|

市場調查報告書

商品編碼

1641900

彈道複合材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Ballistic Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

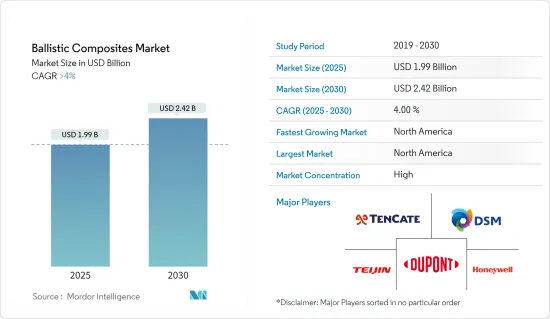

2025 年防彈複合材料市場規模預估為 19.9 億美元,預計到 2030 年將達到 24.2 億美元,預測期內(2025-2030 年)的複合年成長率將超過 4%。

COVID-19 疫情對防彈複合材料市場來說是一個動盪的時期。雖然它帶來了供應鏈中斷、需求波動和經濟不確定性等挑戰,但它也刺激了創新,凸顯了安全和永續性方面的新機遇,並鼓勵製造業採用有益技術。一進程的可能性。儘管疫情的長期影響仍然明顯,但市場的適應能力和對高性能防護材料的持續需求表明未來充滿希望。

主要亮點

- 現代戰爭需要輕便、舒適的防護衣,既要能提供足夠的防彈保護,又不能影響機動性,因此國防和航太工業的需求不斷成長,推動著市場的發展。

- 另一方面,防彈複合材料的加工和製造通常需要複雜且勞力密集的技術。這可能會增加成本並阻礙所研究市場的成長。

- 許多國家的國防費用和預算不斷增加,對防禦彈道威脅的輕量材料的需求不斷增加,這可能會在預測期內帶來機會。

- 北美佔據全球市場主導地位,最大的消費國是美國和加拿大等國家。

彈道複合材料市場趨勢

車輛裝甲需求不斷增加

- 防彈複合材料市場對車輛裝甲的需求正在穩定成長。這背後有許多因素,包括日益成長的安全問題、技術進步和不斷擴大的應用。

- 裝甲運兵車、戰鬥車輛甚至一些軍用卡車擴大使用防彈複合材料進行防護。

- 陸戰車輛受到足以抵禦機關槍射擊和高空砲火的裝甲保護。這些車輛包括一個外部裝甲套件,其中包括玻璃纖維增強支撐板。加固的底盤可以保護車內的人員免受地雷的傷害。外部裝甲設計通常包括由陶瓷面編織芳香聚醯胺製成的模組化擴展裝甲系統面板。屋頂內部採用模製芳香聚醯胺增強複合複合材料製成,內部方面採用模製 S 玻璃纖維增強複合複合材料製成。

- 直升機底部也需要裝甲防護,以抵禦小型武器的地面攻擊。直升機機身需要很輕,因此機身底部通常更容易受到地面小型武器的射擊。這使船員處於危險之中。直升機底部的輕型裝甲已經使用多年。

- 全球戰爭的增加導致軍艦所需軍用車輛的需求增加,這可能會在預測期內增加對車輛裝甲的需求。

- 國防開支和安全預算的增加導致對裝甲車和先進裝甲技術的投資增加。

- 中國的國防工業正在崛起,許多中國公司取代了西方國防強國。該國正在大力投資升級其軍隊,使得 8 家國防相關企業躋身世界前 25 名。

- 目前,中國每年生產軍用飛機約300架。隨著中國軍事工業的不斷發展,中國國產軍用飛機的需求和供應可能會大幅增加。此舉可望帶動中國軍用飛機製造業的快速發展。

- 2021 年 6 月,印尼宣布了另一項計劃,到 2040 年代中期斥資 1,250 億美元升級和現代化其軍隊。總期限包括五個策略計畫期,每個計畫期為五年。第一個戰略計劃將涵蓋 2020 年至 2024 年期間,與最低基本部隊 (MEF) 計劃的最後階段相吻合。該文件提案在未來25年內花費790億美元用於國防裝備,325億美元用於維護,剩餘的134億美元用於支付外國貸款利息。

- 在日本,國防費用的增加、下一代武器的採購增加以及軍事通訊中先進技術的採用正在推動日本整個市場的成長。根據斯德哥爾摩國際和平研究所(SIPRI)2022年報告,日本國防預算為460億美元,是全球第十大國防費用。它已核准2023會計年度514億美元的國防費用。

- 複合材料逐漸進入海軍艦艇和陸戰車的裝甲系統。複合材料已經取代了鋼、鋁甚至鈦合金,部分原因是由於彈道效率的提高(類似於結構材料比強度和剛性重量比的重大進步)以及其重量輕。複合部件可以作為主裝甲的一部分,對抵禦手榴彈、迫擊砲、火砲和其他爆炸物產生的彈片特別有效。該車輛可以使用 S 玻璃或編織凱夫拉裝甲層壓板。

