|

市場調查報告書

商品編碼

1641924

Edge Analytics:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Edge Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

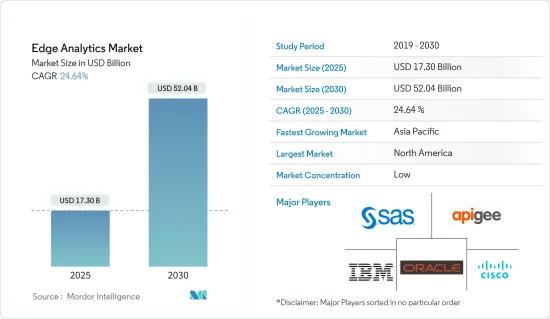

邊緣分析市場規模預計在 2025 年達到 173 億美元,預計到 2030 年將達到 520.4 億美元,預測期內(2025-2030 年)的複合年成長率為 24.64%。

邊緣分析是一項新興技術,有望透過更接近資料來源來減輕雲端伺服器的負載。邊緣分析可以即時分析資料,從而可以更好地依賴雲端服務。製造業、醫療保健和零售業等行業預計將受益最多,因為處理後的資料將即時可用,從而實現即時決策,提高效率。

主要亮點

- 邊緣分析是一種資料收集和分析策略,它對邊緣、節點、網路交換器和其他網路端點的資料執行自動分析計算,而不是等待資料被繼電器集中式資料儲存。

- 隨著網路和雲端運算的不斷滲透,全球邊緣分析產業未來前景廣闊。此外,日益成長的自動化需求正在推動市場成長。

- 借助連網設備產生的大量資料推動了邊緣分析市場的成長,而即時智慧則成為網路設備上邊緣分析成長的催化劑,邊緣分析的採用是提高擴充性和成本最佳化。

- 然而,缺乏安裝和管理基於邊緣的解決方案的熟練人員阻礙了市場的發展。預計網路節點效率的提高將為預測年份內邊緣分析市場規模的擴大提供有利的前景。

- COVID-19 疫情對邊緣分析市場產生了積極影響,因為 COVID-19 封鎖期間遠端工作和員工缺勤的趨勢促使了對自動化和物聯網解決方案的需求。已顯示出顯著的成長。此外,疫情過後,由於數位化技術的普及,市場也實現了快速成長。

邊緣分析市場趨勢

透過連網設備增加資料傳輸將推動市場成長

- 邊緣分析的需求是由每天產生並儲存在雲端中的大量資料所驅動。據Cisco稱,拉丁美洲每月消費者控制的網際網路通訊協定(IP) 流量資料預計將從 2017 年的每月 0.7Exabyte成長到 2022 年的每月 1.92Exabyte。

- 根據 Errision 的數據,2021 年透過固定無線存取 (FWA) 的每月資料流量為 16.6 Exabyte ,高於 2020 年的 9.7 Exabyte 。預計未來幾年將出現強勁成長,到 2028 年每月 FWA資料流量將達到約 130 Exabyte。 FWA 是一種透過 5G、4G 和 3G 實現固定寬頻連線的技術,即使在基礎設施有限的地區也能提供寬頻連線。 2021 年,FWA資料流量超過 5G行動連線,但預計 2024 年 5G 行動流量將超過 FWA 流量。

- 此外,大量資料被儲存在邊緣,希捷估計到 2025 年物聯網設備將產生超過 90 Zetta位元組的資料。預計響應資料對於物聯網、人工智慧和區塊鏈等下一代技術將極為重要。

- 此外,邊緣分析是智慧城市等新概念的核心,它會自動即時分析和計算收集的資料,而不是將資料發送回集中式資料儲存或伺服器,因此對智慧城市技術的投資也一個關鍵促進因素。邊緣分析應用程式數量的增加預計將推動邊緣分析市場的發展,從而為最終用戶提供更快、更快回應的服務。

- 邊緣運算作為一種提高網路效能的技術已經存在了一段時間。邊緣運算使資料分析部分依賴網路頻寬,並將資料儲存在更靠近資料來源的地方。邊緣運算還將資料處理和儲存從孤島設定移出,更靠近最終用戶,在設備、霧層和邊緣資料中心進行處理。

