|

市場調查報告書

商品編碼

1642156

全Flash陣列:市場佔有率分析、產業趨勢與成長預測(2025-2030)All Flash Array - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

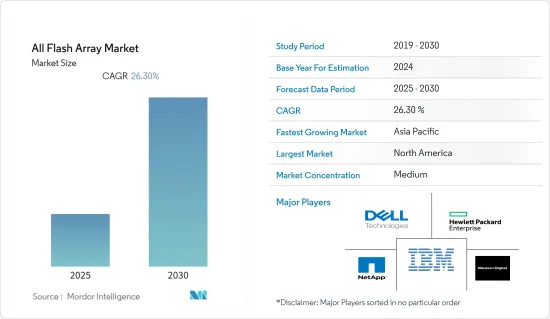

預計預測期內全Flash陣列市場複合年成長率將達到 26.3%。

主要亮點

- 企業產生的資料的增加,加上雲端技術的日益普及,預計將推動市場的發展。此外,巨量資料和分析推動了資料存取和處理模式,需要更高的儲存效能和更高的並發性(巨量資料加劇了資料移動性問題)。

- 快閃記憶體的採用主要受到其功耗、效能提升和易於維護等效用的推動,這些優勢推動了其採用率。此外,包括即時分析和要求苛刻的資料庫系統在內的關鍵任務應用程式可以透過快閃記憶體儲存系統輕鬆實現。

- SCM 可能會部署為全Flash陣列的快取層。這些新進展可望最佳化工作負載效能,同時降低儲存成本。

- 此外,非揮發性記憶體規範 (NVMe) 等改進實現了比傳統通訊協定更快的效能和更高的密度,從而擴展了企業全快閃儲存產業。

- 預計到 2022 年,印度等地區將見證醫療保健、保險和通訊垂直領域的企業快閃記憶體儲存的積極成長。印度的成長將主要受到物聯網、人工智慧和巨量資料創新的推動。各組織正在尋求自動化技術和基於消費的定價。

全Flash陣列(AFA) 市場趨勢

資料中心預計將佔很大佔有率

- 不斷成長的資料中心工作負載產生了新的儲存效能要求,而硬碟 (HDD) 無法輕易滿足此要求。使用快閃記憶體作為持久性儲存技術解決了這些挑戰。

- 據NASSCOM稱,到2025年印度資料中心市場的投資預計將達到46億美元。主要原因是印度網際網路使用量不斷成長、雲端運算需求不斷增加、政府數位化努力以及數位服務供應商的在地化。與更成熟的市場相比,在印度開發和營運的成本效益是我們最大的優勢。

- 此外,根據 CloudScene 的數據,截至 2021 年,全球約有 8,000 個資料中心,可提供 110 個國家的資訊。其中六個國家佔據資料中心的大部分:美國(佔總數的33%)、英國(5.7%)、德國(5.5%)、中國(5.2%)、加拿大(3.3%)和荷蘭(3.4%)。

- 根據WSTS預測,2021年記憶體元件銷售收入將達到約1,538億美元,較2020年的1,175億美元成長約31%。

北美預計將佔據主要市場佔有率

- 多種產品的供應顯示北美佔有較大的市場佔有率。此外,美國也是該市場其他知名參與者的總部,例如戴爾公司、IBM 公司和 Net App 公司。受巨量資料和相關應用支出增加的推動,全Flash陣列的採用正在推動該地區的成長。

- 由於資料中心數量最多且醫療保健、IT、BFSI、零售和媒體行業快速成長,該地區佔據全Flash陣列市場的大部分佔有率。據Cloudscene稱,美國和加拿大擁有全球最多的資料中心,共3,029個,預計將推動全Flash陣列的需求。

- 由於擁有著名的資訊科技產業和主要供應商,北美正在大力投資IT基礎設施。該地區的 BFSI 產業蓬勃發展,各組織願意投資IT基礎設施來滿足客戶需求。

- 該地區還佔全球雲端解決方案支出的最大佔有率。據經濟戰略研究所(ESI)稱,美國經濟將受益於企業在雲端服務(雲端處理、資料分析和物聯網)方面的支出。到2025年,預計將產生1.7兆美元的新支出,為GDP增加3兆美元,並為美國經濟創造800萬個就業機會。

全Flash陣列(AFA) 產業概覽

全Flash陣列市場競爭激烈,有許多地區和全球參與者。產品創新正在推動市場發展,供應商也正在投資技術創新。主要參與者包括戴爾科技、西部資料公司、惠普企業、NetApp Inc. 和 IBM 公司。

