|

市場調查報告書

商品編碼

1851446

社群媒體分析:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Social Media Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

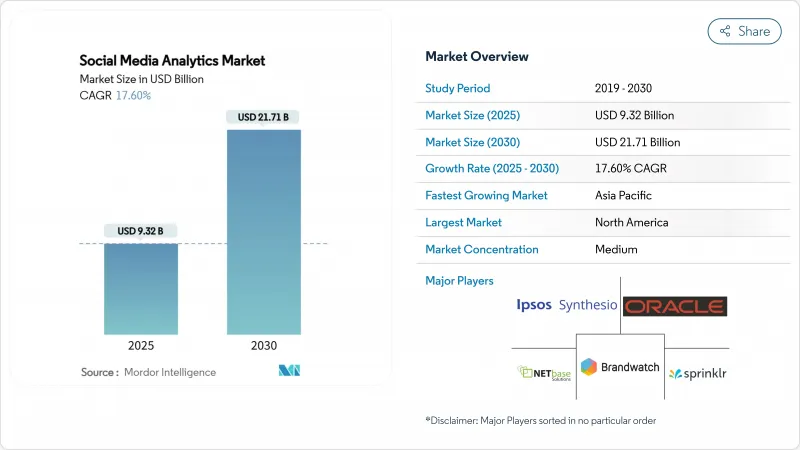

預計到 2025 年,社群媒體分析市場規模將達到 93.2 億美元,到 2030 年將達到 217.1 億美元,年複合成長率為 17.6%。

此次擴張的驅動力在於企業對即時情緒偵測、預測行為建模和宣傳活動報酬率衡量的需求激增。成長也反映出市場正從獨立的品牌監測轉向整合式、人工智慧主導引擎,這些引擎能夠大規模地攝取文字、影像、音訊和影片。加速的雲端遷移、社交電商的興起以及新的資料隱私法規正在重塑解決方案的藍圖。能夠將多模態處理、透明的模型管治和特定領域的資料連接器結合的供應商正在贏得市場佔有率,因為買家正在將各種獨立工具整合到嵌入式的客戶體驗體系中。因此,產品藍圖的重點在於持續的模型重訓練和內建的客戶經驗輔助功能,以保持差異化優勢。

全球社群媒體分析市場趨勢與洞察

社群媒體用戶數量呈指數級成長

預計到2025年,將有超過52.4億人參與社群媒體,不斷成長的數據量將推動社群媒體分析市場向可擴展的雲端架構發展,以分析每天數十億次的互動。影片優先的互動模式日益普及——TikTok的平均互動率為2.50%,而Instagram僅為0.50%——迫使供應商整合圖像和影片分類器,取代僅基於文字的情緒分析工具。醫療保健提供者正利用用戶數量的激增來追蹤公共衛生訊號,因為90%的美國成年人透過社交平臺獲取健康資訊。資料多樣性加劇了供應商的鎖定效應,因為專有領域本體和語言模型會隨著時間的推移而提高準確性。然而,去除重複的機器人和虛假互動會增加計算成本,並需要不斷改進演算法。

GenAI驅動的洞察引擎推動北美地區的提升銷售

北美企業正大力投資基因人工智慧(GenAI),以期將被動監控轉變為預測性指引。該地區69%的負責人認為基因人工智慧對內容個人化具有革命性意義。先進的變壓器模型能夠以99.68%的準確率檢測虛假訊息,從而提高整體資料保真度。一項銀行試點計畫將長短期記憶網路(LSTM)應用於136,150條社交媒體帖子,實現了91%的客戶情緒分類準確率,從而能夠進行微細分宣傳活動。然而,只有12%的企業報告了明確的基因人工智慧投資報酬率,這為能夠填補技能缺口的供應商創造了諮詢和管理服務的機會。部署低程式碼模型訓練介面和可解釋性儀表板的供應商最有可能獲得更高的收入。

