|

市場調查報告書

商品編碼

1851277

北美雷射雷達:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)North America LiDAR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

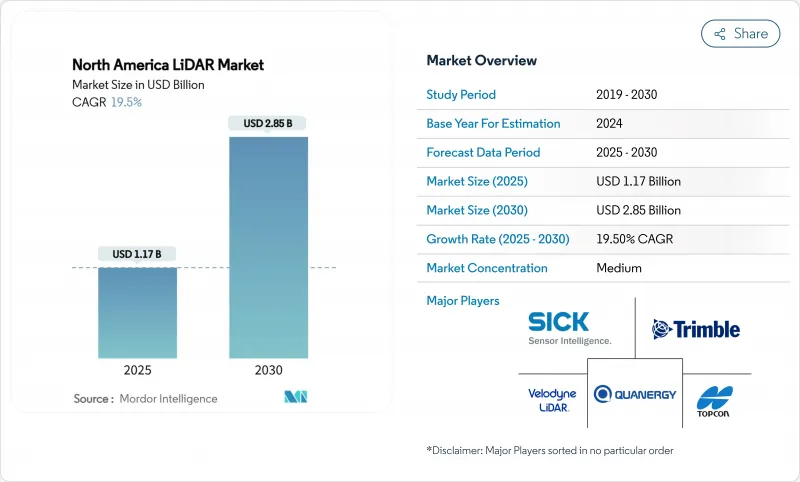

預計到 2025 年,北美LiDAR市場規模將達到 11.7 億美元,到 2030 年將達到 28.5 億美元,年複合成長率為 19.5%。

隨著固態技術的突破性進展縮小了感測器尺寸並降低了成本,聯邦基礎設施項目要求提供精確的資產數據,以及超視距無人機走廊擴大了空中測繪的範圍,市場需求正在加速成長。汽車原始設備製造商(OEM)正在將LiDAR(LiDAR)整合到L3級自動駕駛套件中,林業和公共機構也正在採用這項技術進行野火風險建模和電網巡檢。價格下降、感測器融合技術的創新以及日益成長的環境監測需求將支撐整體兩位數的成長。隨著整合供應商將客製化軟體與晶片級硬體相結合,以在平均售價下降的情況下保護利潤率,市場競爭將更加激烈。

北美LiDAR市場趨勢與洞察

固態LiDAR的整合加速了汽車生產計劃

固態感測器正從有限的試點計畫走向主流量產。 Luminar 為Volvo EX90 提供的系列產品,印證了 OEM 廠商對更高可靠性和更低機械複雜性的信心。 BMW i7 和大眾 ID.Buzz 都整合了 Innoviz 的感測器單元,實現了 L3 級自動駕駛功能;豐田表示,晶片級成本的降低使得中階車型也能採用這項技術。合賽 37% 的全球汽車市佔率凸顯了規模經濟帶來的價格競爭。在北美雷射雷達市場,隨著單價優勢的提升,感測器正被整合到電動皮卡中,以滿足美國聯邦汽車運輸安全管理局 (FMCSA) 對大型車輛自動緊急煞車 (AEB) 的規定。

利用超視距無人機變革基礎設施監控

加拿大運輸部2025年無人機系統(RPAS)法規允許中型無人機進行超視距飛行(BVLOS),從而能夠在偏遠地區以經濟高效的方式進行雷射雷達線路測量製圖。美國聯邦航空管理局(FAA)第107部分豁免條款也反映了這種彈性,並加快了公共工程和鐵路巡檢的進度。美國國家海洋暨大氣總署(NOAA)的高空視距宣傳活動顯示了其運作的成熟度,而商業業者則在電動垂直起降飛行器(eVTOL)上部署輕型掃描儀,單次飛行即可完成數千公里的測繪。由此產生的數據降低了人工巡檢成本,並有助於資產管理人員建立雲端基礎的數位雙胞胎。

