|

市場調查報告書

商品編碼

1641977

AI 晶片組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)AI Chipsets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

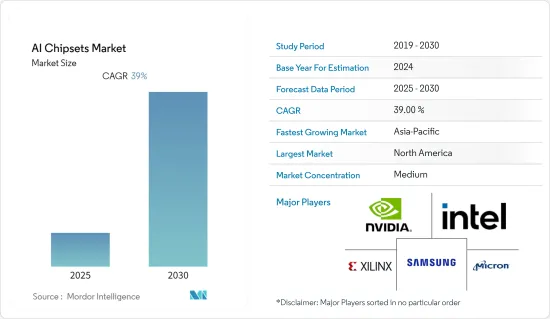

預計預測期內AI晶片組市場複合年成長率為39%。

主要亮點

- 汽車、金融和零售等多個領域對機器學習的需求正在迅速成長,推動了人工智慧技術的採用。 AI晶片在汽車產業最突出的應用包括生產無人駕駛汽車,以實現L5等級的自動駕駛技術。

- 人工智慧(AI)滲透到了消費性電子產品的幾乎每個方面。它的用途不僅限於行動電話,而且還擴展到汽車產業。這種成長為半導體產業帶來了許多新的視角。處理不斷增加的資料量的需求是影響AI晶片組市場成長的主要因素。

- 此外,人工智慧有望在未來開闢許多商機,因為它使機器能夠執行各種類似人類的活動。此外,人們對以人為本的人工智慧系統發展的日益關注也在推動市場成長。然而,技術純熟勞工的短缺以及標準和通訊協定的缺乏阻礙了市場的成長。

- 隨著人工智慧逐漸成為全球技術,對大量 ASIC 的需求預計會增加。亞馬遜和谷歌等公司已開始努力增強其伺服器矽晶圓。

- 公司正在利用人工智慧等新技術來設計新的人工智慧晶片。例如,根據2021年6月發表在《自然》雜誌上的一篇論文,Google正在其下一代AI晶片的設計中使用AI和機器學習。據該公司稱,人工智慧將能夠在不到六小時內完成人類需要數月才能完成的任務。

- 此外,神經型態研究的增加是人工智慧硬體領域的一個新興領域,預計將推動對人工智慧晶片的需求。這裡的直覺是開發受大腦實際神經功能啟發的技術,因此得名神經形態。神經元的低能量和高品質輸出激發了研究人員開發脈衝神經網路 (SNN) 的興趣。然而,這些 SNN 需要自己的硬體。

- COVID-19疫情對AI晶片組市場的供應鏈和生產產生了不利影響。這對半導體製造商的影響是嚴重的。接受人工智慧來改善消費者服務並降低營運成本、人工智慧應用數量的不斷成長、處理能力的不斷提高以及深度學習和神經網路的日益普及是主要的市場驅動力。全球半導體供應鏈中的許多公司由於勞動力限制而限制或停止了營運,為依賴半導體的最終產品公司帶來了瓶頸。

人工智慧晶片市場趨勢

消費性電子產品可望強勁成長

- 由於新冠疫情,半導體晶片短缺導致全球消費性電子產品生產陷入停滯。然而,疫情導致對筆記型電腦、桌上型電腦和遊戲機等家用電子電器的需求龐大,給產品公司、製造商和最終消費者帶來了混亂。設備製造商加大力度滿足動盪的消費科技市場的需求。預計晶片短缺和高需求的局面將在未來2-3年持續,推動消費性電子產品對AI晶片的需求。

- 量子計算技術在解決複雜問題和執行分析計算方面的應用日益廣泛,市場可能會受益。例如,Google LLC 的量子電腦 Sycamore 是目前最快的電腦,能夠在大約 200 秒內完成任務。人工智慧、機器學習、電腦視覺、巨量資料、AR/VR等技術正在實現量子運算。對量子運算的廣泛了解將增加對人工智慧晶片組的需求,從而有助於推動產業成長。

- 人工智慧技術正在應用於汽車和製造業等各個行業,以簡化流程。疫情期間,製造商專注於增強基於人工智慧的解決方案,這可能會使整個產業受益。例如,2020 年 5 月,Nvidia 公司更新了其 EGX Edge AI 平台,推出了新設備 EGX Jetson Xavier NX 和 EGX A100。

