|

市場調查報告書

商品編碼

1641864

聚丁二烯橡膠 (PBR):市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Polybutadiene Rubber (PBR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

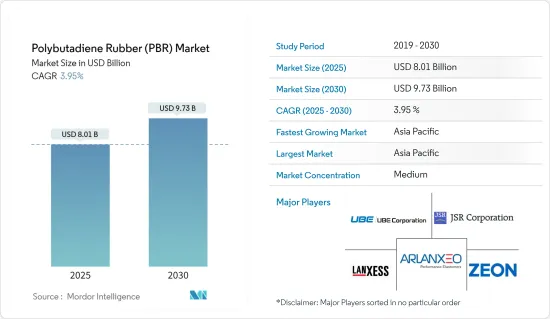

聚丁二烯橡膠(PBR) 市場規模估計並預測到2025 年將達到80.1 億美元,預計到2030 年將達到97.3 億美元,在預測期內(2025-2030 年)的複合年成長率為3.95% 。

COVID-19 疫情對聚丁二烯橡膠市場產生了不利影響。全國範圍的封鎖和嚴格的社交距離措施導致汽車生產陷入停滯,從而影響了聚丁二烯橡膠市場。然而,在新冠疫情爆發後,一旦限制措施解除,市場就恢復良好。由於輪胎製造、鞋類和運動配件應用對聚丁二烯橡膠的需求增加,市場出現強勁復甦。

關鍵亮點

- 汽車行業需求的不斷成長和合成橡膠行業的成長預計將推動聚丁二烯橡膠市場的發展。

- 嚴格的環境法規和有關接觸聚丁二烯的健康問題預計將阻礙市場的成長。

- 預計消費者即將轉向電動車,這將在預測期內為市場創造機會。

- 預計亞太地區將主導市場。此外,輪胎製造、鞋類和運動配件應用對聚丁二烯橡膠的需求不斷增加,預計在預測期內將實現最高的複合年成長率。

聚丁二烯橡膠市場趨勢

輪胎製造應用領域佔據市場主導地位

- 丁二烯用於製造合成橡膠和合成橡膠,例如聚丁二烯橡膠 (PBR)、苯乙烯-丁二烯橡膠(SBR)、丁腈橡膠 (NR) 和聚氯丁二烯 (氯丁橡膠)。

- PBR用於製造輪胎。聚丁二烯主要用於生產汽車輪胎。據估計,輪胎製造過程消耗了全球70%以上的聚丁二烯產量。聚丁二烯主要用於輪胎側壁,以減少駕駛過程中不斷彎曲造成的疲勞。丁二烯也用於多種其他汽車零件。

- 在美國和其他國家,輪胎出貨量正在增加,推動了聚丁二烯橡膠市場的發展。根據美國輪胎工業協會 (USTMA) 的數據,預計 2023 年輪胎總出貨量將達到 3.342 億條,而 2022 年為 3.32 億條,2019 年為 3.327 億條。

- 此外,根據美國輪胎工業協會(USTMA)的數據,2023年乘用車輪胎、輕型卡車輪胎和卡車輪胎的OEM(原始設備)出貨量預計將變化2.3%、1.3%和-0.6%。總合銷量將增加100萬台。因此,汽車OEM產業不斷成長的需求正在推動當前的研究市場的發展。

- 汽車產量的增加推動了用於輪胎製造的聚丁二烯橡膠市場的發展。根據OICA預測,2022年全球汽車產量將達8,500萬輛,而2021年為8,020萬輛,成長率為6%。中國、美國和印度是全球最突出的汽車市場。

- 近年來對電動車的需求不斷增加以及消費者即將轉向電動車,預計將在預測期內為聚丁二烯橡膠 (PBR) 輪胎創造商機。在歐洲,德國、英國等國的電動車產量正在增加。

- 在德國,汽車製造商正在大力投資電動車的生產。例如,2023年6月,福特宣布科隆電動車中心正式落成,這是位於德國的高科技生產工廠,將為數百萬歐洲客戶生產福特新一代電動乘用車。根據福特介紹,科隆中心的年產能將達到25萬輛電動車。因此,預計電動車產量的增加將推動當前的研究市場。

- 因此,預計輪胎製造應用領域將在預測期內佔據市場主導地位。

亞太地區佔市場主導地位

- 預計預測期內亞太地區將主導聚丁二烯橡膠市場。由於輪胎製造、工業橡膠製造和鞋類等應用的需求不斷增加,預計中國、印度和日本等國家市場將呈指數級成長。

- 中國是全球產銷最大的汽車市場。根據國際汽車結構組織(OICA)預測,2022年中國汽車產量將達2,702萬輛,較2021年同期成長3%。

- 在中國,隨著消費者擴大轉向電池驅動的汽車,汽車產業正在經歷趨勢的轉變。根據乘聯會的預測,2022年電動車和插電式汽車銷量將達到567萬輛,較2021年成長近一倍。這些趨勢將增加該國對汽車輪胎的需求,推動目前研究的市場發展。

