|

市場調查報告書

商品編碼

1637835

碳酸鈣 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

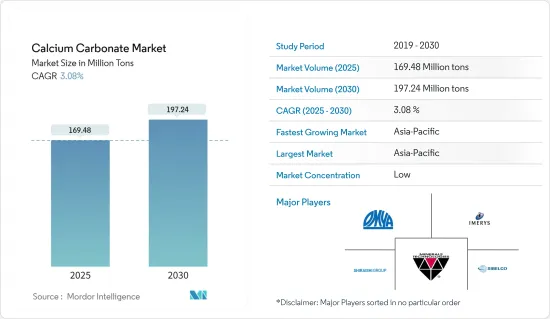

預計2025年碳酸鈣市場規模為1,6948萬噸,預估至2030年將達19,724萬噸,預測期間(2025-2030年)複合年成長率為3.08%。

COVID-19 的爆發以及由此產生的封鎖和社交疏遠規範迫使汽車、建築和其他製造業的各個行業完全關閉。然而,目前市場估計已達到大流行前的水平。

主要亮點

- 從中期來看,推動全球碳酸鈣市場的關鍵因素是亞太地區建設活動的擴大以及造紙業用碳酸鈣取代高嶺土。

- 與碳酸鈣相關的健康危害預計將阻礙預測期內的市場成長。

- 綠色應用的重要性日益增加,預計將為所研究的市場提供新的機會。

- 亞太地區,包括中國、印度和日本等主要消費國,主導全球市場。

碳酸鈣市場趨勢

造紙業主導市場

- 碳酸鈣是造紙工業應用中考慮的基本成分之一,因為它被用作填充材和塗料。 CaCO3 的不透明度、亮度和平滑度等工作特性使其成為生產書寫、印刷和包裝用紙的理想成分。

- 這是一種礦物填料,可顯著降低造紙成本。礦物質比纖維更容易乾燥,這也降低了基礎原料的成本。碳酸鈣也用於紙張塗料,因為它可以為印刷紙表面帶來亮度和光滑度。

- 目前,碳酸鈣在其他造紙填料中佔據主導地位。偏好碳酸鈣的主要原因是對更明亮、更膨鬆的紙張的需求。在鹼性造紙製程中使用 CaCO3 有顯著的優勢。

- 在造紙工業中,碳酸鈣用作高嶺土的替代品。合成沉澱碳酸鈣比高嶺土更亮、更白,許多製造商用於紙張填充和塗層用途。它具有更好的不透明度、光澤度、高亮度和表面光潔度,從而改善印刷適性。

- 碳酸鈣不僅用作高嶺土的替代品,也用於木漿和添加劑中。在鹼性造紙過程中,造紙廠使用碳酸鈣作為填料。碳酸鈣佔造紙用填料和顏料總佔有率的32%。

- 目前,造紙業碳酸鈣的市場需求以亞太地區為主導,以中國為首。對紙包裝和紙巾產品的需求不斷成長預計將推動亞太市場的發展。根據印度造紙工業協會(IPMA)統計,印度造紙業約佔世界紙張產量的4%。該產業預計營業額為 7,000 億印度盧比(84.7456 億美元)(國內市場規模為 8,000 億印度盧比(96.8521 億美元)),財政貢獻約為 500 億印度盧比(6 億美元)。

- 該地區經濟的快速繁榮和食品消費的成長推動了包裝需求。衛生紙的需求是由人口成長和衛生標準提高所推動的。

- 所有上述因素預計將在預測期內推動碳酸鈣的需求。

亞太地區可望主導全球市場

- 由於該地區建設活動的增加,預計亞太地區將引領碳酸鈣市場。

- 隨著該地區建築業的成長,碳酸鈣的需求預計將受到中國、印度和印尼等新興經濟體經濟活動增加和新投資機會的推動。

- 中國是全球最大的製漿造紙生產國,森林蘊藏量佔國土面積的22.5%。工業現代化且高度機械化,勞動廉價。由於政府的植樹造林舉措,中國的森林覆蓋率正在增加。

- 中國是世界上最大的塑膠、黏合劑和密封劑、橡膠、油漆和被覆劑的生產國和消費國。大多數塑膠、黏合劑和密封劑以及油漆和被覆劑都被汽車和建築行業消耗。汽車工業是橡膠的主要消費領域。

- 印度政府的2022年全民住宅計畫也是該產業的重大變革。此外,聯邦內閣核准設立 35.8 億美元的另類投資基金 (AIF),以重振該國主要城市約 1,600 個停滯的住宅計劃。

- 據印度造紙工業協會(IPMA)稱,印度的紙漿和紙張市場繼續以每年6-7%的速度成長,但過去三年產量有所下降。這與穩定成長的消費量形成鮮明對比。

- 總體而言,亞太地區碳酸鈣市場預計將主導全球市場,亞太地區各終端用戶產業的需求不斷增加。

碳酸鈣產業概況

碳酸鈣市場部分整合。該市場的一些主要企業包括 Omya AG、Mineral Technologies Inc.、Imerys、Shiraishi Group 和 Sibelco。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 亞太地區建設活動的成長