成本競爭力問題阻礙了市場滲透。

LiDAR的成本是雷達的三到五倍,這限制了其在售價低於3萬美元的車輛中的應用。 Luminar公司的Halo藍圖旨在將價格降低50%,但主流市場的價格持平不太可能在2028年之前實現。像合賽這樣的中國供應商正透過降低人事費用和垂直整合光學技術來壓縮利潤空間。北美工廠正在透過自動化進行調整,但折舊免稅額機制限制了北美LiDAR市場價格的快速波動。

細分市場分析

到2024年,地面系統將佔北美LiDAR市場收入的42%。對高精度施工樁錨的持續需求支撐著銷售,但該細分市場的成長僅限於兩位數的低點。承包商在拓寬公路或維修橋樑時,將三腳架式設備視為可重複的基準。然而,ClearSkies Geomatics的租賃模式降低了擁有門檻,雖然會壓縮製造商的利潤空間,但會擴大裝置量。

隨著各機構對線性資產數位化,行動和無人機平台以25%的複合年成長率成長。基於RIEGL技術的垂直起降無人機巡檢電力線的速度比地面團隊快10倍,為面臨野火責任風險的公共產業提供支援。 Phase One的整合式相機雷射吊艙可將飛行時間縮短40%,進而提高投資報酬率。隨著檢測公司採用功能強大的慣性測量單元(IMU)來穩定數據,機隊營運商贏得了多年期檢測契約,並帶來了持續的感測器訂單。這種轉變提升了靈活供應商的市場佔有率,並提高了北美雷射雷達市場的業務收益。

到2024年,機械式雷射雷達仍將佔據北美市場63%的佔有率,這得益於其成熟的測量範圍和完善的供應鏈。旋轉鏡設計廣泛應用於公路測繪車和航空測深,在這些應用中,360度全方位覆蓋比耐用性更為重要。然而,維護週期和組裝複雜性會增加生命週期成本。

由於晶圓級光學元件的活動部件較少,固態光學元件的複合年成長率高達22%。京瓷的融合感測器整合了攝影機和LiDAR層,實現了無視差感知。海克斯康的單光子模組每秒可擷取1400萬個數據點,使中高度飛機能夠進行高速走廊掃描。隨著產量的擴大,預計到2028年,其單位成本將與機械式雷射雷達持平,這將為北美LiDAR市場的晶片整合供應商帶來更多設計機會。

北美LiDAR市場按產品(機載LiDAR、地面LiDAR)、類型(機械式LiDAR、固體雷射雷達)、測量範圍、組件(雷射掃描儀、GPS/GNSS接收器等)、應用(線路測量製圖、ADAS和自動駕駛車輛等)、最終用戶(汽車、工程和建設公司等)以及地區進行細分。市場預測以美元計價。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 美國汽車製造商正在迅速將固體雷射雷達整合到L3級自動駕駛汽車專案中。

- 美國聯邦航空管理局超視距飛行豁免加速了加拿大對商用無人機走廊測繪的需求

- 美國老舊交通基礎設施的數位雙胞胎計劃投資激增

- 美國)資助的雷射雷達增強型智慧走廊計劃 (2024-2028)

- 電動卡車製造商迅速採用配備雷射雷達的ADAS系統,以滿足美國聯邦汽車運輸安全管理局(FMCSA)日益嚴格的安全規定。

- 北美林業和環境機構將在2023年特大火災後,利用LiDAR技術進行野火風險建模。

- 市場限制

- 量產型L2+車輛中,雷達/視覺系統仍將維持較高的價格溢價。

- 缺乏熟練的LiDAR數據處理人員導致州運輸部計劃延誤

- 對高性能雷射的出口限制限制了加拿大航太供應商。

- Velodyne-Auster合併後採購不確定性;

- 價值/供應鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 買方/消費者的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 依產品

- 航空LiDAR

- 地面LiDAR

- 移動和無人機雷射雷達

- 按類型

- 機械LiDAR

- 固體雷達

- 按範圍

- 近距離(小於100公尺)

- 中程(100-300公尺)

- 遠距(>300公尺)

- 按組件

- 雷射掃描儀

- GPS/GNSS接收器

- 慣性測量單元(IMU)

- 攝影機和其他感測器

- 透過使用

- 線路測量製圖

- 高級駕駛輔助系統和自動駕駛汽車

- 工程與施工

- 環境與林業

- 安全與執法

- 最終用戶

- 車

- 工程和建設公司

- 工業和公共產業

- 航太/國防

- 聯邦和州政府機構

- 按國家/地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ouster Inc.(incl. Velodyne)

- Teledyne Optech

- Trimble Inc.

