|

市場調查報告書

商品編碼

1639423

歐洲資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

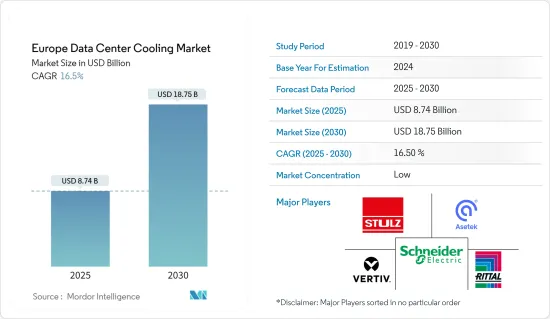

預計 2025 年歐洲資料中心冷卻市場價值將達到 87.4 億美元,預計到 2030 年將達到 187.5 億美元,預測期(2025-2030 年)的複合年成長率為 16.5%。

中小企業擴大採用雲端運算、政府對該地區資料安全的監管以及國內公司不斷成長的投資是推動該地區資料中心冷卻需求的主要因素。

主要亮點

- 冷卻技術的選擇通常是基於資料中心的位置。隨著企業不斷尋求削減成本,節能冷卻方法正被視為傳統冷卻方法的潛在替代方案。此外,邊緣運算的採用和物聯網設備的增加也推動了市場成長。

- 在匈牙利、希臘、波蘭和土耳其等新興歐洲國家, IT基礎設施的發展預計將導致電力容量超過50MW的超大規模資料中心設施建設增加。英國、德國和法國擁有歐洲最多的資料中心,市場參與者可以瞄準這些國家投資新技術。這也將使他們能夠與即將到來的資料中心營運商夥伴關係,以具有市場競爭力的價格滿足市場需求,從而在預測期內促進歐洲資料中心冷卻市場的成長。

- 冷卻系統佔資料中心電力消耗的近40%。公司正嘗試透過建立綠色資料中心來解決這個問題。使用綠色資料中心來儲存、管理和傳遞資訊的趨勢日益成長,這正在幫助許多軟體公司降低能源消費量和整體能源成本。例如,Immersion4 等綠色技術與人工智慧相結合,可以透過實現高效的能源使用和更低的碳足跡來改變資料中心更永續的運作方式。此類綠色資料中心的出現正在推動該地區對冷卻設備的需求。

- 資料中心冷卻系統的安裝需要較高的初始投資,這可能會抑制市場的發展。然而,許多本地供應商和市場先驅正在開發創新解決方案,以低成本改造現有資料中心並降低新設備的安裝成本。此外,減少碳排放和停電期間的冷卻問題可能會阻礙市場成長。

- 由於新資料中心的安裝和現有資料的升級被迫關閉、設備短缺和供應鏈中斷,COVID-19 疫情對市場產生了影響。同時,歐洲國家的資料量和行動資料使用量正在大幅成長,預計將推動整個歐洲資料中心的建立。預計這將在預測期內推動市場成長。預計預測期內政府的支持也將有助於資料中心冷卻市場的發展。

歐洲資料中心冷卻市場趨勢

零售領域可望佔據主要市場佔有率

- 在零售領域,電子商務和線上消費用戶數量的增加預計將產生大量巨量資料,從而推動對資料儲存、安全性和低延遲的需求。這推動了該地區的支出和資料中心數量的增加。零售業的快速發展和工業4.0趨勢也導致了資料中心的興起,增加了對冷卻設備的需求。

- 隨著上網用戶數量的不斷增加,外國零售公司不斷在歐洲國家投資以擴大其儲存容量,從而增加了網路流量和資料中心的壓力。例如,中國電子商務巨頭京東最近確認戰略進軍歐洲零售業。由於該地區的監管嚴格,在該地區投資的外國公司可能會選擇將資料儲存在當地,以緩解資料保護法的過渡。這反過來有望增加資料中心冷卻系統的使用,從而在預測期內推動該地區的市場成長。