- 預計預測期內,家用電器類別將佔據 AI 晶片組市場的很大一部分。平板電腦、智慧型手機等各類電子設備規格高階,市場需求強勁。眾多製造商不斷推出新型 AI 晶片組以滿足日益成長的需求。例如,台灣晶片製造商聯發科於 2022 年 5 月發布了用於物聯網人工智慧 (AIoT) 裝置的 Genio 架構及其 Genio 1200 晶片。聯發科表示,基於 Genio 1200 晶片的高階 AIoT 解決方案將於 2022 年下半年廣泛普及。

- 人工智慧晶片組市場的發展受到對更快電腦處理器日益成長的需求以及對改善客戶服務和降低營運成本日益成長的需求的推動。由於缺乏經驗豐富的勞動力以及缺乏標準和通訊協定,該行業的發展受到阻礙。

亞太地區可望實現強勁成長

- 預計亞太市場將在韓國、印度和中國等新興經濟體的推動下實現顯著成長。預計基於人工智慧的解決方案的日益接受將支持該地區市場的健康擴張。人工智慧晶片組在智慧型手機、平板電腦和筆記型電腦等家用電子電器的應用日益增多,其中包括整合語音命令等,這導致該地區對人工智慧晶片組的採用率很高。

- 日本是最早制定國家人工智慧政策的國家之一。日本的做法著重於利用人工智慧造福社會和經濟,旨在擴大人工智慧研發技能,建立工業人工智慧系統,並為不斷變化的勞動力市場做好工人的準備。 2019 年 6 月,首相安倍晉三宣布計畫在 2025 年每年培訓 25 萬人接受人工智慧技能培訓。

- 人工智慧晶片組在智慧型手機、平板電腦和筆記型電腦等消費性電子產品中的應用,包括整合語音命令、增強攝影體驗以及根據過去的搜尋收集和分類相關資料,正在推動人工智慧晶片組的廣泛採用。它帶來了。

- 該地區是世界上最大的智慧型手機製造商和半導體公司的所在地。中國、日本、台灣和韓國約佔全球智慧型手機製造商的80%。由於人口數量最多,智慧型手機的使用量正在上升,這很可能成為市場成長的驅動力。

- 該地區的多家市場參與者處於人工智慧晶片開發和製造的前沿。例如,2021年8月,中國科技巨頭百度開始量產第二代崑崙AI晶片,旨在成為晶片產業的主要企業。根據百度介紹,新一代崑崙AI晶片採用7nm製程製程生產,算力較上一代提升2至3倍。

AI晶片產業概況

- 儘管一些大型和小型全球公司正在影響市場,但AI晶片組市場預計將逐步整合。該市場仍處於發展初期。目前業界知名的參與者包括英特爾公司、三星電子、NVIDIA 公司、賽靈思公司和美光科技。為了在AI晶片組市場佔據主導地位,這些參與者正在進行合作、新產品創新和市場擴張等競爭策略進步。

- 2021 年 8 月-IBM 宣布推出一款新晶片 Telum,預計將使 IBM 客戶能夠大規模利用深度學習推理。該晶片採用集中式設計,使客戶能夠充分利用AI處理器的全部功能來處理AI專用工作負載,包括貸款處理,貿易清算和付款,詐騙檢測和反洗錢,以及金融服務工作負載,例如風險分析。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- 產業價值鏈分析

- COVID-19 對 AI 晶片組市場的影響評估

第5章 市場動態

- 市場促進因素

- 自動駕駛技術需求不斷成長

- 物聯網應用邊緣分析的成長

- 市場限制

- 設計和人工智慧介面的複雜性

第6章 市場細分

- 按組件

- 中央處理器 (CPU)

- 圖形處理單元 (GPU)

- 神經網路處理器(NNP)

- 其他組件

- 按應用

- 消費性電子產品

- 車

- 衛生保健

- 自動化和機器人

- 其他用途

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東

第7章 競爭格局

- 公司簡介

- Advanced Micro Devices Inc.(AMD)

- Xilinx Inc.

- Graphcore Ltd

- Huawei Technologies Co. Ltd

- IBM Corporation

- Intel Corporation

- NVIDIA Corporation

- Micron Technology Inc.

- Samsung Semiconductor(Samsung Electronics Co. Ltd)

第8章投資分析

第9章:市場的未來

簡介目錄

Product Code: 64258

The AI Chipsets Market is expected to register a CAGR of 39% during the forecast period.

Key Highlights

- The rapidly growing demand for machine learning in multiple sectors, such as automotive, finance, and retail, boosts the adoption of AI technology. The most famous application of AI chipsets in the automotive industry includes manufacturing a driverless car to achieve the L5 level of autonomous technology.

