|

市場調查報告書

商品編碼

1642041

邊緣運算:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Edge Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

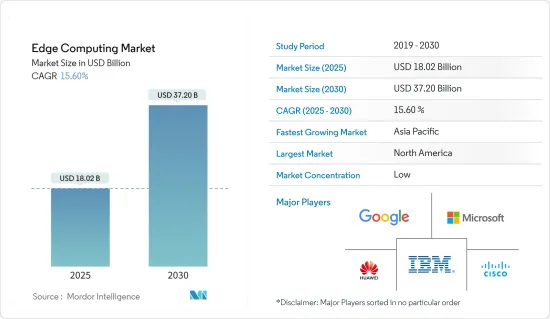

邊緣運算市場規模在 2025 年估計為 180.2 億美元,預計到 2030 年將達到 372 億美元,預測期內(2025-2030 年)的複合年成長率為 15.6%。

物聯網的不斷普及以及 5G 營運的增強是推動受調查市場成長的主要動力。相當一部分工業IoT服務供應商和聚合商正在提供支援 5G 的網路產品,並可能在未來幾年採用邊緣運算來處理大量資料。

主要亮點

- 在所調查的市場中取得重大進展的主要企業包括思科、HPE、戴爾和華為。這些公司正在開發適合工業現場惡劣工況和運作環境的邊緣運算產品,包括防電磁干擾、防塵、防爆、防振、防電流電壓波動等。這些公司正在努力透過夥伴關係和頻繁的產品開發來創造邊緣運算市場的下一個大事件。

- 邊緣運算由思科、英特爾、微軟和戴爾 EMC 等供應商以及由普林斯頓大學和普渡大學等學術機構主導的 OpenFog 聯盟等組織主導。該聯盟旨在為霧和邊緣運算部署開發參考架構。

- 2022 年 1 月,Verizon 與 AWS 合作,將行動邊緣運算擴展到美國 30% 的大都會區,新增夏洛特、底特律、洛杉磯和明尼阿波利斯。這種組合最大限度地減少了從平台上託管的應用程式連接到最終用戶設備所需的延遲和網路跳數。

- 邊緣運算市場由大型供應商主導,他們佔據了調查市場的很大佔有率,並且在各個地理市場激烈競爭以站穩腳跟。出於此原因,供應商正在建立多種聯盟和夥伴關係關係,以增加其市場佔有率和技術力。

- 例如,2022年4月,Ball與AWS續約了合約。此次合作旨在利用 AWS Wavelength 在加拿大啟動首個公共多接取邊緣運算(MEC) 部署。 5G網路可望為邊緣運算市場帶來新的成長機會。

- 隨著企業以服務速度和低延遲作為差異化策略,COVID-19 疫情將對 5G 和多重存取邊緣運算 (MEC) 的部署產生正面影響。更深層的網路和運算融合以支援次世代應用程式是未來的發展方向。

邊緣運算市場趨勢

預計通訊業將以顯著的複合年成長率成長

- 通訊是全球市場上成長最快的產業之一。該產業目前正在升級其基礎設施,為 5G 轉型做準備,再加上全球 5G 應用的快速成長,推動通訊業對邊緣運算資源的投資。

- 在5G和物聯網的推動下,邊緣運算將徹底重塑通訊網路。此外,對雲端的依賴、對網路連接的依賴以及物聯網的巨大成長和潛力是推動通訊業者走向邊緣的一些關鍵因素。通訊業者不僅可以利用邊緣來增強其核心連接業務、減少客戶延遲,還可以引入邊緣資料管理等新服務。

- 此外,隨著 5G 技術受到更多監管並成為主流,預計符合 5G 標準的設備數量將會增加,從而帶來一些容量挑戰。雖然毫米波頻段有望與 3G 和 4G 頻段有很大差異,但不斷成長的用戶數量可能會對邊緣的額外運算資源產生需求。例如,根據GSMA Intelligence的資料,全球5G市場滲透率預計將從2020年的3%增加到2030年的64%。