- 尤其是,根據電子商務基金會的數據,得益於歐洲網路普及率高,歐洲 B2C 電子商務銷售額預計將成長約 13%,達到 6,210 億美元。巨量資料的數量正在增加,這可能導致該地區資料中心和冷卻系統的增加。

- 據歐盟統計局稱,義大利和波蘭的電子商務用戶數量正在激增。這導致了大量資料的產生和儲存需求的增加。因此,預計歐洲資料中心冷卻市場將在預測期內成長。

英國佔有最大市場佔有率

- 英國的公司正在積極投資新的資料中心,預計這將對預測期內該地區的市場成長產生積極影響。例如,歐洲主機託管和網路公司 Interxion 在倫敦開設了第三個資料中心,擴展了其面向消費者的營運商和 CDN 產品。預計這一發展將提高冷卻系統的利用率,從而推動市場成長。

- 德國時尚零售商 H&M 計劃在其位於斯德哥爾摩的新資料中心引入冷卻和熱回收系統。資料中心產生的多餘熱量將由能源公司 Fortum Varme 分配並重新利用給全市的客戶(滿載時為 2,500 套現代住宅公寓)。

- 英國擁有歐洲最多的資料中心。市場相關人員可以瞄準這些國家投資新技術。我們還可以與新興的資料中心營運商夥伴關係,以具有市場競爭力的價格滿足他們的需求。

- 採用綠色能源、水回收、零水冷卻系統、回收和廢棄物管理等綠色和可再生解決方案來建造最永續的資料中心。包括英國在內的歐洲國家的巨量資料量正在增加,對低延遲、大容量資料中心的需求也日益成長,預計這將導致冷卻系統的利用率提高。據Science Direct稱,預測期內資料中心的能源使用量可能佔全球電力供應的2.13%。

- 各行各業的公司都在努力降低營運成本,並擴大在全國各地的資料中心冷卻系統中使用人工智慧技術。例如,西門子推出了基於人工智慧的熱最佳化,利用 Vigilant AI 產品來增強資料中心冷卻系統。

歐洲資料中心冷卻產業概況

歐洲資料中心冷卻市場比較分散,技術帶來的好處以及政府透過對資料中心實施效率法規的支持預計將推動資料中心冷卻市場的成長。主要市場參與者包括 IBM 公司、富士通有限公司、日立有限公司、惠普企業和Schneider ElectricSE。隨著主要參與者在現有市場中的強勢存在,市場滲透率正在不斷提高。對創新的日益關注推動了對新技術的需求,這反過來又刺激了對其進一步發展的投資。

- 2024 年 5 月 Rittal 與多家超大規模資料中心營運商合作開發了模組化冷卻系統。該解決方案透過直接水冷實現超過1MW的冷卻能力。專門針對高功率密度 AI 應用進行調整。

- 2024 年 1 月 Aligned 資料 Centers 是一家技術基礎設施公司,為全球超大規模和企業客戶提供永續、創新和適應性強的資料中心和按規模建立解決方案。項正在申請專利的解決方案,旨在支援密集的運算要求次世代應用程式和高效能運算,包括人工智慧、機器學習和超級電腦。 DeltaFlow 擴展了 Aligned 的 ExpandOnDemand 功能,為客戶提供了無縫擴展和調整的靈活性,以支援不斷變化的運算環境。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況(範圍:包括與資料中心冷卻相關的當前區域趨勢的詳細分析)

- 冷卻的主要成本考量

- 分析與資料中心營運相關的主要成本開銷,重點關注資料中心冷卻

- 資料中心冷卻的關鍵創新和發展

- 資料中心採用的主要節能技術

第5章 市場動態

- 市場促進因素(關鍵因素包括日益關注能源消耗和轉向綠色解決方案,這些因素基於未來 5-7 年的相對影響進行繪製)

- 市場動態(監管的動態性質和不斷變化的客戶需求等關鍵因素將根據其在未來 5-7 年內的相對影響進行繪製)

- 市場機會

- 封閉式與非封閉式架空地板

- 產業生態系統分析

6. 區域資料中心足跡現況分析

- 資料中心 IT 負載能力與麵積分佈區域分析(2017-2030 年)