- 2022 年 2 月—IBM 宣布推出 IBM FlashSystem Cyber Vault,以協助偵測勒索軟體和其他網路攻擊並快速復原。此外,IBM 也宣布推出基於 IBM Spectrum Virtualize 的全新 FlashSystem 儲存模型,提供單一、一致的營運環境,旨在提高混合雲環境中的網路彈性和應用程式效能。

- 2022 年 3 月 - NetApp 和 Cisco 宣布推出 FlexPod XCS,從而實現 FlexPod 的演進,為現代應用程式、資料和混合雲端服務提供一個自動化平台。 FlexPod 採用經過 Cisco 和 NetApp 預先檢驗的儲存、網路和伺服器技術建置。此外,新的 FlexPod XCS 平台旨在加速混合雲環境中現代應用程式和資料的交付。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 調查前提

第2章調查方法

第3章執行摘要

第4章 市場動態

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 選擇全Flash陣列的先決條件/注意事項

- 評估新冠肺炎對市場的影響

第5章 市場動態

- 市場促進因素

- 資料中心數量不斷增加

- 易於管理和維護

- 市場限制

- 初始成本

- 寫入周期緩慢

第6章 市場細分

- 按類型

- 傳統的

- 自訂

- 按最終用戶應用

- 資訊科技和通訊業

- BFSI

- 衛生保健

- 政府

- 其他最終用戶應用程式

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 其他亞太地區

- 世界其他地區

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- Silk Platform

- Dell Inc.

- Hewlett Packard Enterprise Development LP

- NetApp Inc.

- Violin Systems LLC

- IBM Corporation

- Fujitsu Ltd.

- Pure Storage, Inc.

- Western Digital Corporation

- Huawei Technologies Co., Ltd.

第8章投資分析

第9章:市場的未來

簡介目錄

Product Code: 66997

The All Flash Array Market is expected to register a CAGR of 26.3% during the forecast period.

Key Highlights

- The gain in data generated by the enterprise, coupled with the increasing adoption of cloud technology, is anticipated to drive the market. Moreover, with big data and analytics, data access and processing patterns demand a higher storage performance and improved concurrency (Big Data aggravates the data mobility issues).

- Flash storage adoption mainly depends on its usefulness, such as power consumption, improving performance, and ease of maintenance, which have raised the adoption rate. Moreover, mission-critical applications, including real-time analytics and demanding database systems, can be achieved easily with flash storage systems.

- SCMs will likely be deployed as a caching layer for an all-flash array. These new evolutions are expected to provide optimized workload performance while decreasing storage costs.

- Furthermore, improvements such as Non-Volatile Memory Express (NVMe) have increased the enterprise all-flash storage industry, allowing faster performance and more density than conventional protocols.

- Territories like India anticipate positive growth for enterprise flash storage from healthcare, insurance, and telecommunications verticals across 2022. India's growth is primarily due to IoT, AI, and big data innovation. Organizations are looking ahead to automation technologies and consumption-based pricing.

All-flash Array (AFA) Market Trends

Data centers is Expected to Hold Significant Share

- Growing data center workloads create new storage performance requirements that are very difficult to address with hard disk drives (HDDs). Using flash as a persistent storage technology resolves these challenges.

- According to NASSCOM, India's data center market investment is expected to reach USD 4.6 billion by 2025, mainly due to India's growing internet usage, increased cloud computing demands, digitalization initiatives by the government, and localization by digital service providers. India's higher cost efficiency in development and operation is its biggest advantage compared to more mature markets.

- Moreover, as per CloudScene, with 110 countries' available information, as of 2021, there were around 8,000 data centers globally. Among these, six countries hold a majority of data centers: the United States (33% of total), the UK (5.7%), Germany (5.5%), China (5.2%), Canada (3.3%), and the Netherlands (3.4%).

- According to WSTS, in 2021, revenue from memory component sales was about USD 153.8 billion, an increase from the USD 117.5 billion in revenue recorded in 2020, which shows an approximately 31% increase in revenue.

North America is Expected to Hold Major Market Share

- Multiple product launches suggest that North America holds a significant market share. Moreover, the United States acts as headquarters for other prominent players in the market, such as Dell Inc., IBM Corporation, Net App Inc., etc. Adopting the all-flash array enhances the growth of this region, fueled by increased expenditures in big data and related applications.

- The region holds a significant share of the all-flash array market due to the presence of the highest number of data centers and booming healthcare, information technology, BFSI, retail, and media industries. According to Cloudscene, the number of data centers in the US and Canada is 3029, the highest in the world, and expected to drive the demand for the all-flash array market.

- North America spends a significant amount on IT infrastructure, owing to the presence of prominent information technology industry and key vendors' companies. The region is home to a thriving BFSI industry where organizations are ready to spend on IT infrastructure to cater to the needs of their customers.