- 包裝和造紙工業快速成長

- 在造紙工業中以碳酸鈣取代高嶺土

- 抑制因素

- 與碳酸鈣相關的健康危害

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模(基於數量))

- 類型

- 研磨碳酸鈣 (GCC)

- 沉澱碳酸鈣(PCC)

- 目的

- 建築材料原料

- 營養補充品

- 熱塑性塑膠添加劑

- 填料和顏料

- 黏合劑成分

- 瓦斯脫硫

- 土壤中和劑

- 其他

- 最終用戶產業

- 紙

- 塑膠

- 黏合劑和密封劑

- 建築學

- 油漆/塗料

- 藥品

- 車

- 農業

- 橡皮

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Chemical & Mineral Industries Pvt. Ltd

- FUJIAN SANMU NANO CALCIUM CARBONATE CO. LTD

- GLC Minerals

- Gulshan Polyols Ltd

- Huber Engineered Materials

- Imerys

- Kemipex

- Lhoist

- Maruo Calcium Co. Ltd

- Minerals Technologies Inc.

- Mississippi Lime Company

- Newpark Resources Inc.

- OKUTAMA KOGYO CO. LTD

- Omya AG

- Provale Holding SA

- SCHAEFER KALK GmbH & Co. KG.

- Shiraishi Kogyo Kaisha Ltd

- Sibelco

第7章 市場機會及未來趨勢

- 塑膠和橡膠產業對奈米碳酸鈣的需求不斷成長

- 綠色應用的重要性日益增加

The Calcium Carbonate Market size is estimated at 169.48 million tons in 2025, and is expected to reach 197.24 million tons by 2030, at a CAGR of 3.08% during the forecast period (2025-2030).

The outbreak of COVID-19 and resultant lockdowns and social distancing norms led to the complete shutdown of various industries in the automotive, construction, and other manufacturing segments. However, the market is currently estimated to have reached pre-pandemic levels.

Key Highlights

- Over the medium term, major factors driving the global calcium carbonate market are growing construction activities in the Asia-Pacific region and the replacement of kaolin with calcium carbonate in the paper industry.

- Health hazards associated with calcium carbonate are expected to hinder the market's growth during the forecast period.

- The emerging importance of green applications is expected to provide new opportunities for the market studied.

- The Asia-Pacific region, which includes the major consumption countries, such as China, India, and Japan, dominates the global market.

Calcium Carbonate Market Trends

Paper Sector to Dominate the Market

- Calcium carbonate is one of the essential ingredients considered for applications in the paper industry, as it is employed as fillers and for coating purposes. The working qualities of CaCO3, like opacity, brightness, and smoothness, make it an ideal component for the manufacturing of writing, printing, and packaging-grade paper.

- It is a mineral filler, which substantially reduces the production cost of paper. As the minerals are easier to be dried than fibers, it also reduces the cost of basic materials. Calcium carbonate is also used in paper coating, as it brings out the brightness and smoothness on the surface of printing paper.

- In the present scenario, CaCO3 is dominant over other papermaking filler materials. The main reason behind the preference for calcium carbonate is the demand for brighter and bulkier paper. There are significant advantages to the use of CaCO3 in the alkaline papermaking process.

- In the paper industry, calcium carbonate is used as a replacement for kaolin. Since the synthesized precipitated calcium carbonate is brighter and whiter than kaolin, many manufacturers have been using it for paper filling and coating purposes. It offers better opacity, gloss, high brightness, surface finishing, and improves printability.

- Calcium carbonate is not only used as a substitute for kaolin but also for wood pulp and additives. In the alkaline papermaking process, calcium carbonate is used in a paper mill as a filler material. Calcium carbonate amounts for 32% of the total share of filler and pigments used in paper production.

- Currently, the Asia-Pacific leads the market demand for calcium carbonate in the paper industry, with China being the leading consumer. Increasing demand for paper packaging and tissue products is expected to drive the market in the Asia-Pacific region. According to the Indian Paper Manufacturers Association (IPMA), the Indian paper industry accounts for about 4% of the world's production of paper. The estimated turnover of the industry is INR 70,000 crore (~USD 8,474.56 million) (domestic market size of INR 80,000 crores (~USD 9,685.21 million)), and its contribution to the exchequer is around INR 5,000 crore (~USD 605.33 million).

- The packaging demand is driven by rapid economic upticks and growing food consumption in the region. The tissue demand is driven by population growth and improving hygiene standards.

- All the aforementioned factors are expected to boost the demand for calcium carbonate during the forecast period.

Asia-Pacific Expected to Dominate the Global Market

- The Asia-Pacific region is projected to lead the market for calcium carbonate owing to increasing construction activities in the region.

- Along with the growing construction industry in the region, the demand for calcium carbonate is expected to be driven by increasing economic activities and new investment opportunities in emerging economies, such as China, India, and Indonesia, among others.

- China is the largest pulp and paper producing country in the world, owing to large forest reserves, which amount to 22.5% of the land area. The industry is modern and highly mechanized, and labor is cheap. Forest cover is increasing in China owing to the government's afforestation initiatives.

