|

市場調查報告書

商品編碼

1643017

無線連接:市場佔有率分析、行業趨勢和統計、成長預測 2025-2030Wireless Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

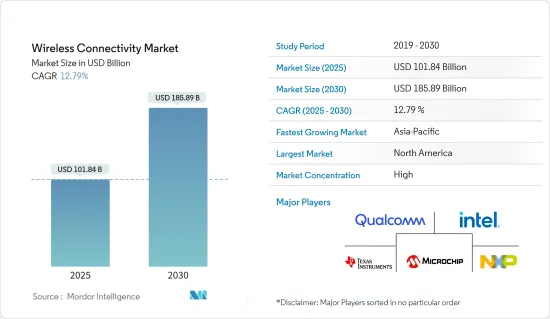

無線連接市場規模預計在 2025 年達到 1,018.4 億美元,預計到 2030 年將達到 1,858.9 億美元,預測期內(2025-2030 年)的複合年成長率為 12.79%。

主要亮點

- 無線連接市場正在經歷顯著成長,原因是對互聯設備的需求不斷成長,這些設備涵蓋 Wi-Fi、藍牙和 Zigbee 等一系列技術,可實現無縫網際網路訪問和資料傳輸,而無需電纜。

- 醫療保健和智慧家庭等各個領域的連網型設備的激增,推動了對藍牙和 Zigbee 等低功耗、短距離連接解決方案的需求。例如,亞馬遜的智慧揚聲器 Echo 使用 Wi-Fi 和藍牙技術來增強連接性。此外,消費者對智慧恆溫器、照明和安全系統等智慧家庭設備的興趣日益濃厚,推動了對無線連接的需求。

- 對家用電子電器的不斷成長的需求正在推動市場成長。人工智慧、物聯網、擴增實境和虛擬實境等先進技術的採用也加速了各個工業領域對無線連接的需求。全球智慧基礎設施的發展也是推動無線連線需求增加的主要因素。

- 此外,全球各國政府對使用無線連接進行各種應用的智慧城市計劃的投資不斷增加,也推動了市場的成長。例如,2023 年 10 月,資訊科技與電子通訊部 (DITE&C) 宣布計劃在全州建立和營運 100 多個 Wi-Fi 熱點,以提供免費且無縫的網路服務。熱點將設立在政府辦公室、公車站、公共公園和市民服務中心等人潮眾多的地方。

- 然而,由於無線網路容易受到網路攻擊,安全問題正在限制無線連線市場的成長。隨著無線通訊在各個行業和應用領域的不斷成長,強大的安全措施對於防止資料外洩和惡意軟體攻擊至關重要。不良的加密通訊協定、薄弱的身份驗證機制和薄弱的網路配置可能會洩漏敏感資訊並危害無線系統的安全。

- 例如,根據無線寬頻聯盟(WBA)在其《2023 年 WBA 年度產業報告》中進行的一項調查,超過三分之一(33%)的服務供應商、技術供應商和企業已經計劃在 2023年終前部署 Wi-Fi 7。此外,44% 的受訪者計劃在未來 12 到 18 個月內採用 Wi-Fi 6E。 Wi-Fi 普及率不斷提高的前景預計將推動無線連線市場大幅成長。

無線連線市場趨勢

汽車產業可望推動市場成長

- 藍牙無線連接擴大被各種汽車系統設備採用,以實現免持通話、音訊串流、車載資訊娛樂系統等的無線通訊和連接。使用 Wi-Fi 和藍牙等無線連接,用戶可以將他們的智慧型手機和其他智慧型裝置連接到資訊娛樂系統。因此,預計汽車銷售的成長將推動對無線連接解決方案的需求。

- 現代汽車越來越像移動物聯網 (IoT) 設備,使用一系列感測器收集內部和外部資訊並採取行動,以提高駕駛員的安全性和舒適度。無線通訊在汽車技術進步中發揮著不可或缺的作用,ADAS(高級駕駛輔助系統)和車載資訊娛樂等應用產生的資料量不斷增加,推動著藍牙、Wi-Fi 和蜂窩等無線技術的創新,從而促進市場成長。

- 自動駕駛和聯網汽車在消費者中越來越受歡迎,預計將繼續成長。展出的高級駕駛輔助系統 (ADAS) 旨在縮小當今和未來車輛之間的差距。此外,隨著汽車行業技術創新的不斷發展,終端消費者願意在最新技術上投入更多,以增強駕駛體驗並提高駕駛員和乘客的安全性。預計這將推動對自動駕駛汽車無線連接解決方案的需求。

