|

市場調查報告書

商品編碼

1639397

亞太地區炭黑 -市場佔有率分析、產業趨勢、成長預測(2025-2030 年)Asia-Pacific Carbon Black - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

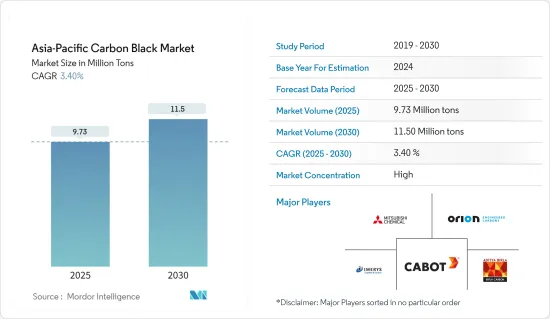

預計2025年亞太地區炭黑市場規模為973萬噸,2030年將達1,150萬噸,預測期間(2025-2030年)複合年成長率為3.4%。

市場受到 COVID-19 的負面影響。受疫情影響,亞太地區多個國家已進入封鎖狀態,以遏止病毒傳播。許多公司和工廠關閉,擾亂了全球供應鏈,影響了生產、交貨時間和產品銷售。目前,市場已從 COVID-19 大流行中恢復並正在顯著成長。

主要亮點

- 紡織業應用的擴大、專門食品炭黑市場滲透率的擴大以及輪胎行業需求的快速成長是推動市場的主要因素。

- 原料價格波動和綠色輪胎的崛起預計將阻礙市場成長。

- 電動和自動駕駛汽車的日益普及以及印刷應用炭黑需求的快速成長將為未來幾年的市場提供機會。

亞太地區炭黑市場趨勢

對輪胎和工業橡膠製品的需求增加

- 橡膠化合物中添加炭黑可改善散熱性能、操控性、胎面磨損和燃油效率。它還具有提高的耐磨性。炭黑主要用作橡膠產業填料,以產生補強效果,例如改變彈性模量和拉伸強度。用於改善產品中的分子間力或內聚力,並賦予橡膠黏合劑、密封劑和被覆劑導電性。

- 汽車產業的表現是炭黑需求的重要指標。根據國際汽車工業協會 (OICA) 的數據,亞太地區的汽車產量到 2022 年將增加 7%,達到 5,000 萬輛,而 2021 年的產量為 4,600 萬輛。

- 中國和印度在亞太地區橡膠和輪胎行業中佔據主導地位。中國是該地區最大的橡膠輪胎生產國和消費國。充足的原料供應和政府的支持措施為這些國家的輪胎和橡膠產業做出了積極貢獻。

- 根據中國橡膠工業協會(CRIA)正式發布的橡膠工業「十四五」發展規劃指引,預計到2025年我國輪胎年產量將達7.04億條。其中,乘用車子午線輪胎5.27億條,卡車、客車子午線輪胎1.48億條,斜交卡車輪胎2900萬條,超大型工業輪胎2萬條,農用輪胎1200萬條,航空輪胎5.4萬條。這一擴張標誌著國際市場對中國輪胎產品的需求不斷成長,使中國輪胎產業成為全球市場的主要參與企業。

- 此外,印度汽車製造業的不斷成長導致各輪胎製造商在該國投資新建生產設施。例如,Yokohama Rubber於2022年4月開始在安得拉邦維沙卡帕特南生產越野輪胎,日產能為69噸橡膠。該公司還正在進行第二階段的擴建,計劃於 2024 年開始,這將使 Nissan 產能增加至 132 噸。

- 因此,考慮到上述因素,預計在預測期內輪胎和工業橡膠製品領域對炭黑的需求將會增加。

中國主導市場

- 中國是亞太市場最大的炭黑消費國。這是由於汽車業對炭黑的需求增加。輪胎應用佔據中國炭黑市場的最大佔有率。

- 中國是亞太地區最大的輪胎生產國。不過,根據國家統計局統計,2022年輪胎產量為8.56億條,與前一年同期比較下降5%。這一下降被認為是由於西方國家能源成本上升和交通量下降導致 2022 年下半年出口需求下降。

- 從積極的一面來看,中國汽車產量顯著成長,有助於該國的輪胎需求。根據OICA統計,2022年中國汽車產量較2021年成長3%。

- 隨著下游需求的增加,中國塗料市場正在快速成長。蓬勃發展的建築、汽車和工業領域預計將推動油漆和塗料市場的發展。反過來,預計這將增加預測期內對炭黑的需求。

- 根據歐洲塗料協會統計,中國有近萬家塗料生產公司。全球領先的塗料製造商大多在中國設有製造地,包括立邦塗料、阿克蘇諾貝爾、中國船舶塗料、PPG工業、BAF SE、艾仕得塗料等。油漆和塗料公司擴大在中國投資。

- 例如,2022年7月,BASF歐洲公司透過子公司BASF塗料(廣東)(BCG)擴大了位於中國南方廣東省江門市的塗料基地的汽車重塗塗料生產能力。透過本次擴建計劃,公司的生產能力已增加到每年30噸。

