|

市場調查報告書

商品編碼

1640697

軟體定義安全:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Software Defined Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

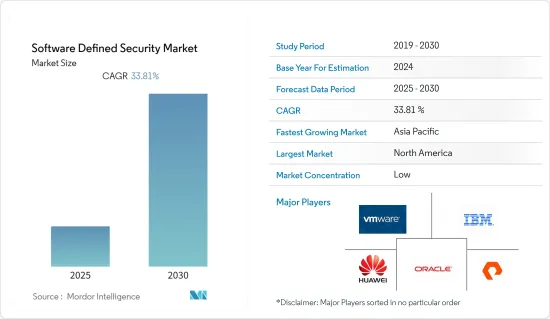

預計預測期內軟體定義安全市場複合年成長率為 33.81%。

主要亮點

- 軟體定義儲存(SDS)是企業儲存市場新興趨勢之一。 SDS 是一個更大的生態系統的一部分,其中軟體與相應的硬體分離,讓您可以根據所需的儲存量自由選擇已安裝的硬體。 SDS 可讓您降低成本,同時提高效能和靈活性。就這樣,企業逐漸走向軟體定義儲存。

- 一些協會正在塑造 SDS 在終端用戶行業中的應用方式,其中大多數協會與主要供應商有直接聯繫,以進行類似的工作。儲存網路產業協會(SNIA)為企業儲存產業制定標準。現有的儲存供應商包括 IBM、Dell EMC 和 NetApp,以及 Atlantis Computing 和 Falcon Star 等新興供應商。其中一些公司(如 NetApp、IBM 和 Red Hat)提供軟體,而其他公司(如 HPE 和 Dell EMC)則提供超融合解決方案。思科等其他公司則提供硬體並與 SDS 軟體供應商合作。

- 透過使用網路安全解決方案和軟體安裝,政府對資料安全的監管和標準日益增多,預計將在未來幾年為網路解決方案提供誘人的前景。 2022 年 2 月,Telstra 將向澳洲聯邦、州和地方政府擴展新的網路安全解決方案。網路偵測和回應能力將與政府系統和雲端基礎的服務整合,使用來自 Telstra 託管安全服務平台的巨量資料分析來監控網路威脅,而 Sovereign SecureEdge 在檢測和回應分散式威脅方面將特別有用。環境中的雲端安全。

- 這些線上安全程序是為了確保您的安全。為了避免危險和攻擊,必須規範真正的基礎,分離、觀察和確保現有框架。由於亞馬遜網路服務等雲端服務公司廣泛使用和可存取地儲存高度敏感和獨特的資料,與網路安全相關的風險有所增加,從而導致市場成長。

- 在疫情期間,軟體定義儲存在迅速擴大我們的客戶群和加速收入成長方面發揮了重要作用。在 COVID-19 期間,儲存成長並沒有停止,但一直在不斷發展,以便為無法擴展 Kubernetes 基於容器的資料管理的公司提供跨平台的整合功能。

軟體定義安全市場趨勢

雲端驅動軟體定義安全

- 這與幾年前相比發生了巨大變化,當時大多數資訊安全專家認為雲端是有限且安全的。如今,雲端被視為一種潛在的轉型,而不是安全態勢的潛在權衡,雲端是採用安全硬體和基礎設施的墊腳石,這些硬體和基礎設施受益於日益成長的網路威脅和日益成長的網路連接。它正在威脅玩家。雲端可能是安全轉型背後的驅動力。

- 雲端基礎設施旨在滿足新的需求,特別是在垂直和水平規模和安全性方面。雲端環境通常採用以技術和服務為中心的安全解決方案,無論位於何處,都可以在全球順利擴展。

- 雲端處理徹底改變了企業使用、分發和儲存資料、應用程式和工作負載的方式。但同時,各種新的安全隱憂和問題也隨之出現。隨著越來越多的資料儲存在雲端和公共雲端服務中,風險也隨之增加。在最終用戶數位化需求的推動下,一些國家,特別是新興國家,處於雲端運算採用的前沿。由於內容、邊緣服務和最後一哩連接的資料傳輸不斷成長的需求,互連頻寬容量正在擴大。

