|

市場調查報告書

商品編碼

1906897

工業物聯網(IIoT):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Industrial Internet Of Things (IIoT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

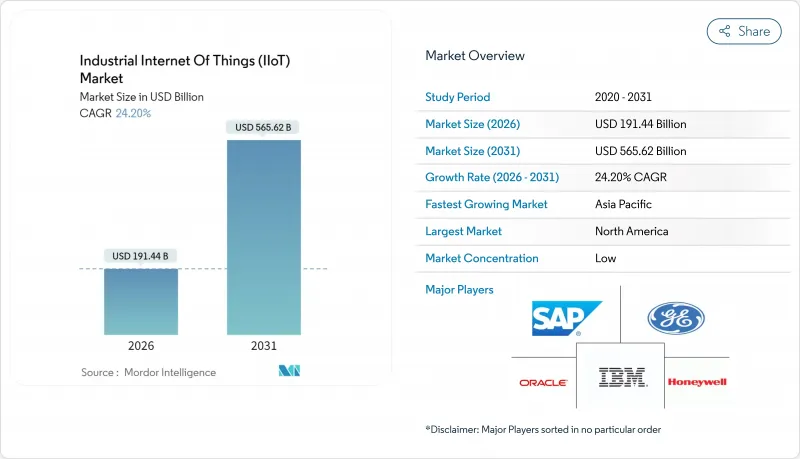

工業物聯網 (IIoT) 市場規模預計將從 2025 年的 1,541.4 億美元成長到 2026 年的 1914.4 億美元,到 2031 年將達到 5,656.2 億美元,2026 年至 2031 年的複合年成長率為 24.2%。

這一成長軌跡反映了感測器價格的快速下降、私有5G的廣泛部署以及基於晶片組的邊緣AI設計,這些設計能夠在營運現場實現即時分析。製造商正在加速採用這些技術,以從被動維護轉向預測性維護,提高整體設備效率(OEE),並緩解供應鏈衝擊。雖然雲端資源對於車隊級分析仍然至關重要,但對於延遲敏感的控制迴路,混合邊緣雲端架構更受歡迎。隨著基於結果的服務模式成為常態,操作技術供應商和雲端超大規模資料中心業者之間的合作日益密切,競爭格局也因此呈現出變化。

全球工業物聯網 (IIoT) 市場趨勢與洞察

先進的感測器整合和更低的設備成本

單元級感測器的價格持續下降,而嵌入式處理器不斷增強神經網路加速功能,使得諸如意法半導體 (STMicroelectronics) 的 STM32N6 MCU 等人工智慧設備無需獨立加速器即可進行現場推理。製造商擴大採用非侵入式感測器覆蓋傳統設備,尤其是在現有工廠中,而不是更換整個系統。低功耗廣域通訊技術(例如 LoRaWAN)將覆蓋範圍擴展到遠端設備,而智慧感測器自診斷功能則將生命週期事件日誌匯總到分析中心。更高的可視性帶來了更高的投資報酬率,並加速了因維修成本而停滯的計劃。因此,工業IoT市場正在吸引更多注重成本的中型工廠,從而擴大基本客群。

促進預測性維護和OEE提升

營運經理將計劃外停機視為策略風險。持續的狀態資料為機器學習模型提供支持,能夠提前數週檢測異常情況,並將計劃外停機時間減少兩位數百分比。振動、熱和聲學特徵使維護團隊能夠專注於優先任務,從而將有限的人力資源釋放出來,用於更高價值的活動。數位雙胞胎疊加技術可以模擬多條生產線的服務場景,從而最佳化備件庫存和技術人員調度。在流程工業中,避免的停機就能避免數百萬美元的生產損失,因此,即使資本支出受到限制,預測系統仍然是預算中的優先事項。

OT網路安全與舊有系統漏洞

在網路出現之前的工業控制設備如今部署在融合網路中,擴大了攻擊面。設備生命週期的延長使得PLC更容易受到未打補丁的攻擊。各部門正在安裝檢驗的物聯網節點,從而創建了繞過中央安全控制的「影子OT」。低程式碼開發平台加速了應用程式的部署,但缺乏管治,它們會導致不安全程式碼的擴散。負責人在權衡生產力提升和網路風險之間做出選擇,通常會推遲聯網升級,直到縱深防禦和零信任框架到位。

