|

市場調查報告書

商品編碼

1640684

機油 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Engine Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

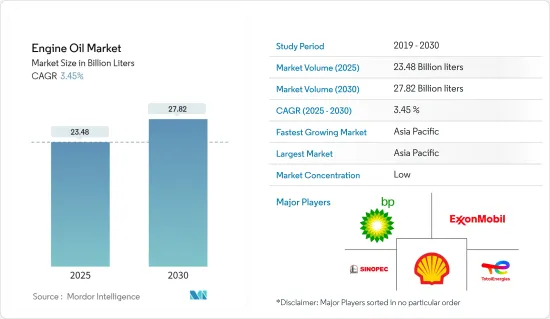

預計 2025 年機油市場規模為 234.8 億公升,到 2030 年將達到 278.2 億公升,預測期內(2025-2030 年)的複合年成長率為 3.45%。

新冠疫情危機影響了全球汽車產業,導致大多數地區的汽車生產和銷售突然停止。這些停工導致全球數百萬輛汽車停產。汽車產業對機油市場有直接影響,因為機油用於提高引擎整體效率並減少排放氣體。然而,在2021年下半年限制措施解除後,隨著汽車產業活動的活性化,市場成長穩定恢復,進而引發市場復甦。

關鍵亮點

- 從中期來看,汽車產銷量的增加以及高性能潤滑油的普及是推動市場成長的關鍵因素。

- 然而,預計在預測期內,換油間隔的增加和電動車(EV)的適度影響是抑制目標產業成長的關鍵因素。

- 中東和非洲不斷發展的汽車工業以及北美和亞太地區眾多即將開展的建設計劃很可能很快就會為全球市場提供豐厚的成長機會。

- 預計亞太地區將主導市場,並可能在預測期內實現最高的複合年成長率。

機油市場趨勢

汽車產業需求不斷成長

- 機油廣泛用於潤滑內燃機。機油由75-90%的基礎油和10-25%的添加劑組成,主要用於全球汽車和其他運輸領域。

- 使用機油的主要好處是減少磨損、防止腐蝕並保持引擎平穩運轉。機油在運動部件之間形成一層薄膜,可促進熱傳遞並減少部件接觸時的張力。

- 小型汽車產銷量的增加預計將對機油消耗產生直接影響。因此,預計預測期內機油的需求將會增加。

- 根據國際汽車工業組織(OICA)預測,2022年全球汽車產量將達85,016,728輛,與前一年同期比較成長5.9%。 2021年、2022年汽車產量年增率與前一年同期比較6%。

- 同樣,根據 OICA 的數據,2022 年商用車產量將達到 5,749 萬輛,較 2021 年的 5,644 萬輛有所成長。

- 同時,根據美國商務部經濟分析局的數據,2022 年年輕型汽車零售將為 13,754,300 輛,與 2021 年的 14,946,900 輛相比最低。

- 此外,根據德國汽車工業協會(Verband 工業)預測,2022年德國汽車產量預計將達到340萬輛,較2021年的310萬輛成長9.6%。

- 因此,預計上述因素將對未來機油市場產生重大有利影響。

亞太地區佔市場主導地位

- 亞太地區在機油市場佔據主導地位,主要原因是汽車生產和發電行業的需求大幅成長。

- 中國是世界領先的汽車製造國之一。該國的汽車工業正在不斷改進其產品,重點是生產燃料效率更高、排放氣體的汽車。

- 根據中國工業協會(CAAM)的數據,2022 年中國乘用車銷量約 2,356 萬輛,商用車銷量約 330 萬輛。

- 同樣,根據印度品牌資產基金會的預測,到2022會計年度,印度的發電能力將增加到400吉瓦左右。這延續了先前發電能力的成長。 1992年至2022年間,印度的發電量增加了5倍。

- 據內閣府透露,2022年國內製造商的重型電機訂單約為2.25兆日圓(約152.2億美元),較上年的約2.15兆日圓(約145.5億美元)有所減少。

- 因此,預計上述因素將在未來幾年對該地區的機油市場產生重大影響。

機油業概況

機油市場比較分散。主要參與企業包括(不分先後順序):道達爾能源、埃克森美孚、英國石油公司、殼牌公司和中國石油化學集團公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 汽車產銷售成長

- 高性能潤滑劑的採用日益增多

- 限制因素

- 延長換油週期

- 電動車(EV)對未來影響不大

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 監理政策分析

第5章 市場區隔(市場規模(基於數量))

