|

市場調查報告書

商品編碼

1641997

專業服務自動化:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Professional Services Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

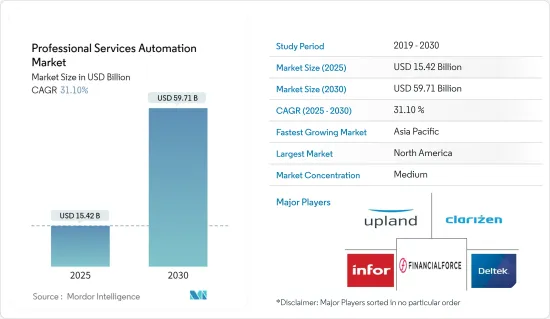

專業服務自動化市場規模在 2025 年預計為 154.2 億美元,預計到 2030 年將達到 597.1 億美元,預測期內(2025-2030 年)的複合年成長率為 31.1%。

對於尋求快速有效處理的收件人來說,手動、實體、紙本發票帶來了許多挑戰。

主要亮點

- 市場正在見證多種解決方案創新,這些創新正在幫助推動市場成長。例如,VOGSY 是唯一基於 Google G Suite 建構的 PSA 解決方案,為專業服務組織的整體流程提供業務流程支援和整合。它建立在單一、可訪問的平台上,為所有部門的員工提供支援。 VOGSY 最重要的差異化因素是我們建立了簡單而又複雜的 PSA 解決方案,使用戶能夠做更多的事情。

- 由於前所未有的部署靈活性、擴充性、增強的協作、成本效益優勢和全球可用性,預計在預測期內雲端基礎的部署類型將在應收帳款自動化市場中顯著成長。市場上有多家供應商透過公共雲端和私有雲端提供付款收集解決方案,這些解決方案透過各種訂閱和計量收費模式提供。

- 新冠肺炎疫情影響全球,對新創階段的企業和政府造成了嚴重的負面影響。它對審核、會計和其他財務流程產生了嚴重影響。自那時起,由於當時市場需要的技術創新和進步,該行業和供應商經歷了顯著的成長。專業服務自動化市場預計將繼續保持良好的成長動能。

專業服務自動化 (PSA) 市場趨勢

BFSI 主導專業服務自動化市場

- 銀行業的自動化透過自動執行重複且耗時的後端業務,幫助金融機構簡化業務、降低業務成本並最佳化債務催收流程。它也有助於推動產業發展,消除冗餘流程,提高金融機構的信任。此外,金融機構可以將寶貴的資源重新分配到各種其他重要的增值計劃和不可避免的人力參與的任務上。

- 服務自動化正在被 BFSI 領域廣泛採用,以大規模自動化發票處理、資料輸入、彙報、現金收款、債務追收、供應商付款等交易業務。近日,中國工商銀行正式為不列顛哥倫比亞省客戶推出個人ICBC保險單線上續保服務。

- 此外,根據紐約聯邦儲備銀行預測,截至2022年第二季度,美國消費者債務將超過16兆美元。其中大部分是房屋抵押貸款,約10.4兆美元,其次是學生貸款,約1.59兆美元。

北美主導專業服務自動化市場

- 北美佔據著大部分的市場佔有率。北美區域市場涵蓋了該行業大部分的技術領導者。這些領導者積極致力於推動現有技術並增加創新市場產品。由於勞動力快速老化,該地區的需求不斷增加,自動化將促進順利管理和有效分配可用資源。

- 北美區域成長的動力來自於服務業加速擴張和技術不斷發展。此外,該地區的組織正在採用無機成長策略來擴大其全球影響力。

- 此外,該地區兩大經濟體美國和加拿大正在投資新興技術並開發IT基礎設施設施。由於 Autotask Corporation 和 FinancialForce.com 等主要市場參與者提供專業服務自動化軟體和服務,美國是該地區的重要股東。

- 此外,北美是摩根大通、Visa、萬事達卡和美國銀行等主要 BFSI 公司的所在地,這些公司是專業服務自動化市場的主要貢獻者和推動者。

專業服務自動化 (PSA) 產業概覽

專業服務自動化市場是半靜態的。當今的專業服務公司面臨的挑戰包括缺乏知識淵博和經驗豐富的人才、強勁的市場環境、併購衍生以及日益成熟的客戶。同時,決策者和高階主管們對PSA解決方案的優勢及其在提高公司競爭力和盈利方面的作用有了更深入的了解。市場的一些關鍵發展包括:

