|

市場調查報告書

商品編碼

1640422

積層製造與材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Additive Manufacturing and Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

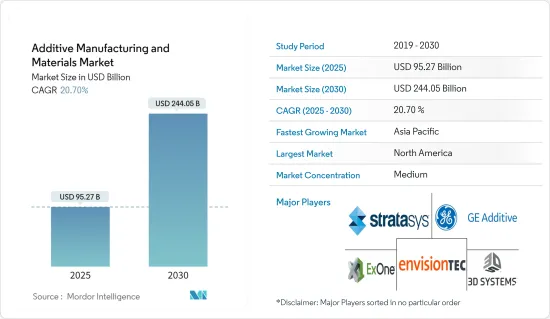

積層製造和材料市場規模在2025年預估為952.7億美元,預計到2030年將達到2,440.5億美元,預測期間(2025-2030年)的複合年成長率為20.7%。

如今,各種規模的製造商都積層製造視為其工廠的重要組成部分。積層製造使產業能夠生產重新設計的成品,這些成品更堅固、更輕、零件更少,同時也能克服供應鏈中斷的問題。

主要亮點

- 工業3D列印技術對於工廠實現即插即用運作至關重要。根據 Sculpteo 的調查,41% 的公司確認積層製造改善了他們的流程,使他們能夠更有效率地完成任務。受近期生物基材料興起的推動,59% 的用戶希望使用更多永續材料。同時,47% 的 3D 列印減少了對多種資源的需求,因為有些設計透過傳統技術是「不可能實現的」。

- 積層製造廣泛應用於許多產業,航太業是最早採用 3D 列印的產業之一。在醫療保健領域,3D 列印用於醫療設備和牙科的假牙、嵌體和其他植入。為了進一步發展 3D 列印,影像處理方法將測量患者的膝蓋或下巴,並將所需植入的 CAD 設計直接髮送到 3D 列印機,印表機將立即開始生產。

- 新冠疫情讓 3D 列印得以應對挑戰。該技術可以快速生產 3D 列印口罩和防護罩。隨著新的 3D 列印材料、機器和積層製造技術進入市場,擁有 3D 列印架構專業知識的公司可以擴展其服務,因為產業正在向他們尋求創新技術。

- 總部位於英國的本特利汽車公司已向 3D 列印領域投資 300 萬美元。此項投資用於多噴射熔合技術和 FDM 機器。基於粉末的技術使該汽車製造商能夠在一天半的時間內生產出批量的零件,比同行提高了生產率。

積層製造和材料市場趨勢

汽車業預計將佔很大佔有率

- 3D 列印在生產最終汽車零件方面非常有用。大眾、寶馬和福特等汽車製造商使用積層技術來製造其汽車的最終零件。熔融長絲製造技術 (3F 或 FFF) 是 3D 列印領域的最新進展,人們正在探索一系列具有與塑膠相似特性的材料。 3D 列印使公司能夠創建所需的零件和設計,從而無需依賴外部供應商,使其生產過程更加高效。

- 積層製造可以實現無工具生產,並且具有幾乎無限的設計靈活性。例如,福特汽車使用3D列印技術來生產零件。該公司整合AI和3D技術來增強其業務能力。 2022年3月,該公司開發了操作3D列印機的機器人系統。此介面將使來自不同供應商的機器能夠使用相同的語言並自主操作生產線的各個部分。

- 通用汽車計劃在2035年實現其所有車型零排放。積層製造在設計複雜零件、輕量化車輛和提高電池性能方面發揮關鍵作用。當通用汽車遇到交付2022 年雪佛蘭 Tahoe 所需零件生產中斷時,它轉向了惠普的 3D 列印平台。在轉用惠普的多射流熔融 (MJF) 3D 列印技術後,通用汽車能夠縮短乾燥時間並加快其全尺寸 SUV 的生產進度。在五週的時間裡,他們成功生產並打磨了約30,000輛汽車所需的60,000個零件。