- 最終用戶產業

- 發電

- 汽車及其他運輸設備

- 重型機械

- 冶金與金屬加工

- 化學製造

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 菲律賓

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 墨西哥

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 西班牙

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 卡達

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- AMSOIL INC

- Bharat Petroleum Corporation Limited

- BP plc

- Chevron Corporation

- China Petrochemical Corporation

- Eni SPA

- Exxon Mobil Corporation

- FUCHS

- Gazpromneft-Lubricants, Ltd

- Gulf Oil International

- Hindustan Petroleum Corporation Limited

- Idemitsu Kosan Co.,Ltd

- Illinois Tool Works Inc.

- Indian Oil Corporation Ltd

- JX Nippon Oil & Gas Exploration Corporation

- LUKOIL

- Motul

- Petrobras

- PETRONAS Lubricants International

- Phillips 66 Company

- PT Pertamina Lubricants

- Repsol

- Shell PLC

- SK Enmove CO., Ltd

- Tide Water Oil Co. (India) Ltd

- TotalEnergies

- Valvoline Cummins Pvt. Ltd.

第7章 市場機會與未來趨勢

- 中東和非洲汽車工業的成長

- 北美和亞太地區的眾多建設計劃

The Engine Oil Market size is estimated at 23.48 billion liters in 2025, and is expected to reach 27.82 billion liters by 2030, at a CAGR of 3.45% during the forecast period (2025-2030).

The COVID-19 crisis impacted the global automotive industry, as both the production and sales of motor vehicles came to a sudden halt in most regions. These work stoppages led to a loss in the production of millions of vehicles across the world. The automobile industry has a direct effect on the engine oil market as it is used to improve the overall efficiency of an engine and reduce emissions. However, the market growth picked up steadily, owing to increased automotive activities after the lifting of restrictions in the second half of 2021, leading to market recovery.

Key Highlights

- Over the medium term, the increasing automotive production and sales and the increasing adoption of high-performance lubricants are significant factors driving the growth of the market studied.

- However, extended drain intervals and the modest impact of electric vehicles (EVs) are key factors anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the growing automotive industry in the Middle East and Africa and numerous upcoming construction projects in North America and APAC are likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Engine Oil Market Trends

Increasing Demand from Automotive Industry

- Engine oils are widely used to lubricate internal combustion engines. They are composed of 75-90% base oils and 10-25% additives and are mostly used in automotive and other transport segments across the world.

- The major advantages of using engine oils are wear and tear reduction, corrosion protection, and the engine's smooth operation. They function by creating a thin film between the moving parts for enhancing heat transfer and reducing tension during the contact of parts.

- The increasing production and sales of light-duty vehicles are estimated with a direct impact on engine oil consumption. It, in turn, is anticipated to drive the demand for engine oil during the forecast period.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production reached 85,016,728 units in 2022, and the production increased by 5.9% when compared to the previous year's data. Motor vehicle production growth year-on-year between the 2021 and 2022 markets was at 6%.

- Similarly, as per OICA, commercial vehicle production reached 57.49 million units in 2022 and registered growth when compared to 56.44 in 2021.

- Meanwhile, as per the Bureau of Economic Analysis of the United States Department of Commerce, light vehicle retail sales reached 13,754.3 thousand units, registering the lowest production when compared to 14,946.9 thousand units in 2021.

- Further, according to the German Association of the Automotive Industry (Verband der Automobilindustrie), automobile production in Germany reached 3.4 million in 2022 and registered a growth of 9.6% when compared to 3.1 million in 2021.

- As a result, the factors above are anticipated with a substantial beneficial influence on the engine oil market in the future years.

The Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominated the engine oil market primarily due to the huge growing demand for automotive production and power generation industries.

- China holds the title of the world's leading automobile manufacturer. The nation's automotive industry is poised for product advancement, emphasizing the production of vehicles aimed at enhancing fuel efficiency and reducing emissions, addressing escalating environmental concerns attributed to increasing pollution levels in the country

- According to the China Association of Automobile Manufacturers(CAAM), in 2022, approximately 23.56 million passenger cars and 3.3 million commercial vehicles were sold in China.