- Artificial intelligence (AI) is entering nearly every aspect of consumer electronics. Its uses are growing beyond cell phones to include the automotive industry. This growth is bringing a slew of new prospects to the semiconductor industry. The requirement to process a constantly rising volume of data is a major element influencing the AI chipset market's growth.

- Moreover, as AI enables machines to perform various activities like those operated by human beings, numerous opportunities are expected to open in the future. Additionally, the growing focus on developing human-aware AI systems is boosting the growth of the market. However, the lack of a skilled workforce and the absence of standards and protocols are restraining the market growth.

- The need for a large number of ASICs is anticipated to rise as artificial intelligence gains more ground in global technology. Companies, such as Amazon and Google, are already in the process of fortifying their server silicon endeavors.

- Companies are using new technologies, such as artificial intelligence, to design new AI chips. For instance, as per a paper published in the journal Nature in June 2021, Google is using AI and machine learning to help design its next generation of AI chips. According to the company, work that takes months for humans can be completed by AI in under six hours.

- Furthermore, the increasing neuromorphic research is an emerging field within the areas of AI hardware anticipated to boost the demand for AI chips. The intuition here is to develop techniques inspired by the real neurons in the brain function; hence, the name neuromorphic was used. The low energy and high-quality output of neurons have enthused researchers to develop Spiking Neural Networks (SNNs). However, these SNNs require hardware of their own.

- The outbreak of COVID-19 has negatively impacted the AI chipsets market's supply chain and production. The impact on semiconductor producers was severe. The acceptance of AI for improving consumer services and reducing operational costs, the expanding number of AI applications, improving processing power, and the growing adoption of deep learning and neural networks are major market drivers. Many companies in the semiconductor supply chain worldwide restricted or even stopped operations due to workforce constraints, causing a bottleneck for semiconductor-dependent end-product companies.

AI Chipsets Market Trends

Consumer Electronics Is Expected to Witness Significant Growth

- Semiconductor chip shortage halted the production of consumer electronics worldwide due to the COVID-19 pandemic. However, the pandemic created a huge demand for consumer electronics, such as laptops, desktops, and gaming consoles, causing chaos for product companies, manufacturers, and end consumers. Equipment manufacturers focused on meeting this demand from the volatile consumer technology market. The chip shortage and high demand scenario are expected to continue until the next 2 to 3 years, driving the demand for AI chips for consumer electronics.

- The market will benefit from the increased use of quantum computing technologies to tackle complicated issues and perform analytical computations. For example, Google LLC's Sycamore quantum computer is the fastest computer, capable of completing work in roughly 200 seconds. Artificial intelligence, machine learning, computer vision, Big Data, AR/VR, and other technologies enable quantum computers. The expanding understanding of quantum computing will boost the demand for AI chipsets, thus boosting the industry's growth.

- AI technologies have been deployed in various industries, including automotive and manufacturing, to streamline processes. The industry may benefit from manufacturers' focus on enhanced AI-based solutions during the pandemic. For example, in May 2020, Nvidia Corporation updated its EGX Edge AI platform by launching new devices, namely, the EGX Jetson Xavier NX and EGX A100.

- The consumer electronics category is likely to occupy a major proportion of the AI chipset market during the forecast period. Various electronic devices, such as tablets and smartphones, are in high demand in the market with high-end specifications. Numerous manufacturers are continuously introducing novel AI chipsets to cater to the rising demand. For instance, in May 2022, MediaTek, a Taiwanese chipmaker, announced the Genio architecture for artificial intelligence of things (AIoT) devices, as well as the Genio 1200 chip. Premium AIoT solutions based on the Genio 1200 chip will be widely accessible in the latter half of 2022, according to MediaTek.

- The AI chipsets market is being driven by the increasing need for high-speed computer processors and increasing demand for better customer services and lower operating costs. The industry is being restrained by a shortage of experienced labor and a lack of standards and protocols.

Asia-Pacific Is Anticipated to Witness Significant Growth

- The Asia-Pacific market is projected to grow significantly due to emerging economies like South Korea, India, and China. The increased acceptance of AI-based solutions will support the market's healthy expansion in the region. The growing application of AI chipsets in consumer electronics, such as smartphones, tablets, and laptops, involves integrating voice commands, among others, which has resulted in the high adoption of AI chipsets in the region.

- Japan was one of the first nations to adopt a national AI policy. Japan's approach, primarily focused on making AI helpful to both society and the economy, intends to expand AI R&D skills, build AI systems with industrial applications, and prepare workers for labor market transformations. In June 2019, Prime Minister Shinzo Abe unveiled a plan to train 250,000 people in AI skills annually by 2025.

