|

市場調查報告書

商品編碼

1640437

丙烯酸纖維:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Acrylic Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

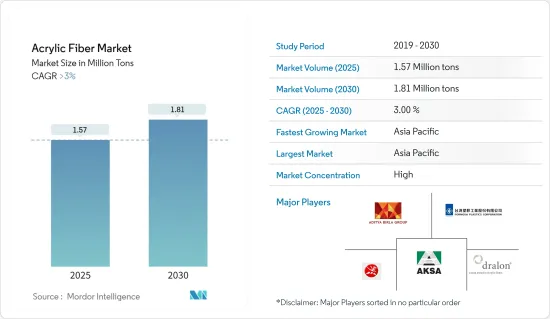

丙烯酸纖維市場規模預計在 2025 年為 157 萬噸,預計到 2030 年將達到 181 萬噸,預測期內(2025-2030 年)的複合年成長率將超過 3%。

2021 年的新冠疫情對市場產生了負面影響,導致企業、產品和製造設施放緩,減少了經濟活動。不過,預計市場將在預測期內復甦。

關鍵亮點

- 推動市場成長的關鍵因素包括對服裝的高需求和工業應用的增加。

- 然而,聚酯等替代品的可用性以及全球對丙烯酸纖維生產的嚴格規定預計將阻礙市場的成長。

- 然而,預計丙烯酸紙的成長機會和未來市場將在預測期內提供充足的成長機會。

- 由於東南亞國協和印度的需求量很大,亞太地區佔據了丙烯酸纖維市場的主導地位。

腈綸市場趨勢

羊毛佔據市場主導地位

- 羊毛在服飾中的使用歷史可追溯至古代。羊毛具有抗皺、吸濕、保溫等優良能。羊毛的一大特性是它能夠隨著時間的推移恢復變形。因此,用這種纖維製成的服裝頗具吸引力。

- 以 100% 羊毛纖維編織或針織的織物用途廣泛,包括毛衣、派克大衣、靴子、靴子內襯、帽子、手套、運動服、地毯、毛毯、滾筒刷、塊毯、防護衣、假髮、頭髮已成為製作接髮等服飾的標準。

- 大部分腈綸纖維都用於羊毛腈綸混紡,這種混紡織品非常受歡迎。圓形針織品採用 55% 羊毛和 45% 腈綸混紡。這種混紡纖維特別用於生產運動服,具有易於護理、耐用、外觀保持性好、色彩造型鮮豔和手感舒適等優點。

- 根據需求,世界各地使用多種不同的混合物。 50/50 和 70/30 腈綸羊毛混紡布料製成的服飾價格便宜,外觀漂亮,而且易於護理。 50/50 的腈綸/羊毛混紡用於製作耐用且不變形的輕質服飾,而 70/30 的腈綸/羊毛混紡則用於製作休閒褲。

- 據國際毛紡織組織稱,中國仍然是世界上最大的羊毛纖維買家,但美國對羊毛的需求也在增加。截至 2022 年 11 月的一年中,進口到美國的羊毛服飾數量與 2021 年同期相比增加了 47%。

- 因此,預計預測期內羊毛領域對丙烯酸纖維的需求將持續增加,並佔據市場主導地位。

中國主導亞太市場

- 中國是全球最大的腈綸生產國,佔世界腈綸產量的30%以上。受國內和國際市場特別是東南亞國協、歐洲、美國、日本等市場需求的推動,中國紡織業規模逐年擴大。

- 伊朗、印度、越南、巴基斯坦和阿拉伯聯合大公國是中國出口腈綸的最大市場。我們也從日本、德國、泰國、韓國和土耳其等國家進口腈綸纖維。

- 中國是世界上最大的紡織品生產國和出口國。以以金額為準,其約佔世界紡織品出口總額的43%。因此,中國服飾的成長可望提振腈綸市場。

- 該國紡織業取得了顯著的成長。根據中國國家統計局統計,2023年中國重點紡織企業主營收益與前一年同期比較%。 2023年,中國紡織品服飾出口預計將達到歷史最高的2,936億美元。