嚴格的隱私法規限制了資料粒度。

GDPR的實施使歐盟出版商的第三方追蹤能力降低了14.79%,迫使平台開發諸如聯邦學習等保護隱私的分析解決方案。 《加州消費者隱私法案》在美國範圍內也實施了類似的限制。 Meta的「付費或同意」政策表明,同意框架如何降低資料可用性並使跨平台用戶資料拼接變得更加複雜。能夠在保護個人隱私的同時提供匯總的、群體層面的洞察的供應商,將能夠遵守法規並降低客戶的風險敞口。

細分市場分析

到2024年,解決方案將佔總收入的65%,凸顯其作為社群媒體分析市場入門級產品的地位。雖然訂閱許可可能提供可預測的淨利率,但目前企業面臨大量待實施項目,因此更傾向於選擇服務合約。預計服務業務將以23.3%的複合年成長率成長,這需要進行模型校準、分類設計和監管映射。這一成長表明,社群媒體分析市場在實施和最佳化方面的規模將超過基礎平台費用,尤其是在GenAI工作流程需要客製化提示工程的情況下。 Sprinklr 2025會計年度的營收為7.964億美元,高於2023會計年度的6.182億美元,這反映了其軟體+諮詢的雙軌模式。

專業服務的發展勢頭也受到垂直行業合規性差異的驅動。醫療保健客戶要求符合 HIPAA 標準,而銀行客戶則要求信用風險決策模型具有可解釋性。與領域專家和資料科學家合作的服務提供者可以加快價值實現速度並提高市場佔有率。因此,諮詢合作夥伴正在共同開發基於結果的定價模式,這種模式與更高的轉換率和更低的客戶流失率相關,從而獎勵各方增加經常性收入。

預計到2024年,雲端運算將佔據社群媒體分析市場72%的佔有率,並在2030年之前維持21.8%的複合年成長率,這主要得益於自動擴展和託管安全技術的推動。彈性GPU叢集處理視訊串流和變壓器模型的成本效益高於大多數本地部署方案。混合部署方案在受資料居住規則約束的產業仍然存在,但超大規模資料中心在區域資料中心的投資降低了資料主權障礙。因此,隨著即時儀錶板成為董事會層級的營運工具,面向雲端工作負載的社群媒體分析市場規模將會擴大。

雲端原生供應商利用持續配置,每週推送功能更新,從而改善機器人偵測、語言覆蓋範圍和合規性範本。與 Snowflake 和 Databricks 等大型資料倉儲生態系統的整合,實現了對行銷、銷售和服務的統一可視性。相反,傳統的本地部署方案在模型升級和修補程式方面存在延遲,增加了營運風險。

區域分析

北美將引領社群媒體分析市場,預計到2024年營收成長率將達到38%,這主要得益於其成熟的數位廣告生態系統和早期部署的人工智慧技術。美國超過75%的廣告支出都發生在網路上,這推動了社群媒體監聽工具在全通路編配宣傳活動中的應用。由於各州隱私權法規的差異,企業面臨日益成長的合規成本,也促使企業需要具備政策感知能力的分析架構。儘管社群媒體分析技術已經發展成熟,但隨著品牌將其應用場景從行銷擴展到風險管理、投資者關係和職場文化評估等領域,該技術仍保持成長動能。

亞太地區到2030年將以21.3%的複合年成長率領跑,主要得益於行動優先的消費群體大規模接受社交電商。到2024年,該地區的社群媒體廣告支出將達到770億美元,年增15%,這將推動跨語言情緒分析和網紅詐欺偵測的投資。中國的生態系統創新,例如淘寶直播帶貨,正向東南亞蔓延,催生出待開發區的分析需求。印度的多語言多樣性進一步要求建構適應性強的本體,並促進夥伴關係開發本地語言模型。

GDPR 和《數位服務法案》迫使企業探索合規的分析方案,而不是放棄洞察生成。提供用戶許可管理、設備端處理和差分隱私報告等功能的供應商,正吸引越來越多謹慎的買家。同時,拉丁美洲和中東及非洲地區的網路普及率不斷提高,將推動現成雲端分析解決方案的採用。巴西和海灣地區的城市叢集體現了成熟的市場行為,在無需大量在地化成本的情況下,加速了社群媒體分析市場的普及。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 社群媒體用戶數量呈指數級成長

