|

市場調查報告書

商品編碼

1642077

PaaS(支付即服務):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Payment as a Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

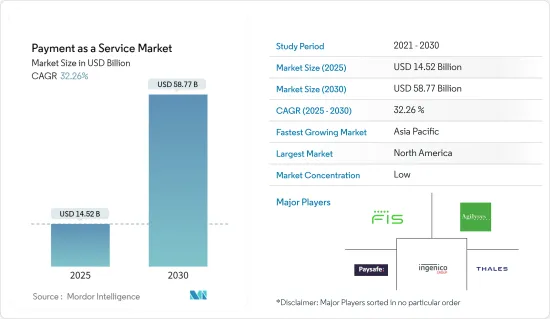

支付即服務 (PaaS) 市場規模預計在 2025 年為 145.2 億美元,預計到 2030 年將達到 587.7 億美元,預測期內(2025-2030 年)的複合年成長率為 32.26%。

在當前情況下,智慧型手機普及率正在上升,刺激了透過行動應用程式銷售商品和服務,從而為客戶提供輕鬆便捷的購物體驗。人們對便利購買商品和服務的需求日益成長,導致了向付款和無現金付款的快速轉變。電子商務業務的不斷成長將進一步推動全球付款服務供應商市場的發展。

主要亮點

- 各國正在採取的促進數位和線上貿易的措施預計將促進商業發展。 Mastercard、Visa 和 Rupay 等全球付款網路的出現也推動了 PaaS 市場的擴張,這些支付網路為客戶提供了無摩擦的付款處理。

- 智慧型手機的日益普及以及對線上服務的需求不斷成長正在推動持續成長。隨著全球對智慧型手機使用的日益重視和網際網路的大規模普及,預計它將保持其在市場上的主導地位。此外,隨著銀行和金融機構提供即時付款服務,越來越多的客戶轉向線上付款管道。因此,市場對網路付款的需求不斷增加。

- 付款產業經歷了重大轉型,舊方法現在只需單擊即可被新模組取代。此外,PaaS(支付即服務)不僅改變零售格局。銀行現在意識到,PaaS 的廣泛採用代表著為客戶提供可靠選擇的機會。因此,對電子商務的日益依賴,尤其是零售業,正在推動 PaaS(支付即服務)市場的發展。

- 缺乏跨境貿易的全球標準可能會抑制市場發展。由於使用者友善的全球付款系統、國際標準和各國政府法規的差異,銀行和企業可能會受到不利影響。這通常需要手動收集和更正資料。

- 由於全球消費者擴大使用和採用線上數位化支付方式,COVID-19 疫情對支付即服務產業產生了重大影響。此外,隨著消費者對市場上的付款技術越來越熟悉,支付即服務 (PaaS) 正在經歷顯著成長。然而,自疫情爆發以來,數位付款的採用率顯著增加,攜帶現金和用現金支付的趨勢有所下降,而這一直是支付即服務 (PaaS) 市場的主要成長要素之一。

PaaS(支付即服務)市場趨勢

零售業預計將做出重大貢獻

- 隨著電子商務產業的快速成長,零售商正迅速採用數位付款技術,為客戶提供更便利的體驗。根據行動付款大會顯示,全球有25億人喜歡在網路購物。到 2025 年,這一數字預計將成長到 40 億。根據英國零售商協會 (BRC) 的數據,簽帳金融卡佔所有交易的 42.6%,而現金佔 42.3%。根據英國金融市場統計,英國77% 的零售支出是透過信用卡支付的。

- 商家擴大採用尖端技術來提高其在市場上的存在感和知名度。例如,全球最大的零售商沃爾瑪最近宣布將開始接受PayPal Cash MasterCards 用於店內購物。該公司希望與付款提供者合作,允許客戶使用PayPal的行動應用程式在沃爾瑪商店提取現金或將錢存入他們的帳戶。

- 此外,許多提供付款服務的公司正在擴大業務,以增加其在市場上的佔有率。例如,全球最廣泛的線上零售商線上付款系統Amazon Pay已向當地零售商推出了「先買後付」功能。亞馬遜已經在其百貨連鎖店 Shoppers Stop 推出了這項付款服務,而該線上零售商擁有 5% 的股份,並正在其雜貨連鎖店 More 安裝必要的基礎設施。