- 根據 Equinix 全球互連指數 (GXI) 報告,拉丁美洲地區預計將以 50% 的複合年成長率主導已安裝互連頻寬容量發展,預計到2023 年在該地區營運的企業將達到12 億美元。地區將貢獻安裝 1,479 Tbps 的互連頻寬。隨著雲端運算需求潛力的上升,多家供應商的採用率不斷提高,從而推動了支出。

- 此外,數位化將增加雲端交付的壓力,鼓勵 IT 部門採用更多的軟體和服務,擺脫硬體定義的權衡。這一因素,加上買家的整合和商品化,將使基礎設施即服務 (SaaS) 和託管服務提供者比傳統硬體供應商擁有更大的權力。因此,軟體定義技術預計將在未來幾年內成長。

亞太地區將佔據軟體定義安全市場最大佔有率

- 在亞太地區,跨企業的非結構化資料量呈指數級成長,不僅儲存在本地,還儲存在雲端環境中。此外,隨著物聯網在該區域的普及,邊緣產生的資料正在迅速增加。這些因素支援高度擴充性、可靠且安全的儲存架構。

- 在人口密集的國家,如中國和印度,存儲仍然依賴於傳統硬體,需要進行數位轉型才能跟上技術變化,使該地區成為軟體定義存儲(SDS) 服務的領先提供商。可圖供應商。

- 此外,日益增多的網路攻擊迫使中國加強國防能力。然而,中國也是世界其他地區網路攻擊的重要源頭。

- 2022年3月,網路安全公司Mandiant聲稱,一個中國政府支持的駭客組織作為情報收集行動的一部分,對美國一個地方政府機構進行了駭客攻擊。美國當局稱,駭客利用一個嚴重的軟體漏洞於 2021 年 12 月入侵了兩個國家機構的網路。據聯邦調查局和網路安全和基礎設施安全美國(CISA) 稱,目標國家機構包括交通、醫療保健、高等教育、農業和法院網路和系統。

- 尤其是超大規模國際數位資料內容供應商和公有雲端服務供應商,如 Facebook、Google、亞馬遜網路服務 (AWS) 和阿里雲,正在建立大型平台。尤其是香港的遠端儲存服務需求持續成長,奠定了基礎。

軟體定義安全產業概況

由於多種網路威脅迫使政府和產業在電腦網路空間投入更多資金,軟體定義安全市場高度分散。投資增加導致市場競爭加劇,許多新參與企業以更低的價格提供解決方案。市場的主要企業包括 Pure Storage Inc.、華為技術有限公司、VMWare Inc.、戴爾公司、甲骨文公司和 IBM 公司。這些公司不斷創新和升級其產品以滿足日益成長的市場需求。

- 2023 年1 月- 領先的汽車供應商和全球合作夥伴法雷奧(Valeo) 與整合式、自動駕駛和電動汽車自動駕駛汽車網路安全解決方案的領先供應商C2A Security 宣布簽署合資協議,為自動駕駛汽車開發和部署保全服務安全解決方案。此次新的合作滿足了業界對簡化和有效的網路安全的需求。 C2A Security 與法雷奧之間的合作將使汽車產業能夠採用自動化網路安全,在將安全放在首位的同時實現創新和麵向未來的業務。

- 2022 年 10 月-全球領先的應用程式安全測試工具供應商 Veracode 宣布其持續軟體安全平台已增強,以納入容器安全。現有客戶現在可以參與 Veracode Container Security 早期存取舉措。新的 Veracode 容器安全服務涵蓋容器映像的安全性配置、漏洞掃描和秘密管理系統,旨在滿足雲端原生軟體工程團隊的需求。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 相關人員分析

- 市場促進因素

- 對快速回應和提高安全性的需求

- 雲端服務的採用率提高

- 市場限制

- 缺乏虛擬環境中的安全意識

- 缺乏業界標準

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

第5章 市場區隔

- 按類型

- 堵塞

- 文件

- 目的

- 超融合基礎設施

- 按公司規模

- 中小企業

- 大型企業

- 按最終用戶

- BFSI

- 通訊和 IT

- 政府

- 其他最終用戶

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 南美洲

- 中東和非洲

第6章 競爭格局

- 公司簡介

- IBM Corporation

- Oracle Corporation

- Netapp Inc.