- 歐洲成熟和新興資料中心熱點區域分析(重點介紹主要成熟和新興資料中心市場,以實現全面覆蓋)

- 直流冷卻法規結構的區域分析

第 7 章資料中心冷卻市場細分

- 依冷卻技術分類(主要趨勢、2022-2029 年市場規模估計與預測、未來展望)

- 空氣冷卻

- CRAH

- 冷卻器和節熱器

- 冷卻塔(涵蓋直接冷卻、間接冷卻及雙級冷卻)

- 其他

- 液體冷卻

- 浸入式冷卻

- 晶片直接冷卻

- 後門式熱交換器

- 空氣冷卻

- 按行業

- 資訊科技和電信

- 零售和消費品

- 衛生保健

- 媒體與娛樂

- 聯邦政府

- 其他最終用戶

- 按國家

- 英國

- 德國

- 俄羅斯

- 丹麥

- 挪威

- 荷蘭

- 西班牙

- 波蘭

- 瑞士

- 奧地利

- 比利時

- 法國

- 義大利

- 愛爾蘭

- 瑞典

第8章 競爭格局

- 公司簡介

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Asetek A/S

- Alfa Laval AB

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air Conditioning Ltd

第9章投資分析

第10章 市場機會與未來趨勢

The Europe Data Center Cooling Market size is estimated at USD 8.74 billion in 2025, and is expected to reach USD 18.75 billion by 2030, at a CAGR of 16.5% during the forecast period (2025-2030).

The growing adoption of cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data center cooling in the region.

Key Highlights

- Cooling technologies are usually selected based on the data centers' geographical location. As companies regularly seek to mitigate costs, energy-efficient cooling methods are being considered the potential alternatives to traditional cooling methods. The market's growth is also fueled by edge computing adoption and the increase in IoT devices.

- Developments in IT Infrastructure in emerging European countries such as Hungary, Greece, Poland, and Turkey are expected to increase the construction of hyperscale data center facilities with over 50 MW power capacity. The United Kingdom, Germany, and France had the highest number of data centers across Europe, and market players can target these countries to invest in their new technologies. Also, they can form partnerships with upcoming data center organizations to cater to market requirements at a competitive price, aiding the growth of the European data center cooling market over the forecast period.

- The cooling systems are responsible for almost 40% of the data center power consumption. Companies are trying to tackle this issue by setting up green data centers. The growing trends toward deploying green data centers for storing, managing, and distributing information have helped many software companies reduce energy consumption and total energy costs. For example, green technologies, such as Immersion4 in combination with AI, are changing how data centers operate to make them more sustainable with efficient energy usage and low carbon footprint. Such green data centers' emergence drives the demand for cooling units in the region.

- Data center cooling systems require a high initial investment to set up, which could restrain the market. However, many local vendors and market players are developing innovative solutions by modifying the existing data centers at a low cost to reduce the cost of setting up a new unit. Additionally, reduced carbon emission and cooling issues during power outages could hamper the growth of the market.

- The COVID-19 pandemic impacted the market owing to lockdowns, shortage of devices, and supply chain disruptions to set up new data centers and update the existing data centers. On the other hand, there is a massive rise in data volume and mobile data usage in European countries, which is anticipated to boost the setup of data centers across Europe. This will propel the market growth over the forecast period. Also, government support is projected to boost the development of the data center cooling market over the forecast period.

Europe Data Center Cooling Market Trends

The Retail Segment is Expected to Hold a Significant Market Share

- In the retail segment, the increasing number of users in e-commerce and online spending is creating an enormous volume of Big Data, which is expected to propel the need for data storage, security, and reduced latency. This boosts the region's expenditure and the number of data centers. Rapid development in the retail sector and Industry 4.0 trends are also responsible for the rise of data centers, enhancing the need for cooling devices.

