|

市場調查報告書

商品編碼

1643009

生物分解性地膜:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Biodegradable Mulch Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

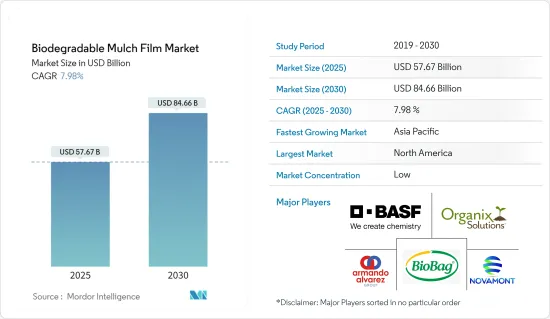

生物分解性地膜市場規模預計在 2025 年為 576.7 億美元,預計到 2030 年將達到 846.6 億美元,預測期內(2025-2030 年)的複合年成長率為 7.98%。

關鍵亮點

- 土壤中的生物分解性對於農業和園藝產品來說是一個主要優點。生物分解性分解地膜的可用性得到了快速提升,農民可以在田地中使用後將生質塑膠地膜收集起來並犁入土中,而無需進行回收,從而提高了工作效率。然而,使用生物分解性覆蓋物對環境的潛在影響尚未得到徹底研究,用於檢驗其安全性的國際標準(如 ISO 17088、ASTM D6400、ISO 17556 和 ASTM D5988)目前正在研究中。

- 如果處理不當,非生物分解的地膜會導致農業表土流失,估計每年每個作物週期結束時,約有 166 千噸地膜從田地流失。相較之下,經土壤生物分解性認證的地膜由於其生物分解性,不僅可以防止土壤流失,而且在阻止農業土壤中微塑膠的徑流和積累方面發揮著至關重要的作用。此外,這些經過認證的地膜有助於減少難以回收的塑膠廢棄物的產生。

- 溫室業務的擴張將推動市場發展。根據世界溫室蔬菜統計數據,全世界有溫室種植面積1228,000英畝。生物分解性塑膠覆蓋物碎片在完全生物分解之前會以物理方式改良土壤。但PE塑膠碎片會降低土壤的滲透性和吸水性,其累積會影響溫室栽培土壤生態系統,最終影響植物的發芽和生長。因此,該領域對生物分解性地膜市場的需求正在增加。

- 政府對有機覆蓋物的支持性法規正在推動市場的發展。例如,在歐洲,EN17033是針對農業和園藝使用的生物分解性地膜的新產品標準,規定了必要的要求和測試方法。該標準旨在為農民、經銷商和相關人員提供明確的參考。 EN 17033 很可能取代歐洲其他現有的國家標準。

- 製造過程中添加的有害添加劑以及高昂的安裝成本對市場成長構成了挑戰。由於地膜的初始成本高,無法取得,對成長構成了挑戰。此外,隨著農民意識的增強,在生物分解性地膜生產中使用塑化劑來提高利潤正成為市場挑戰。

生物分解性地膜市場趨勢

水果和蔬菜佔很大佔有率

- 無論是黑色還是透明的地膜在現代農業中都扮演著重要角色。這些孔使種植或直接播種作物變得更加容易,並增強了對作物生長至關重要的幾個因素。此方法不僅提高了各類蔬菜的栽培效率,而且可以提早收穫、增加產量,並改善農產品的品質。

- 此外,該薄膜還能顯著減少土壤水分流失,保持地面濕潤,減少額外澆水的需要,從而節省成本。實地試驗表明,與傳統方法相比,使用農膜可使蔬菜產量提高近一倍。

- 黑白地膜具有雙重用途。它不僅可以防止雜草生長,還可以阻斷相關植物的生長。此外,這些薄膜還可以作為防雨屏障,防止有價值的農藥和肥料被沖走。它還有助於保持土壤濕度,防止土壤壓實,保持土壤疏鬆,適合植物生長。