- 在車輛裝甲領域,防彈複合複合材料具有以下優點:減輕車輛重量、提高機動性、減少裝甲所需零件、提高燃油效率、延長車輛壽命。

北美佔據市場主導地位

- 由於航太和國防工業活動的成長以及降低成本、降低碳排放和減少燃料消費量的不斷成長的需求,北美地區佔據了全球市場佔有率的主導地位。

- 美國是受調查市場中最大的消費國家。美國國防部(DoD)2022會計年度的預算權限約為7,220億美元,比2020會計年度的7,050億美元增加170億美元。相較之下,總統對2023會計年度的預算要求為國防部撥款7,730億美元。該預算主要是為了實現空中、海上和陸戰領域能力的現代化,以及技術創新,以增強國家的競爭優勢。

- 到 2023 年,海軍可能增加 16,900 名人員,海軍陸戰隊可能增加 1,400 名人員,空軍可能增加 13,700 名人員,使現役軍人總數達到 1,365,500 人。

- 該法案還包括投資 65 億美元增加歐洲的坦克和裝甲車等作戰裝備,這是五角大廈安撫歐洲盟友計畫的一部分。

- 截至 2022 年 10 月,美國和 BAE 系統公司正在合作尋找加速生產新型裝甲多用途車輛的方法,以更快取代老化的 M113 裝甲運兵車。

- 據美國國會研究服務處稱,AMPV(裝甲多用途車)的年產量計劃到 2024 會計年度將增至 131 輛,並至少在 2027 會計年度保持這一水平。據報道,2020 年生產延遲之前發布的 AMPV 計畫文件要求到 2024 會計年度 AMPV 的年產量達到 190 輛。

- 俄烏戰爭爆發後,美國向烏克蘭運送了大規模武器,烏克蘭國防部門也開始大舉採購。為了更好地應對俄羅斯的威脅,空軍正在擴大採購。例如:

- 近日,2022年3月,美國請求撥款110億美元,用於2023會計年度購買61架洛克希德·馬丁公司的F-35閃電II飛機。其採購計畫中約45%用於戰鬥機(83.89億美元),23%用於現役平台的改裝(42.57億美元)。

- 由於上述因素,該地區的防彈複合材料市場預計將在預測期內顯著成長。

彈道複合材料產業概況

防彈複合材料市場因其性質而部分整合。主要企業(不分先後順序)包括杜邦、DSM、Honeywell國際、Tencate Protective Fibers、帝人。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 增加國防費用

- 航太和國防工業對輕量材料的需求不斷增加

- 其他促進因素

- 限制因素

- 加工製造成本高

- 原物料供應不穩定

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 依纖維類型

- 芳香聚醯胺

- 超高分子量聚乙烯 (UHMWPE)

- S-玻璃

- 其他纖維類型(生物基纖維、奈米複合材料等)

- 按矩陣類型

- 聚合物

- 聚合物陶瓷

- 金屬

- 按應用

- 車輛裝甲

- 防彈衣

- 頭盔和臉部防護

- 其他應用(航空和海洋防護、高性能運動器材等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- ArmorCore

- BAE Systems

- Barrday Inc

- Coherent Corp.

- DSM

- DuPont

- Gaffco Ballistics

- Gurit Holding AG

- Honeywell International Inc.

- Integris

- MKU LIMITED

- Morgan Advanced Materials

- Plastic Reinforcement Fabrics Ltd

- Roihu Inc.

- Southern States, llc

- Teijin Limited

- TenCate Protective Fabrics

第7章 市場機會與未來趨勢

- 防彈地形自適應車輛的開發

- 生物基防彈紡織品的開發

The Ballistic Composites Market size is estimated at USD 1.99 billion in 2025, and is expected to reach USD 2.42 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The COVID-19 pandemic was a mixed bag for the Ballistic Composites Market. While it presented challenges due to supply chain disruptions, demand fluctuations, and economic uncertainty, it also spurred innovation, highlighted new opportunities in security and sustainability, and potentially accelerated the adoption of beneficial technologies in manufacturing. The long-term impact of the pandemic is evident, but the market's adaptability and the ongoing need for high-performance protection materials suggest a promising future.

Key Highlights

- One of the major factors driving the market is the increasing demand from the defense and aerospace industries, as modern warfare emphasizes lightweight and comfortable body armor that provides adequate ballistic protection without compromising mobility.

- On the flip side, the processing and manufacturing of ballistic composites often involve complex and labor-intensive techniques. It drove up the costs and may act as a hindrance to the growth of the market studied.