細分市場分析

到2025年,硬體將佔工業IoT市場佔有率的46.15%,其中感測器、閘道器和工業用電腦是核心組成部分。感測器和致動器構成狀態監控的基礎,而邊緣閘道則負責預處理遙測資料和管理頻寬。然而,服務和連接方面的複合年成長率將達到25.12%,這凸顯了整合挑戰正在如何重塑採購決策。專業服務團隊正在對現有設備維修,使其符合最新通訊協定,而託管服務正在吸引那些缺乏內部OT-IT人才的中型工廠。

事實上,隨著硬體供應商擴大將設備管理入口網站和遠端監控訂閱服務捆綁銷售,產品和服務之間的界線正變得日益模糊。系統整合商透過運營他們之前部署的基礎設施來獲得持續收入。低程式碼儀表板正逐漸成為主流,使維運團隊無需編寫程式碼即可建立自訂視覺化介面,從而減少對企業IT部門的依賴。因此,工業IoT市場正從一次性資本投資轉向生命週期夥伴關係。

雲端平台憑藉其低廉的初始成本和靈活的分析能力,將在2025年佔據工業IoT市場52.91%的佔有率。然而,純雲環境無法滿足10毫秒以下的控制要求。因此,混合邊緣雲端部署正以25.28%的複合年成長率快速成長。製造商在現場處理振動頻譜和機器視覺幀,並將匯總後的資訊傳輸到雲端,以最佳化其整個設備群。

私有 5G 骨幹網路將透過提供確定性、低延遲的上行鏈路來加速這種融合。容器化的微服務使工程師能夠將 AI 模組放置在計算連續體的任何位置,從而符合製藥和國防等行業的資料主權規則。雖然純本地部署模式仍將在高度監管的細分市場中繼續存在,但混合架構將成為工業IoT市場下一代部署的常態。

區域分析

北美先進的製造業基礎、雄厚的創業融資以及對私有5G試點計畫的早期應用,正推動其在2025年佔據38.36%的市場佔有率。聯邦政府推行的促進製造業回流和增強供應鏈韌性的項目,正在推動對國內供應鏈透明度的需求。法規結構,特別是美國食品藥物管理局(FDA)的流程監控規則,正在推動生命科學工廠的即時品質記錄。

亞太地區正以24.98%的複合年成長率成長,這得益於全球最大的電子生產群集以及政府補貼降低了初始部署成本。中國的一線城市正主導,而印度的技術中心則正向鄰近的東協出口商拓展低成本的整合服務。跨境零件貿易促進了互通解決方案的實現,進一步擴大了工業IoT市場。

歐洲正努力在嚴格的資料隱私法和永續性指令之間尋求平衡。 GDPR推動架構朝向本地邊緣處理發展,而2050年碳中和目標則要求進行詳細的能源計量。德國汽車巨頭正在採用基於TSN的OPC UA進行IT-OT基礎設施整合,這為整個歐洲經濟區提供了一個可供複製的參考模型。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 先進的感測器整合和更低的設備成本

- 促進預測性維護和OEE提升

- 政府主導的智慧製造舉措

- 面向重工業的專用 5G 園區網路

- 基於ESG的能源消費量基準

- 基於晶片組的工業邊緣人工智慧加速器

- 市場限制

- OT網路安全與舊有系統漏洞

- 缺乏跨廠商互通性標準

- 現有系統缺乏數位雙胞胎人才

- 低程式碼物聯網應用會增加影子IT風險

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 投資與資金籌措分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 感測器和致動器

- 邊緣閘道器和工業用電腦

- 工業機器人和控制器

- 軟體

- 設備管理平台

- 分析與視覺化

- MES/SCADA數位雙胞胎軟體

- 服務和連接

- 專業且綜合

- 託管服務

- 連結服務(行動通訊業者、低功耗廣域網路、衛星通訊)

- 硬體

- 按部署模式

- 本地部署

- 雲

- 混合/邊緣雲端

- 透過連接技術

- 有線(乙太網路、PROFINET、Modbus-TCP)

- 短距離無線通訊(BLE、Wi-Fi 6/6E)

- 蜂窩通訊(4G LTE-M、專用 5G)

- LPWAN(LoRa WAN、Sigfox、NB-IoT)

- 按最終用戶行業分類

- 個人作品

- 工藝製造

- 石油和天然氣

- 公共產業(電力、水)

- 運輸/物流

- 採礦和金屬

- 醫療和藥品

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon Web Services Inc.