- 由於用於水果和蔬菜的地膜比例很高,而且其處理會產生許多環境問題,因此生物分解性地膜被認為是替代傳統聚乙烯地膜的最佳解決方案。

- 此外,傳統地膜廢棄物受到土壤和蔬菜殘留物的嚴重污染,回收過程成本高、耗時且不經濟,造成了環境問題。這種生物分解性的地膜具有以下優點:在其使用壽命結束後,可以簡單地將其處理到土壤中或堆肥系統中,由土壤微生物進行生物分解。這可以節省您的時間和金錢。

- BASF的聚合物 Ecovio M 由聚乳酸 (PLA) 製成,是一種生物基材料,可完全生物分解。這樣做的好處是,農民收成後不用費力去除地膜,可以直接耕地,節省時間和金錢。

- 此外,義大利每年也向其他國家出口大量新鮮水果和蔬菜,Novamon 等公司提供用於蔬菜加工的 Mater-Bi 地膜。義大利是歐洲領先的番茄生產國。據義大利國家食品蔬菜工業保護協會稱,2023 年義大利番茄產品出口額與前一年同期比較成長了 25.2%。

亞太地區將經歷顯著的市場成長

- 預計亞太地區生物分解性地膜的成長率最高。這是由於人口不斷成長,特別是中國和印度的人口,導致糧食需求增加,從而導致作物生產中生物分解性地膜的使用增加。

- 政府也正在採取必要措施提高農業生產力。在中國,國家發展和改革委員會表示希望在農業領域推廣包括生物分解性地膜在內的非塑膠產品。

- 此外,印度政府預計未來幾年將增加豆類產量,預計將大幅增加對生物分解性地膜的需求。根據 PIB 預測,2021-2022 年豆類種植面積將達到 2,730.2 萬噸,預計 2022-2023 年將增加 2,750.4 萬噸。

- 此外,2023 年 5 月,新加坡 RWDC Industries 與生物技術新興企業和工藝技術提供商 Lummus Technology 簽署了一份合作備忘錄,該公司開創了生物聚合物解決方案來取代石油基塑膠。此次合作旨在引領全球措施,推廣使用生物分解性的聚合物 PHA。

生物分解性地膜產業概況

生物分解性地膜市場細分化,主要參與者採用新產品推出和協議等各種策略來擴大其在該市場的佔有率。主要參與企業包括BASF SE 和 BioBag International AS。

- 2023 年 10 月,包裝和紙張製造商 Mondi 與領先的農業繩、網和繩索製造商 Cotesi 合作,發起了一項聯合計劃,以加強農業部門的永續性。兩家公司合作的核心是推出一種新的紙基解決方案「Advantage Kraft Mulch」。這種創新產品旨在取代長期以來一直是農民主要食物的傳統塑膠地膜。地膜在農業中發揮著至關重要的作用,可以保護農作物免受鳥類、雜草、土壤侵蝕、過度陽光和暴雨等各種威脅。傳統上,這些薄膜由塑膠製成,在種植時鋪設,在收穫時丟棄。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 擴大溫室業務

- 世界各地政府對有機覆蓋物的支持與監管

- 市場限制

- 安裝成本高,生產過程中添加有害添加劑

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 按聚合物

- 澱粉

- 聚羥基烷酯(PHA)

- 聚乳酸(PLA)

- 其他聚合物(脂肪族-芳香族共聚物 (AAC))

- 按應用

- 水果和蔬菜

- 花朵

- 穀物和油籽

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 歐洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 其他亞太地區

- 其他

- 北美洲

第6章 競爭格局

- 公司簡介

- BASF SE

- BioBag International AS

- Organix AG

- Armando Alvarez Group

- Novamont SpA

- Agriplast Tech India Pvt. Ltd

- Pooja Plastic Industries

- Barbier Group

- Dubois Agrinovation

- Hopewell Industries

- Investment Analysis

第7章 市場機會與未來趨勢

簡介目錄

Product Code: 69049

The Biodegradable Mulch Film Market size is estimated at USD 57.67 billion in 2025, and is expected to reach USD 84.66 billion by 2030, at a CAGR of 7.98% during the forecast period (2025-2030).