- The rise in defense expenditures and budgets of many countries and the demand for lightweight materials for protection against ballistic threats are likely to act as opportunities in the forecast period.

- North America dominated the market across the world, with the most significant consumption from countries such as the United States and Canada.

Ballistic Composites Market Trends

Increasing Demand for Vehicle Armors

- The demand for vehicle armor in the ballistic composites market is definitely on the rise. It is driven by a multitude of factors, such as growing security concerns, technological advancements, expanding applications, and many more.

- Armored personnel carriers, combat vehicles, and even some military trucks are increasingly utilizing ballistic composites for protection.

- Land combat vehicles are protected by armor sufficient to withstand heavy machinegun fire and overhead artillery fire. These vehicles include external armor kits, which include glass fiber-reinforced support plates. A strengthened undercarriage protects the personnel inside from mines. Exterior armor design generally includes modular expandable armor system panels made with ceramic-faced woven aramid. The roof interiors consist of molded-woven aramid reinforced composites, and the interior sides contain molded, S-fiberglass-reinforced composites.

- Armor protection against ground fire from small arms is also required on the bottom of helicopters. As the fuselage of helicopters needs to be light, the base portion is generally vulnerable to small-arms fire from the ground. It puts the occupants at risk. Lightweight armor for the bottom of helicopters is in use for many years.

- Increasing warfare across the world is increasing the demand for military vehicles required in warships, which is likely to increase the demand for vehicle armor during the forecast period.

- Increased defense spending and security budgets are leading to more significant investment in armored vehicles and advanced armor technologies.

- China's defense industry is increasing, with many Chinese firms displacing Western defense powerhouses. The country invests heavily to upgrade its military, thus making its eight defense firms among the top 25 in the world.

- Currently, the annual output of Chinese military aircraft is around 300. As China's military industry continues to grow, the demand for and supply of Chinese military aircraft will increase substantially. It will drive the rapid development of China's military aircraft manufacturing industry.

- In June 2021, Indonesia unveiled another plan to spend USD 125 billion through the mid-2040s to upgrade and modernize its military arsenal. The total period runs through a period of five strategic plans, each lasting five years. The first strategic plan runs from 2020 to 2024 and coincides with the final phase of the Minimum Essential Force (MEF) program. The document proposes funding of USD 79 billion for defense equipment during these 25 years, USD 32.5 billion for sustainment, and the remaining USD 13.4 billion for interest payments on foreign loans.

- In Japan, an increase in defense expenditure, rising procurement of next-generation weapons, and adoption of advanced technologies in military communication drive the growth of the market across Japan. According to the report published by the Stockholm International Peace Research Institute (SIPRI) in 2022, Japan was the tenth largest defense spender in the world, with a defense budget of USD 46 billion. The country approved USD 51.4 billion in defense spending in FY2023.

- Composite materials gradually crept into armor systems for naval vessels and land combat vehicles. They displaced steel, aluminum, and even titanium alloys, partly due to improved ballistic efficiencies similar to the significant advancements in specific strength and stiffness made in structural materials, as well as being lightweight. Composite parts can be part of the primary armor, especially effective against fragmentation, originating from grenades, mortars, artillery, and other explosive devices. Vehicles can use armor laminates of either S-glass or Kevlar fabric.

- In the area of vehicle armor, ballistic composites provided the following benefits: reduced the weight of a vehicle, increased mobility, decreased number of components required to armor, increased fuel efficiency, and increased life of the vehicle.

North American Region to Dominate the Market

- The North American region dominated the global market share due to the growing aerospace and defense industrial activities and the increasing need to bring down costs, lower carbon dioxide emissions, and reduce fuel consumption.

- The United States is the largest consumer of the market studied. For FY 2022, the Department of Defense's (DoD) budget authority is approximately USD 722 billion, an increase of USD 17 billion from USD 705 billion in 2020. In comparison, the FY 2023 President's budget request was USD 773 billion for the DoD. The budget primarily aims to modernize capabilities in the air, maritime, and land warfighting domains and to innovate to strengthen the country's competitive advantage.

- By 2023, the Navy forces may increase by 16,900, the Marine Corps by 1,400, and the Air Force by 13,700, increasing the total active-duty military to 1,365,500 personnel.

- The proposal also includes an investment of USD 6.5 billion to place more tanks, armored vehicles, and other combat equipment in Europe as part of the Pentagon plan to reassure European allies.

- As of October 2022, the US Army and BAE Systems are working together to identify ways to accelerate production of the new Armored Multi-Purpose Vehicle, which would let the service more quickly replace aging M113 armored troop carriers.