- Leica Geosystems AG(Hexagon)

- Innoviz Technologies

- Sick AG

- Topcon Corporation

- LeddarTech Inc.

- Faro Technologies Inc.

- DENSO Corporation

- RoboSense(USA)

- AEye Inc.

- Luminar Technologies Inc.

- Valeo SA

- Quanergy Systems Inc.

- Hesai Technology(NA operations)

- Phoenix LiDAR Systems

- Geo-SLAM Ltd.

- RIEGL Laser Measurement Systems

- MicroVision Inc.

- Neptec Technologies Corp.

- Phantom Intelligence Inc.

- Continental AG

第7章 市場機會與未來展望

The North America LiDAR market is valued at USD 1.17 billion in 2025 and is forecast to reach USD 2.85 billion by 2030, advancing at a 19.5% CAGR.

Demand accelerates as solid-state breakthroughs shrink sensor size and cost, federal infrastructure programs mandate precise asset data, and BVLOS drone corridors expand aerial mapping. Automotive OEMs are locking LiDAR into Level 3 autonomy packages, while forestry and utility agencies adopt the technology for wildfire-risk modelling and grid inspections. Price declines, sensor-fusion innovation, and rising environmental monitoring needs collectively sustain double-digit growth. Competitive intensity rises as consolidated suppliers' pair bespoke software with chip-level hardware to protect margins amid falling average selling prices.

North America LiDAR Market Trends and Insights

Solid-State LiDAR Integration Accelerates Automotive Production Programs

Solid-state sensors are moving from limited pilots into mainstream production programs. Luminar's series supply on Volvo's EX90 confirms OEM confidence in higher reliability and reduced mechanical complexity. BMW's i7 and Volkswagen's ID.Buzz integrate Innoviz units for Level 3 capability, while Toyota reports chip-level cost reductions that open mid-segment adoption. Hesai's 37% global automotive share underscores how scale economics force price competition. As unit economics improve, the North America LiDAR market embeds sensors in electric pickups to satisfy forthcoming FMCSA automatic emergency braking rules for heavy vehicles.

BVLOS Drone Operations Transform Infrastructure Monitoring

Transport Canada's 2025 RPAS regulations authorize medium-sized drones for beyond-visual-line-of-sight operations, enabling cost-effective LiDAR corridor mapping in remote provinces. FAA Part 107 waivers mirror this flexibility south of the border, accelerating utility and rail inspections. NOAA's high-altitude BVLOS campaigns demonstrate operational maturity, while commercial operators deploy lightweight scanners on eVTOL craft to survey thousands of kilometres per flight. Resulting data reduces manual inspection costs and fuels cloud-based digital twins for asset managers.

Cost Competitiveness Challenges Limit Mass-Market Penetration

LiDAR units still cost three to five times more than radar alternatives, deterring inclusion in sub-USD 30,000 vehicles. Luminar's Halo roadmap targets a 50% price cut, yet mainstream parity remains elusive before 2028. Chinese suppliers such as Hesai pressure margins through lower labour costs and vertically integrated optics. North American factories respond with automation, but depreciation schedules constrain rapid price movements in the North America LiDAR market.

Other drivers and restraints analyzed in the detailed report include:

- Digital Twin Infrastructure Projects Drive Long-Term Demand

- Smart-Corridor Initiatives Leverage Federal Infrastructure Funding

- Workforce Development Gaps Constrain Project Execution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ground-based systems held 42% of 2024 revenue in the North America LiDAR market. Continued demand for high-accuracy construction staking anchors sales, yet the segment's growth lags at low-double-digit rates. Contractors value tripod-mounted units for repeatable benchmarks during highway widening and bridge retrofits. However, rental models from ClearSkies Geomatics reduce ownership barriers, trimming manufacturer margins but enlarging the installed base.