預計亞太地區將出現顯著成長

- 作為「中國製造2025」策略的一部分,中國設定了提高工業競爭力的目標。我們透過投資 3D 列印等最尖端科技和培養未來的勞動力來實現這一目標。根據Materialise對中國製造企業所做的調查,30%的企業同意3D列印的使用將變得比傳統製造業更重要。

- 中國航空業已開始在其下一代軍用飛機中使用尖端的 3D 列印技術,其中 3D 列印零件已用於製造最近首飛的飛機。

- 3D生物列印技術由韓國浦項科技大學(POSTECH)開發,用於列印逼真的人造器官。據該研究所稱,3D 列印與人工智慧和機器人技術相結合,可實現更自動化、更複雜的替代器官生成方式。

- 日本企業集團 JGC Holdings Corporation 引進了 COBOD 3D 列印機用於建築工程。採用COBOD技術,可顯著減少模板施工所需的時間。該公司計算得出,3D 列印可以將這一過程從 16 天縮短至 8 天。

積層製造和材料產業概況

積層製造和材料市場競爭激烈。擁有巨大市場佔有率的領先公司正專注於開發 3D 列印技術的衍生設計能力。透過採用針對積層製造最佳化的軟體功能,這些公司希望擴大其在國際市場的基本客群,並利用策略合作舉措來增加市場佔有率和盈利。 Stratasys、ExOne 和 3D Systems Corporation 是服務該行業的一些主要公司。

- 2022 年 8 月-聚合物 3D 列印公司 Stratasys 收購科思創股份公司 (Covestro AG),積層製造和材料業務提供支援。這種創新材料非常適合 3D 列印的新使用案例,特別是用於生產牙齒矯正器和汽車零件等最終用途零件。此次收購使 Stratasys 能夠推進其策略,提供業界最好、最完整的聚合物 3D 列印產品組合。這也使我們能夠加快對 3D 列印材料尖端開發的投資。

- 2022 年 8 月-Carbon 收購積層製造軟體供應商 ParaMatters。此次收購將使 Carbon 的產品開發團隊能夠使用該軟體的自動化技術在更短的時間內創造出更高效能的零件設計。這些設計具有先進的幾何形狀和改進的性能特徵。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場動態

- 市場促進因素

- 新技術和改進技術推動產品客製化

- 汽車和航太工業對輕量化結構的需求

- 市場限制

- 對智慧財產權保護的擔憂

第6章 市場細分

- 依技術分類

- 立體光刻技術

- 熔融沉積建模

- 雷射燒結

- 黏著劑噴塗列印

- 其他技術

- 按最終用戶

- 航太和國防

- 車

- 衛生保健

- 產業

- 其他最終用戶

- 按材質

- 塑膠

- 金屬

- 陶瓷

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 以色列

- 南非

- 其他中東和非洲地區

- 北美洲

第7章 競爭格局

- 公司簡介

- 3D Systems Corporation

- General Electric Company(GE Additive)

- EnvisionTEC GmbH

- EOS GmbH

- Exone Company

- Mcor Technologies Ltd

- Materialise NV

- Optomec Inc.

- Stratasys Ltd

- SLM Solutions Group AG

第8章投資分析

第9章:市場的未來

The Additive Manufacturing and Materials Market size is estimated at USD 95.27 billion in 2025, and is expected to reach USD 244.05 billion by 2030, at a CAGR of 20.7% during the forecast period (2025-2030).

Production companies of all sizes currently view Additive Manufacturing as an essential component of their factories. With additive manufacturing, industries can manufacture finished goods that are stronger, lighter, and redesigned to have fewer parts while overcoming supply chain interruption.

Key Highlights

- Industrial 3D printing technology is essential for factories to operate in plug-and-play mode. According to a survey by Sculpteo, 41% of the companies confirm that Additive Manufacturing has helped them complete their task more efficiently while improvising their process. 59% of users desire to use more sustainable materials, driven by the increasing number of bio-based materials in recent years. At the same time, 47% of 3D printing reduces the need for multiple resources because some designs are 'impossible' to achieve using traditional techniques.