- Due to the increasing number of online users, foreign retail companies regularly invest in European countries to expand their storage capacity, increasing internet traffic and the load on data centers. For instance, JD.com, a Chinese e-commerce giant, recently confirmed a strategic entry into the European retail sphere. Due to stringent regulations in the region, foreign companies investing in the area may store their data locally for smooth transitions regarding the data protection law. As a result, the usage of data center cooling systems is expected to increase, thereby boosting the market growth in the region over the forecast period.

- Notably, according to the E-commerce Foundation, the European B2C e-commerce turnover is expected to expand by approximately 13% to reach USD 621 billion due to the high internet penetration in the region. It may increase the Big Data volume, leading to more data centers and cooling systems in the area.

- According to Eurostat, Italy and Poland witnessed tremendous growth in e-commerce users. It led to the generation of a vast amount of data, thereby strengthening storage requirements. As a result, the European data center cooling market is expected to grow over the forecast period.

The United Kingdom Accounts For the Largest Market Share

- Companies in the UK are rigorously investing in new data centers, and this is expected to positively impact the market growth in the region over the forecast period. For instance, Interxion, a European colocation and networking company, commenced its third data center in London, expanding carriers and CDNs for consumers. This development is expected to propel cooling system utilization and foster market growth.

- H&M, a fashion retailer in the country, plans to integrate a cooling and heat recovery system in its new data center in Stockholm. The excess heat generated from the data center is reused by Fortum Varme, an energy company, by distributing it to customers (2,500 modern residential apartments at full load) throughout the city.

- The UK recorded the highest number of data centers across Europe. Market players can target these countries to invest in their new technologies. Also, they can form partnerships with upcoming data center organizations to cater to their requirements at a competitive price, which may aid the growth of the European data center cooling market over the forecast period.

- Green and renewable solutions, such as green electricity, water reclamation, zero water cooling systems, recycling, and waste management, are being used to build the most sustainable data centers. Growth in Big Data volume across European countries, including the United Kingdom, is expected to increase the need for low-latency and high-capacity data centers, thereby boosting cooling system utilization. According to Science Direct, data center energy use might account for 2.13% of worldwide electricity supply over the forecast period.

- Companies are regularly trying to reduce their operational cost across their verticals, increasing the AI technology used in data center cooling systems in the country. For instance, Siemens introduced AI-based thermal optimization, wherein the company utilizes Vigilant AI products to enhance cooling systems in data centers.

Europe Data Center Cooling Industry Overview

The European data center cooling market is fragmented as the benefits offered by the technology and support from the government by imposing efficiency regulations on data centers are expected to help the growth of the data center cooling market. Some major market players are IBM Corporation, Fujitsu Ltd, Hitachi Ltd, Hewlett-Packard Enterprise, and Schneider Electric SE. Market penetration is growing with a strong presence of major players in established markets. With the increasing focus on innovation, the demand for new technologies is growing, which, in turn, is driving investments for further developments.

- May 2024: Rittal, in collaboration with multiple hyperscale data center operators, developed a modular cooling system. This solution boasts a cooling capacity exceeding 1 MW, achieved through direct water cooling. It is specifically tailored to cater to the high-power densities of AI applications.

- January 2024: Aligned Data Centers, the technology infrastructure company providing sustainable, innovative, and adaptive scale data centers and build-to-scale solutions for global hyperscale and enterprise customers, introduced its DeltaFlow liquid cooling technology, a patent-pending solution built to support the high-density compute requirements of next-generation applications and high-performance computing, including artificial intelligence, machine learning, and supercomputers. DeltaFlow extended Aligned's ExpandOnDemand capabilities, providing customers the flexibility to seamlessly scale and pivot to support shifting computing environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (Coverage: A detailed analysis of the current regional trends related to Data Center Cooling are included in this section)

- 4.2 Key cost considerations for Cooling

- 4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

- 4.2.2 Key innovations and developments in Data Center Cooling

- 4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

- 5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

- 5.3 Market Opportunities

- 5.4 Comparison of raised floor with containment & raised floor without commitment

- 5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT REGIONAL DATA CENTER FOOTPRINT

- 6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Regional Analysis of the Established DC Markets and Emerging DC Hotspots in Europe region (we will include coverage by highlighting major established and emerging DC markets)