- 因此,預計所有這些市場趨勢將在預測期內推動中國丙烯酸纖維市場的需求。

腈綸產業細分

腈綸纖維市場本質上是整合的。市場的主要企業包括 Aksa Akrilik Kimya Sanayii AS、Dralon、吉林化纖集團、Aditya Birla Management Corporation Pvt.Ltd 和台塑股份有限公司(不分先後順序)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 服裝需求旺盛

- 增加工業用途

- 其他促進因素

- 限制因素

- 聚酯等替代品的可用性

- 全球對腈綸生產有著嚴格的規定

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(市場規模(基於數量))

- 形式

- 史泰博

- 燈絲

- 混合

- 羊毛

- 棉布

- 其他混合物(纖維素)

- 應用

- 服飾

- 家居家具

- 工業的

- 其他用途(室內裝潢)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- Aditya Birla Management Corporation Pvt. Ltd

- Aksa Akrilik Kimya Sanayii AS

- China Petrochemical Corporation(Sinopec)

- Dralon

- Formosa Plastics Corporation

- Indian Acrylics Limited

- Japan Exlan Co., Ltd

- Jiangsu Zhongxin Resources Group

- Jilin Chemical Fiber Group Co. Ltd

- Kaltex

- Kaneka Corporation

- Mitsubishi Chemical Corporation

- Pasupati Acrylon

- PetroChina Company Limited

- Taekwang Industrial Co. Ltd

- Toray Industries Inc.

- Vardhman Acrylics Ltd

第7章 市場機會與未來趨勢

- 壓克力紙的未來市場

- 其他機會

The Acrylic Fiber Market size is estimated at 1.57 million tons in 2025, and is expected to reach 1.81 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2021, as the pandemic resulted in the slowdown of businesses, products, and manufacturing facilities, resulting in less economic activity. However, the market is expected to recover during the forecast period.

Key Highlights

- The major factors driving the growth of the market studied include the high demand for apparel and increasing industrial applications.

- On the flip side, the availability of substitutes like polyester and stringent regulations worldwide on the production of acrylic fiber are expected to hinder the growth of the market.

- However, growing opportunities and the future market for acrylic paper are expected to offer ample growth opportunities during the forecast period.

- Asia-Pacific dominated the acrylic fiber market due to high demand from the ASEAN countries and India.

Acrylic Fiber Market Trends

The Wool Segment to Dominate the Market

- The use of wool for clothing dates back to ancient times. Wool has outstanding properties, such as resistance to wrinkles, moisture absorption, and warmth. A significant feature of wool is its ability to recover from deformation over time. Hence, clothing made from these fibers is attractive.

- Fabrics woven or knitted with 100% wool fiber have become a standard in making apparel, such as sweaters, hoodies, boots, boot lining, hats, gloves, athletic wear, carpeting, blankets, roller brushes, upholstery, area rugs, protective clothing, wigs, and hair extensions.

- A majority of acrylic fiber is used to make wool and acrylic blends, which are very popular. A blend of 55% wool and 45% acrylic fiber is used to make circular knit goods. This blend is particularly used in making sportswear, with characteristics like ease of care, durability, appearance retention, color styling, and palatability.

- Different blends are used worldwide depending on the requirements. The 50/50 and 70/30 acrylic wool blends are popular among those apparel that are inexpensive, look good, and are easy to handle. The 50/50 acrylic wool blend is used to make lightweight apparel that has excellent durability and shape retention, while the 70/30 acrylic wool blend is used to make slacks.

- According to the International Wool Textile Organization, China remains the top buyer of wool fiber globally, yet there is an increasing demand for wool in the United States. During the year that concluded in November 2022, the quantity of wool clothing brought into the United States increased by 47% compared to the same period in 2021.

- Hence, increasing demand for acrylic fiber in the wool segment is expected to dominate the market over the forecast period.

China to Dominate the Market in Asia-Pacific

- China is the largest producer of acrylic fibers in the world, accounting for a share of more than 30% of global acrylic fiber production. Owing to the demand from domestic and international markets, primarily from ASEAN countries, Europe, the United States, and Japan, the textile industry in China has expanded over the years.