- 5G、物聯網和邊緣運算的結合將為通訊服務提供者及其客戶帶來變革。邊緣運算技術已成為通訊業的主要投資領域,這得益於通訊服務供應商 (CSP) 改善用戶體驗以及啟用和支援新經營模式的需求。 CSP 正在投資邊緣運算技術以滿足不斷成長的需求。

- 為了滿足全球市場的這一潛在需求,多種開放原始碼架構已相繼出現。開放網路基金會和 Akraino Edge Stack計劃等措施預計將加速該領域對邊緣運算的需求。

預計亞太地區將以最高複合年成長率成長

- 中國在5G和邊緣運算方面已經取得了良好的開端。監視文化可能會影響技術的發展。 Meta、蘋果、Netflix 和谷歌等西方公司透過制定使用個人資料投放廣告的標準塑造了全球數位經濟。阿里巴巴、百度、華為和中興等中國公司正在塑造邊緣運算支援的監控技術的未來方向。中國的這些努力滿足了需求,因此佔據了該地區的最高佔有率。

- 根據GSMA的調查,近90%的中國行動生態系統參與者將邊緣運算視為5G時代的關鍵商機。該國的邊緣運算部署旨在滿足智慧港口、校園和工廠的需求。隨著未來幾年 5G 網路的擴展,體育賽事、遊戲和自動駕駛等邊緣運算使用案例將成為可能。

- IIJ 已在其 Shirai資料中心園區(Shirai DCC)內部署了 MDC。 MDC 由澳洲製造商 Zella DC 生產,並首次在日本推出。它配備了資料中心的所有基本功能,包括冷卻、不斷電系統(UPS)、環境感測器、監視錄影機和實體安全(包括遠端啟動電子鎖)。

- 作為「數位印度」計畫的一部分,印度政府計劃在該國推廣物聯網。政府已撥款 7,000 億印度盧比用於建設 100 個由物聯網設備驅動的智慧城市。政府打算控制交通、有效利用水和電,並使用物聯網感測器收集資料以用於醫療保健和其他服務。

- 2022 年 2 月,Reliance Jio 在印度 50 多處物業的雲端原生 5G 網路上啟用了邊緣運算。通訊業者已經完成了針對印度「前 1,000 個城市」的 5G 計劃,並組建了專門的團隊,專注於在該國提供「專門的 5G 推出解決方案」。 Jio、Airtel 和 Vodafone Idea 目前正在使用實驗性 5G 頻譜與設備和企業合作夥伴一起試行創新的 5G 用例。

- 此外,2022 年 3 月,塔塔諮詢服務公司宣布使用 Microsoft Azure 私有行動邊緣運算(Private MEC)為企業推出一套 5G 邊緣解決方案。由於這些發展,預計預測期內亞太地區對邊緣運算的需求將會成長。

邊緣運算產業概覽

邊緣運算市場分散且競爭激烈。目前,市場由戴爾、微軟、亞馬遜和谷歌等雲端基礎的物聯網供應商主導。此外,通用電氣等公司憑藉其為航太和製造業等各行業提供邊緣運算解決方案的專業知識,在市場上也佔有重要地位。收購、與產業參與者的合作以及新產品/服務的推出是供應商的主要競爭策略。

- 2022 年 4 月 - 戴爾科技擴展其邊緣解決方案,幫助零售商從零售店產生的資料中更快地獲取更多價值並提供增強的客戶體驗。

- 2022年3月,華為與Du簽署了關於多接入邊緣運算(MEC)聯合創新的合作備忘錄。兩家公司將在中東研究、檢驗和複製MEC應用。兩家公司還旨在支持全球數位經濟的發展並加速中東地區的數位轉型。