- 6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 DATA CENTER COOLING MARKET SEGMENTATION

- 7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)

- 7.1.1 Air-based Cooling

- 7.1.1.1 CRAH

- 7.1.1.2 Chiller and Economizer

- 7.1.1.3 Cooling Tower (covers direct, indirect & two-stage cooling)

- 7.1.1.4 Others

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-Chip Cooling

- 7.1.2.3 Rear-Door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By End-user Vertical

- 7.2.1 IT & Telecom

- 7.2.2 Retail & Consumer Goods

- 7.2.3 Healthcare

- 7.2.4 Media & Entertainment

- 7.2.5 Federal & Institutional agencies

- 7.2.6 Other End Users

- 7.3 By Country

- 7.3.1 United Kingdom

- 7.3.2 Germany

- 7.3.3 Russia

- 7.3.4 Denmark

- 7.3.5 Norway

- 7.3.6 Netherlands

- 7.3.7 Spain

- 7.3.8 Poland

- 7.3.9 Switzerland

- 7.3.10 Austria

- 7.3.11 Belgium

- 7.3.12 France

- 7.3.13 Italy

- 7.3.14 Ireland

- 7.3.15 Sweden

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Vertiv Group Corp.

- 8.1.2 Stulz GmbH

- 8.1.3 Schneider Electric SE

- 8.1.4 Rittal GmbH & Co. KG

- 8.1.5 Asetek A/S

- 8.1.6 Alfa Laval AB

- 8.1.7 Iceotope Technologies Limited

- 8.1.8 Green Revolution Cooling Inc.

- 8.1.9 Chilldyne Inc.

- 8.1.10 Airedale International Air Conditioning Ltd

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

整合式機架安裝單元 (CDU) 市場:按階段、容量、應用和最終用戶分類的全球預測,2026-2032 年資料中心CDU市場:按類型、組件、冷卻方式、容量、應用工作負載、最終用途、企業規模、安裝方式、分銷管道分類,全球預測,2026-2032年

整合式機架安裝單元 (CDU) 市場:按階段、容量、應用和最終用戶分類的全球預測,2026-2032 年資料中心CDU市場:按類型、組件、冷卻方式、容量、應用工作負載、最終用途、企業規模、安裝方式、分銷管道分類,全球預測,2026-2032年 資料中心冷卻市場:依組件、冷卻技術、資料中心類型和行業劃分 - 全球預測至2036年

資料中心冷卻市場:依組件、冷卻技術、資料中心類型和行業劃分 - 全球預測至2036年 資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2026-2032)

資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2026-2032) 節水型資料中心技術市場,全球預測至2034年:依冷卻技術、水源、水處理方法、所有權模式及地區分類

節水型資料中心技術市場,全球預測至2034年:依冷卻技術、水源、水處理方法、所有權模式及地區分類 2026年全球資料中心冷卻市場報告

2026年全球資料中心冷卻市場報告 全球資料中心冷卻市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球資料中心冷卻市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 資料中心冷卻系統市場 - 全球產業規模、佔有率、趨勢、機會與預測:冷卻策略、最終用途類型、服務、最終用戶產業、地區和競爭格局,2021-2031年

資料中心冷卻系統市場 - 全球產業規模、佔有率、趨勢、機會與預測:冷卻策略、最終用途類型、服務、最終用戶產業、地區和競爭格局,2021-2031年 資料中心冷卻市場規模、佔有率和趨勢分析報告:按組件、類型、污染物、結構、應用、地區和細分市場預測(2026-2033 年)資料中心以氟化冷媒市場:按產品類型、冷卻技術、分銷管道和最終用戶分類 - 全球預測(2026-2032 年)

資料中心冷卻市場規模、佔有率和趨勢分析報告:按組件、類型、污染物、結構、應用、地區和細分市場預測(2026-2033 年)資料中心以氟化冷媒市場:按產品類型、冷卻技術、分銷管道和最終用戶分類 - 全球預測(2026-2032 年)