- The region also accounts for significant global spending on cloud solutions. According to Economic Strategy Institute (ESI), the US economy will benefit from corporation spending on cloud services (cloud computing, data analysis, and the Internet of Things). It is expected to contribute USD 1.7 trillion in new spending, add USD 3 trillion to GDP, and create 8 million jobs for the US economy by 2025.

All-flash Array (AFA) Industry Overview

The All Flash Array Market is moderately competitive, with many regional and global players. Innovation drives the market in product offerings, and each vendor invests in innovation. Key players include Dell Technologies, Western Digital Corporation, Hewlett Packard Enterprise, NetApp Inc., and IBM Corporation.

- February 2022 - IBM introduced IBM FlashSystem Cyber Vault to support companies in better detecting and recovering quickly from ransomware and other cyberattacks. In addition, the company also revealed new FlashSystem storage models, based on IBM Spectrum Virtualize, to deliver a single and consistent operating environment designed to improve cyber resilience and application performance within a hybrid cloud environment.

- March 2022 - NetApp and Cisco announced the evolution of FlexPod with the introduction of FlexPod XCS, providing one automated platform for modern applications, data, and hybrid cloud services. FlexPod comprises pre-validated storage, networking, and server technologies from Cisco and NetApp. Moreover, the new FlexPod XCS platform is designed to accelerate the delivery of modern applications and data in a hybrid cloud environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Industry Attractiveness - Porter's Five Force Analysis

- 4.1.1 Bargaining Power of Suppliers

- 4.1.2 Bargaining Power of Consumers

- 4.1.3 Threat of New Entrants

- 4.1.4 Intensity of Competitive Rivalry

- 4.1.5 Threat of Substitute Products

- 4.2 Pre-requisites/Consideration for choosing All-Flash Array

- 4.3 Assessment of covid -19 impact on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Data Centers

- 5.1.2 Ease of Management and Maintenance

- 5.2 Market Restraints

- 5.2.1 Initial Cost Involved

- 5.2.2 Lower Write Cycles

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Traditional

- 6.1.2 Custom

- 6.2 By End-User Application

- 6.2.1 IT and Telecom Industry

- 6.2.2 BFSI

- 6.2.3 Healthcare

- 6.2.4 Government

- 6.2.5 Other End-User Applications

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 South Korea

- 6.3.3.4 India

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.4.1 Latin America

- 6.3.4.2 Middle-East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Silk Platform

- 7.1.2 Dell Inc.

- 7.1.3 Hewlett Packard Enterprise Development LP

- 7.1.4 NetApp Inc.

- 7.1.5 Violin Systems LLC

- 7.1.6 IBM Corporation

- 7.1.7 Fujitsu Ltd.

- 7.1.8 Pure Storage, Inc.

- 7.1.9 Western Digital Corporation

- 7.1.10 Huawei Technologies Co., Ltd.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

全Flash陣列市場報告:2031 年趨勢、預測與競爭分析

全Flash陣列市場報告:2031 年趨勢、預測與競爭分析 全球全快閃陣列 (AFA) 市場規模(按快閃媒體、儲存架構、最終用戶產業、地區、範圍和預測)

全球全快閃陣列 (AFA) 市場規模(按快閃媒體、儲存架構、最終用戶產業、地區、範圍和預測) 全Flash陣列市場:按儲存架構、快閃記憶體媒體和最終用戶分類 - 2025-2030 年全球預測

全Flash陣列市場:按儲存架構、快閃記憶體媒體和最終用戶分類 - 2025-2030 年全球預測 基於快閃記憶體的陣列市場:按產品類型、儲存容量、組織規模和最終用戶 - 2025-2030 年全球預測

基於快閃記憶體的陣列市場:按產品類型、儲存容量、組織規模和最終用戶 - 2025-2030 年全球預測 全快閃陣列市場- 全球產業規模、佔有率、趨勢、機會和預測,按類型(傳統和客製化)、最終用戶(IT 和電信業、BFSI、醫療保健、政府)、按地區、按競爭細分,2019年-2029F

全快閃陣列市場- 全球產業規模、佔有率、趨勢、機會和預測,按類型(傳統和客製化)、最終用戶(IT 和電信業、BFSI、醫療保健、政府)、按地區、按競爭細分,2019年-2029F 基於快閃記憶體的陣列市場:按產品類型、按公司類型、按儲存容量、按最終用途行業、按地區

基於快閃記憶體的陣列市場:按產品類型、按公司類型、按儲存容量、按最終用途行業、按地區 全Flash陣列的全球市場 2023-2027

全Flash陣列的全球市場 2023-2027