- Similarly, according to the India Brand Equity Foundation, in the financial year 2022, India's power generation capacity rose to nearly 400 GW. Thereby, the growth in generation capacity from the previous years continues. Between 1992 and 2022, the country's electricity capacity experienced a five-fold increase.

- As per Cabinet Office Japan, in 2022, the order value for heavy electrical machinery from manufacturers in Japan amounted to approximately JPY 2.25 trillion (~USD 15.22 billion), increasing from around JPY 2.15 trillion (~USD 14.55 billion) in the previous year.

- As a result, the factors above are projected to have a substantial influence on the engine oil market in the region in the coming years.

Engine Oil Industry Overview

The engine oil market is fragmented in nature. The major players include (not in particular order) Total Energies, Exxon Mobile Corporation, BP p.l.c., Shell PLC, and China Petrochemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Automotive Production and Sales

- 4.1.2 Increasing Adoption of High-performance Lubricants

- 4.2 Restraints

- 4.2.1 Extended Drain Intervals

- 4.2.2 Modest Impact of Electric Vehicles (EVs) in the Future

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 End-user Industry

- 5.1.1 Power Generation

- 5.1.2 Automotive and Other Transportation

- 5.1.3 Heavy Equipment

- 5.1.4 Metallurgy and Metalworking

- 5.1.5 Chemical Manufacturing

- 5.1.6 Other End-user Industries

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Philippines

- 5.2.1.6 Indonesia

- 5.2.1.7 Malaysia

- 5.2.1.8 Thailand

- 5.2.1.9 Vietnam

- 5.2.1.10 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Mexico

- 5.2.2.3 Canada

- 5.2.2.4 Rest of North America

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Russia

- 5.2.3.6 Spain

- 5.2.3.7 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Qatar

- 5.2.5.4 United Arab Emirates

- 5.2.5.5 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AMSOIL INC

- 6.4.2 Bharat Petroleum Corporation Limited

- 6.4.3 BP p.l.c

- 6.4.4 Chevron Corporation

- 6.4.5 China Petrochemical Corporation

- 6.4.6 Eni SPA

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 FUCHS

- 6.4.9 Gazpromneft - Lubricants, Ltd

- 6.4.10 Gulf Oil International

- 6.4.11 Hindustan Petroleum Corporation Limited

- 6.4.12 Idemitsu Kosan Co.,Ltd

- 6.4.13 Illinois Tool Works Inc.

- 6.4.14 Indian Oil Corporation Ltd

- 6.4.15 JX Nippon Oil & Gas Exploration Corporation

- 6.4.16 LUKOIL

- 6.4.17 Motul

- 6.4.18 Petrobras

- 6.4.19 PETRONAS Lubricants International

- 6.4.20 Phillips 66 Company

- 6.4.21 PT Pertamina Lubricants

- 6.4.22 Repsol

- 6.4.23 Shell PLC

- 6.4.24 SK Enmove CO., Ltd

- 6.4.25 Tide Water Oil Co. (India) Ltd

- 6.4.26 TotalEnergies

- 6.4.27 Valvoline Cummins Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Automotive Industry in Middle East and Africa

- 7.2 Numerous Upcoming Construction Projects In North America and APAC

汽車引擎機油冷卻器市場:按類型、結構、分銷管道、車型分類 - 2025-2030 年全球預測

汽車引擎機油冷卻器市場:按類型、結構、分銷管道、車型分類 - 2025-2030 年全球預測 冬青油市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、最終用途、配銷通路和地理位置

冬青油市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、最終用途、配銷通路和地理位置 油冷卻器市場預測:~2030年全球旁通過濾器市場預測(截至2030年)

油冷卻器市場預測:~2030年全球旁通過濾器市場預測(截至2030年) 汽車三輪車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭細分,2018-2028

汽車三輪車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭細分,2018-2028 汽車中型和重型商用車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級、按需求類別、按地區、競爭分類,2018-2028

汽車中型和重型商用車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級、按需求類別、按地區、競爭分類,2018-2028 汽車乘用車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭分類,2018 -2028年

汽車乘用車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭分類,2018 -2028年 汽車兩輪車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭細分,2018-2028

汽車兩輪車引擎油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭細分,2018-2028 汽車輕型商用車機油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭細分,2018-2028

汽車輕型商用車機油市場 - 全球產業規模、佔有率、趨勢、機會和預測,按等級(合成、半合成和礦物)、按需求類別(OEM、售後市場)按地區、競爭細分,2018-2028