- 由於各個最終用戶行業的需求不斷增加,炭黑製造商正在建立新的生產設施或擴大現有的生產設施。因此,預計這種趨勢將在未來幾年增加中國對炭黑的需求。

亞太地區炭黑產業概況

亞太炭黑市場具有綜合性。主要企業(排名不分先後)包括卡博特公司、三菱化學集團公司、Orion Engineered Carbons、Imerys 和 Birla Carbon。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 擴大在紡織業的應用

- 提高專門食品炭黑的市場滲透率

- 輪胎產業需求快速成長

- 抑制因素

- 原物料價格不穩定

- 綠色輪胎的興起

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模(基於數量))

- 工藝類型

- 爐黑

- 氣黑

- 燈黑

- 熱感黑

- 目的

- 輪胎及工業橡膠製品

- 塑膠

- 墨粉和印刷油墨

- 塗層

- 纖維

- 其他應用(電力、絕緣、建築等)

- 地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率分析**/排名分析

- 主要企業策略

- 公司簡介

- Birla Carbon

- Bridgestone Corporation

- Cabot Corporation

- Cancarb Limited

- Continental Carbon Company

- Epsilon Carbon Private Limited

- Himadri Specialty Chemical Ltd

- Imerys

- Longxing Chemical Stock Co. Ltd

- Mitsubishi Chemical Group Corporation

- OCI COMPANY Ltd

- Orion Engineered Carbons

- PCBL(Phillips Carbon Black Limited)

- Shandong Huadong Rubber Materials Co., Ltd.

- Tokai Carbon Co. Ltd

第7章 市場機會及未來趨勢

- 電動車和自動駕駛汽車的擴張

- 印刷油墨應用需求快速成長

The Asia-Pacific Carbon Black Market size is estimated at 9.73 million tons in 2025, and is expected to reach 11.50 million tons by 2030, at a CAGR of 3.4% during the forecast period (2025-2030).

The market was negatively impacted due to COVID-19. Owing to the pandemic scenario, several countries in Asia-Pacific went into lockdown to curb the spread of the virus. The shutdown of numerous companies and factories disrupted worldwide supply networks and harmed production, delivery schedules, and product sales. Currently, the market recovered from the COVID-19 pandemic and is increasing significantly.

Key Highlights

- Major factors driving the market studied are growing application in fiber and textile industries, increasing market penetration of specialty black, and surge in demand from the tire industry.

- Volatile raw material prices and the rising prominence of green tires are expected to hinder the studied market's growth.

- Growth in the adoption of electric and self-driving cars and the surge in demand for carbon black in printing applications will likely create opportunities for the market in the coming years.

Asia-Pacific Carbon Black Market Trends

Increasing Demand for Tires and Industrial Rubber Products

- Carbon black improves heat-dissipation capabilities and handling, tread wear, and fuel mileage when added to rubber compounds. It also provides abrasion resistance. Carbon black is mostly used as a rubber sector filler to generate reinforcing effects, such as changing the modulus or tensile strength. It is used to improve the intermolecular or cohesive forces of the product and to provide conductivity to rubber-based adhesives, sealants, and coatings.

- The automotive industry's performance is an important indicator of the demand for carbon black. According to the International Organization of Motor Vehicle Manufacturers (OICA), automotive production in the Asia-Pacific region increased by 7% to 50 million units in 2022, compared to 46 million units recorded in 2021.

- China and India dominate the rubber and tire industry in the Asia-Pacific region. China is the largest producer and consumer of rubber tires in the region. Sufficient availability of raw materials and supporting government initiatives positively contribute to these countries' tire and rubber industries.

- As per the officially released guiding outline for the "14th Five-Year" Development Plan for the Rubber Industry by China Rubber Industry Association (CRIA), China is projected to produce 704 million tires annually by 2025. It includes 527 million passenger radial tires, 148 million truck/bus radial tires, 29 million bias truck tires, 20 thousand extra-large industrial tires, 12 million agricultural tires, and 54 thousand aircraft tires. This expansion suggests the international market's growing demand for China's tire products, positioning China's tire industry as a major player in the global market.

- Furthermore, due to the continuous increase in automotive manufacturing in India, various tire manufacturers are investing in new production facilities in the country. For instance, Yokohama Rubber Co. commenced production of off-road tires in Vishakhapatnam, Andhra Pradesh, in April 2022, with a daily manufacturing capacity of 69 tonnes in rubber weight. The company is also working on the second phase of expansion, expected to begin by 2024, increasing the daily capacity to 132 tonnes.

- Therefore, considering the factors above, the demand for carbon black is expected to rise from the tires and industrial rubber products segment during the forecast period.

China to Dominate the Market

- China is the largest consumer of carbon black in the Asia-Pacific market. It is due to the increasing demand for carbon black from the automotive sector. The tire application accounts for the largest share of the carbon black market in China.

