|

市場調查報告書

商品編碼

1642024

東南亞國協倉儲與配送物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)ASEAN Warehousing And Distribution Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

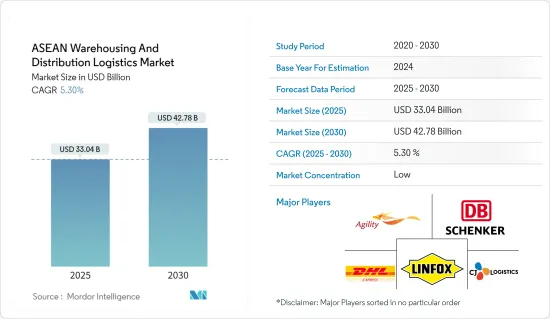

東南亞國協倉儲和配送物流市場規模預計在2025年為330.4億美元,預計到2030年將達到427.8億美元,預測期內(2025-2030年)複合年成長率為5.3%。

作為全球成長最快的經濟體之一,東南亞受惠於由全球貿易、外來投資以及區域和全球價值鏈一體化所推動的廣泛經濟成長模式。然而,為了維持這一成長勢頭,需要進行多項改革來增強該地區的經濟和社會復原力。這些改革包括降低競爭和市場准入的監管壁壘,以促進創新、生產力和效率。

由於電子商務領域的快速成長,東協的倉儲和配送物流預計將快速成長。最後一哩物流的高需求和快速發展的交通基礎設施正在促進東協倉儲和配送物流市場的發展。除了物流業的成長之外,外國公司在該地區的存在以及政府的舉措(例如 Adapt 和 Grow &Go Digital)也推動了該地區倉儲和配送市場的成長。新加坡是東協主要國家之一。其地理位置和強大的貨運及物流業務使其成為該地區發展最快的國家之一。該地區的大型公司正在大力投資倉儲基礎設施。

一些地區對倉庫的需求正在增加,這主要是由於電子商務的成長。去年,專門開發倉庫和工廠的BW(越南第一大工廠開發商)收到的請求比以往任何時候都多。 BW的長期發展策略是有效利用這些短期機會,透過建造輕型、現代化的工業倉庫來滿足製造業日益成長的需求和電子商務的爆炸性成長。

冷藏需求的不斷成長迫使企業調整其供應鏈策略。據行業報告稱,外國投資者對在越南建造冷藏倉庫的興趣日益濃厚,因為他們受益於都市化進程和零售現代化,從而改變了越南大城市獲取生鮮食品的方式。隨著重大基礎設施的投資和發展,例如期待已久的隆城國際機場的建設,預計未來的供應鏈將變得更加高效。

東南亞國協倉儲配送物流市場趨勢

增加泰國的倉庫空間

倉庫不只是一個倉庫。進行即時包裝、組裝和產品客製化等增值業務。過去五年來,泰國的電子商務經歷了巨大的成長。該電子商務倉庫群位於曼谷 Bangna-Trat 路沿線 15 公里至 23 公里處。

近年來,泰國的零售市場大幅成長。在全國範圍內,有組織的零售和現代購物穩步成長。隨著泰國民眾可支配收入的不斷增加、年輕人口的龐大以及旅遊業的蓬勃發展,許多外國品牌正在進入泰國。這導致倉儲服務的增加。

在泰國,由於經濟逐漸復甦,倉庫租賃業者預計將在預測期內繼續擴大業務,這主要得益於出口產業的改善和國內零售業的復甦。未來三年對新供應的投資可能會增加。大型營運商將處於最前線,造成部分局部市場供應過剩,加劇價格競爭,限制營運商提高租金的能力。

大多數營運商目前正在對其設施進行現代化改造,以提供現代化的倉儲解決方案,從而擴大基本客群並透過附加服務增加收益。參與企業還將升級倉庫建築,以滿足行業標準(例如LEED 計劃),投資於能源效率和環境保護,並安裝設施,使其更能抵禦洪水和地震等自然災害。進行現代化改造手段,例如:倉庫擴大了占地面積和天花板空間,以提高貨物運輸的速度和便利性。

電子商務成長推動東南亞國協市場

東南亞電子商務的現階段不僅僅是增值。該地區的消費者擴大透過各種管道在網路上購買各種各樣的產品。該地區的供應鏈可能需要新的物流能力來滿足日益成長的履約需求。已經具備這些能力的公司和新進者都可能從這些變化中受益最多。

東南亞是一個由處於不同發展階段的經濟體組成的大雜燴,因此各國的電子商務普及率有差異也是自然而然的。印尼和新加坡佔該地區電子商務滲透率的 30% 左右,緊隨其後的是菲律賓、泰國和越南,各佔 15% 左右。印尼作為東南亞最大的經濟體,憑藉其龐大的消費市場,佔該地區GMV成長的51%。