- Telefonaktiebolaget LM Ericsson

- Fujitsu Ltd.

- Mitsubishi Electric Corporation

- SAP SE

- Siemens AG

- Honeywell International Inc.

- Emerson Electric Co.

- OMRON Corporation

- International Business Machines Corporation

- Robert Bosch GmbH

- Oracle Corporation

- PTC Inc.

- Telit IoT Platforms Limited

- NXP Semiconductors NV

- Cisco Systems Inc.

- Infineon Technologies AG

- Rockwell Automation Inc.

- Advantech Co. Ltd.

- Schneider Electric SE

- ABB Ltd.

- Hitachi Ltd.

- General Electric Company

- Intel Corporation

- Arm Ltd.

第7章 市場機會與未來展望

The industrial internet of things market is expected to grow from USD 154.14 billion in 2025 to USD 191.44 billion in 2026 and is forecast to reach USD 565.62 billion by 2031 at 24.2% CAGR over 2026-2031.

The growth trajectory reflects a sharp decline in sensor prices, wider private-5G roll-outs, and chiplet-based edge-AI designs that allow real-time analytics at the point of operation. Manufacturers are accelerating deployments to move from reactive to predictive maintenance, improve overall-equipment-effectiveness, and cushion supply-chain shocks. Cloud resources remain pivotal for fleet-wide analytics, yet hybrid edge-cloud architectures are being favored for latency-sensitive control loops. Competitive dynamics reveal stronger collaboration between operational-technology vendors and cloud hyperscalers as outcome-based service models become the norm.

Global Industrial Internet Of Things (IIoT) Market Trends and Insights

Integration of Advanced Sensors and Falling Device Costs

Unit-level sensor prices keep falling while embedded processors add neural acceleration, enabling AI-ready devices such as STMicroelectronics' STM32N6 MCU that runs in-situ inference without a discrete accelerator. Manufacturers, especially in brownfield plants, now blanket legacy assets with non-intrusive sensors instead of complete system swaps. Low-power wide-area options like LoRaWAN extend coverage to remote assets, and smart-sensor self-diagnostics feed lifetime event logs into analytics hubs. Expanded visibility drives stronger return-on-investment cases, speeding projects that previously stalled due to retrofit costs. Consequently, the industrial internet of things market enjoys a larger addressable base among cost-sensitive mid-tier factories.

Push for Predictive Maintenance and OEE Improvement

Operations heads see unplanned downtime as a strategic liability. Continuous condition data equips machine-learning models that flag anomalies weeks in advance, cutting unscheduled stoppages by double-digit percentages. Vibration, thermal, and acoustic signatures guide maintenance crews toward prioritized tasks, freeing scarce labor for higher-value assignments. Digital-twin overlays simulate service scenarios across multiple lines, optimizing spare-parts inventory and technician dispatch. In process industries, every avoided shutdown saves millions in lost throughput, explaining why predictive systems draw premium budgets despite capital discipline.

OT Cybersecurity and Legacy System Vulnerabilities

Industrial-control gear that predates the internet now sits on converged networks, enlarging the attack surface. Extended equipment lifecycles mean patches may never be issued, leaving PLCs exposed. Departments sometimes install unvetted IoT nodes, creating "shadow OT", that bypass central security controls. Low-code development platforms accelerate application rollout but, without governance, can propagate insecure code. Operators must weigh production gain against cyber risk, often delaying internet-connected upgrades until layered defenses and zero-trust frameworks are in place.

Other drivers and restraints analyzed in the detailed report include:

- Government-backed Smart-Manufacturing Initiatives

- Private 5G Campus Networks in Heavy Industry

- Lack of Cross-Vendor Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained 46.15% of industrial internet of things market share in 2025, anchored by sensors, gateways, and industrial PCs. Sensors and actuators form the backbone of condition monitoring, while edge gateways pre-process telemetry to manage bandwidth. However, Services and Connectivity is registering a 25.12% CAGR, underlining how integration pain points are reshaping procurement decisions. Professional-service teams retrofit brownfield assets to modern protocols, and managed offerings attract mid-market factories that lack in-house OT-IT talent.