- 此外,通用汽車中東公司還推出了與Google合作開發的新型車載技術,增強了其在連接領域的領導地位並提升了客戶體驗。通用汽車中東公司宣布推出嵌入Google的資訊娛樂系統,作為其車輛智慧技術目標的一部分。這些新功能增強了整體客戶體驗,使客戶更容易將他們的數位生活帶入未來的聯網汽車。

- Google 內建服務將成為 LT 裝飾及以上車型的標準配置,並將在所有配備 OnStar 模組系統的通用汽車品牌中廣泛推廣。這意味著科威特和阿拉伯聯合大公國的客戶可以透過他們的 Wi-Fi 計劃享受 Google 的內建服務,而科威特和巴林的客戶可以透過他們的個人行動 Wi-Fi 熱點進行連線。

亞太地區可望創下高成長

- 該地區的市場成長主要受益於消費者支出的成長和智慧家庭的日益普及。根據軟體公司Utimaco在2023年4月進行的數位調查,新加坡智慧家庭設備的使用率大幅增加,61%的受訪者表示使用智慧電視,43%表示使用家用電器,33%表示使用節能設備、虛擬助理和吸塵機器人。這是該地區擴大採用無線連接解決方案的主要成長要素。

- 智慧城市日益發展的趨勢正在鼓勵公司和機構開發新產品和解決方案,促進該地區智慧城市的發展。例如,2023 年 10 月,IIIT 海德拉巴智慧城市生活實驗室與安全智慧無線技術領導者 Silicon Labs 合作,宣布部署覆蓋校園的 Wi-SUN 網路,以支援物聯網 (IoT) 和智慧城市的研究和解決方案。這些發展正加速整個全部區域對於無線連線的需求。

- 此外,該地區 5G 網路的擴張預計將成為直接和間接推動市場成長的主要因素之一。根據GSMA最新報告,預計2030年,5G將為東亞和太平洋新興經濟體貢獻約9,600億美元。 5G有望成為該地區部署自動化智慧工廠的主要動力。

- 物聯網(IoT)平台的採用在中國正在迅速成長。中國在半導體生產和製造領域的主導地位及其在工業物聯網(lIoT)推進和應用方面的參與和發展預計將在終端用戶行業中創造對無線連接的需求。

無線連線產業概況

無線連接市場的競爭格局較為分散,市場上有許多參與者競爭,包括高通公司、英特爾公司、德州儀器公司、恩智浦半導體公司和微晶片科技公司。市場正在透過產品推出、合併和收購進行策略探索,以獲得競爭優勢。

- 2024年2月,全球物聯網解決方案供應商移遠通訊宣布推出兩款新型Wi-Fi模組FCU741R和FCS950R,以及藍牙模組HCM010S和HCM111Z。隨著藍牙和Wi-Fi模組的推出,該公司旨在為設計人員和開發人員提供多種選擇,以滿足尺寸、成本和功率效率的不同需求。

- 2024 年 1 月,Ceva Inc.(一家使智慧邊緣設備能夠可靠且有效率地連接、感知和推斷資料的矽和軟體 IP 授權商)與凌陽科技(一家多媒體和汽車應用晶片提供者)擴大了合作,將 Ceva 最新一代 RivieraWaves 藍牙音訊解決方案整合到無線系統 airlyra HD 無線設備系列中,該系列針對其他揚聲器和連接藍牙裝置。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場動態

- 市場促進因素

- 物聯網和連網型設備的興起為強大的無線連接解決方案提供了助力

- 建構智慧基礎設施對無線感測器網路的需求不斷增加

- 市場挑戰

- 資料隱私和安全問題

- 缺乏基礎建設、實施成本龐大、缺乏技術訣竅

第6章 市場細分

- 依技術分類

- Wi-Fi

- Bluetooth

- Zigbee

- 其他技術

- 按最終用戶產業

- 車

- 產業

- 衛生保健

- 能源

- 基礎設施

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Qualcomm Incorporated

- Intel Corporation

- Texas Instruments Inc.

- NXP Semiconductors NV

- Microchip Technology Inc.

- MediaTek Inc.

- Rensas Electronics Corporation

- Broadcom Inc.

- STMicroelectronics

- Nordic Semiconductor

第8章投資分析

第9章:市場的未來

The Wireless Connectivity Market size is estimated at USD 101.84 billion in 2025, and is expected to reach USD 185.89 billion by 2030, at a CAGR of 12.79% during the forecast period (2025-2030).