- 數位付款的另一個主要好處是能夠收集客戶資料用於行銷目的。這使得零售商能夠在顧客造訪商店和購買後與顧客建立關係,從而提高顧客獲取率和保留率。

亞太地區是成長最快的地區

- 由於對綜合付款解決方案的需求不斷增加以及付款技術的進步,亞太地區預計將實現顯著成長。此外,該地區智慧型手機普及率和網路普及率的提高也推動了市場的發展。

- 該地區的國家,包括日本、中國、澳洲、韓國和紐西蘭,對經濟成長做出了重大貢獻。例如,亞洲支付網路(APN)由中國、日本、新加坡、馬來西亞、泰國、韓國、紐西蘭、越南、印尼、菲律賓和澳洲等 11 個亞洲國家組成,旨在促進該地區的跨境銀行交易。

- 許多以前依賴現金付款的小型零售商已迅速採用數位付款以保持市場競爭力。例如,印度政府推出驅魔計劃,強制消費者使用電子付款。

- 各付款服務提供者也在亞太地區投資,以挖掘不斷成長的市場並擴大業務。例如,年收入 470 億美元的印度數位付款閘道基礎設施供應商 Infibeam 打算透過積極推廣其旗艦品牌 CCAvenue 來擴大其在數位付款市場的全球影響力。

PaaS(支付即服務)產業概覽

PaaS(支付即服務)市場競爭激烈,且分散,付款服務供應商眾多。市場參與者不斷致力於開發創新產品。供應商越來越注重透過併購來擴大市場佔有率並獲得市場吸引力。

- 2022 年 11 月,主要企業首選的全球金融科技平台 Adyen 宣布,北美領先的雜貨科技公司 Instacart 已選擇該公司作為額外的付款處理合作夥伴。

- 2022年10月,付款接受技術合作夥伴Ingenico與澳洲領先的付款服務供應商之一Live Payments達成長期策略夥伴關係關係,為零售商和計程車提供無縫便捷的付款和商業解決方案。 Ingenico 將為澳洲各地的 LivePayments 推出其 AXIUM 系列 Android 智慧付款。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 智慧型手機的普及和線上服務需求的不斷成長

- 對電子商務平台的依賴日益增加

- 市場限制

- 缺乏全球付款標準

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響

第5章 市場區隔

- 按服務類型

- 商家融資

- 監理合規性

- 安全和防詐欺

- 付款應用程式和閘道器

- 其他服務

- 按最終用戶產業

- 零售與電子商務

- BFSI

- 飯店業

- 媒體與娛樂

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 澳洲

- 其他亞太地區

- 拉丁美洲

- 墨西哥

- 巴西

- 其他拉丁美洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 北美洲

第6章 競爭格局

- 公司簡介

- FIS

- Thales Group

- Ingenico Group

- Agilysys Inc.

- Paysafe Holdings UK Limited

- Total System Services Inc.

- Mastercard

- PayPal Holdings Inc.

- Verifone

- Pineapple Payments

第7章投資分析

第8章 市場機會與未來趨勢

The Payment as a Service Market size is estimated at USD 14.52 billion in 2025, and is expected to reach USD 58.77 billion by 2030, at a CAGR of 32.26% during the forecast period (2025-2030).

In the current scenario, the increasing smartphone penetration is proliferating the growth of the sale of goods and services extensively through mobile apps to assist customers by providing an easy and convenient shopping experience. The rise in demand for easy and convenient purchases of goods and services resulted in a radical shift toward digital and cashless payments. The increase in e-commerce business further boosts the global payment service provider market.

Key Highlights

- The business is anticipated to increase due to efforts being made in numerous nations to promote digital and online transactions. The expansion of the PaaS market is also expected to be aided by the advent of payment networks like Mastercard, Visa, and Rupay on a global scale for the processing of smooth payments for clients.

- The increased demand for smartphone penetration and the incorporation of online services is experiencing continuous growth. It is expected to maintain its dominance in the market with an increase in emphasis on smartphone usage and massive internet penetration across the world. In addition, customers are using online payment channels more frequently as banks and financial institutions provide real-time payment services. Therefore, demand for online payments is experiencing a continuous rise in the market.

- The payment industry has experienced a significant transformation, and the old methods are replaced with new modules with a single click. Moreover, payment as a service (PaaS) is not only changing the scene for retailers. Banks are now realizing that the rise in PaaS use is an opportunity to give their clients a reliable choice. Thus, the increasing dependence on e-commerce, especially in retail, drives the payment as a service market.

- The absence of a global standard for cross-border transactions could restrain the market. Due to the lack of a worldwide payment system that is simple to use, international standards, and differing government rules in different countries, banks and businesses may be negatively impacted. This frequently necessitates manual intervention to gather and correct data.