- 2022 年 3 月 - Foghorn 與 IBM 合作,提供安全、開放的下一代混合雲平台,該平台具有先進的閉合迴路系統控制和邊緣驅動的人工智慧 (AI)。透過整合邊緣和雲端功能,Foghorn 和 IBM 計畫幫助客戶快速處理、部署、分析、儲存和訓練從邊緣到雲端的關鍵資料,以支援業務流程。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- COVID-19 市場影響評估

第5章 市場動態

- 市場促進因素

- 法律行業對自動化的需求不斷增加,訴訟案件數量不斷增加

- 律師事務所擴大使用人工智慧來完成法律事務

- 市場限制

- 敏感或合法資料的隱私問題

第6章 市場細分

- 按組件

- 硬體

- 軟體

- 服務

- 按最終用戶

- 金融與銀行

- 零售

- 醫療保健和生命科學

- 產業

- 能源與公共產業

- 通訊業

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 澳洲

- 其他亞太地區

- 拉丁美洲

- 墨西哥

- 巴西

- 其他拉丁美洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 北美洲

第7章 競爭格局

- 公司簡介

- Microsoft Corporation

- Google LLC(Alphabet Inc.)

- IBM Corporation

- Huawei Technologies Co. Limited

- Cisco Systems Inc.

- Hewlett Packard Enterprise Company

- Juniper Networks Inc.

- Dell Technologies Inc.

- Capgemini Engineering(Capgemini)

- EdgeIQ(MachineShop Inc.)

- ADLINK Technology Inc.

- General Electric Company

- Amazon Web Services Inc.

第8章投資分析

第9章:市場的未來

The Edge Computing Market size is estimated at USD 18.02 billion in 2025, and is expected to reach USD 37.20 billion by 2030, at a CAGR of 15.6% during the forecast period (2025-2030).

The increasing adoption of IoT is augmented by 5G operations, primarily driving the growth of the market studied. A significant share of industrial IoT service providers and aggregators are offering 5G capable network offerings that are expected to adopt edge computing over the coming years for handling the sheer amount of data.

Key Highlights

- The key players that are significantly active in the market studied include cisco, HPE, Dell, and Huawei. They have been developing edge computing products that adapt to harsh working conditions and operating environments at industrial sites, such as anti-electromagnetic interference, anti-dust, anti-explosion, anti-vibration, and anti-current/voltage fluctuations. These companies are making significant efforts in the edge computing market to create the next big thing by engaging in partnerships and making frequent product developments.

- Edge computing is being led by initiatives like OpenFog Consortium, an organization headed by vendors in the market studied, including Cisco, Intel, Microsoft, and Dell EMC, as well as academic institutions like Princeton University and Purdue University. The consortium aims at developing reference architectures for fog and edge computing deployments.

- In January 2022, Verizon and AWS partnered to expand to 30% more metro area locations in the United States with mobile edge computing with the addition of Charlotte, Detroit, Los Angeles, and Minneapolis. The combination minimizes the latency and network hops required to connect from an application hosted on the platform to the end user's device.

- The edge computing market is dominated by major vendors that cover a significant share of the market studied, and they are intensely competing to gain a foothold in different regional markets. Owing to this, vendors are involved in several partnerships and alliances to gain market presence and technological capabilities.

- For instance, In April 2022, Ball extended its agreement with AWS. This collaboration aims to launch the first public multi-access edge computing (MEC) with AWS Wavelength in Canada. 5G network is expected to bring new growth opportunities to the edge computing market.

- The COVID-19 pandemic positively affects the 5G and multi-access edge computing (MEC) deployments as businesses strategize service speed and low latency as key differentiators. The tight integration of network and compute to support next-generation apps is the way forward.

Edge Computing Market Trends

Telecommunication Sector is Expected to Grow at A significant CAGR

- Telecommunications is one of the fastest evolving industries in the global market. The industry is currently in the process of upgrading its infrastructure to prepare for the 5G transition coupled with the booming 5G penetration across the world, is driving the telecom sector to invest in edge computing resources.