- China is the largest producer of tires in the Asia-Pacific region. However, according to the statistics reported by the National Bureau of Statistics, the production of tires stood at 856 million units in 2022, showcasing a decline of 5% from the previous year. The decline is perceived as a consequence of the reduction in export demand in the second half of 2022 due to the rising energy cost and decline in traffic in Europe and American countries.

- On the positive front, automotive production in China witnessed a prominent rise which aided the demand for tires in the country. According to the OICA, automotive production in China in 2022 increased by 3% compared to 2021.

- The coatings market is growing rapidly in China, with increasing downstream demand. The booming construction, automotive, and industrial sectors will likely propel the paint and coatings market. It, in turn, is expected to boost the demand for carbon black during the forecast period.

- According to European Coatings, nearly 10,000 coatings manufacturers are located in China. Most leading global coating manufacturers, such as Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BAF SE, and Axalta Coatings, contain their manufacturing bases in China. Paints and coatings companies are increasingly growing investments in the country.

- For instance, in July 2022, BASF SE, through its subsidiary BASF Coatings (Guangdong) Co., Ltd. (BCG), expanded its manufacturing capabilities for automotive refinish coatings at its coatings site in Jiangmen, Guangdong Province in South China. The company increased its production capacity to 30 kilotons annually through this expansion project.

- Due to the increasing demand of various end-user industries, carbon black manufacturers are setting up new production facilities and expanding existing manufacturing facilities. Hence, such trends are expected to increase the demand for carbon black in China in the upcoming years.

Asia-Pacific Carbon Black Industry Overview

The Asia-Pacific carbon black market is consolidated in nature. The major companies (in noy any particular order) include Cabot Corporation, Mitsubishi Chemical Group Corporation, Orion Engineered Carbons, Imerys, and Birla Carbon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Application in Fiber and Textile Industries

- 4.1.2 Increasing Market Penetration of Specialty Black

- 4.1.3 Surge in Demand from Tire Industry

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Prices

- 4.2.2 Rising Prominence of Green Tires

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Process Type

- 5.1.1 Furnace Black

- 5.1.2 Gas Black

- 5.1.3 Lamp Black

- 5.1.4 Thermal Black

- 5.2 Application

- 5.2.1 Tires and Industrial Rubber Products

- 5.2.2 Plastics

- 5.2.3 Toners and Printing Inks

- 5.2.4 Coatings

- 5.2.5 Textile Fibers

- 5.2.6 Other Applications (Power, Insulation, Construction, etc.)

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 ASEAN Countries

- 5.3.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Birla Carbon

- 6.4.2 Bridgestone Corporation

- 6.4.3 Cabot Corporation

- 6.4.4 Cancarb Limited

- 6.4.5 Continental Carbon Company

- 6.4.6 Epsilon Carbon Private Limited

- 6.4.7 Himadri Specialty Chemical Ltd

- 6.4.8 Imerys

- 6.4.9 Longxing Chemical Stock Co. Ltd

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 OCI COMPANY Ltd

- 6.4.12 Orion Engineered Carbons

- 6.4.13 PCBL (Phillips Carbon Black Limited)

- 6.4.14 Shandong Huadong Rubber Materials Co., Ltd.

- 6.4.15 Tokai Carbon Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth in the Adoption of Electric Cars and Self-driving Cars

- 7.2 Surge in Demand for Printing Inks Application

全球乙炔炭黑市場:2024年

全球乙炔炭黑市場:2024年 2025-2033 年炭黑市場規模、佔有率、趨勢和預測(按類型、等級、應用和地區分類)

2025-2033 年炭黑市場規模、佔有率、趨勢和預測(按類型、等級、應用和地區分類) 北美炭黑 -市場佔有率分析、產業趨勢、成長預測(2025-2030)

北美炭黑 -市場佔有率分析、產業趨勢、成長預測(2025-2030) 歐洲炭黑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

歐洲炭黑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 炭黑市場規模、佔有率、成長分析,按類型、應用、等級、地區分類 - 產業預測,2024-2031 年

炭黑市場規模、佔有率、成長分析,按類型、應用、等級、地區分類 - 產業預測,2024-2031 年 炭黑市場機會、成長動力、產業趨勢分析及 2025 年至 2034 年預測

炭黑市場機會、成長動力、產業趨勢分析及 2025 年至 2034 年預測 炭黑市場:按類型、等級和應用分類 - 2025-2030 年全球預測

炭黑市場:按類型、等級和應用分類 - 2025-2030 年全球預測 爐用炭黑市場:依等級、應用分類 - 2025-2030 年全球預測

爐用炭黑市場:依等級、應用分類 - 2025-2030 年全球預測 鉛酸電池炭黑市場:按電池類型、等級分類 - 2025-2030 年全球預測

鉛酸電池炭黑市場:按電池類型、等級分類 - 2025-2030 年全球預測 全球炭黑市場:按工藝類型、應用、地區、範圍和預測

全球炭黑市場:按工藝類型、應用、地區、範圍和預測