- GenAI驅動的洞察引擎推動北美地區的提升銷售

- 加速應用內社交電商的投資報酬率追蹤

- 全球廣告商(美國和歐盟)強制的品牌安全指標推動市場發展

- 市場限制

- 嚴格的隱私法規限制了資料粒度。

- 多模態資料解讀分析技能的差距阻礙了市場發展

- 機器人和假流量會扭曲市場情緒指標,阻礙市場發展。

- 價值鏈分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 透過部署模式

- 雲

- 本地部署

- 按模組

- 社群媒體監測與追蹤

- 社群媒體衡量/聆聽與分析

- 按最終用戶行業分類

- 媒體與娛樂

- 資訊科技和電訊

- BFSI

- 零售與電子商務

- 旅遊與飯店

- 醫療保健和生命科學

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 中東

- GCC

- 土耳其

- 以色列

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sprinklr

- Oracle Corporation

- Synthesio(Crimson Hexagon)

- Brandwatch

- NetBase Solutions Inc.

- Meltwater(Sysomos Inc.)

- Talkwalker

- Sprout Social

- Digimind Social

- Brand24

- Hootsuite Inc.

- Khoros, LLC

- Clarabridge(now Qualtrics)

- Cision Ltd.

- Socialbakers(now Emplifi)

- Mentionlytics

- YouScan

- Pulsar Platform

- Dataminr

- Unmetric

- Awario

- Nuvi

- Adobe Inc.

第7章 市場機會與未來展望

The social media analytics market size stands at USD 9.32 billion in 2025 and is forecast to reach USD 21.71 billion by 2030, advancing at a 17.6% CAGR.

Surging enterprise demand for real-time sentiment detection, predictive behavioral modeling, and campaign ROI measurement underpins this expansion. Growth also reflects a decisive pivot from stand-alone brand monitoring toward unified, AI-driven insight engines that ingest text, image, audio, and video at scale. Accelerated cloud migration, the proliferation of social commerce, and fresh data-privacy mandates are reshaping solution roadmaps. Vendors able to combine multimodal processing, transparent model governance, and domain-specific data connectors are capturing share as buyers consolidate point tools into integrated customer-experience stacks. Competitive intensity remains high because switching costs are modest and proof-of-value cycles are short; as a result, product roadmaps emphasize continuous model retraining and embedded GenAI co-pilots to sustain differentiation.

Global Social Media Analytics Market Trends and Insights

Exponential Growth of Number of Social Media Users

More than 5.24 billion individuals engage on social channels in 2025, expanding data volumes and pushing the social media analytics market toward scalable cloud architectures that parse billions of daily interactions. Rising video-first engagement on TikTok, with 2.50% average interaction rates versus 0.50% on Instagram, forces vendors to embed image and video classifiers, displacing text-only sentiment tools. Healthcare providers leverage this user surge to track public health signals, with 90% of US adults sourcing health information on social platforms. Data diversity strengthens vendor lock-in because proprietary domain ontologies and language models improve accuracy over time. However, the need to de-duplicate bots and fake interactions escalates compute costs and necessitates continual algorithmic refinement.

GenAI-Powered Insight Engines Driving Upsell in North America

North American enterprises invest heavily in GenAI to transform passive monitoring into predictive guidance. Sixty-nine percent of regional marketers call GenAI revolutionary for content personalization. Advanced transformer models now detect misinformation with 99.68% accuracy, lifting overall data fidelity. Banking pilots that applied Long Short-Term Memory networks across 136,150 social posts achieved 91% customer-sentiment classification accuracy, enabling micro-segmented campaign offers. Yet only 12% of firms report clear GenAI ROI, creating advisory and managed-service opportunities for providers that can bridge the skills gap. Vendors rolling out low-code model-training interfaces and explainability dashboards are best positioned to capture expansion revenue.

Stringent Privacy Regulations Limiting Data Granularity

GDPR enforcement cut third-party tracking capability by 14.79% for EU publishers, compelling platforms to devise privacy-preserving analytics such as federated learning. The California Consumer Privacy Act extends similar constraints across the United States. Meta's "Pay or Okay" policy illustrates how consent frameworks reduce data availability and complicate cross-platform user stitching. Vendors able to deliver aggregated, cohort-level insights while preserving individual privacy comply with regulation and reduce client risk exposure.