- 2022 年 10 月-Infor 宣布將在海德拉巴 Hitec City 開設新的開發中心 (DC),擴大其印度業務。該公司還宣布,將在一塊佔地 35 萬平方英尺的土地上建造一座新的多層、最先進的開發中心,可容納 3,500 名員工。此外,這項投資將使 Infor 能夠開拓數位技術,包括雲端、行動性、資料分析、人工智慧和物聯網,以提供新的產業特定功能。

- 2022 年 5 月-Mavenlink 和 Kimble Applications 宣布推出Kantata,這是兩家公司成功合併和整合後成立的。兩家公司表示,Kantata 將加速開發和交付最全面的垂直 SaaS 解決方案,旨在幫助專業服務機構最佳化和提高業務績效,打造蓬勃發展的業務。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況(新冠疫情對市場的影響)

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場動態

- 市場促進因素

- 自動化和降低成本的趨勢日益增強

- 中小企業需求旺盛

- 市場挑戰

- 市場缺乏產品訊息

第6章 市場細分

- 依部署類型

- 本地

- 雲

- 按類型

- 解決方案

- 發票

- 計劃管理

- 費用管理

- 其他解決方案

- 服務

- 解決方案

- 按最終用戶產業

- BFSI

- 建築、工程和建設

- 法律服務

- 衛生保健

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第7章 競爭格局

- 公司簡介

- Autotask Corporation(Datto Inc.)

- Mavenlink, Inc.

- Clarizen Inc.

- Deltek Inc.

- Financialforce Inc.

- Infor Inc.

- NetSuite Inc.(Oracle Corporation)

- Upland Software Ltd.

- Projector PSA Inc.

- Replicon Inc.

- Unanet Technologies

- Workfront, Inc

第8章投資分析

第9章 市場機會與未來趨勢

The Professional Services Automation Market size is estimated at USD 15.42 billion in 2025, and is expected to reach USD 59.71 billion by 2030, at a CAGR of 31.1% during the forecast period (2025-2030).

Paper-based invoices that are manual & physical pose several challenges for recipients looking to quickly and effectively process them.

Key Highlights

- The market has witnessed several solution innovations, aiding in the market growth. For instance, VOGSY, the only PSA solution built on Google's G Suite, offers business process support and integration across the core processes of professional services organizations. It is built on a single, accessible platform and supports employees across all departments. VOGSY's most significant differentiator is that it created a simple yet sophisticated PSA solution that engages users to do more.

- Cloud-based deployment types are expected to have significant growth in the accounts receivable automation market during the forecast period due to their unprecedented deployment flexibility, scalability, enhanced collaboration, cost-efficiency benefits, and global availability. Several vendors in the market are providing payment collection solutions through the public and private cloud, and solutions are available in various subscriptions and pay-per-use models.

- COVID-19 had a global impact and, in turn, severely influenced businesses and governments in a deeply negative way at the starting phase. The implications for auditing, accounting, and other financial processes were severely affected. Later the industry and its vendors saw a significant boost due to their innovations and advancement, which were the market's needs at the time. And excellent growth is expected in the future of the market of Professional Services Automation.

Professional Services Automation (PSA) Market Trends

BFSI Holds a Dominant Position in Professional Services Automation Market

- Automation in the banking industry helps financial institutions simplify their operations, minimizing the operation costs and optimizing their credit collection process by automating the repetitive and time-taking backend tasks. It also helps the industry evolve, eliminate redundant processes, and improve the credibility of financial institutions. It further allows the institutions to deploy their valuable resources to various other critical value-added projects and tasks where the involvement of humans is inevitable.

- Services automation is widely adopted in the BFSI sector as it automates transactional tasks at scale, such as processing invoices, data entry, reporting, cash collection, credit collection, payment to vendors, and many more. Recently, ICBC launched the convenience of renewing personal ICBC insurance policies online for its customer in British Columbia, which will enable them to have the option to renew their policy using their computer, tablet, or mobile device.

- Moreover, according to New York Fed, Consumers in the United States had over USD 16 trillion in debt as of the second quarter of 2022. In addition, they stated that most of that debt was home mortgages, at approximately USD 10.4 trillion and Student loan debt was the second largest component, totaling approximately USD 1.59 trillion.

North American Holds a Dominant Share of Professional Services Automation Market

- North America occupies a significant share of the market. North America's regional market includes the majority of industry technology leaders. These leaders are actively operating towards the progress of existing technologies and the growth of innovative market offerings. Greater demand is experienced owing to the quickly aging workforce in the region, and automation facilitates smooth management and effective allocation of available resources.

- North America's regional growth can further be attributed to the accelerated sprawl in the service industry and advancing technological developments. The regional organizations have also embraced inorganic growth strategies to encourage global presence.

