|

市場調查報告書

商品編碼

1641863

先進複合材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Advanced Composite Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

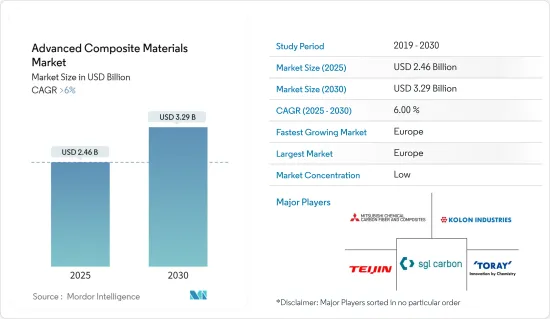

先進複合材料市場規模預計在 2025 年為 24.6 億美元,預計到 2030 年將達到 32.9 億美元,在預測期內(2025-2030 年)的複合年成長率將超過 6%。

COVID-19 疫情對先進複合材料市場產生了不利影響。全國範圍的封鎖和嚴格的社交距離措施導致飛機和汽車製造工廠關閉,從而影響了先進複合材料市場。然而,在新冠疫情過後,限制措施解除後市場已恢復良好。由於航太和國防、風力發電和汽車終端用戶產業對先進複合材料的消費增加,市場出現強勁復甦。

航太和國防工業對輕量材料的需求不斷增加以及對省油和輕型汽車的需求不斷成長預計將推動市場的發展。

預計原物料價格上漲將阻礙市場成長。

預計預測期內先進複合材料的回收和奈米複合材料的需求不斷增加將為市場創造機會。

預計北美地區將佔據市場主導地位。此外,航太和國防、風力發電、汽車和船舶終端用戶產業對先進複合材料的需求不斷增加,預計在預測期內將出現最高的複合年成長率。

先進複合材料的市場趨勢

航太和國防終端用戶產業佔據市場主導地位

- 航太工業對複合材料的需求日益增加。民用運輸飛機大量使用複合材料,因為減輕飛機重量可以提高燃油效率,從而降低營運成本。

- 先進複合材料具有多種熱性能和化學性能,包括高強度、高剛性、耐熱性、耐化學性、導電性等。因此,航太和國防工業擴大使用先進的複合材料。

- 根據國際航空運輸協會(IATA)的預測,2021年全球商業航空收入預計將達到4,720億美元,2022年預計將達到7,270億美元,與前一年同期比較增43.6%。預計到 2023年終將達到 7,790 億美元。由於這些因素,預計未來幾年航太零件製造對先進複合材料的需求將會增加。

- 全球最大飛機製造商之一波音公司宣布,2022年總合交付480架飛機,較2021年全球整體總合架飛機成長41%。因此,預計新飛機交付的增加將推動對先進複合材料的需求。

- 美國是北美的飛機製造地。空中巴士和波音是全國最大的飛機製造商。例如,2022年,空中巴士交付了661架民航機,截至年終的新訂單為1,078架。同樣,波音公司已訂單57 架 737 Max 8噴射機,預計將於 2025 年交付。因此,預計飛機需求的增加將推動先進複合材料市場的發展。

- 在歐洲,尤其是法國和德國等國家的飛機產量不斷增加,預計將推動對先進複合材料的需求。 2023 年 5 月,飛機製造商 VoltAero 宣布計畫在法國建立混合動力飛機製造工廠。因此,該地區新飛機產量的增加將推動該地區對先進複合材料的需求。

- 許多國家都致力於發展國內國防工業,同時也當地生產硬體。預計這些因素將在預測期內推動對先進複合材料的需求。因此,由於上述因素,預計航太和國防應用領域將在預測期內佔據市場主導地位。

北美佔據市場主導地位

- 預計預測期內北美地區將主導先進複合材料市場。美國、加拿大和墨西哥等國家在航太和國防、汽車和電子工業領域對先進複合材料的需求日益增加。

- 根據美國運輸統計局的資料,2022年美國航空公司的客運量將達到8.53億人次,較2021年的6.74億人次成長率為30%。因此,一些航空公司正在擴大持有並採購具有先進功能的飛機,以滿足日益成長的航空旅行需求。例如,2022年2月,美國航空向波音公司訂購了30架737 Max 8。因此,預計民航機需求的不斷成長將推動當前的研究市場。

- 在北美,尤其是美國,電子產業預計將經歷溫和成長。預計未來幾年對新技術產品的需求不斷增加將有助於市場擴張。

- 在美國,電子產業技術進步和研發活動創新步伐的加快,導致對更新、更快的電子產品的需求增加。據美國消費技術協會稱,美國家用電子電器技術銷售的零售收入預計將在 2022 年達到 5,050 億美元,而 2021 年為 4,610 億美元。

- 據美國先進醫療技術協會(AMTA)稱,美國醫療技術公司在為患者診斷和提供優質治療方法、改善健康結果、降低醫療成本和推動經濟成長方面發揮著至關重要的作用。美國是全球最大的醫療設備市場,佔全球醫療設備市場的40%以上。