In practice, hardware vendors increasingly bundle device-management portals and remote-monitoring subscriptions, blurring product-service boundaries. Systems integrators earn annuities from operating the infrastructure they once commissioned. As low-code dashboards become mainstream, operational teams build custom visualizations without coding, reducing reliance on enterprise IT. The industrial internet of things market thus gravitates toward life-cycle partnerships rather than one-time capital purchases.

Cloud platforms accounted for 52.91% of industrial internet of things market size in 2025 by offering elastic analytics at lower upfront cost. Yet pure cloud cannot meet sub-10-millisecond control requirements; hence, hybrid edge-cloud deployments are growing at 25.28% CAGR. Manufacturers process vibration spectra or machine-vision frames on-site and forward aggregated insights to the cloud for fleet-level optimization.

Private-5G backbones accelerate this fusion by providing deterministic, low-latency uplinks. Containerized microservices let engineers drop AI modules anywhere along the compute continuum, conforming to data-sovereignty rules in pharmaceuticals and defense. On-premises only models persist in niche, high-regulation niches, but hybrid architectures are expected to become the default for next-generation roll-outs in the industrial internet of things market.

The Industrial Internet of Things Market Report is Segmented by Component (Hardware, Software, and Services and Connectivity), Deployment Model (On-Premises, Cloud, and Hybrid/Edge-Cloud), Connectivity Technology (Wired, Short-Range Wireless, Cellular, and LPWAN), End-User Vertical (Discrete Manufacturing, Process Manufacturing, Oil and Gas, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 38.36% share in 2025 stems from its advanced manufacturing base, strong venture funding, and early adoption of private-5G pilots. Federal programs that incentivize reshoring and resilience amplify demand for visibility across domestic supply chains. Regulatory frameworks, notably FDA process-monitoring rules, push real-time quality logging in life-sciences plants.

Asia Pacific, growing at 24.98% CAGR, benefits from the world's largest electronics production clusters and government subsidies that lower initial deployment costs. China's tier-one cities spearhead large-scale smart factories, while India's tech centers extend low-cost integration services to neighboring ASEAN exporters. Cross-border component trade encourages interoperable solutions, further enlarging the industrial internet of things market.

Europe balances stringent data-privacy laws with sustainability directives. GDPR steers architectures toward local edge processing, and the continent's 2050 carbon-neutral goal mandates granular energy metering. Germany's automotive primes adopt OPC UA over TSN to converge IT-OT backbones, providing reference models replicated across the European Economic Area.

- Amazon Web Services Inc.

- Telefonaktiebolaget LM Ericsson

- Fujitsu Ltd.

- Mitsubishi Electric Corporation

- SAP SE

- Siemens AG

- Honeywell International Inc.

- Emerson Electric Co.

- OMRON Corporation

- International Business Machines Corporation

- Robert Bosch GmbH

- Oracle Corporation

- PTC Inc.

- Telit IoT Platforms Limited

- NXP Semiconductors N.V.

- Cisco Systems Inc.

- Infineon Technologies AG

- Rockwell Automation Inc.

- Advantech Co. Ltd.

- Schneider Electric SE

- ABB Ltd.

- Hitachi Ltd.

- General Electric Company

- Intel Corporation

- Arm Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of advanced sensors and falling device costs

- 4.2.2 Push for predictive maintenance and OEE improvement

- 4.2.3 Government-backed smart-manufacturing initiatives

- 4.2.4 Private 5G campus networks in heavy industry

- 4.2.5 ESG-driven energy-intensity benchmarking

- 4.2.6 Chiplet-based industrial edge AI accelerators

- 4.3 Market Restraints

- 4.3.1 OT cybersecurity and legacy system vulnerabilities

- 4.3.2 Lack of cross-vendor interoperability standards

- 4.3.3 Scarcity of brown-field digital-twin talent

- 4.3.4 Rising shadow-IT risk from low-code IoT apps

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitutes

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Sensors and Actuators

- 5.1.1.2 Edge Gateways and IPCs

- 5.1.1.3 Industrial Robots and Controllers

- 5.1.2 Software

- 5.1.2.1 Device Management Platforms

- 5.1.2.2 Analytics and Visualization

- 5.1.2.3 MES/SCADA and Digital-Twin Software

- 5.1.3 Services and Connectivity

- 5.1.3.1 Professional and Integration

- 5.1.3.2 Managed Services

- 5.1.3.3 Connectivity Services (MNOs, LPWAN, Satellite)