- Edge computing is poised to significantly reshape telecom networks, driven by 5G and the IoT. Additionally, the dependence on the cloud, the reliance on internet connectivity, and the enormous growth and potential of the IoT are some of the critical factors driving telecoms toward the edge. Telecom operators can use edge both to boost their core connectivity business and reduce latency for their own customers, as well as to introduce new services such as data management at the edge.

- Further, as 5G technologies become more regulated and go mainstream, 5G-compliant devices are expected to grow, leading to several capacity issues. Although the mm-wave bands ensure that they are highly differentiated from the 3G or 4G bands, the increased number of subscriptions is likely to create demand for additional computing resources at the edge.For instance, according to the data from GSMA Intelligence, the 5G market penetration worldwide is expected to increase from 3% in 2020 to 64% in 2030.

- The combination of 5G, IoT, and edge computing would be transformational for both communication service providers and their customers. Edge computing technology has become the major area of investment in the telecom industry, driven by CSPs' need to enhance user experiences and enable and support new business models. CSPs are investing in edge computing technology to meet the growing demand.

- Owing to such potential demand in the global market, several open-source architectures are emerging. Initiatives by The Open Networking Foundation, Akraino Edge Stack project, and others, are expected to accelerate the demand for edge computing in the sector.

Asia Pacific is Expected to Grow at a Highest CAGR

- China has made a good start in terms of 5G and the edge; a surveillance culture could set the course for the evolution of technology. Western companies such as Meta, Apple, Netflix, and Google have shaped the global digital economy by establishing standards for using personal data to target ads. Chinese companies such as Alibaba, Baidu, Huawei, and ZTE are shaping the future direction of edge computing-backed surveillance technology. Such initiatives in China cater to the demand; thus, the country has the highest share in the region.

- According to a survey by GSMA, approximately 90% of mobile ecosystem players in China recognized edge computing as a significant revenue opportunity in the 5G era. The country's edge computing deployments are designed to meet smart ports, campuses, and factories' requirements. As the 5G networks scale over the next few years, edge computing use cases, such as sporting events, gaming, and autonomous driving, will be possible.

- IIJ deployed MDC on the premises of Shiroi Data Center Campus (Shiroi DCC). The MDC, from Australian manufacturer Zella DC, was the first to be installed in Japan. It is equipped with the functions a data center needs, including a cooling unit, an uninterruptible power supply (UPS), environmental sensors, security cameras, and physical security, including a remote-controlled electronic lock.

- As part of the Digital India initiative, the Government of India planned to give IoT a push in the country. The government has allocated INR 7,000-crore funds to develop 100 smart cities powered by IoT devices. The government intends to control traffic, efficiently use water and power, and collect data using IoT sensors for healthcare and other services.

- In February 2022, Reliance Jio enabled edge computing on its cloud-native 5G network at more than 50 facilities across India. The telco has completed 5G planning for the "top 1,000 cities" across India, and dedicated teams have been formed to focus on "dedicated solutions for 5G deployment" in the country. Jio, Airtel, and Vodafone Idea are currently piloting innovative 5G use cases with their equipment and enterprise partners using the trial 5G spectrum.

- Moreover, in March 2022, Tata Consultancy Services announced the launch of an enterprise 5G edge solution suite with Microsoft Azure Private Mobile Edge Computing (Private MEC). Such developments are poised to grow the demand for edge computing in the Asia Pacific region over the forecast period.

Edge Computing Industry Overview

The edge computing market is fragmented and competitive in nature. Currently, the market is dominated by cloud-based IoT vendors, such as Dell, Microsoft, Amazon, and Google. Companies like GE, which have the expertise of delivering edge computing solutions across different industries, including aerospace or manufacturing, also have significant market positions. Acquisitions, partnerships with industry participants, and new product/service rollouts have been the vendors' key competitive strategies. Some of the recent developments in the market are:

- April 2022 - Dell Technologies expanded its edge solutions to help retailers quickly generate more value and deliver enhanced customer experiences from data generated in retail locations.

