|

市場調查報告書

商品編碼

1641897

錳:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Manganese - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

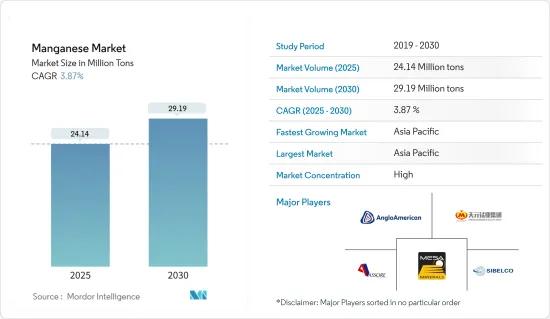

預計2025年錳市場規模為2,414萬噸,預計2030年將達2919萬噸,預測期內(2025-2030年)複合年成長率為3.87%。

在2020年的疫情中,政府為遏制新的 COVID-19 病例蔓延而實施的封鎖措施導致建設活動暫時停止,導致建設產業對鋼鐵的需求下降。然而,考慮到疫情過後的情況,建設產業正在恢復步伐,未來幾年市場需求可能會增加。

主要亮點

- 短期內,由於電動車需求不斷成長,鋰離子電池生產對錳的需求預計將推動市場成長。

- 相反,政府限制政策和日益嚴重的環境問題所帶來的不利條件預計會阻礙市場成長。

- 然而,電池中錳的使用可能為全球市場提供豐厚的成長機會。

- 預計亞太地區將主導市場,並在預測期內以最高的複合年成長率成長。

錳市場趨勢

建築業需求增加

- 錳用於鋼是因為它可以提高鋼的淬硬性和抗張強度。全球超過40%的鋼材用於建築領域,包括建築應用(結構型材、鋼筋、板材產品、非結構鋼等)、基礎設施和交通運輸。

- 錳也能作為溫和的氧化劑。鋼鐵也用於海上石油鑽井平台、橋樑、土木工程施工機械、壓力容器、發電廠和水力發電廠。

- 預計到 2030 年,全球建築業規模將達到約 12.9 兆美元,主要由印度、中國和美國等國家推動。

- 中國建設產業看起來不穩定,因為它正在應對恆大危機(截至 2021 年 6 月,該公司的債務就高達 3000 億美元),並正處於全面爆發的中國金融危機和景氣衰退的邊緣。不容否認。

- 在美國,總統拜登宣布了一項計劃,將在2021年投入2兆美元,將國家基礎設施改造成綠色產業。

- 至2025年,印度建築市場產出預計將以年均7.1%的速度成長。此外,預計2030年印度房地產產業產值將達到1兆美元,對GDP的貢獻率將達到13%。

亞太地區佔市場主導地位

- 由於中國、印度和日本等國家的需求不斷成長,亞太地區在全球市場佔據主導地位。

- 近年來,快速的都市化導致新建設計劃的投資增加,尤其是在開發中國家。亞太地區佔全球建築業投資的大部分,主要受中國、印度、日本和東南亞國協投資增加的推動。

- 基礎設施建設活動的增加以及歐盟大型公司進入利潤豐厚的中國市場進一步刺激了該行業的擴張。

- 印度建築業貢獻了國內生產毛額的9%左右。印度建設產業透過自動途徑允許 100% 的外國直接投資,可以投資於已完工的城鎮、商場/購物中心和商業建築的營運和管理計劃。預計這將在預測期內推動該行業的發展。

- 根據中國國家統計局的數據,2021年中國工業生產與前一年同期比較成長約9.6%。此外,2022年10月工業生產年增5.0%,而上個月年增6.3%,刺激了受調查市場的需求。

錳行業概況

錳市場局部盤整。市場上的主要企業(不分先後順序)包括英美資源集團、Assore Limited(Assmang Proprietary Limited)、寧夏天元錳業集團、Mesa Minerals Limited 和 Sibelco。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 電動車需求不斷成長

- 其他促進因素

- 限制因素

- 其他限制因素

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 價格趨勢

- 生產分析

第5章 市場區隔(市場規模:基於數量)

- 按應用

- 合金

- 電解錳

- 電解

- 其他用途

- 按最終用途部門

- 工業

- 建造

- 儲能與電力

- 其他最終用途部門

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Anglo American PLC

- Assore Limited(Assmang Proprietary Limited)

- BHP

- Carus Group Inc.

- Eramet

- Jupiter Mines Limited

- Mesa Minerals Limited

- MOIL LIMITED

- Ningxia Tianyuan Manganese Industry Group Co. Ltd

- NIPPON DENKO CO. LTD

- Sibelco

- Tata Steel

- Vale

第7章 市場機會與未來趨勢

- 錳在電池中的未來用途。

The Manganese Market size is estimated at 24.14 million tons in 2025, and is expected to reach 29.19 million tons by 2030, at a CAGR of 3.87% during the forecast period (2025-2030).

During the pandemic scenario in 2020, construction activities were temporarily stopped during the government-imposed lockdown to curb the spread of new COVID-19 cases, which decreased the demand for steel from the construction industry. However, considering the post-pandemic scenario, the construction industry is picking up the pace which is likely to increase the demand for the market in the coming years.

Key Highlights

- Over the short term, the increasing demand for manganese in lithium-ion battery production, owing to the rising demand for electric vehicles, is expected to drive the market's growth.

- Conversely, unfavorable conditions arising from restrictive governmental policies and growing environmental concerns are expected to hinder market growth.