Key Highlights

- Biodegradability in the soil provides huge benefits for agricultural and horticultural products. Biodegradable mulching films have made rapid improvements in terms of usability, allowing cultivators to plow in bioplastic mulch after use instead of collecting them from the field for recycling, which improves operational efficiency. However, the potential environmental consequences of using biodegradable mulches have not been thoroughly studied, and international standards, such as ISO 17088, ASTM D6400, ISO 17556, and ASTM D5988, for validating their safeness are in the ongoing research phase.

- Non-biodegradable mulch films, when not properly disposed of, can lead to the loss of agricultural topsoil, with an estimated 166 kiloton/year dragged away from fields at the end of each crop cycle. In contrast, certified soil-biodegradable mulch films, with their biodegradability, not only prevent this soil loss but also play a crucial role in halting the leakage and accumulation of microplastics in agricultural soils. Additionally, these certified mulch films help curb the production of plastic waste that is notoriously challenging to recycle.

- The expansion of the greenhouse project drives the market. According to the World Greenhouse Vegetable Statistics, there are 1,228,000 acres of greenhouse growing space for production worldwide. Biodegradable plastic mulch fragments physically modify soil before they are fully biodegraded. However, PE plastic fragments reduce soil infiltration and water absorption, by which the accumulation may affect soil ecosystems in greenhouse plantations and, ultimately, result in plant germination and growth. Thus, the demand for biodegradable mulch film market increases in this segment.

- Supportive regulation from the governments for organic mulching across the world is driving the market. For instance, in Europe, EN 17033 is the new product standard made for biodegradable mulch films used in agriculture and horticulture and specifies the necessary requirements and test methods. The standard is designed for a clear reference to farmers, distributors, and stakeholders. EN 17033 is more likely to replace other pre-existing national standards in Europe.

- High installation cost, along with the addition of harmful additives during the manufacturing process, challenges the growth of the market. The deficit in the availability of such mulch films with high initial costs is challenging the growth. Moreover, the involvement of plasticizers in the manufacturing of biodegradable mulch film to make profits may challenge the market with growing awareness among the farmers.

Biodegradable Mulch Film Market Trends

Fruits and Vegetables to Account for a Significant Share

- Mulch films, whether black or transparent, play a crucial role in modern agriculture. They facilitate the planting or direct sowing of crops through punched holes, enhancing several factors pivotal for crop growth. This method not only boosts the effectiveness of growing various vegetables but also leads to earlier harvests, increased yields, and improved produce quality.

- Moreover, these films significantly reduce moisture loss from the soil, keeping the ground moist and subsequently cutting down on the need for additional watering, thus reducing costs. Field trials have demonstrated that using agricultural films can nearly double vegetable harvests compared to traditional methods.

- Black and black/white mulch films serve a dual purpose. They not only prevent weed growth but also shield against accompanying flora. Additionally, these films act as a protective barrier against rain, safeguarding valuable agrochemicals and fertilizers from being washed away. By maintaining soil moisture, they also prevent soil compaction, ensuring it stays loose and conducive for plant growth.

- Due to the large proportion of mulch films used in fruits and vegetables and all the environmental problems related to their disposal, biodegradable mulch films seem to be the best solution for replacing conventional polyethylene mulches.

- Additionally, traditional mulch film waste causes an environmental problem because it is very contaminated with soil and vegetable residues, making the recycling process expensive, time-consuming, and an uneconomic activity. These biodegradable mulch films have the advantage of being disposed directly into the soil or into a composting system at the end of their lifetime and undergo biodegradation by soil microorganisms. This saves time and money.

- BASF offers the polymer Ecovio M, which is made up of polymer PLA (polylactic acid), which has biobased content and is completely biodegradable. Its advantage is that the farmer does not have to laboriously collect the mulch films after harvest but can plow them directly, which helps save time and money.

- Furthermore, Italy exports tons of fresh fruits and vegetables to other countries annually, and players such as Novamont offer Mater-Bi mulch film for processing vegetables. Italy is the main European producer of tomatoes. According to the Associazione Nazionale Industriali Conserve Alimentari Vegetali, the export value of tomato products in Italy rose by 25.2% in 2023 compared to the previous year.