Key Highlights

- The wireless connectivity market is experiencing significant growth, driven by the increasing demand for seamless internet access and interconnected devices encompassing various technologies, including Wi-Fi, Bluetooth, and Zigbee, enabling data transmission without requiring cables.

- The proliferation of connected devices across various sectors like healthcare and smart homes drives demand for low-power, short-range connectivity solutions, such as Bluetooth and Zigbee. For instance, Amazon's growing portfolio of Echo smart speakers leverages Wi-Fi and Bluetooth technology for connectivity. In addition, the growing consumer interest in smart home devices, such as smart thermostats, lighting, and security systems, is boosting the demand for wireless connectivity.

- The increasing demand for consumer electronic devices drives the market's growth. Adopting advanced technologies like AI, IoT, AR, and VR is also accelerating demand for wireless connectivity across various industry verticals. The global development of smart infrastructure is also a significant factor in the increasing demand for wireless connectivity.

- Moreover, the increasing investment by governments globally in smart city projects that use wireless connectivity for various applications is propelling the market's growth. For instance, in October 2023, the Department of Information Technology, Electronics & Communication (DITE&C) announced a plan to set up and operationalize more than 100 Wi-Fi hotspots across the state to provide free and seamless internet services. The hotspots will be at selected government offices, bus stands, public parks, citizen service centers, and other locations with high footfalls.

- However, security concerns are restraining the wireless connectivity market's growth as wireless networks are vulnerable to cyberattacks. As wireless communication continues to grow across industries and applications, strong security measures are essential to prevent data breaches and malware attacks. Poor encryption protocols, weak authentication mechanisms, and vulnerable network configurations can reveal sensitive information and compromise the security of wireless systems.

- For instance, according to a survey by the Wireless Broadband Alliance (WBA) as part of the WBA Annual Industry Report 2023, more than a third (33%) of service providers, technology vendors, and enterprises already plan to deploy Wi-Fi 7 by the end of 2023. Further, 44% are planning to adopt Wi-Fi 6E in the next 12-18 months. Such growth prospects in adopting Wi-Fi are anticipated to add significant growth to the wireless connectivity market.

Wireless Connectivity Market Trends

The Automotive Industry is Expected to Drive the Market's Growth

- Bluetooth wireless connectivity is increasingly used in various automotive system equipment to enable wireless communication and connectivity, including hands-free calling, audio streaming, and in-car infotainment systems. By using wireless connectivity like wi-fi and bluetooth, users are able to connect their smartphones and other smart devices to their infotainment systems. Thus, the growth in the sales of automotive vehicles would drive demand for wireless connectivity solutions.

- Modern automobiles increasingly resemble mobile internet of things (IoT) devices and increasingly use a wide range of sensors to enhance driver safety and comfort by collecting and responding to internal and external information. As wireless communications play an essential role in advancing automotive technology, the increasing amount of data produced by applications like advanced driver assistance systems (ADAS) and in-vehicle infotainment is driving innovations in wireless technologies like bluetooth and wi-fi, as well as cellular and adding growth to the market.

- Autonomous vehicles and connected cars are becoming more popular among consumers and are expected to continue to grow over the coming years. The advanced driving assistance systems (ADAS) on display aim to bridge the gap between the cars of today and the cars of tomorrow. In addition, with more technological innovation in the auto industry, end consumers are willing to spend more money on the newest technology that enhances the driving experience and enhances the safety of drivers and passengers. This would drive demand for wireless connectivity solutions for autonomous vehicles.

- Moreover, GM Middle East launched new in-vehicle technology with Google built-in, strengthening connectivity leadership and enhancing the customer experience. General Motors Middle East announced the introduction of infotainment systems with Google built in as part of its vehicle intelligence technology goals. These new features would augment the overall customer experience and make it easier for customers to bring their digital lives into future connected vehicles.

- The Google built-in services would be standard on LT and higher trims, with widespread deployment across all GM vehicle brands equipped with the OnStar module system. Thus, customers in Kuwait and the UAE can utilize Google built-in via their wi-fi plans, while those in KSA and Bahrain can connect through their personal mobile wi-fi hotspots.

Asia-Pacific is Expected to Register High Growth Rate

- The market expansion in the region is primarily driven by consumers' increased spending and the growing adoption of smart homes. According to a digital survey conducted by Utimaco, a software company, in April 2023, the use of smart home devices has significantly increased in Singapore, with 61% of respondents stating that they are using smart TVs, 43% using home appliances, and 33% using energy saving devices, virtual assistants, and vacuum cleaner robots. This becomes a primary growth factor for the region's increasing adoption of wireless connectivity solutions.