- China is globally the largest manufacturer and consumer of plastics, adhesives and sealants, rubber, and paints and coatings. The majority of plastics, adhesives and sealants, and paints and coatings are consumed by the automotive and construction industries. The automotive industry is the major consumer of rubber.

- The Indian government's 'Housing for All by 2022' scheme is also a major game-changer for the industry. Additionally, the Union Cabinet has approved the setting up of a USD 3.58 billion alternative investment fund (AIF) in order to revive around 1,600 stalled housing projects across the top cities in the country.

- According to the Indian Paper Manufacturers Association (IPMA), even though India's pulp and paper market has been growing around 6-7% per annum, the industry witnessed a drop in production over the past three years. This contrasts with the consumption, which is exhibiting a steady rise.

- Overall, with the demand increasing from various end-user industries in the region, the Asia-Pacific market for calcium carbonate is projected to dominate the global market.

Calcium Carbonate Industry Overview

The calcium carbonate market is partially consolidated in nature. Some of the major players in the market include Omya AG, Mineral Technologies Inc., Imerys, Shiraishi Group, and Sibelco, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Construction Activities in the Asia-Pacific Region

- 4.1.2 Rapidly Increasing Packaging and Paper Industry

- 4.1.3 Replacement of Kaolin with Calcium Carbonate in Paper Industry

- 4.2 Restraints

- 4.2.1 Health Hazards Associated with Calcium Carbonate

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Ground Calcium Carbonate (GCC)

- 5.1.2 Precipitated Calcium Carbonate (PCC)

- 5.2 Application

- 5.2.1 Raw Substance for Construction Material

- 5.2.2 Dietary Supplement

- 5.2.3 Additive for Thermoplastics

- 5.2.4 Filler and Pigment

- 5.2.5 Component of Adhesives

- 5.2.6 Desulfurization of Fuel Gas

- 5.2.7 Neutralizing Agent in Soil

- 5.2.8 Other Applications

- 5.3 End-user Industry

- 5.3.1 Paper

- 5.3.2 Plastic

- 5.3.3 Adhesives and Sealants

- 5.3.4 Construction

- 5.3.5 Paints and Coatings

- 5.3.6 Pharmaceutical

- 5.3.7 Automotive

- 5.3.8 Agriculture

- 5.3.9 Rubber

- 5.3.10 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Australia and New Zealand

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chemical & Mineral Industries Pvt. Ltd

- 6.4.2 FUJIAN SANMU NANO CALCIUM CARBONATE CO. LTD

- 6.4.3 GLC Minerals

- 6.4.4 Gulshan Polyols Ltd

- 6.4.5 Huber Engineered Materials

- 6.4.6 Imerys

- 6.4.7 Kemipex

- 6.4.8 Lhoist

- 6.4.9 Maruo Calcium Co. Ltd

- 6.4.10 Minerals Technologies Inc.

- 6.4.11 Mississippi Lime Company

- 6.4.12 Newpark Resources Inc.

- 6.4.13 OKUTAMA KOGYO CO. LTD

- 6.4.14 Omya AG

- 6.4.15 Provale Holding SA

- 6.4.16 SCHAEFER KALK GmbH & Co. KG.

- 6.4.17 Shiraishi Kogyo Kaisha Ltd

- 6.4.18 Sibelco

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand from the Plastic and Rubber Industry for Nano-calcium Carbonate

- 7.2 Emerging Importance of Green Applications

2025-2029 年全球碳酸鈣 (CaCO3) 市場

2025-2029 年全球碳酸鈣 (CaCO3) 市場 碳酸鈣市場規模、佔有率、成長分析,按類型、最終用戶、地區 - 按行業預測,2024-2031 年

碳酸鈣市場規模、佔有率、成長分析,按類型、最終用戶、地區 - 按行業預測,2024-2031 年 活性碳酸鈣市場:按類型、應用分類 - 2025-2030 年全球預測

活性碳酸鈣市場:按類型、應用分類 - 2025-2030 年全球預測 碳酸鈣市場:按類型、應用分類 - 2025-2030 年全球預測

碳酸鈣市場:按類型、應用分類 - 2025-2030 年全球預測 全球食品級碳酸鈣市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球食品級碳酸鈣市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 合成碳酸鈣的全球市場:2024年

合成碳酸鈣的全球市場:2024年 碳酸鈣的全球市場的考察,預測(~2030年)

碳酸鈣的全球市場的考察,預測(~2030年) 碳酸鈣市場:按類型、按應用、按地區

碳酸鈣市場:按類型、按應用、按地區 全球研磨碳酸鈣 (GCC) 市場評估:按粒度、按純度等級、按應用、按最終產品、按地區、機會、預測 (2016-2030)

全球研磨碳酸鈣 (GCC) 市場評估:按粒度、按純度等級、按應用、按最終產品、按地區、機會、預測 (2016-2030) 碳酸鈣北美市場規模、佔有率、趨勢分析報告:按產品、應用、地區和細分市場預測,2023-2030

碳酸鈣北美市場規模、佔有率、趨勢分析報告:按產品、應用、地區和細分市場預測,2023-2030