Other drivers and restraints analyzed in the detailed report include:

- Acceleration of In-App Social Commerce ROI Tracking

- Brand-Safety Metric Mandates by Global Advertisers

- Analytics Skill-Set Gap for Multimodal Data Interpretation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions contributed 65% of 2024 revenue, underlining their role as the entry point to the social media analytics market. Subscription licenses provide predictable margins, yet enterprises now confront implementation backlogs that favor service engagements. Services are forecast to rise at a 23.3% CAGR as firms seek model calibration, taxonomy design, and regulatory mapping. This uptick illustrates how the social media analytics market size for implementation and optimization eclipses basic platform fees, especially when GenAI workflows demand bespoke prompt engineering. Sprinklr's USD 796.4 million FY25 revenue, up from USD 618.2 million in FY23, showcases the dual-stream model of software plus advisory.

The momentum in professional services also stems from vertical compliance nuances. Healthcare clients require HIPAA alignment, while banking customers demand model explainability for credit-risk decisions. Providers that pool domain experts with data scientists reduce time-to-value and deepen wallet share. Consequently, advisory partners co-develop outcome-based pricing tied to conversion uplift or churn reduction, aligning incentives and boosting recurring revenue.

Cloud captured 72% of the social media analytics market share in 2024 and is projected to sustain a 21.8% CAGR through 2030 on the strength of auto-scaling and managed security. Elastic GPU clusters process video streams and transformer models more cost-effectively than most on-premise alternatives. Hybrid options persist in sectors bound by data-residency rules, yet hyperscaler investment in regional zones lowers sovereignty barriers. The social media analytics market size for cloud workloads will therefore expand as real-time dashboards become board-level operational tools.

Cloud-native providers leverage continuous deployment to push weekly feature releases that refine bot-detection, language coverage, and compliance templates. Integration with broader data-warehouse ecosystems such as Snowflake and Databricks enables unified marketing, sales, and service visibility. Conversely, legacy on-premise installations struggle with model-versioning and patch latency, increasing operational risk.

The Social Media Analytics Market Report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise), Module (Social Media Monitoring and Tracking, Social Media Measurement/Listening and Analytics), End-User Industry (Media and Entertainment, IT and Telecom, BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the social media analytics market with 38% revenue in 2024, buoyed by sophisticated digital-ad ecosystems and early GenAI rollouts. More than 75% of US ad expenditure is online, driving pervasive use of social listening tools within omnichannel campaign orchestration. Enterprises face rising compliance overhead due to state-level privacy statutes, prompting demand for policy-aware analytics frameworks. Despite maturity, growth continues as brands extend usage from marketing into risk, investor relations, and workplace culture assessment.

Asia-Pacific posts the highest regional CAGR at 21.3% through 2030 as mobile-first populations adopt social commerce at scale. The region's USD 77 billion social-media ad spend in 2024, up 15% year over year, anchors investment in cross-language sentiment and influencer fraud detection. China's ecosystem innovation-such as Taobao's live-stream selling-spills over to Southeast Asia, creating green-field analytics demand. India's multilingual diversity further necessitates adaptable ontologies, spurring local-language model development partnerships.

Europe records steady growth because GDPR and the Digital Services Act force enterprises to seek compliant analytics alternatives rather than abandon insight generation. Vendors that embed consent management, on-device processing, and differential-privacy reporting expand pipeline among cautious buyers. Meanwhile, Latin America, Middle East, and Africa begin adopting off-the-shelf cloud analytics as internet penetration rises. Urban clusters in Brazil and the Gulf states mirror advanced market behaviors, accelerating social media analytics market adoption without incurring heavy localization expenditure.

- Sprinklr

- Oracle Corporation

- Synthesio (Crimson Hexagon)

- Brandwatch

- NetBase Solutions Inc.

- Meltwater (Sysomos Inc.)

- Talkwalker

- Sprout Social

- Digimind Social

- Brand24

- Hootsuite Inc.