- 此外,根據中國橡膠工業協會的數據,到2025 年,中國輪胎年產量預計將達到7.04 億條,其中包括5.27 億條乘用車子午線輪胎和5.27 億條一次性輪胎。 148% 。 5.4萬條。因此,預計該國對聚丁二烯橡膠的需求將會成長。

- 印度也是亞太地區最大的橡膠生產國和消費國之一。印度橡膠產業由橡膠生產部門和快速成長的橡膠製品製造和消費部門組成。

- 根據汽車輪胎工業協會 (ATMA) 的數據,到 2032 會計年度,印度輪胎產業的收益預計將達到 220 億美元,而 2022 會計年度為 90 億美元。因此,預計輪胎需求的增加將推動所研究市場的發展。

- 在印度,大約12%的橡膠用於鞋類生產。國際品牌的滲透加上都市化正在推動該國鞋類市場的發展。印度政府正在「印度製造」計畫下大力推動製鞋業的發展。目前,其鞋類產量約佔全球年產量的 9%。印度的製鞋業是該地區繼中國之後最大的製鞋業之一。

- 由於這些因素,該地區的聚丁二烯橡膠市場預計將在預測期內成長。

聚丁二烯橡膠產業概況

聚丁二烯橡膠市場部分整合。市場的主要企業包括(不分先後順序)ENEOS Materials Corporation、Arlanxeo、Zeop Co.、Lanxees 和 UBE Co.

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 汽車產業需求增加

- 合成橡膠工業的成長

- 其他促進因素

- 限制因素

- 嚴格的環境法規

- 接觸聚丁二烯的健康問題

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 應用

- 輪胎製造

- 鞋類

- 運動配件

- 其他應用(化學、聚合物改質等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 俄羅斯

- 北歐國家

- 土耳其

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- ARLANXEO

- Indian Oil Corporation Ltd

- ENEOS Materials Corporation

- KUMHO PETROCHEMICAL

- LANXESS

- LG Chem

- Reliance Industries Limited

- SABIC

- SIBUR International GmbH

- Synthos

- Trinseo

- UBE Corporation

- THE YOKOHAMA RUBBER CO., LTD

- ZEON CORPORATION

- KURARAY CO., LTD.

- Versalis SpA

第7章 市場機會與未來趨勢

- 未來消費者將轉向電動車

- 其他機會

The Polybutadiene Rubber Market size is estimated at USD 8.01 billion in 2025, and is expected to reach USD 9.73 billion by 2030, at a CAGR of 3.95% during the forecast period (2025-2030).

The COVID-19 pandemic had negatively impacted the market for polybutadiene rubber market. The nationwide lockdowns and strict social distancing measures had resulted in a halt in automotive vehicle manufacturing, thereby affecting the market for polybutadiene rubber. However, post-COVID pandemic, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in demand for polybutadiene rubber in tire manufacturing, footwear, and sports accessories applications.

Key Highlights

- The increasing demand from the automobile industry and the growth in the synthetic rubber industry are expected to drive the polybutadiene rubber market.

- The stringent environmental regulations and the health concerns regarding exposure to polybutadiene are expected to hinder the market's growth.

- The upcoming consumer shift to electric vehicles is expected to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for polybutadiene rubber in tire manufacturing, footwear, and sports accessories applications.

Polybutadiene Rubber Market Trends

Tire Manufacturing Application Segment to Dominate The Market

- Butadiene is used in the manufacturing of synthetic rubbers and elastomers that include polybutadiene rubber (PBR), styrene-butadiene rubber (SBR), nitrile rubber (NR), and polychloroprene (Neoprene), all of which are used in the production of other goods and materials.

- PBR is used in the manufacturing of tires. Polybutadiene is primarily utilized in the production of automotive tires. It is estimated that the tire manufacturing process consumes over 70% of the world's polybutadiene production. It is primarily utilized in tires as a sidewall to reduce fatigue caused by continual flexing throughout the run. Butadiene is also used in a variety of other automotive components.

- In countries like the United States, the shipment of tires is increasing, which is driving the market for Polybutadiene rubber. According to the U.S. Tire Manufacturers Association (USTMA), the total shipments of tires are expected to reach 334.2 million units in 2023, as compared to 332.0 million units in 2022 and 332.7 million units in 2019.

- Furthermore, according to the U.S. Tire Manufacturers Association (USTMA), in 2023, Original Equipment (OE) shipments for passenger, light truck, and truck tires are expected to change by 2.3%, 1.3% and -0.6%, respectively, with a total increase of 1.0 million units. Thus, the increasing demand for automotive OEM industries will drive the current studied market.