- Huawei Technologies Co. Ltd

- Fujitsu Limited

- Genetec Inc.

- VMWare Inc.(Dell Inc.)

- Hitachi Vantara Corp.

- Pure Storage Inc.

- Promise Technology Inc.

- FalconStor Software Inc.

第7章投資分析

第8章 市場展望

The Software Defined Security Market is expected to register a CAGR of 33.81% during the forecast period.

Key Highlights

- Software-defined storage (SDS) is one of the new technologies trending in the enterprise storage market. SDS is part of a larger ecosystem where the software is separated from its respective hardware, revealing the freedom to choose installed hardware depending on the amount of storage needed. SDS enables cost savings while improving performance and flexibility. Thus, enterprises are slowly shifting toward software-defined storage.

- Multiple associations shape how SDS is employed across end-user industries with direct connections to major vendors, most of which are involved in similar endeavors. The Storage Network Industry Association (SNIA) sets standards for the enterprise storage industry. The established storage vendors include IBM, Dell EMC, NetApp, and emerging players, like Atlantis Computing and Falcon Star. Some offer software, like NetApp, IBM, and RedHat, while others offer hyper-converged solutions, like HPE and Dell EMC. Others, like Cisco, offer hardware and partner with SDS software vendors.

- An increase in government regulations and standards for data security, as achieved through the use of cybersecurity solutions and the installation of software, is expected to provide attractive prospects for cyber solutions in the next years. Telstra will expand its new cyber security solutions for federal, state, and municipal governments in Australia in February 2022. The Cyber Detection and Response capacity integrates with government systems and cloud-based services to monitor cyber threats using big data analytics from Telstra's managed security service platform, while Sovereign SecureEdge assists in delivering cloud security, especially in the context of a distributed workforce.

- These online security procedures are meant to ensure safety. To avoid any danger or attack, regulating genuine foundations, present frameworks should be isolated, observed, and guaranteed. Dangers associated with network security are growing, aided by the widespread use and accessibility of cloud companies such as Amazon Web Services for storing sensitive and unique data, which is expected to hinder market growth.

- Over the pandemic, software-defined storage has proven invaluable in rapidly expanding its customer base and accelerating top-line growth. For businesses during COVID-19 that continued to see unabated growth in storage but were unable to scale their Kubernetes container-based data management, there has been constant development primed toward enabling integrational capabilities across the platform case point, the previously mentioned NetApp addition of Kubernetes capability.

Software Defined Security Market Trends

Cloud is Driving Software Defined Security

- There has been a strong shift from a few years ago when most information security professionals saw the cloud as limited and secure. The cloud is now seen as transformational rather than a possible security posture tradeoff, threatening security hardware and infrastructure players, who have profited from growing cyber threats and expanding increasingly connected networks. The cloud may prove to be the driver of security transformation.

- Cloud infrastructure is designed to meet new, emerging needs, particularly in terms of vertical and horizontal scale and security. Cloud settings will typically employ technology and service-centric security solutions that can scale worldwide and smoothly without regard to location.

- Cloud computing has revolutionized how businesses utilize, distribute, and store data, apps, and workloads. It has, however, generated various new security concerns and problems. The risk grows with so much data and public cloud services being stored in the cloud. Several nations, primarily emerging economies, are at the forefront of cloud adoption, aided by end-user demand for digitization. Interconnection bandwidth capacity has been expanding due to increased demand from content, edge services, and last-mile connections to transport-led growing data volumes.

- According to Equinix's Global Interconnection Index (GXI) report, the LATAM region is predicted to dominate interconnection bandwidth capacity installation development by a 50% CAGR, with firms operating in the region contributing 1,479 Tbps by 2023. As the potential of cloud demand grows, several providers are experiencing an increase in adoption, which is driving expenditures.

- Moreover, digitalization will add to cloud delivery pressures and force IT into more software and services and away from hardware-defined tradeoffs. This factor, coupled with buyer consolidation and commoditization, will make infrastructure-as-a-service (IaaS) and managed service providers powered by software-defined abilities much more powerful than conventional hardware vendors. Therefore, due to such determinants, software-defined technologies are predicted to grow in the coming years.