- 5.1.1 Hardware

- 5.2 By Deployment Model

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid/Edge-Cloud

- 5.3 By Connectivity Technology

- 5.3.1 Wired (Ethernet, PROFINET, Modbus-TCP)

- 5.3.2 Short-Range Wireless (BLE, Wi-Fi 6/6E)

- 5.3.3 Cellular (4G LTE-M, Private 5G)

- 5.3.4 LPWAN (LoRa WAN, Sigfox, NB-IoT)

- 5.4 By End-user Vertical

- 5.4.1 Discrete Manufacturing

- 5.4.2 Process Manufacturing

- 5.4.3 Oil and Gas

- 5.4.4 Utilities (Power, Water)

- 5.4.5 Transportation and Logistics

- 5.4.6 Mining and Metals

- 5.4.7 Healthcare and Pharmaceuticals

- 5.4.8 Other End-user Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Fujitsu Ltd.

- 6.4.4 Mitsubishi Electric Corporation

- 6.4.5 SAP SE

- 6.4.6 Siemens AG

- 6.4.7 Honeywell International Inc.

- 6.4.8 Emerson Electric Co.

- 6.4.9 OMRON Corporation

- 6.4.10 International Business Machines Corporation

- 6.4.11 Robert Bosch GmbH

- 6.4.12 Oracle Corporation

- 6.4.13 PTC Inc.

- 6.4.14 Telit IoT Platforms Limited

- 6.4.15 NXP Semiconductors N.V.

- 6.4.16 Cisco Systems Inc.

- 6.4.17 Infineon Technologies AG

- 6.4.18 Rockwell Automation Inc.

- 6.4.19 Advantech Co. Ltd.

- 6.4.20 Schneider Electric SE

- 6.4.21 ABB Ltd.

- 6.4.22 Hitachi Ltd.

- 6.4.23 General Electric Company

- 6.4.24 Intel Corporation

- 6.4.25 Arm Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

工業IoT(IIoT) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能和解決方案分類

工業IoT(IIoT) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能和解決方案分類 2026-2034年全球工業物聯網(IIoT)市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球工業物聯網(IIoT)市場規模、佔有率、趨勢和成長分析報告 4G/5G工業智慧物聯網閘道市場(按組件、連接方式、最終用戶和部署模式分類)-2026-2032年全球預測工業IoT硬體市場按組件類型、連接方式、部署模式、應用和最終用戶產業分類,全球預測(2026-2032年)工業智慧閘道器市場:按產業、連接技術、應用、部署模式和外形規格-全球預測,2026-2032年

4G/5G工業智慧物聯網閘道市場(按組件、連接方式、最終用戶和部署模式分類)-2026-2032年全球預測工業IoT硬體市場按組件類型、連接方式、部署模式、應用和最終用戶產業分類,全球預測(2026-2032年)工業智慧閘道器市場:按產業、連接技術、應用、部署模式和外形規格-全球預測,2026-2032年 工業IoT自動化市場預測至2032年:按組件、部署模式、連接類型、應用、最終用戶和地區分類的全球分析

工業IoT自動化市場預測至2032年:按組件、部署模式、連接類型、應用、最終用戶和地區分類的全球分析 物聯網機器人(IoRT)市場規模、佔有率和成長分析(按組件、平台、應用、最終用戶和地區分類)-2026-2033年產業預測

物聯網機器人(IoRT)市場規模、佔有率和成長分析(按組件、平台、應用、最終用戶和地區分類)-2026-2033年產業預測 工業物聯網 (IIoT) 市場規模、佔有率和成長分析(按部署類型、產品/服務、垂直產業、連接技術和地區分類)—2026-2033 年產業預測新興工業人工智慧生態系統中的全球成長機會:2025-2029 年全球多感官學習與發展套件市場:預測至2032年-按產品類型、組件、技術、分銷管道、應用、最終用戶和地區進行分析

工業物聯網 (IIoT) 市場規模、佔有率和成長分析(按部署類型、產品/服務、垂直產業、連接技術和地區分類)—2026-2033 年產業預測新興工業人工智慧生態系統中的全球成長機會:2025-2029 年全球多感官學習與發展套件市場:預測至2032年-按產品類型、組件、技術、分銷管道、應用、最終用戶和地區進行分析