- March 2022 - Huawei and Du signed a memorandum of understanding (MoU) for joint innovation on multiaccess edge computing (MEC). The two companies would research, verify, and replicate MEC-oriented applications in the Middle East. The companies also aim to accelerate digital transformation in the Middle East, along with supporting the development of the global digital economy.

- March 2022 - FogHorn collaborated with IBM to provide a secure and open next-generation hybrid cloud platform with advanced, closed-loop system control capabilities and edge-powered artificial intelligence (AI). By bringing together edge and cloud capabilities, FogHorn and IBM plan to help customers rapidly process, deploy, analyze, store, and train critical data from the edge to the cloud and enhance their business processes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand For Automation And Increasing Number Of Litigations In The Legal Industry

- 5.1.2 Growth In The Utilization Of Ai By Legal Companies To Complete Legal Cases

- 5.2 Market Restraints

- 5.2.1 Data Privacy Concerns Of The Confidential And Legal Data

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 By End-user

- 6.2.1 Financial and Banking Industry

- 6.2.2 Retail

- 6.2.3 Healthcare and Life Sciences

- 6.2.4 Industrial

- 6.2.5 Energy and Utilities

- 6.2.6 Telecommunications

- 6.2.7 Other End-users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Australia

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.4.1 Mexico

- 6.3.4.2 Brazil

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Microsoft Corporation

- 7.1.2 Google LLC (Alphabet Inc.)

- 7.1.3 IBM Corporation

- 7.1.4 Huawei Technologies Co. Limited

- 7.1.5 Cisco Systems Inc.

- 7.1.6 Hewlett Packard Enterprise Company

- 7.1.7 Juniper Networks Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Capgemini Engineering (Capgemini)

- 7.1.10 EdgeIQ (MachineShop Inc.)

- 7.1.11 ADLINK Technology Inc.

- 7.1.12 General Electric Company

- 7.1.13 Amazon Web Services Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球邊緣運算人工智慧市場 - 2025 年至 2032 年

全球邊緣運算人工智慧市場 - 2025 年至 2032 年 邊緣安全市場規模、佔有率及成長分析(按組件、部署模式、組織規模、垂直產業和地區)-2025 年至 2032 年產業預測

邊緣安全市場規模、佔有率及成長分析(按組件、部署模式、組織規模、垂直產業和地區)-2025 年至 2032 年產業預測 邊緣 AI 嵌入式 PC 市場報告:2031 年趨勢、預測與競爭分析邊緣運算市場規模、佔有率及成長分析(按組件、組織規模、應用、最終用戶和地區)-2025 年至 2032 年產業預測

邊緣 AI 嵌入式 PC 市場報告:2031 年趨勢、預測與競爭分析邊緣運算市場規模、佔有率及成長分析(按組件、組織規模、應用、最終用戶和地區)-2025 年至 2032 年產業預測 2025年人工智慧(AI)邊緣運算全球市場報告2025年邊緣人工智慧軟體全球市場報告2025 年超大規模邊緣運算全球市場報告

2025年人工智慧(AI)邊緣運算全球市場報告2025年邊緣人工智慧軟體全球市場報告2025 年超大規模邊緣運算全球市場報告 工業邊緣市場:按組件、應用、軟體部署模式、組織規模、垂直和地區分類的全球市場 - 預測至 2030 年多接取邊緣運算市場規模、佔有率、成長分析,按產品、按公司規模、按網路類型、按最終用途、按地區 - 行業預測,2025 年至 2032 年

工業邊緣市場:按組件、應用、軟體部署模式、組織規模、垂直和地區分類的全球市場 - 預測至 2030 年多接取邊緣運算市場規模、佔有率、成長分析,按產品、按公司規模、按網路類型、按最終用途、按地區 - 行業預測,2025 年至 2032 年 邊緣運算市場(全球)(2025-2029)

邊緣運算市場(全球)(2025-2029)