隨著東南亞電子商務市場進入下一個成長階段,消費者在付款產品類別和通路上進行更多的數位購買,提出了更高的要求,並創造了新的、先進的物流解決方案。 。另一方面,隨著供應鏈的轉變,分銷商可能會減少對中國進口的依賴,並將採購路線擴展到更多東南亞國家。因此,他們將尋求擴大上游能力,以獲得更廣泛的價值組合,為物流供應商開闢更多的管道。

東南亞國協倉儲配送物流產業概況

東南亞國協倉儲配送物流市場細分化,許多參與企業爭奪新興市場的關鍵地位。東協地區的一些國家,例如印尼和菲律賓,成長緩慢,既有許多本土參與企業,也有一些國際參與企業。然而,新加坡、越南和泰國是競爭激烈的市場,擁有許多國際參與企業。 CEVA、Yusen Logistics、Kerry Logistics 和 DHL 是該地區的主要參與者。電子商務和國際貿易的壓力越來越大,促使參與企業在該地區建立許多倉庫。長期在國內的存在使得本地參與企業和經銷商能夠與國際參與企業競爭。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

- 分析方法

- 研究階段

第3章執行摘要

第4章 市場動態與洞察

- 當前市場狀況

- 市場動態

- 驅動程式

- 在黃金位置策略性地放置倉庫起著關鍵作用

- 電子商務的興起導致倉庫空間增加

- 限制因素

- 物流倉儲市場競爭激烈,既有國內的競爭對手,也有國外的參與企業。

- 複雜的法律規範,包括稅收、許可證和許可要求,可能成為進入障礙

- 機會

- 自動化在建造未來倉庫中發揮關鍵作用

- 驅動程式

- 產業吸引力-波特五力分析

- 價值鏈/供應鏈分析

- 東南亞國協政府法規

- 倉庫技術開發

- 倉庫租金洞察

- 一般倉儲業見解

- 危險品倉庫洞察

- 深入了解冷藏

- 洞察電子商務成長的影響

- 深入了解自由區和工業

- COVID-19 對市場的影響

第5章 市場區隔

- 按地區

- 新加坡

- 泰國

- 馬來西亞

- 越南

- 印尼

- 菲律賓

- 其他東南亞國協

第6章 競爭格局

- 公司簡介

- DHL Supply Chain

- Ceva Logistics

- CJ Century Logistics

- DB Schenker

- Agility

- Linfox

- Kuehne+Nagel

- Yusen Logistics

- Kerry Logistics

- CWT Ltd

- Gemadept

- Tiong Nam Logistics

- Ych Group

- Singapore Post

- WHA Corporation

- Keppel Logistics*

- 其他公司(關鍵資訊/概況)

第7章:未來趨勢與機遇

第 8 章 附錄

The ASEAN Warehousing And Distribution Logistics Market size is estimated at USD 33.04 billion in 2025, and is expected to reach USD 42.78 billion by 2030, at a CAGR of 5.3% during the forecast period (2025-2030).

As one of the world's fastest-growing economies, Southeast Asia has benefitted from a broad-based economic growth model based on global trade, inward investment, and regional and global integration into value chains. However, sustaining this growth momentum will necessitate several reforms to strengthen the region's economic and social resilience. These reforms will include lowering regulatory barriers to competition and market entry to promote innovation, productivity, and efficiency.

Warehousing and distribution logistics in ASEAN are expected to experience rapid growth due to the rapid growth of the e-commerce sector. The high demand for last-mile logistics and the fast-developing transportation infrastructure contribute to the development of ASEAN's warehousing and distribution logistics market. The presence of foreign firms in the region, as well as government initiatives like Adapt and Grow & Go Digital, in addition to the growing logistics industry, is driving the growth of the warehousing and distribution market in the region. Singapore is one of the major countries in ASEAN. With its geographical location and strong freight and logistics business, it is one of the fastest-growing countries in the region. Major players in the region have significantly funded the warehouse infrastructure.

Warehousing demand has been on the rise in some regions, mainly due to the growth of e-commerce. The previous year, BW (Vietnam's #1 Industrial For-Rent Developer), specializing in developing warehouses and factories to rent, received unprecedented requests. BW's long-term development strategy allowed it to take advantage of these short-term opportunities effectively by constructing light and contemporary industrial warehouses to cater to the growing manufacturing demand and the explosion of e-commerce growth.

The demand for cold storage is rising, forcing companies to adjust their supply chain strategies. According to the industry report, foreign investors are increasingly interested in building cold storage facilities in Vietnam to benefit from the urbanization process and retail modernization, changing how Vietnam's big cities get fresh food. The supply chains are expected to become more efficient in the future due to significant infrastructure investment and development, including the construction of the long-awaited Long Thanh International Airport.

ASEAN Warehousing And Distribution Logistics Market Trends

Increase in Warehousing Space in Thailand

Warehouses are not just storage rooms. They house value-added operations such as just-in-time packing, assembly, product customization, etc. Over the past five years, Thailand has seen incredible growth in e-commerce. The e-commerce warehousing cluster is between 15 and 23 km along Bang Na-trat Road in Bangkok.