- 根據OICA預測,2022年美國汽車產量將從2021年的915萬輛達到1,006萬輛,成長率為9%。因此,預計汽車產量的增加將推動該地區先進複合材料市場的發展。

- 由於這些因素,該地區先進複合材料市場預計將在預測期內實現成長率。

先進複合材料產業概況

先進複合材料市場較為分散。市場的主要企業包括東麗工業公司、可隆工業公司、西格里碳素公司、三菱化學碳纖維及複合材料公司和帝人株式會社(不分先後順序)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 航太和國防工業對輕量材料的需求不斷增加

- 省油、輕量化汽車的需求日益增加

- 其他促進因素

- 限制因素

- 原物料價格上漲

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 複合材料類型

- 陶瓷基質材料 (CMC)

- 金屬複合材料(MMC)

- 聚合物基複合材料 (PMC)

- 核心材質

- 光纖類型

- 醯胺纖維

- 玻璃纖維

- 碳纖維

- 最終用戶產業

- 航太和國防

- 風力發電

- 運輸

- 海洋

- 消費品

- 其他最終用戶產業(醫療、電子等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3B-the fibreglass company

- Dow

- Henkel Corporation

- Hexcel Corporation

- HYOSUNG ADVANCED MATERIALS

- Kolon Industries Inc.

- Mitsubishi Chemical Carbon Fiber and Composites Inc.

- Owens Corning

- SGL Carbon

- Solvay

- TEIJIN LIMITED

- Toray Industries Inc.

- Yantai Tayho Advanced Materials Co. Ltd

第7章 市場機會與未來趨勢

- 先進複合材料的回收利用

- 奈米複合材料的需求不斷增加

The Advanced Composite Materials Market size is estimated at USD 2.46 billion in 2025, and is expected to reach USD 3.29 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The COVID-19 pandemic had negatively impacted the market for advanced composite materials. The nationwide lockdowns and strict social distancing measures resulted in the closure of airplane and automotive manufacturing facilities, thereby affecting the market for advanced composite materials. However, post-COVID pandemic, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of advanced composite materials in aerospace and defense, wind energy, and automotive end-user industries.

The increasing demand for lightweight materials in the aerospace and defense industries and the rising demand for fuel-efficient and lightweight vehicles are expected to drive the market.

The increasing prices of raw materials are expected to hinder the market's growth.

The recycling of advanced composites and the increasing demand for nanocomposites are expected to create opportunities for the market during the forecast period.

The North American region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for advanced composite materials in aerospace and defense, wind energy, automotive, and marine end-user industries.

Advanced Composite Materials Market Trends

Aerospace and Defense End-user Industry to Dominate the Market

- The demand for composite materials is increasing in the aerospace industry. The use of composite materials in commercial transport aircraft is massive because reduced airframe weight enables better fuel economy and, therefore, lowers operating costs.

- The advanced composite materials include high strength, stiffness, heat and chemical resistivity, electrical conductivity, and various other thermal and chemical properties. Thus, the usage of advanced composites is increasing in the aerospace and defense industry.

- According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 472 billion in 2021 and USD 727 billion in 2022, registering a growth rate of 43.6% Y-o-Y. Furthermore, the revenue is expected to reach USD 779 billion by the end of 2023. Such factors are likely to increase the demand for advanced composite materials from aerospace parts manufacturing in the years to come.

- Boeing, one of the largest global aircraft manufacturers, announced it delivered a total of 480 aircraft in 2022, which is an increase of 41% compared to the total of 340 aircraft across the world in 2021. Thus, the increasing deliveries of new aircraft are expected to drive the demand for advanced composites.

- The United States is the manufacturing hub for airplanes in the North American region. Airbus and Boeing are the largest manufacturers of airplanes in the country. For instance, in 2022, Airbus delivered 661 commercial aircraft, registering 1,078 gross new orders by the end of the year. Similarly, Boeing Aeroplane OEM company received orders for 57 of the 737 Max 8 jets, with delivery expected through 2025. Thus, the increasing demand for airplanes is expected to drive the market for advanced composite materials.

- In Europe, the rising production of aircraft, mainly in countries such as France and Germany, is expected to drive the demand for advanced composite materials. In May 2023, VoltAero, an aircraft manufacturer, announced plans to build a manufacturing facility for hybrid-electric aircraft in France. Thus, the increasing production of new aircraft in the region will drive the demand for advanced composites in the region.

- Many countries are focusing on growing a domestic defense industry while manufacturing hardware locally. These factors are expected to drive the demand for advanced composite materials during the forecast period. Hence, owing to the factors mentioned above, the aerospace and defense application segment is expected to dominate the market during the forecast period.

North America Region to Dominate the Market

- The North American region is expected to dominate the market for advanced composite materials during the forecast period. The demand for advanced composite materials is increasing in aerospace and defense, automotive, and electronics industries in countries like the United States, Canada, and Mexico.