- Nevertheless, the usage of manganese in batteries is likely to create lucrative growth opportunities for the global market.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Manganese Market Trends

Increasing Demand from Construction Sector

- Manganese is used in steel, as it increases hardenability and tensile strength. Over 40% of the world's steel is used in the construction sector for building applications (structural sections, reinforcing bars, sheet products, non-structural steel, and others), infrastructure, and transportation.

- Manganese also acts as a mild oxidizing agent. Steels are also used in offshore oil rigs, bridges, civil engineering and construction machines, pressure vessels, power plants, and hydroelectric plants.

- The global construction industry is estimated to be about USD 12.9 trillion by 2030, primarily driven by countries such as India, China, and the United States.

- China's construction industry looks shaky as the country is dealing with the Evergrande crisis (the company has USD 300 billion of liabilities alone as of June 2021), and a full-fledged Chinese financial crisis and the effect of recession can't be ruled out.

- In the United States, President Biden introduced a USD 2 trillion plan in 2021 to overhaul and upgrade the nation's infrastructure, into a greener industry.

- By 2025, the Indian construction market output is expected to grow on average by 7.1% each year. Additionally, the real estate industry in India is expected to reach USD 1 trillion by 2030 and contribute to 13% of the GDP.

Asia Pacific to Dominate the Market

- Asia Pacific has dominated the market globally, owing to increasing demand from countries such as China, India, and Japan.

- With rapid urbanization, especially in developing countries, investments in new construction projects have been increasing over recent years. Asia Pacific has dominated the construction sector investments worldwide due to the growth in investments in China, India, Japan, and ASEAN countries.

- Increasing infrastructure construction activities and the entry of major players from the European Union into the lucrative market of China have further fueled the industry's expansion.

- The construction industry in India contributes about 9% of the country's GDP. 100% foreign direct investment in the construction industry in India under automatic route is permitted in completed projects for operations and management of townships, malls/shopping complexes, and business constructions. This is expected to boost the industry in the forecast period.

- According to the National Bureau of Statistics of China, Chinese industrial production increased by about 9.6% in 2021, as compared to the previous year. Furthermore, industrial production increased by 5.0% Y-o-Y in October 2022, following an increase of 6.3% Y-o-Y in the previous month, thereby stimulating the demand for the market studied.

Manganese Industry Overview

The manganese market is partially consolidated in nature. Some of the major players in the market (not in particular order) include Anglo American PLC, Assore Limited (Assmang Proprietary Limited), Ningxia Tianyuan Manganese Industry Group Co. Ltd, Mesa Minerals Limited, and Sibelco, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand of Electric Vehicles

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Price Trends

- 4.6 Production Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Application

- 5.1.1 Alloys

- 5.1.2 Electrolytic Manganese Dioxide

- 5.1.3 Electrolytic Manganese Metals

- 5.1.4 Other Applications

- 5.2 By End-use Sector

- 5.2.1 Industrial

- 5.2.2 Construction

- 5.2.3 Power Storage and Electricity

- 5.2.4 Other End-use Sectors

- 5.3 By Geography

- 5.3.1 Asia Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Anglo American PLC

- 6.4.2 Assore Limited (Assmang Proprietary Limited)

- 6.4.3 BHP

- 6.4.4 Carus Group Inc.

- 6.4.5 Eramet

- 6.4.6 Jupiter Mines Limited

- 6.4.7 Mesa Minerals Limited

- 6.4.8 MOIL LIMITED

- 6.4.9 Ningxia Tianyuan Manganese Industry Group Co. Ltd

- 6.4.10 NIPPON DENKO CO. LTD

- 6.4.11 Sibelco

- 6.4.12 Tata Steel

- 6.4.13 Vale

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Use of Manganese in Electrical Batteries

矽錳市場報告:2031 年趨勢、預測與競爭分析

矽錳市場報告:2031 年趨勢、預測與競爭分析 2030 年錳鐵市場預測:按等級、製造流程、應用、最終用戶、地區進行的全球分析

2030 年錳鐵市場預測:按等級、製造流程、應用、最終用戶、地區進行的全球分析 全球矽錳市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球矽錳市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 全球錳鐵市場:2025 年2025 年全球矽錳市場報告電解二氧化錳市場規模、佔有率、成長分析,按類型、按等級、按電解製程、按應用、按最終用戶、按地區 - 行業預測,2025-2032 年錳市場規模、佔有率和成長分析(按類型、礦石品位、形式、應用、最終用途和地區)- 產業預測 2025-2032

全球錳鐵市場:2025 年2025 年全球矽錳市場報告電解二氧化錳市場規模、佔有率、成長分析,按類型、按等級、按電解製程、按應用、按最終用戶、按地區 - 行業預測,2025-2032 年錳市場規模、佔有率和成長分析(按類型、礦石品位、形式、應用、最終用途和地區)- 產業預測 2025-2032 錳鐵市場規模、佔有率、趨勢分析報告:按等級、按應用、按地區、細分市場預測,2025-2030年碳酸錳市場報告:2030 年趨勢、預測與競爭分析

錳鐵市場規模、佔有率、趨勢分析報告:按等級、按應用、按地區、細分市場預測,2025-2030年碳酸錳市場報告:2030 年趨勢、預測與競爭分析 錳市場:按礦石品位、應用和最終用途分類 - 2025-2030 年全球預測

錳市場:按礦石品位、應用和最終用途分類 - 2025-2030 年全球預測