- Additive Manufacturing is used widely in many industries, and the aerospace industry was the first to embrace 3D printing. In healthcare, medical devices and dentistry use 3D printing in items such as dental prostheses, inlays, and other implants. For further developments in 3D printing, imaging methods will measure the patient's knee or jaw and then send a CAD blueprint of the required implant directly to the 3D printer, which will immediately start building it.

- The Covid-19 pandemic allowed 3D printing to rise to the challenge. The rapid production of 3D-printed face masks and shields was possible using this technology. When new 3D printing materials, machines, and additive manufacturing techniques enter the market, companies proficient in 3D printing architectures can expand their services as the industries will approach them for innovative skills.

- UK-based Bently Motors adopted 3D printing with an investment of 3 million USD. This investment was used in multi-jet fusion technology and FDM machines. With powder-based technology, the automotive player could manufacture a batch of parts in a day and a half, thereby increasing its productivity compared to its counterparts.

Additive Manufacturing Materials Market Trends

Automotive to is expected Hold a Significant Share

- 3D printing is very helpful in manufacturing the final car parts. Automotive players like Volkswagen, BMW, and Ford use additive technology to manufacture final car parts. Fused Filament Fabrication (3F or FFF) is the latest improvement in 3D printing, where different materials are examined to have properties similar to plastics. With a 3D printer, the required parts and designs can be created, which makes the companies independent of external suppliers and further streamlines the production processes.

- Additive Manufacturing allows for toolless production with almost endless design flexibility. For instance, Ford Automotive uses 3D printing technology for production parts. The company is integrating AI with 3D technology to enhance its business capabilities. In March 2022, the automotive leader developed a robotic system to operate 3D printers. This interface allows machines from different suppliers to speak to each other in the same language and operate parts of the production line autonomously.

- General Motors plans to turn its entire fleet into zero-emission vehicles by 2035. Additive Manufacturing plays a vital role in designing intricate parts and lightweight vehicles with extended battery performance. When General Motors faced hindrances in producing a component needed to deliver the 2022 Chevrolet Tahoe, it turned to HP's 3D printing platform. After switching to HP's Multi Jet Fusion (MJF) 3D printing technology, GM was able to reduce the drying time, which sped up the manufacturing schedule for full-sized SUVs. Over five weeks, the necessary 60,000 parts for about 30,000 vehicles were successfully made and polished.

Asia Pacific is expected to witness significant growth rate

- China has set targets to increase industrial competitiveness as part of its Made in China 2025 strategy. They will do this by investing in cutting-edge technologies, like 3D printing, and preparing the future workforce. A survey conducted by Materialise among Chinese manufacturing companies stated 30% of companies agree that the use of 3D printing that will become more important than traditional manufacturing.

- China's aviation sector has begun using cutting-edge 3D printing technologies on next-generation warplanes, with 3D printed components being used to construct aircraft that had their maiden flight recently.

- The 3D bio-printing technique was developed by the Pohang University of Science and Technology (POSTECH) in South Korea for realistic engineered organs. As per the research institute, more automatized and elaborate methods for generating organ substitutes would be possible if 3D printing is integrated with AI and robotic technologies.

- JGC Holdings Corporation, a Japanese conglomerate, installed COBOD 3D printer in its construction work. Adopting COBOD technology will drastically reduce formwork construction time. The firm calculated that 3D printing might have cut this process from 16 days down to eight.

Additive Manufacturing Materials Industry Overview

The additive manufacturing and materials market is quite competitive. The major players with a significant market share are concentrating on developing generative design capabilities for 3D printing techniques. By adopting software capabilities optimized for additive manufacturing, companies want to increase their customer bases across international markets and utilize strategic collaborative initiatives to increase their market share and profitability. Stratasys, ExOne, and 3D Systems Corporation are some of the major players serving this industry.