北美預計將創下最大市場規模

- 由於政府法規和合規性支援以及中小企業的接受度不斷提高,美國仍然是邊緣分析的主要市場。此外,由於邊緣分析服務集中在製造業和通訊業,邊緣分析市場也顯著成長。邊緣分析的需求與雲端流量直接相關。由於雲端流量的大幅增加,市場將顯著成長。

- 北美保險公司正在改變其使用雲端運算的方式。產物保險和意外險以及壽險公司都採用了雲端運算來提高靈活性、提高業務效率、吸引新人才並降低業務成本,但保險公司也開始將雲端運算視為一項商業資產。 。使用分散式邊緣運算架構可以顯著降低雲端營運成本。邊緣設備可以協同處理雲端設備無法單獨處理的關鍵操作,從而減少對雲端的依賴。

- 該地區的感測器技術也正在顯著成長。感測器技術的創新與硬體成本的降低相結合可以建立邊緣到雲端的範式。具有處理單元的感測器可以幫助在不一致的雲端環境中採取關鍵操作,然後與雲端同步。

- 加拿大以快速採用新技術而聞名。當今大多數新技術都是資料密集型的。由於創建、處理和傳輸的資料如此之多,我們目前的資料中心和雲端基礎設施已接近最大容量。

- 隨著目前產生和使用的新資料量不斷增加,這些基礎設施不太可能滿足客戶的需求。在所有相關參數中,延遲可能是對您的業務最關鍵的因素。

邊緣分析產業概覽

邊緣分析市場高度分散,主要企業包括思科系統公司、甲骨文公司、SAS 研究所、IBM 公司和 Apigee 公司。市場參與者正在採用合作、創新和收購等策略來增強其產品供應並獲得永續的競爭優勢。

- 2022 年 6 月 - 領先的IT基礎設施基礎架構服務供應商 Kyndryl 與思科將利用思科解決方案和 Kyndryl 託管服務協助企業客戶加速向資料主導組織的轉型。

- 2022 年 6 月 - 先鋒合作夥伴 SAS 和 ClearBlade 幫助製造業、石油和天然氣以及運輸業等資產密集型行業的營運經理以更簡單、更具成本效益的方式對所有流資料做出更明智的決策。最大限度地提高操作技術的效率 (透過解鎖價值來獲得「OT」裝備。合作夥伴將在物聯網連接資產上利用人工智慧 (AI) 和機器學習,使 OT 高管能夠存取、分析和處理邊緣和雲端的串流資料,而無需依賴 IT 或資料科學家來加速流程。 。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 技術簡介

- 說明分析

- 預測分析

- 指示性分析

- 診斷分析

- 產業價值鏈分析

- COVID-19 對市場的影響

第5章 市場動態

- 市場促進因素

- 物聯網中連接設備的數量不斷成長

- 透過連網設備增加資料傳播

- 市場限制

- 邊緣技術的採用尚處於早期階段

- 資料安全和安全威脅

第6章 市場細分

- 依部署類型

- 本地

- 雲

- 按組件

- 解決方案

- 服務(專業服務、主機服務)

- 按最終用戶產業

- 銀行、金融服務和保險(BFSI)

- 資訊科技/通訊

- 製造業

- 衛生保健

- 零售

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 日本

- 中國

- 印度

- 其他亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- Cisco Systems Inc.

- Oracle Corporation

- SAS Institute Inc.

- IBM Corporation

- Apigee Corporation

- Predixion Software

- AGT International Inc.

- Foghorn Systems

- CGI Group Inc.

- Intel Corporation

- Greenwave Systems

- Microsoft Corporation

第8章投資分析

第9章:市場的未來

The Edge Analytics Market size is estimated at USD 17.30 billion in 2025, and is expected to reach USD 52.04 billion by 2030, at a CAGR of 24.64% during the forecast period (2025-2030).

Edge Analytics is an emerging technology expected to ease the load on cloud servers as it is closer to the data source. Edge Analytics can analyze data in real-time, enabling higher dependencies on cloud services. Industries like Manufacturing, healthcare, and retail are expected to benefit the most from the real-time availability of processed data, enabling them to achieve higher efficiencies using real-time decision-making.