- According to the Congressional Research Service, the AMPV(Armored Multi-Purpose Vehicle) annual production rate reportedly, by FY2024, AMPV production rates are planned to increase to 131 vehicles per year and to continue at that level until at least FY2027. Earlier AMPV program planning documents issued before the 2020 production delay had reportedly called for an annual production rate of 190 AMPVs per year by FY2024.

- The country's defense agencies are on a spree of procurements in view of the Russia-Ukraine war that drove significant US weapon supply to Ukraine. To successfully tackle any Russian threat, the Air Force is carrying out growth in procurement. For instance:

- Recently, in March 2022, the Pentagon requested a USD 11 billion fund for 61 Lockheed Martin F-35 Lightning II aircraft for FY2023. About 45% of that procurement plan is for combat aircraft (USD 8.389 billion) and 23% for modifying in-service platforms (USD 4.257 billion).

- Owing to the factors above, the ballistic composites market in the region is expected to increase at a significant rate during the forecast period.

Ballistic Composites Industry Overview

The ballistic composites market is partially consolidated in nature. The major players (not in any particular order) include DuPont, DSM, Honeywell International Inc., TenCate Protective Fibers, and Teijin Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rise in Defense Expenditure

- 4.1.2 Increasing Demand for Lightweight Materials in the Aerospace and Defense Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Processing and Manufacturing Costs

- 4.2.2 Volatile Raw Material Supply

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Fiber Type

- 5.1.1 Aramids

- 5.1.2 Ultra-high-molecular Weight Polyethylene (UHMWPE)

- 5.1.3 S-glass

- 5.1.4 Others Fiber Types (Bio-based Fibers, Nanocomposites, etc. )

- 5.2 Matrix Type

- 5.2.1 Polymer

- 5.2.2 Polymer-ceramic

- 5.2.3 Metal

- 5.3 Application

- 5.3.1 Vehicle Armor

- 5.3.2 Body Armor

- 5.3.3 Helmet and Face Protection

- 5.3.4 Other Applications (Aircraft and Marine Protection, High-Performance Sporting Goods, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ArmorCore

- 6.4.2 BAE Systems

- 6.4.3 Barrday Inc

- 6.4.4 Coherent Corp.

- 6.4.5 DSM

- 6.4.6 DuPont

- 6.4.7 Gaffco Ballistics

- 6.4.8 Gurit Holding AG

- 6.4.9 Honeywell International Inc.

- 6.4.10 Integris

- 6.4.11 MKU LIMITED

- 6.4.12 Morgan Advanced Materials

- 6.4.13 Plastic Reinforcement Fabrics Ltd

- 6.4.14 Roihu Inc.

- 6.4.15 Southern States, llc

- 6.4.16 Teijin Limited

- 6.4.17 TenCate Protective Fabrics

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Terrain Motor Vehicles with Ballistic Protection

- 7.2 Development of Bio-Based Ballistic Fibers

防彈複合材料市場規模、佔有率和成長分析(按原料、纖維類型、產品、應用和地區)- 2025-2032 年行業預測

防彈複合材料市場規模、佔有率和成長分析(按原料、纖維類型、產品、應用和地區)- 2025-2032 年行業預測 彈道複合材料市場:按纖維、基體、應用和最終用途分類-2025-2030 年全球預測

彈道複合材料市場:按纖維、基體、應用和最終用途分類-2025-2030 年全球預測 2024-2032 年按纖維類型(芳綸、超高分子量聚乙烯、S 玻璃等)、基體類型(聚合物基複合材料、陶瓷基複合材料、金屬基複合材料)、應用和地區分類的彈道複合材料市場報告

2024-2032 年按纖維類型(芳綸、超高分子量聚乙烯、S 玻璃等)、基體類型(聚合物基複合材料、陶瓷基複合材料、金屬基複合材料)、應用和地區分類的彈道複合材料市場報告 全球彈道複合材料市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球彈道複合材料市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測![防彈複合材料市場:趨勢、機會與競爭分析 [2024-2030]](/sample/img/cover/42/1496950.png) 防彈複合材料市場:趨勢、機會與競爭分析 [2024-2030]

防彈複合材料市場:趨勢、機會與競爭分析 [2024-2030] 軍用防彈鋼板的全球市場(2024年)

軍用防彈鋼板的全球市場(2024年) 彈道複合材料市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按纖維類型、基質類型、按應用、地區和競爭細分

彈道複合材料市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按纖維類型、基質類型、按應用、地區和競爭細分 防彈複合材料市場 - 依纖維類型(芳綸纖維基、超高分子量聚乙烯)、副產品(聚合物基複合材料、陶瓷基複合材料、金屬基複合材料)、按應用和預測,2023 - 2032

防彈複合材料市場 - 依纖維類型(芳綸纖維基、超高分子量聚乙烯)、副產品(聚合物基複合材料、陶瓷基複合材料、金屬基複合材料)、按應用和預測,2023 - 2032