Asia-Pacific to Witness Significant Market Growth

- Asia-Pacific is projected to register the highest rate in biodegradable mulch film, as the increasing population, especially in China and India, is increasing the demand for food, increasing the usage of biodegradable mulch films in crop production.

- The government is also taking necessary steps to improve the productivity of crops. In China, the government's National Development and Reform Commission stated that China wants to promote non-plastic products, including biodegradable mulch film, in the agriculture sector.

- Additionally, in India, the government estimates an increase in pulse production for the coming years, which is expected to significantly raise the demand for biodegradable mulch films. According to PIB, 273.02 lakh tonnes of pulses were expected to be farmed during 2021-2022, with an increment of 275.04 lakh tonnes compared to 2022-2023.

- Furthermore, in May 2023, Singapore's RWDC Industries, a biotech start-up pioneering biopolymer solutions as alternatives to petroleum-based plastics, and Lummus Technology, a provider in process technology, inked a memorandum of understanding (MOU). This collaboration aims to spearhead worldwide initiatives for deploying PHA, a biodegradable polymer.

Biodegradable Mulch Film Industry Overview

The biodegradable mulch film market is fragmented, and the major players are using various strategies, such as new product launches and agreements, to increase their footprints in this market. Key players in the market are BASF SE, BioBag International AS, etc.

- October 2023: Packaging and paper provider Mondi teamed up with Cotesi, a prominent producer of twine, nets, and ropes for agriculture, in a joint effort to bolster sustainability in the agricultural sector. Their collaboration centers around the launch of a new paper-based solution, Advantage Kraft Mulch. This innovative product is designed to supplant the conventional plastic mulch films that have long been a staple for farmers. Mulch films play a crucial role in agriculture, shielding crops from a gamut of threats, including birds, weeds, soil erosion, excessive sunlight, and heavy rain. Traditionally, these films were crafted from plastic, laid out during planting, and subsequently discarded at harvest, exacerbating the prevalent plastic waste dilemma.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Greenhouse Projects

- 4.2.2 Supportive Regulation from the Governments for Organic Mulching Across the World

- 4.3 Market Restraints

- 4.3.1 High Installation Cost and Addition of Harmful Additives in Manufacturing

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Polymer

- 5.1.1 Starch

- 5.1.2 Polyhydroxyalkanoates (PHA)

- 5.1.3 Polylactic Acid (PLA)

- 5.1.4 Other Polymers (Aliphatic-Aromatic Copolymers (AAC))

- 5.2 By Application

- 5.2.1 Fruits and Vegetables

- 5.2.2 Flowers and Plants

- 5.2.3 Grains and Oilseeds

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BASF SE

- 6.1.2 BioBag International AS

- 6.1.3 Organix AG

- 6.1.4 Armando Alvarez Group

- 6.1.5 Novamont SpA

- 6.1.6 Agriplast Tech India Pvt. Ltd

- 6.1.7 Pooja Plastic Industries

- 6.1.8 Barbier Group

- 6.1.9 Dubois Agrinovation

- 6.1.10 Hopewell Industries

- 6.2 Investment Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

生物分解性地膜市場規模、佔有率和趨勢分析報告:按原料、作物、地區和細分市場預測,2025-2030 年

生物分解性地膜市場規模、佔有率和趨勢分析報告:按原料、作物、地區和細分市場預測,2025-2030 年 生物分解性地膜市場:按原料、作物類型和應用分類 - 全球預測 2025-2030

生物分解性地膜市場:按原料、作物類型和應用分類 - 全球預測 2025-2030 全球可生物分解地膜市場規模研究,按原料、作物類型、應用和區域預測 2022-2032

全球可生物分解地膜市場規模研究,按原料、作物類型、應用和區域預測 2022-2032 全球生物分解地膜市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球生物分解地膜市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 可生物分解地膜市場,依材料類型、作物類型、厚度、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

可生物分解地膜市場,依材料類型、作物類型、厚度、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 到 2030 年生物分解性地膜市場預測:按作物類型、材料、厚度、應用、最終用戶和地區進行的全球分析

到 2030 年生物分解性地膜市場預測:按作物類型、材料、厚度、應用、最終用戶和地區進行的全球分析