Key Highlights

- Edge analytics is a data collecting and analysis strategy in which an automated analytical calculation is done on data at the edge of a node, network switch, or another network endpoint instead of waiting for the data to be relayed back to centralized data storage.

- An increase in internet and cloud adoption offers enormous prospects for the global edge analytics industry in the future. Moreover, the rising need for automation boosts the market growth.

- The proliferation of a large amount of data with the help of connected devices is driving the growth of the edge analytics market, with real-time intelligence acting as a catalyst for the growth of edge analytics on network devices and adopting edge analytics, increasing scalability and cost optimization.

- However, the lack of skilled personnel to install and manage edge-based solutions hinders market development. The increasing network node efficiency is predicted to provide lucrative prospects for advancing the edge analytics market size throughout the forecast year.

- The COVID-19 pandemic had a positive impact on the edge analytics market, which exhibited significant growth during the period, owing to remote working trends and employee unavailability during the period of COVID-19 lockdowns, which prompted the need for automation and IoT solutions during the period, assisting in the growth of the edge analytics market during the period. Post-pandemic also, the market is growing rapidly with the increased adoption of digitization technologies.

Edge Analytics Market Trends

Rising Propagation of Data Over Connected Devices Drives the Market Growth

- The need for Edge Analytics is further driven by the massive amount of data generated on everyday, which is stored on the cloud. According to Cisco Systems, the data on consumer-managed Internet Protocol (IP) monthly traffic in Latin America was 0.7 exabytes per month in 2017, expected to grow to 1.92 exabytes in 2022.

- According to Errision, Monthly data traffic through fixed wireless access (FWA) was measured at 16.6 exabytes in 2021, up from 9.7 exabytes in 2020. Strong growth is expected over the coming years, with monthly FWA data traffic forecast to reach almost 130 exabytes by 2028. FWA is a technology enabling a fixed broadband connection via 5G, 4G, or 3G and can provide broadband connections in areas with limited infrastructure. FWA data traffic outstripped that of 5G mobile connections in 2021, though 5G mobile traffic is expected to surpass FWA traffic by 2024.

- Moreover, a large amount of data is stored on the Edge, and Seagate estimates that the IoT devices will generate more than 90 zettabytes of data by 2025. Data readiness is expected to be critical for next-generation technologies like IoT, AI, and blockchain.

- Also, the edge analytics capabilities of automatic analytical computation of collected data in real-time, instead of sending the data back to the centralized data store or server, will be the core of new concepts, like smart cities, due to which increased investment in smart cities technology is expected to boost the market for edge analytics that will provide faster and responsive services to end user.

- Edge Computing has been in the technological space for some time, surging network performance. Due to edge computing, data analytics partly relies on the network bandwidth to save data close to the data source. Also, edge computing makes data handled and stored away from the silo setup closer to end users, with processing in the device, the fog layer, or the edge data center.

North America is Expected to Register the Largest Market

- The United States remains a prominent market for Edge Analytics due to the increasing acceptance of edge analytics among small and medium-scale firms, supported by government regulations and compliance. Additionally, the significant growth of the edge analytics market can be attributed to the high concentration of manufacturing and telecommunication industries that majorly adopt edge analytics services. The demand for edge analytics is directly related to cloud traffic. Due to the huge increase in cloud traffic, significant growth in the market can be observed.

- North American Insurance companies are changing the way they utilize cloud computing. While both property & casualty and life insurers have employed the cloud to increase agility, increase operating efficiency, attract new talent and reduce operating costs, there is an emerging trend in insurers viewing the cloud as a business asset. Cloud operations cost can be significantly reduced by using a distributed edge computing architecture, where edge devices together process a critical operation, which a cloud device cannot process independently, thereby reducing cloud dependency.

- Also, significant growth in sensor technology can be witnessed in the region. By combining sensor technology innovations with reducing hardware costs, the edge-to-cloud paradigm can be established. Sensors with processing units can help take critical actions in an inconsistent cloud environment and later synchronize with the cloud.

- Canada is known to be an early adopter of new technologies. Most new technologies at present are data intensive. They create, process, and transfer large amounts of data, due to which the current infrastructure, consisting of data centers and the cloud, is inching toward its maximum capacity.

- With the amount of new data generated and used at present, these infrastructures won't support the needs of their customers. Of all the parameters involved, latency will be the most crucial factor for the business.