Mobile and UAV platforms grow at 25% CAGR as agencies digitize linear assets. RIEGL-based VTOL drones cover transmission lines 10 times faster than terrestrial teams, supporting utilities facing wildfire liability. Phase One's integrated camera-laser pods cut flight hours 40%, enhancing ROI. As survey firms embed robust IMUs to stabilize data, fleet operators win multi-year inspection contracts, feeding sustained sensor orders. This migration boosts share for agile suppliers and elevate service revenues across the North America LiDAR market.

Mechanical architectures still command 63% share of the North America LiDAR market size in 2024 thanks to proven range and established supply chains. Rotating mirror designs service highway mapping vans and airborne bathymetric surveys where 360-degree coverage outweighs durability concerns. Yet maintenance intervals and assembly complexity inflate lifecycle costs.

Solid-state variants post 22% CAGR as wafer-level optics deliver fewer moving parts. Kyocera's fusion sensor merges camera and LiDAR layers for parallax-free perception, attractive to OEMs demanding slimmer housings. Hexagon's single-photon module pushes 14 million points per second, enabling fast corridor scans from mid-altitude aircraft. As volume scales, per-unit cost is projected to reach parity with mechanical peers by 2028, shifting design wins toward chip-integrated suppliers within the North America LiDAR market.

North America LiDAR Market Segmented by Product (Aerial LiDAR, Ground-Based LiDAR), Type (Mechanical LiDAR, Solid-State LiDAR), Range, Component (Laser Scanners, GPS/GNSS Receiver and More), Application (Corridor Mapping and Surveying, ADAS and Autonomous Vehicles, and More), End-User (Automotive, Engineering and Construction Firms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ouster Inc. (incl. Velodyne)

- Teledyne Optech

- Trimble Inc.

- Leica Geosystems AG (Hexagon)

- Innoviz Technologies

- Sick AG

- Topcon Corporation

- LeddarTech Inc.

- Faro Technologies Inc.

- DENSO Corporation

- RoboSense (USA)

- AEye Inc.

- Luminar Technologies Inc.

- Valeo SA

- Quanergy Systems Inc.

- Hesai Technology (NA operations)

- Phoenix LiDAR Systems

- Geo-SLAM Ltd.

- RIEGL Laser Measurement Systems

- MicroVision Inc.

- Neptec Technologies Corp.

- Phantom Intelligence Inc.

- Continental AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid integration of solid-state LiDAR in Level-3 autonomous vehicle programs by U.S. OEMs

- 4.2.2 FAA BVLOS waivers accelerating commercial drone corridor mapping demand in Canada

- 4.2.3 Surging investments in digital-twin projects for aging U.S. transportation infrastructure

- 4.2.4 LiDAR-enriched Smart-Corridor initiatives under U.S. IIJA funding (2024-2028)

- 4.2.5 Early-mover adoption of LiDAR-embedded ADAS by electric-truck makers to meet stricter FMCSA safety mandates

- 4.2.6 North-American forestry and environmental agencies pivoting to LiDAR for wildfire-risk modelling post-2023 mega-fires

- 4.3 Market Restraints

- 4.3.1 Persistent price-premium vs. radar/vision in mass-produced L2+ vehicles

- 4.3.2 Skilled-talent scarcity in LiDAR data processing delaying state-DOT projects

- 4.3.3 Export-control restrictions on high-performance lasers limiting Canadian aerospace suppliers

- 4.3.4 Post-merger procurement uncertainty after Velodyne-Ouster consolidation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Aerial LiDAR

- 5.1.2 Ground-based LiDAR

- 5.1.3 Mobile and UAV LiDAR

- 5.2 By Type

- 5.2.1 Mechanical LiDAR

- 5.2.2 Solid-state LiDAR

- 5.3 By Range

- 5.3.1 Short-range (<100 m)