- According to data from the Bureau of Transportation Statistics, airlines in the United States carried 853 million passengers in 2022 at a growth rate of 30% compared to 674 million passengers in 2021. Thus, several airline companies are expanding their fleet and procuring aircraft with advanced capabilities to cater to the increasing demand for air passengers. For instance, in February 2022, American Airlines ordered 30 new 737 Max 8 jets from Boeing. Thus, the rising demand for commercial airplanes is expected to drive the current studied market.

- In North America, especially in the United States, the electronics industry is expected to grow at a moderate rate. An increase in the demand for new technological products is expected to help the market expansion in the future.

- In the United States, the rapid pace of innovation in terms of the advancement of technologies and R&D activities in the electronics industry is driving the demand for newer and faster electronic products. According to the Consumer Technology Association, the retail revenue from consumer electronics and technology sales in the United States was estimated at USD 505 billion in 2022, compared to USD 461 billion in 2021.

- According to the Advanced Medical Technology Association (AMTA), America's medical technology companies play a crucial role in diagnosing and providing patients with quality treatment options, improving outcomes, reducing healthcare costs, and driving economic growth. The United States is the world's largest medical device market, accounting for over 40% of the global medical device market.

- According to OICA, in 2022, the United States automotive vehicle production reached 10.06 million compared to 9.15 million units manufactured in 2021, at a growth rate of 9%. Thus, the rise in vehicle production will drive the market for advanced composite materials in the region.

- Due to all such factors, the market for advanced composite materials in the region is expected to register a growth rate during the forecast period.

Advanced Composite Materials Industry Overview

The advanced composite materials market is fragmented in nature. Some of the major players in the market include (not in any particular order) TORAY INDUSTRIES INC., Kolon Industries Inc., SGL Carbon, Mitsubishi Chemical Carbon Fiber and Composites Inc., and TEIJIN LIMITED.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Lightweight Materials in the Aerospace and Defense Industry

- 4.1.2 Rising Demand for Fuel Efficient and Lightweight Vehicles

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Prices of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Composite Type

- 5.1.1 Ceramic Matrix Composites (CMCs)

- 5.1.2 Metal Matrix Composites (MMCs)

- 5.1.3 Polymer Matrix Composites (PMCs)

- 5.1.4 Core Materials

- 5.2 Fiber Type

- 5.2.1 Aramid Fiber

- 5.2.2 Glass Fiber

- 5.2.3 Carbon Fiber

- 5.3 End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Wind Energy

- 5.3.3 Transportation

- 5.3.4 Marine

- 5.3.5 Consumer Goods

- 5.3.6 Other End-user Industries (Medical, Electronics, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 UAE

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3B - the fibreglass company

- 6.4.2 Dow

- 6.4.3 Henkel Corporation

- 6.4.4 Hexcel Corporation

- 6.4.5 HYOSUNG ADVANCED MATERIALS

- 6.4.6 Kolon Industries Inc.

- 6.4.7 Mitsubishi Chemical Carbon Fiber and Composites Inc.

- 6.4.8 Owens Corning

- 6.4.9 SGL Carbon

- 6.4.10 Solvay

- 6.4.11 TEIJIN LIMITED

- 6.4.12 Toray Industries Inc.

- 6.4.13 Yantai Tayho Advanced Materials Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Recycling Advanced Composites

- 7.2 Increasing Demand for Nano Composites

全球先進複合材料市場:市場規模、市場佔有率、趨勢、產業分析(依纖維類型、製造流程、最終用途和地區)、未來預測(2025-2034年)

全球先進複合材料市場:市場規模、市場佔有率、趨勢、產業分析(依纖維類型、製造流程、最終用途和地區)、未來預測(2025-2034年) 纖維纏繞複合材料市場-2025年至2030年的預測先進複合材料的全球市場(2018年~2034年)

纖維纏繞複合材料市場-2025年至2030年的預測先進複合材料的全球市場(2018年~2034年) 高性能複合材料市場:按纖維、樹脂類型、製造流程和應用分類的全球預測 - 2025-2030

高性能複合材料市場:按纖維、樹脂類型、製造流程和應用分類的全球預測 - 2025-2030 先進複合材料市場規模、佔有率、成長分析,按纖維類型、樹脂類型、地區分類 - 產業預測,2024-2031

先進複合材料市場規模、佔有率、成長分析,按纖維類型、樹脂類型、地區分類 - 產業預測,2024-2031 先進複合材料市場機會、成長動力、產業趨勢分析及 2024 年至 2032 年預測先進複合材料市場規模、佔有率、趨勢分析報告:按產品、按應用、按樹脂類型、按地區、細分市場預測,2024-2030全球先進複合材料市場 - 2023-2030

先進複合材料市場機會、成長動力、產業趨勢分析及 2024 年至 2032 年預測先進複合材料市場規模、佔有率、趨勢分析報告:按產品、按應用、按樹脂類型、按地區、細分市場預測,2024-2030全球先進複合材料市場 - 2023-2030