Edge Analytics Industry Overview

The edge analytics market is highly fragmented with the presence of major players like Cisco Systems Inc., Oracle Corporation, SAS Institute Inc., IBM Corporation, and Apigee Corporation. Players in the market are adopting strategies such as partnerships, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- June 2022 - Kyndryl, one of the leading providers of IT infrastructure services, and Cisco announced a technological partnership to assist corporate clients in accelerating their transition into data-driven organizations driven by Cisco solutions and Kyndryl managed services.

- June 2022 - Pioneering partners SAS and ClearBlade are assisting operations managers in asset-intensive industries such as manufacturing, oil and gas, and transportation in maximizing the effectiveness of their operational technology (OT) equipment by unlocking the value of all streaming data in a simpler and cost-effective manner. The partners are leveraging artificial intelligence (AI) and machine learning on IoT-connected assets to enable OT executives to access, analyze, and act on streaming data at the Edge and in the Cloud without relying on IT or data scientists, shortening the process from months to weeks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.3.1 Descriptive Analytics

- 4.3.2 Predictive Analytics

- 4.3.3 Prescriptive Analytics

- 4.3.4 Diagnostic Analytics

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Number of Connected Devices in IoT

- 5.1.2 Rising Propagation of Data Over Connected Devices

- 5.2 Market Restraints

- 5.2.1 Adoption of Edge Technology in Nascent stage

- 5.2.2 Threat of Data Safety and Security

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-Premises

- 6.1.2 Cloud

- 6.2 By Component

- 6.2.1 Solutions

- 6.2.2 Services (Professional and Managed Services)

- 6.3 By End User Industry

- 6.3.1 Banking, Financial Services, and Insurance (BFSI)

- 6.3.2 IT and Telecommunication

- 6.3.3 Manufacturing

- 6.3.4 Healthcare

- 6.3.5 Retail

- 6.3.6 Other End-user Industry

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 Japan

- 6.4.3.2 China

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Oracle Corporation

- 7.1.3 SAS Institute Inc.

- 7.1.4 IBM Corporation

- 7.1.5 Apigee Corporation

- 7.1.6 Predixion Software

- 7.1.7 AGT International Inc.

- 7.1.8 Foghorn Systems

- 7.1.9 CGI Group Inc.

- 7.1.10 Intel Corporation

- 7.1.11 Greenwave Systems

- 7.1.12 Microsoft Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

邊緣分析市場規模、佔有率、成長分析、按類型、按組件、按部署、按應用、按最終用途、按地區 - 行業預測,2024-2031 年

邊緣分析市場規模、佔有率、成長分析、按類型、按組件、按部署、按應用、按最終用途、按地區 - 行業預測,2024-2031 年 邊緣分析市場:按元件、類型、業務應用程式、部署模型和產業分類 - 2025-2030 年全球預測

邊緣分析市場:按元件、類型、業務應用程式、部署模型和產業分類 - 2025-2030 年全球預測 全球邊緣分析市場,2024-2028

全球邊緣分析市場,2024-2028 邊緣分析市場 - 全球產業規模、佔有率、趨勢、機會和預測。 2018-2028F 按元件、類型、按應用、部署模式、最終用戶、地區、競爭細分

邊緣分析市場 - 全球產業規模、佔有率、趨勢、機會和預測。 2018-2028F 按元件、類型、按應用、部署模式、最終用戶、地區、競爭細分 邊緣分析市場規模 - 按元件、按業務應用程式、按類型、部署模型、垂直產業和預測,2023 年 - 2032 年

邊緣分析市場規模 - 按元件、按業務應用程式、按類型、部署模型、垂直產業和預測,2023 年 - 2032 年 邊緣分析的市場規模,佔有率,趨勢分析報告:各類型,各零件,配置模式,各用途,各最終用途產業,各地區,及市場區隔趨勢:2023年~2030年

邊緣分析的市場規模,佔有率,趨勢分析報告:各類型,各零件,配置模式,各用途,各最終用途產業,各地區,及市場區隔趨勢:2023年~2030年 邊緣分析市場:當前分析和預測 (2022-2028)

邊緣分析市場:當前分析和預測 (2022-2028)