- The integration of voice commands, enhancement of photography experience, gathering and sorting relevant data based on previous searches, and other applications of AI chipsets in consumer electronics, such as smartphones, tablets, and laptops, resulted in the high adoption of AI chipsets.

- The region is home to the world's largest smartphone manufacturers and semiconductor companies. China, Japan, Taiwan, and South Korea account for roughly 80% of smartphone manufacturers worldwide. The greatest population has led to increased smartphone usage, which is likely to drive market growth.

- Several market players in the region are at the forefront of developing and producing AI chips. For instance, in August 2021, Baidu, a Chinese tech giant, started mass-producing second-generation Kunlun AI chips to become a major player in the chip industry. According to Baidu, the new generation of Kunlun AI chips is produced using 7 nm process technology, with computational capability 2-3 times better than the previous generation.

AI Chipsets Industry Overview

- Though some small and large global companies have influenced the market, the AI chipsets market is expected to be moderately consolidated. The market is still in its early stages of development. Some of the prominent participants in the current industry include Intel Corporation, Samsung Electronics, NVIDIA Corp., Xilinx Inc., and Micron Technology. To obtain leading positions in the AI chipsets market, these players are engaged in competitive strategic advancements, such as collaborations, new product innovations, and market expansions.

- August 2021 - IBM announced a new chip, Telum, which is expected to allow IBM clients to leverage deep learning inference at scale. This chip features a centralized design enabling clients to leverage the full power of the AI processor for AI-specific workloads, making it suitable for financial services workloads, such as loan processing, clearing and settlement of trades, fraud detection, anti-money laundering, and risk analysis.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the AI Chipsets Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Demand for Autonomous Driving Technology

- 5.1.2 Growth in Edge Analytics for IoT Application

- 5.2 Market Restraints

- 5.2.1 Complexity in Design and AI Interface

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Central Processing Unit (CPU)

- 6.1.2 Graphics Processing Unit (GPU)

- 6.1.3 Neural Network Processor (NNP)

- 6.1.4 Other Components

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Healthcare

- 6.2.4 Automation and Robotics

- 6.2.5 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Advanced Micro Devices Inc. (AMD)

- 7.1.2 Xilinx Inc.

- 7.1.3 Graphcore Ltd

- 7.1.4 Huawei Technologies Co. Ltd

- 7.1.5 IBM Corporation

- 7.1.6 Intel Corporation

- 7.1.7 NVIDIA Corporation

- 7.1.8 Micron Technology Inc.

- 7.1.9 Samsung Semiconductor (Samsung Electronics Co. Ltd)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

AI最佳化資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶、功能

AI最佳化資料中心市場分析及預測(至2035年):類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶、功能 2026年全球人工智慧(AI)晶片組市場報告2026年全球人工智慧(晶片組)市場報告

2026年全球人工智慧(AI)晶片組市場報告2026年全球人工智慧(晶片組)市場報告 AWS Annapurna Labs 全球人工智慧、運算、資料和量子處理器採用情況分析低功耗人工智慧晶片組市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、設備、最終用戶、功能、部署類型和解決方案分類

AWS Annapurna Labs 全球人工智慧、運算、資料和量子處理器採用情況分析低功耗人工智慧晶片組市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、設備、最終用戶、功能、部署類型和解決方案分類 全球人工智慧最佳化資料中心能源管理市場:預測(至 2034 年)—按組件、資料中心類型、部署方式、技術、最終用戶和地區進行分析2026年全球生成式人工智慧晶片組市場報告

全球人工智慧最佳化資料中心能源管理市場:預測(至 2034 年)—按組件、資料中心類型、部署方式、技術、最終用戶和地區進行分析2026年全球生成式人工智慧晶片組市場報告 全球人工智慧GPU晶片市場,2025-2029年

全球人工智慧GPU晶片市場,2025-2029年 人工智慧晶片組市場-全球產業規模、佔有率、趨勢、機會和預測,按人工智慧晶片組類型、技術、終端用戶產業、地區和競爭格局分類,2021-2031年預測全球人工智慧晶片組市場:預測至 2032 年—按組件、功能、部署方式、技術、公司類型、最終用戶和地區進行分析

人工智慧晶片組市場-全球產業規模、佔有率、趨勢、機會和預測,按人工智慧晶片組類型、技術、終端用戶產業、地區和競爭格局分類,2021-2031年預測全球人工智慧晶片組市場:預測至 2032 年—按組件、功能、部署方式、技術、公司類型、最終用戶和地區進行分析

▼