.2 Screw

- 5.2 Application

- 5.2.1 Upstream

- 5.2.2 Downstream

- 5.2.3 Midstream

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 Spain

- 5.3.2.4 United Kingdom

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Indonesia

- 5.3.3.5 Rest of Asia-Pacifc

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirated

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Ariel Corporation

- 6.3.2 Atlas Corporation AB

- 6.3.3 Bauer Compressors Inc.

- 6.3.4 Burckhardt Compression Holding AG

- 6.3.5 Clean Energy Fuels Corp.

- 6.3.6 General Electric Company

- 6.3.7 HMS Group

- 6.3.8 Howden Group Ltd

- 6.3.9 Ingersoll Rand PLC

- 6.3.10 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Natural Gas Proved Reserves, Particularly Offshore Gas Fields

全球正排量氣體壓縮機市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球正排量氣體壓縮機市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 氣體壓縮機市場:按類型、功能和最終用戶分類 - 2025-2030 年全球預測

氣體壓縮機市場:按類型、功能和最終用戶分類 - 2025-2030 年全球預測 全球氣體壓縮機市場

全球氣體壓縮機市場 2024-2032 年按壓縮機類型、最終用途行業和地區分類的氣體壓縮機市場報告

2024-2032 年按壓縮機類型、最終用途行業和地區分類的氣體壓縮機市場報告 全球正排量氣體壓縮機市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球正排量氣體壓縮機市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 2024-2028年全球CNG壓縮機市場

2024-2028年全球CNG壓縮機市場 氣體壓縮機全球市場2024-2028

氣體壓縮機全球市場2024-2028 氣體壓縮機市場:按技術、潤滑類型、最終用戶產業:2023-2032 年全球機會分析與產業預測

氣體壓縮機市場:按技術、潤滑類型、最終用戶產業:2023-2032 年全球機會分析與產業預測 CNG 壓縮機市場:按類型、按潤滑方法、按最終用戶、按地區

CNG 壓縮機市場:按類型、按潤滑方法、按最終用戶、按地區 CNG 壓縮機市場報告:2030 年趨勢、預測與競爭分析

CNG 壓縮機市場報告:2030 年趨勢、預測與競爭分析