- Furthermore, the region's two advanced economies, the US and Canada, are investing in emerging technologies and have developed IT infrastructure facilities. The US is a significant shareholder in this region, owing to the presence of leading market players giving professional service automation software and services, such as Autotask Corporation, and FinancialForce.com, among others.

- Moreover, North America is a hub for major BFSI companies like JP Morgan Chase, Visa, Mastercard, and Bank of America, which contribute a lot towards the market of Professional Services Automation and drive the market.

Professional Services Automation (PSA) Industry Overview

The professional services automation market is semi-consolidated. Professional services firms are currently confronted with challenges such as a shortage of knowledgeable and experienced resources, robust market environments, spin-offs from mergers and acquisitions, and increasingly refined and sophisticated clients. At the same time, decision-makers and best executives are becoming more informed of PSA solutions' benefits and their role in making firms more competitive and profitable. Some of the key developments in the market are:

- October 2022 - Infor announced the expansion of its India operations by opening a new development center (DC) in Hitech City, Hyderabad. In addition, the company stated that the new multi-story state-of-the-art development center is spread over 350,000 square feet with a capacity for 3,500 employees. Moreover, this investment will allow Infor to pioneer digital technologies such as cloud, mobility, data analytics, artificial intelligence, and IoT to deliver new industry-specific features and functions specialized for industries.

- May 2022 - Mavenlink and Kimble Applications announced the launch of Kantata, formed through the successful merger and integration of the two companies. The companies stated that Kantata was created to accelerate the development and delivery of the most comprehensive range of vertical SaaS solutions purpose-built that helps professional services organizations to optimize and elevate operational performance for building thriving businesses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (followed by impact of COVID-19 on the market)

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Trend of Automation and Reduction in the Overall Cost

- 5.1.2 High Demand from Small and Medium Enterprise

- 5.2 Market Challenges

- 5.2.1 Lack of Product Information in the Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-Premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Solutions

- 6.2.1.1 Billing & Invoice

- 6.2.1.2 Project Management

- 6.2.1.3 Expense Management

- 6.2.1.4 Others Solutions

- 6.2.2 Services

- 6.2.1 Solutions

- 6.3 By End-user Industry

- 6.3.1 BFSI

- 6.3.2 Architecture, Engineering, and Construction

- 6.3.3 Legal Services

- 6.3.4 Healthcare

- 6.3.5 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Autotask Corporation (Datto Inc.)

- 7.1.2 Mavenlink, Inc.

- 7.1.3 Clarizen Inc.

- 7.1.4 Deltek Inc.

- 7.1.5 Financialforce Inc.

- 7.1.6 Infor Inc.

- 7.1.7 NetSuite Inc. (Oracle Corporation)

- 7.1.8 Upland Software Ltd.

- 7.1.9 Projector PSA Inc.

- 7.1.10 Replicon Inc.

- 7.1.11 Unanet Technologies

- 7.1.12 Workfront, Inc

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球專業服務自動化軟體市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球專業服務自動化軟體市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 2025年專業服務自動化軟體全球市場報告2025 年專業服務自動化全球市場報告

2025年專業服務自動化軟體全球市場報告2025 年專業服務自動化全球市場報告 專業服務自動化軟體市場規模、佔有率、成長分析,按組件、按部署類型、按組織規模、按最終用戶行業、按地區 - 行業預測,2025-2032 年

專業服務自動化軟體市場規模、佔有率、成長分析,按組件、按部署類型、按組織規模、按最終用戶行業、按地區 - 行業預測,2025-2032 年 全球專業服務自動化市場:市場規模、佔有率、趨勢、產業分析(依部署方法、組織規模、最終用途產業和地區)、未來預測(2025-2034)全球專業服務自動化軟體市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)

全球專業服務自動化市場:市場規模、佔有率、趨勢、產業分析(依部署方法、組織規模、最終用途產業和地區)、未來預測(2025-2034)全球專業服務自動化軟體市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031) 專業服務自動化軟體市場:按組件、部署類型、組織規模和產業 - 2025-2030 年全球預測

專業服務自動化軟體市場:按組件、部署類型、組織規模和產業 - 2025-2030 年全球預測 全球專業服務自動化 (PSA) 軟體市場 2024-2028到 2030 年專業服務自動化 (PSA) 市場預測:按組件、部署類型、組織規模、最終用戶和區域進行的全球分析

全球專業服務自動化 (PSA) 軟體市場 2024-2028到 2030 年專業服務自動化 (PSA) 市場預測:按組件、部署類型、組織規模、最終用戶和區域進行的全球分析