- The COVID-19 pandemic has significantly impacted the payment as a service industry, owing to the increased usage and adoption of online and digitalized payment methods among consumers globally. Additionally, payment as a service is experiencing massive growth as consumers become familiar with the payment technology in the market. However, post-pandemic, there was a significant rise in the adoption of digital payments, reducing the trend of carrying and paying through cash which, in turn, has become one of the primary growth factors for the payment as a service market.

Payment as a Service (PAAS) Market Trends

Retail Sector Expected to be a Significant Contributor

- Retailers are rapidly adopting digital payment technology to bring more convenient experiences to their customers, owing to the massive growth in the e-commerce industry. According to the Mobile Payments Conference, 2.5 billion people worldwide prefer online shopping. By 2025, the number will grow to 4 billion digital buyers. According to the British Retail Consortium (BRC), debit cards account for 42.6% of all transactions, whereas cash is 42.3%. According to UK Finance, 77% of all UK retail spending was made by cards.

- Merchants are increasingly implementing cutting-edge technologies to boost their presence and visibility in the market. For instance, the biggest retailer in the world, Walmart, recently said that PayPal Cash Mastercard would be accepted for in-store purchases. The merchant wants to incorporate the payment provider's service so that customers can use the PayPal mobile app to withdraw cash and top up their accounts at Walmart locations.

- In addition, many companies that offer payment services are growing their operations to boost their market presence. For instance, the world's most extensive online retailer's online payment system, Amazon Pay, rolled out "buy now pay later" capabilities to local retailers. Amazon has already introduced the payments service in the department store chain Shoppers Stop, in which the online retailer owns a 5% stake and sets up the necessary infrastructure at the grocery chain More.

- Another significant benefit of digital payment is the ability to collect customer data for marketing purposes. This enables retailers to build customer relationships after their visit or purchase and further work toward customer acquisition and retention.

Asia-Pacific to be the Fastest Growing Region

- The Asia-Pacific region is expected to depict substantial growth owing to the increased demand for integrated payment solutions and advancements in payment technologies in the region. Furthermore, the rise in the penetration of smartphones and internet penetration in the region is propelling the market.

- Countries in the region, such as Japan, China, Australia, South Korea, and New Zealand, contribute significantly toward the growth. For instance, the Asian Payments Network (APN) is a group of 11 Asian countries that include China, Japan, Singapore, Malaysia, Thailand, South Korea, New Zealand, Vietnam, Indonesia, Philippines, and Australia to promote cross-border banking transactions in the region.

- Many small retailers earlier relied more on cash but rapidly deployed digital payments to remain competitive in the market. For instance, as the Indian government launched a demonetization program, consumers were forced to use electronic payments.

- Various payment service providers also invest in the Asia-Pacific region to expand their businesses by tapping the growing market. For instance, the firm Infibeam intends to expand its global presence in the digital payments market by aggressively promoting its flagship brand CCAvenue, a provider of digital payment gateway infrastructure in India with an annual run-rate of USD 47 billion.

Payment as a Service (PAAS) Industry Overview

The payment as a service market is highly competitive and fragmented, owing to the presence of many payment service providers. The market players are consistently focusing on developing innovative products. The vendors increasingly focus on mergers and acquisitions to increase market share and gain market traction.

- In November 2022, Adyen, the global financial technology platform of choice for leading businesses, announced that Instacart, the leading grocery technology company in North America, has selected the company as an additional payments processing partner.

- In October 2022, Ingenico, the technological partner in payments acceptance, and Live Payments, one of Australia's leading payment service providers, entered a long-term strategic partnership to equip retailers and taxis with seamless, convenient payment and commerce solutions. Ingenico will roll out its AXIUM range of Android Smart POS for Live Payments across Australia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Demand for Smartphone Penetration and Incorporation of Online Services

- 4.2.2 Increase Dependence on E-Commerce Platform

- 4.3 Market Restraints

- 4.3.1 Absence of Global Standards for Payments

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Force Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Types of Services

- 5.1.1 Merchant Financing

- 5.1.2 Regulatory Compliance

- 5.1.3 Security and Fraud Protection

- 5.1.4 Payment Applications and Gateways

- 5.1.5 Other Services

- 5.2 By End-user Industry

- 5.2.1 Retail and E-commerce

- 5.2.2 BFSI

- 5.2.3 Hospitality

- 5.2.4 Media and Entertainment

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 South Korea

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 FIS

- 6.1.2 Thales Group

- 6.1.3 Ingenico Group

- 6.1.4 Agilysys Inc.

- 6.1.5 Paysafe Holdings UK Limited

- 6.1.6 Total System Services Inc.

- 6.1.7 Mastercard

- 6.1.8 PayPal Holdings Inc.

- 6.1.9 Verifone

- 6.1.10 Pineapple Payments