- The increasing production volume of automotive vehicles is driving the market for Polybutadiene Rubber used in tire manufacturing. According to OICA, global automotive vehicle production reached 85 million in 2022, as compared to 80.2 million manufactured in 2021, at a growth rate of 6%. China, the United States, and India are the most prominent automotive vehicle markets globally.

- The rising demand for electric vehicles in recent years, as well as an impending consumer shift to electric vehicles, are expected to provide opportunities for polybutadiene rubber (PBR) tires during the forecast period. In Europe, the production volume of electric vehicles is increasing in countries like Germany and the United Kingdom.

- In Germany, automakers are investing heavily in producing electric vehicles in the country. For instance, In June 2023, Ford announced the inauguration of the Cologne Electric Vehicle Center, a hi-tech production facility in Germany that will build Ford's new generation of electric passenger vehicles for millions of European customers. According to Ford, the Cologne Center has an annual production capacity of 250,000 electric vehicles. Thus, the increasing production of electric vehicles is expected to drive the current studied market.

- Thus, the tire manufacturing application segment to dominate the market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for polybutadiene rubber during the forecast period. In countries like China, India, and Japan, the market is expected to grow exponentially owing to the increasing demand from applications such as tire manufacturing, industrial rubber manufacturing, and footwear.

- China is the world's biggest automobile market in terms of both production and sales. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), vehicle production in China reached a total of 27.02 million units in 2022, which is an increase of 3% over 2021 for the same period.

- In China, the automotive industry is witnessing switching trends as the consumer inclination toward battery-operated vehicles is higher. As per the China Passenger Car Association, the country sold 5.67 million EVs and plug-ins in 2022, almost double the sales figures achieved in 2021. These trends will increase the demand for automotive tires in the country, thereby driving the current studied market.

- Furthermore, according to the China Rubber Industry Association (CRIA), the country is projected to produce 704 million tires per year by 2025, including 527 million passenger radial tires, 148 million truck/bus radial tires, 29 million bias truck tires, 20,000 extra-large industrial tires, 12 million agricultural tires, and 54,000 aircraft tires. Thus, the demand for polybutadiene rubber is expected to grow in the country.

- India is also one of the largest producers and consumers of rubber in the Asia-Pacific region. The Indian rubber industry exhibits the co-existence of the rubber production sector and the fast-growing rubber products manufacturing and consuming sector.

- According to the Automotive Tire Manufacturers' Association (ATMA), the Indian tire industry revenue is expected to reach USD 22 billion by FY 2032, as compared to USD 9 billion registered in FY 2022. Thus, the increase in demand for tires is expected to drive the market for the current studied market.

- In India, about 12% of rubber is used to produce footwear. The penetration of international brands, coupled with urbanization, has driven the footwear market in the country. The government has focused on the footwear industry under the 'Make in India' initiative. The country is currently producing around 9% of the global annual production of footwear. The footwear sector in India is one of the largest in the region, behind China.

- Due to all such factors, the market for polybutadiene rubber in the region is expected to grow during the forecast period.

Polybutadiene Rubber Industry Overview

The polybutadiene rubber market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) ENEOS Materials Corporation, Arlanxeo, Zeop Co., Lanxees, and UBE Co., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand From the Automobile Industry

- 4.1.2 Growth in the Synthetic Rubber Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Enviornmental Regulations

- 4.2.2 Health Concerns Regarding Exposure to Polybutadiene

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Tire Manufacturing

- 5.1.2 Footwear

- 5.1.3 Sports Accessories

- 5.1.4 Other Applications (Chemicals, Polymer Modification, etc.)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Indonesia

- 5.2.1.6 Malaysia

- 5.2.1.7 Thailand

- 5.2.1.8 Vietnam

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Russia

- 5.2.3.7 NORDIC Countries

- 5.2.3.8 Turkey

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Qatar

- 5.2.5.4 UAE

- 5.2.5.5 Nigeria

- 5.2.5.6 Egypt

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ARLANXEO

- 6.4.2 Indian Oil Corporation Ltd

- 6.4.3 ENEOS Materials Corporation

- 6.4.4 KUMHO PETROCHEMICAL

- 6.4.5 LANXESS

- 6.4.6 LG Chem

- 6.4.7 Reliance Industries Limited

- 6.4.8 SABIC

- 6.4.9 SIBUR International GmbH

- 6.4.10 Synthos

- 6.4.11 Trinseo

- 6.4.12 UBE Corporation

- 6.4.13 THE YOKOHAMA RUBBER CO., LTD

- 6.4.14 ZEON CORPORATION

- 6.4.15 KURARAY CO., LTD.

- 6.4.16 Versalis S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Upcoming Consumer Shift to Electric Vehicles

- 7.2 Other Opportunities