Asia-Pacific Accounts for the Fastest Growing Share in the Software-defined Security Market

- Asia-Pacific is experiencing a rapid increase in the volume of unstructured data across various enterprises in the region, which is stored not only on-premise but also in cloud environments. In addition, with the proliferation of IoT across the region, the data generated at the edge is rapidly increasing. These factors have supported a scalable, reliable, secure storage architecture.

- With high-density countries like China and India still relying on traditional hardware for their storage and the need for digital transformation to keep up with the technological changes, the region presents lucrative business for software-defined storage (SDS) vendors.

- Furthermore, the increasing cyberattacks have compelled China to bolster its defense capabilities. However, the country is also a significant source of origin for cyberattacks in other regions of the world.

- In March 2022, cybersecurity firm Mandiant alleged that a Chinese government-backed hacking organization hacked local government entities in the United States as part of an intelligence-gathering operation. According to the US authorities, the hackers utilized a significant software defect to access the networks of two states' agencies in December 2021. According to the FBI and the US Cybersecurity and Infrastructure Security Agency (CISA), the state agencies targeted included transportation, health, higher education, agricultural, court networks, and systems.

- In particular, hyper-scale and international digital media content providers and public cloud service providers, like Facebook, Google Amazon Web Services (AWS), and Alibaba Cloud, have been fundamental in pushing demand for remote storage services, significantly enhancing their uptake of data center capacity in the Asian region and particularly in Hong Kong over the past few years by building massive-scale platforms.

Software Defined Security Industry Overview

The software-defined security market is highly fragmented, as several cyber threats are forcing governments and respective industries to invest more in cyberspace. Increasing investments drive many new players to offer solutions at lower prices, making the market more competitive. Some key players in the market are Pure Storage Inc., Huawei Technologies Co. Ltd, VMWare Inc. (Dell Inc.), Oracle Corporation, and IBM Corporation. These players constantly innovate and upgrade their product offerings to cater to the increasing market demand.

- January 2023 - Valeo, a top automobile supplier, and global partner, and C2A Security, a leading supplier of automatic vehicle cybersecurity solutions for integrated, autonomous, and EVs, announced a strategic collaboration to augment Valeo's cybersecurity services on their product lines in development and ongoing operations. The new collaboration responds to the industry's requirement for simplified and effective cybersecurity. The collaboration of C2A Security and Valeo will enable the automotive sector to deploy automated cybersecurity, putting security first while allowing innovation and future business.

- October 2022 - Veracode, a leading global supplier of applications security testing tools, announced that its Continuous Software Security Platform had been enhanced to incorporate container safety. Existing customers can now participate in an early access initiative for Veracode Container Security. The new Veracode Container Security service covers the secure configuration, vulnerability scanning, and secrets management systems for container images and is intended to satisfy the demands of cloud-native software engineering teams.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Market Drivers

- 4.3.1 Requirement for Quicker Response and Increased Security

- 4.3.2 Rise in Cloud Services Adoption

- 4.4 Market Restraints

- 4.4.1 Lack of Security Awareness in Virtualization Environment

- 4.4.2 Industry Standard Deficiency

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of the Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Block

- 5.1.2 File

- 5.1.3 Object

- 5.1.4 Hyper-converged Infrastructure

- 5.2 By Size of Enterprise

- 5.2.1 Small and Medium Enterprise

- 5.2.2 Large Enterprise

- 5.3 By End User

- 5.3.1 BFSI

- 5.3.2 Telecom and IT

- 5.3.3 Government

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Oracle Corporation

- 6.1.3 Netapp Inc.

- 6.1.4 Huawei Technologies Co. Ltd

- 6.1.5 Fujitsu Limited

- 6.1.6 Genetec Inc.

- 6.1.7 VMWare Inc. (Dell Inc.)

- 6.1.8 Hitachi Vantara Corp.

- 6.1.9 Pure Storage Inc.

- 6.1.10 Promise Technology Inc.

- 6.1.11 FalconStor Software Inc.