- Iran, India, Vietnam, Pakistan, and the United Arab Emirates are some of the largest markets where China exports acrylic fibers. The country also imports acrylic fiber from countries like Japan, Germany, Thailand, South Korea, and Turkey.

- China is the largest textile-producing and exporting country in the world. It holds about 43% share of the world's total textile exports in terms of value. Thus, the growth in China's clothing industry is anticipated to boost the market for acrylic fibers.

- The country has witnessed significant growth in the textiles segment. According to the National Bureau of Statistics of China, in 2023, the combined earnings of China's leading textile companies increased by 7.2% compared to the previous year. In 2023, China's exports of textiles and clothing reached a record high of USD 293.6 billion.

- Hence, all such market trends are expected to add to the demand for the acrylic fibers market in China during the forecast period.

Acrylic Fiber Industry Segmentation

The acrylic fiber market is consolidated in nature. Some of the major players in the market include (not in any particular order) Aksa Akrilik Kimya Sanayii AS, Dralon, Jilin Chemical Fiber Group Co. Ltd, Aditya Birla Management Corporation Pvt. Ltd, and Formosa Plastics Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 High Demand for Use in Apparel

- 4.1.2 Increasing Industrial Application

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitutes, like Polyester

- 4.2.2 Stringent Regulations Worldwide on the Production of Acrylic Fiber

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Form

- 5.1.1 Staple

- 5.1.2 Filament

- 5.2 Blending

- 5.2.1 Wool

- 5.2.2 Cotton

- 5.2.3 Other Blendings (Cellulose)

- 5.3 Application

- 5.3.1 Apparel

- 5.3.2 Household Furnishing

- 5.3.3 Industrial

- 5.3.4 Other Applications (Upholstery)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aditya Birla Management Corporation Pvt. Ltd

- 6.4.2 Aksa Akrilik Kimya Sanayii AS

- 6.4.3 China Petrochemical Corporation (Sinopec)

- 6.4.4 Dralon

- 6.4.5 Formosa Plastics Corporation

- 6.4.6 Indian Acrylics Limited

- 6.4.7 Japan Exlan Co., Ltd

- 6.4.8 Jiangsu Zhongxin Resources Group

- 6.4.9 Jilin Chemical Fiber Group Co. Ltd

- 6.4.10 Kaltex

- 6.4.11 Kaneka Corporation

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Pasupati Acrylon

- 6.4.14 PetroChina Company Limited

- 6.4.15 Taekwang Industrial Co. Ltd

- 6.4.16 Toray Industries Inc.

- 6.4.17 Vardhman Acrylics Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Market for Acrylic Paper

- 7.2 Other Opportunities

腈綸市場規模、佔有率及成長分析(按纖維類型、染色方法、混紡、最終用戶和地區)- 2025-2032 年產業預測

腈綸市場規模、佔有率及成長分析(按纖維類型、染色方法、混紡、最終用戶和地區)- 2025-2032 年產業預測 丙烯酸纖維市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

丙烯酸纖維市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 丙烯酸纖維市場:按形狀類型、織物類型、應用分類 - 2025-2030 年全球預測腈綸短纖維市場:按染色方法、混紡、混紡類型和最終用途分類 - 全球預測 2025-2030

丙烯酸纖維市場:按形狀類型、織物類型、應用分類 - 2025-2030 年全球預測腈綸短纖維市場:按染色方法、混紡、混紡類型和最終用途分類 - 全球預測 2025-2030 全球丙烯酸纖維市場評估:依技術、形狀、混合、最終用途產業、地區、機會、預測(2017-2031)

全球丙烯酸纖維市場評估:依技術、形狀、混合、最終用途產業、地區、機會、預測(2017-2031) 腈綸纖維市場-2024年至2029年預測

腈綸纖維市場-2024年至2029年預測 丙烯纖維市場:趨勢,機會,競爭分析【2023-2028年】

丙烯纖維市場:趨勢,機會,競爭分析【2023-2028年】