Thailand has seen massive growth in the retail market in recent years. There has been a steady rise in organized retail or contemporary shopping nationwide. The increasing disposable income of the people in Thailand, the large youth population, and the booming tourism industry have attracted a lot of foreign brands. This has led to an increase in warehousing services.

During the forecast period in Thailand, operators of leased warehouse space will continue to experience business growth in line with a gradual economic upturn, driven mainly by an upturn in the export industry and a recovery in domestic retail. Investment in new supply tends to increase over the next three years. Large players will be at the forefront of this, leading to oversupply in some local markets, increasing competition on pricing, and limiting operators' ability to increase rents.

Currently, the majority of operations are modernizing their facilities to provide modern warehousing solutions, which, in turn, allows them to expand their client base and generate revenue through additional services. Players are also modernizing their facilities through other means, such as upgrading their warehouse buildings to meet industry standards (for example, the LEED scheme), investing in energy efficiency and environmental protection, and installing facilities that enhance resilience to natural disasters, such as flooding and earthquakes. Warehouses have expanded their floor and ceiling space, increasing the speed and ease of goods movement.

E-commerce Growth in the ASEAN Region is Driving the Market

The current phase of e-commerce in Southeast Asia is about more than just increasing value. Consumers in the region increasingly purchase a wider range of products online through various channels. The region's supply chains will likely require new logistics capabilities to meet this growing demand for fulfillment. Those who already possess these capabilities and those new to the market will benefit the most from these changes.

Southeast Asia is a patchwork quilt of economies at various stages of development; it is only natural that e-commerce penetration rates vary from country to country. Indonesia and Singapore account for approximately 30% of the region's e-commerce penetration, with the Philippines, Thailand, and Vietnam trailing at around 15% each. The largest Southeast Asian economy, Indonesia, accounts for 51 of the region's GMV growth due to its large consumer market.

As Southeast Asia's e-commerce market moves into the next phase of growth, customers will make more digital purchases across all product categories and channels, and they will also demand and pay more for new and advanced logistics solutions. On the other hand, merchants will be less reliant on Chinese imports and expand their sourcing channels to more Southeast Asian countries as they migrate their supply chains. As a result, they will look to extend their upstream capabilities to access a wider value mix, which will open up more channels for logistics providers.

ASEAN Warehousing And Distribution Logistics Industry Overview

The warehousing and distribution market in the ASEAN region is fragmented, with many players trying to grab a significant chunk of the developing market. Some of the countries in the ASEAN region, like Indonesia and the Philippines, are moderately growing, with many local players and some international players. However, Singapore, Vietnam, and Thailand are highly competitive markets, with the presence of a large number of international players. CEVA, Yusen Logistics, Kerry Logistics, and DHL are among the major players present in the region. Increasing pressure from e-commerce and international trade has allowed the players to develop many warehouses in the region. Due to the long-term domestic presence, local players and distributors have been able to compete with international players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMERY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 The strategic placement of warehouses in key locations plays a crucial role

- 4.2.1.2 Warehousing Spaces are Increasing in the region due to the rise in e-commerce

- 4.2.2 Restraints

- 4.2.2.1 The logistics and warehouse distribution market is highly competitive, with both domestic and international players

- 4.2.2.2 Complex regulatory frameworks, including taxes, permits, and licensing requirements, can create barriers to entry

- 4.2.3 Opportunities

- 4.2.3.1 Automation plays a significant role in building the warehouse of the future

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Government Regulations in ASEAN Countries

- 4.6 Technological Developments in Warehousing

- 4.7 Insights into Warehousing Rents

- 4.8 Insights into General Warehousing

- 4.9 Insights into Dangerous Goods Warehousing

- 4.10 Insights into Refrigerated Warehousing

- 4.11 Insights into the Effects of E-commerce Growth

- 4.12 Insights into Free Zones and Industrial Parks

- 4.13 Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Geography

- 5.1.1 Singapore

- 5.1.2 Thailand

- 5.1.3 Malaysia

- 5.1.4 Vietnam

- 5.1.5 Indonesia

- 5.1.6 Philippines

- 5.1.7 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 DHL Supply Chain

- 6.2.2 Ceva Logistics

- 6.2.3 CJ Century Logistics

- 6.2.4 DB Schenker

- 6.2.5 Agility

- 6.2.6 Linfox

- 6.2.7 Kuehne + Nagel

- 6.2.8 Yusen Logistics

- 6.2.9 Kerry Logistics

- 6.2.10 CWT Ltd

- 6.2.11 Gemadept

- 6.2.12 Tiong Nam Logistics

- 6.2.13 Ych Group

- 6.2.14 Singapore Post

- 6.2.15 WHA Corporation

- 6.2.16 Keppel Logistics*

- 6.3 Other Companies (Key Information/Overview)