- 5.3.2 Medium-range (100-300 m)

- 5.3.3 Long-range (>300 m)

- 5.4 By Component

- 5.4.1 Laser Scanners

- 5.4.2 GPS/GNSS Receiver

- 5.4.3 Inertial Measurement Unit (IMU)

- 5.4.4 Camera and Other Sensors

- 5.5 By Application

- 5.5.1 Corridor Mapping and Surveying

- 5.5.2 ADAS and Autonomous Vehicles

- 5.5.3 Engineering and Construction

- 5.5.4 Environmental and Forestry

- 5.5.5 Security and Law Enforcement

- 5.6 By End-User

- 5.6.1 Automotive

- 5.6.2 Engineering and Construction Firms

- 5.6.3 Industrial and Utilities

- 5.6.4 Aerospace and Defense

- 5.6.5 Federal and State Government Agencies

- 5.7 By Country

- 5.7.1 United States

- 5.7.2 Canada

- 5.7.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ouster Inc. (incl. Velodyne)

- 6.4.2 Teledyne Optech

- 6.4.3 Trimble Inc.

- 6.4.4 Leica Geosystems AG (Hexagon)

- 6.4.5 Innoviz Technologies

- 6.4.6 Sick AG

- 6.4.7 Topcon Corporation

- 6.4.8 LeddarTech Inc.

- 6.4.9 Faro Technologies Inc.

- 6.4.10 DENSO Corporation

- 6.4.11 RoboSense (USA)

- 6.4.12 AEye Inc.

- 6.4.13 Luminar Technologies Inc.

- 6.4.14 Valeo SA

- 6.4.15 Quanergy Systems Inc.

- 6.4.16 Hesai Technology (NA operations)

- 6.4.17 Phoenix LiDAR Systems

- 6.4.18 Geo-SLAM Ltd.

- 6.4.19 RIEGL Laser Measurement Systems

- 6.4.20 MicroVision Inc.

- 6.4.21 Neptec Technologies Corp.

- 6.4.22 Phantom Intelligence Inc.

- 6.4.23 Continental AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

LiDAR市場-2026-2032年全球市場預測

LiDAR市場-2026-2032年全球市場預測 LiDAR半導體市場預測至2034年-全球分析(按半導體類型、波長、LiDAR類型、技術、組件整合、最終用戶和地區分類)

LiDAR半導體市場預測至2034年-全球分析(按半導體類型、波長、LiDAR類型、技術、組件整合、最終用戶和地區分類) LiDAR市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。

LiDAR市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。 風力發電雷射雷達系統市場規模、佔有率及成長分析:依系統結構設定、測量方法、主要商業應用、終端用戶產業、通路及地區分類-2026-2033年產業預測

風力發電雷射雷達系統市場規模、佔有率及成長分析:依系統結構設定、測量方法、主要商業應用、終端用戶產業、通路及地區分類-2026-2033年產業預測 風力發電雷射雷達市場-全球產業規模、佔有率、趨勢、機會、預測:依部署方式、應用、技術、範圍、地區和競爭格局分類,2021-2031年光學檢測與測距市場預測至2034年-全球按類型、組件、測量距離、安裝、服務、技術、應用和地區分類的分析

風力發電雷射雷達市場-全球產業規模、佔有率、趨勢、機會、預測:依部署方式、應用、技術、範圍、地區和競爭格局分類,2021-2031年光學檢測與測距市場預測至2034年-全球按類型、組件、測量距離、安裝、服務、技術、應用和地區分類的分析 LiDAR測繪市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶和功能分類

LiDAR測繪市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶和功能分類 2026年全球LiDAR軟體市場報告LiDAR濾光片市場:按濾光片類型、波長、技術、應用和部署分類-2026-2032年全球預測

2026年全球LiDAR軟體市場報告LiDAR濾光片市場:按濾光片類型、波長、技術、應用和部署分類-2026-2032年全球預測 LiDAR技術市場:策略洞察與預測(2026-2031年)

LiDAR技術市場:策略洞察與預測(2026-2031年)