- August 2022 - The polymer 3D printing company Stratasys acquired Covestro AG, which supports the additive manufacturing materials business. Innovative materials are proficient in creating new use cases for 3D printing, particularly in producing end-use parts like dental aligners and automotive components. Through this acquisition, Stratasys can advance its business strategy of providing the industry's best and most complete polymer 3D printing portfolio. The company can also accelerate its investments in cutting-edge developments in 3D printing materials.

- August 2022 - Carbon acquired ParaMatters, which provides software for additive manufacturing. The acquisition will help the product development teams of Carbon to create higher-performance part designs in less time using automation techniques of this software. These designs will feature advanced geometries and improved performance characteristics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMNICS

- 5.1 Market Drivers

- 5.1.1 New and Improved Technologies to Drive Product Customization

- 5.1.2 Demand for Lightweight Construction in Automotive and Aerospace Industries

- 5.2 Market Restraints

- 5.2.1 Concerns over Intellectual Property Protection

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Stereo Lithography

- 6.1.2 Fused Deposition Modelling

- 6.1.3 Laser Sintering

- 6.1.4 Binder Jetting Printing

- 6.1.5 Other Technologies

- 6.2 By End User

- 6.2.1 Aerospace and Defense

- 6.2.2 Automotive

- 6.2.3 Healthcare

- 6.2.4 Industrial

- 6.2.5 Other End Users

- 6.3 By Material

- 6.3.1 Plastic

- 6.3.2 Metals

- 6.3.3 Ceramics

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Argentina

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East & Africa

- 6.4.5.1 UAE

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 Israel

- 6.4.5.4 South Africa

- 6.4.5.5 Rest of Middle East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 3D Systems Corporation

- 7.1.2 General Electric Company (GE Additive)

- 7.1.3 EnvisionTEC GmbH

- 7.1.4 EOS GmbH

- 7.1.5 Exone Company

- 7.1.6 Mcor Technologies Ltd

- 7.1.7 Materialise NV

- 7.1.8 Optomec Inc.

- 7.1.9 Stratasys Ltd

- 7.1.10 SLM Solutions Group AG

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

積層製造(AM) 市場:全球產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年)

積層製造(AM) 市場:全球產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年) 全球積層製造市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球積層製造市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 聚合物層積造型的全球市場:市場規模,佔有率,預測,趨勢分析:報價環,各技術,各終端用戶,各地區-2031年為止的預測

聚合物層積造型的全球市場:市場規模,佔有率,預測,趨勢分析:報價環,各技術,各終端用戶,各地區-2031年為止的預測 混合積層製造設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

混合積層製造設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 混合積層製造機器市場報告:2030 年趨勢、預測與競爭分析

混合積層製造機器市場報告:2030 年趨勢、預測與競爭分析 積層製造市場:按組件、按印表機類型、按技術、按軟體、按應用、按地區

積層製造市場:按組件、按印表機類型、按技術、按軟體、按應用、按地區 混合製造機器市場:按類型、材料、應用、最終用戶產業分類 - 2025-2030 年全球預測

混合製造機器市場:按類型、材料、應用、最終用戶產業分類 - 2025-2030 年全球預測 銅積層製造市場:按產品類型、製造技術、應用分類 - 2025-2030 年全球預測

銅積層製造市場:按產品類型、製造技術、應用分類 - 2025-2030 年全球預測 陶瓷積層製造的全球市場:陶瓷類型·流程·終端用戶產業·各地區 (~2032年)

陶瓷積層製造的全球市場:陶瓷類型·流程·終端用戶產業·各地區 (~2032年) 積層製造(AM) 市場規模、佔有率和成長分析:按印表機類型、技術、應用、材料、地區 - 產業預測,2024-2031 年

積層製造(AM) 市場規模、佔有率和成長分析:按印表機類型、技術、應用、材料、地區 - 產業預測,2024-2031 年