- Khoros, LLC

- Clarabridge (now Qualtrics)

- Cision Ltd.

- Socialbakers (now Emplifi)

- Mentionlytics

- YouScan

- Pulsar Platform

- Dataminr

- Unmetric

- Awario

- Nuvi

- Adobe Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential Growth of Number of Social Media Users

- 4.2.2 GenAI-powered Insight Engines Driving Upsell in North America

- 4.2.3 Acceleration of In-App Social Commerce ROI Tracking

- 4.2.4 Brand-safety Metric Mandates by Global Advertisers (US and EU) Drives the Market

- 4.3 Market Restraints

- 4.3.1 Stringent Privacy Regulations Limiting Data Granularity

- 4.3.2 Analytics Skill-set Gap for Multimodal Data Interpretation Hinders the Market

- 4.3.3 Bot and Fake-traffic Distortion of Sentiment Metrics Hinders the Market

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Module

- 5.3.1 Social Media Monitoring and Tracking

- 5.3.2 Social Media Measurement/Listening and Analytics

- 5.4 By End-user Industry

- 5.4.1 Media and Entertainment

- 5.4.2 IT and Telecom

- 5.4.3 BFSI

- 5.4.4 Retail and e-Commerce

- 5.4.5 Travel and Hospitality

- 5.4.6 Healthcare and Life-sciences

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sprinklr

- 6.4.2 Oracle Corporation

- 6.4.3 Synthesio (Crimson Hexagon)

- 6.4.4 Brandwatch

- 6.4.5 NetBase Solutions Inc.

- 6.4.6 Meltwater (Sysomos Inc.)

- 6.4.7 Talkwalker

- 6.4.8 Sprout Social

- 6.4.9 Digimind Social

- 6.4.10 Brand24

- 6.4.11 Hootsuite Inc.

- 6.4.12 Khoros, LLC

- 6.4.13 Clarabridge (now Qualtrics)

- 6.4.14 Cision Ltd.

- 6.4.15 Socialbakers (now Emplifi)

- 6.4.16 Mentionlytics

- 6.4.17 YouScan

- 6.4.18 Pulsar Platform

- 6.4.19 Dataminr

- 6.4.20 Unmetric

- 6.4.21 Awario

- 6.4.22 Nuvi

- 6.4.23 Adobe Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球社群媒體分析市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球社群媒體分析市場規模、佔有率、趨勢和成長分析報告(2026-2034) 社群媒體分析市場機會、成長要素、產業趨勢分析及2026-2035年預測

社群媒體分析市場機會、成長要素、產業趨勢分析及2026-2035年預測 社群媒體分析市場:按組件、部署類型、組織規模、產業、應用和分銷管道分類-2026-2032年全球市場預測

社群媒體分析市場:按組件、部署類型、組織規模、產業、應用和分銷管道分類-2026-2032年全球市場預測 社群媒體分析市場規模、佔有率、趨勢和預測:按組件、部署類型、企業規模、應用、最終用戶和地區分類,2026-2034 年

社群媒體分析市場規模、佔有率、趨勢和預測:按組件、部署類型、企業規模、應用、最終用戶和地區分類,2026-2034 年 全球社群媒體分析市場(至2035年):按產品/服務、功能、方法論、應用、產業和地區分類-產業趨勢和市場預測

全球社群媒體分析市場(至2035年):按產品/服務、功能、方法論、應用、產業和地區分類-產業趨勢和市場預測 社群媒體分析市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署方式、公司類型、功能、應用、最終用戶、地區和競爭格局分類,2021-2031 年

社群媒體分析市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署方式、公司類型、功能、應用、最終用戶、地區和競爭格局分類,2021-2031 年 2026-2030年全球社群媒體分析市場

2026-2030年全球社群媒體分析市場 社群媒體分析市場:按解決方案類型、部署模式、最終用戶和地區分類

社群媒體分析市場:按解決方案類型、部署模式、最終用戶和地區分類 2026年全球社群媒體分析市場報告

2026年全球社群媒體分析市場報告 社群媒體分析市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類

社群媒體分析市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類