- The rise in the trend towards smart cities is pushing firms or institutions to develop new products or solutions to ease the development of smart cities in the region. For instance, in October 2023, the Living Lab IIIT Hyderabad Smart City, in collaboration with Silicon Labs, a leader in secure, intelligent wireless technology, announced the introduction of a campus-wide Wi-SUN network to support research and solutions for the internet of things (IoT) and smart cities. Such developments are accelerating the demand for wireless connectivity across the region.

- Additionally, the expansion of 5G networks in the region is expected to be one of the major factors driving the growth of market, both directly and indirectly. According to the GSMA's latest report, 5G is expected to contribute about USD 960 billion to the developed economies of East Asia and the Pacific by 2030. 5G is expected to be a significant driving force in automated smart factory deployments in the region.

- The widespread use of the internet of things (IoT) platform in China is increasing rapidly. Given China's leading role in the production of semiconductors and manufacturing, its participation in the advancement and application of the industrial internet of things (lIoT) and the development are expected to create demand for wireless connectivity across end-user industries.

Wireless Connectivity Industry Overview

The competitive landscape for the wireless connectivity market is fragmented, with a large number of players competing in the market, including Qualcomm Incorporated, Intel Corporation, Texas Instruments Inc., NXP Semiconductors NV, and Microchip Technology Inc. The market is witnessing strategic developments, such as product launches, mergers, and acquisitions, to gain a competitive edge.

- In February 2024, Quectel Wireless Solutions, a global IoT solutions provider, launched two new wi-fi modules, the FCU741R and the FCS950R, and bluetooth modules, the HCM010S and the HCM111Z. Through this launch of bluetooth and wi-fi modules, the company aims to empower designers and developers with multiple options, catering to diverse needs in terms of size, cost, and power efficiency.

- In January 2024, Ceva Inc., the licensor of silicon and software IP that enables Smart Edge devices to connect, sense, and infer data reliably and efficiently, and Sunplus Technology Co. Ltd, a chip provider for multimedia and automotive applications have expanded their collaboration to integrate Ceva's latest generation RivieraWaves Bluetooth audio solution into the Sunplus airlyra family of HD audio processors targeting wireless speakers, soundbars and other premium wireless audio devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Proliferation of IoT and Connected Devices for Robust Wireless Connectivity Solutions

- 5.1.2 Increased Demand for Wireless Sensor Networks to Create Smart Infrastructure

- 5.2 Market Challenges

- 5.2.1 Data Privacy and Security Concerns

- 5.2.2 Lack of Infrastructure, Huge Implementation Cost, and Absence of Technology Know-how

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Wi-Fi

- 6.1.2 Bluetooth

- 6.1.3 Zigbee

- 6.1.4 Other Technologies

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Industrial

- 6.2.3 Healthcare

- 6.2.4 Energy

- 6.2.5 Infrastructure

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Qualcomm Incorporated

- 7.1.2 Intel Corporation

- 7.1.3 Texas Instruments Inc.

- 7.1.4 NXP Semiconductors NV

- 7.1.5 Microchip Technology Inc.

- 7.1.6 MediaTek Inc.

- 7.1.7 Rensas Electronics Corporation

- 7.1.8 Broadcom Inc.

- 7.1.9 STMicroelectronics

- 7.1.10 Nordic Semiconductor

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

無線連接市場:按技術類型、組件、應用和最終用戶分類 - 2026-2032年全球市場預測

無線連接市場:按技術類型、組件、應用和最終用戶分類 - 2026-2032年全球市場預測 2026年全球無線連接市場報告

2026年全球無線連接市場報告 無線連接市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形式、設備、部署類型及最終用戶分類

無線連接市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形式、設備、部署類型及最終用戶分類 日本無線接取市場報告:按技術、網路類型、最終用戶和地區分類(2026-2034年)

日本無線接取市場報告:按技術、網路類型、最終用戶和地區分類(2026-2034年) 無線連接市場規模、佔有率和成長分析(按類型、最終用途和地區分類)—2026-2033年產業預測

無線連接市場規模、佔有率和成長分析(按類型、最終用途和地區分類)—2026-2033年產業預測 無線連接市場-全球產業規模、佔有率、趨勢、機會及預測(按技術、終端用戶產業、地區和競爭格局分類,2020-2030 年預測)

無線連接市場-全球產業規模、佔有率、趨勢、機會及預測(按技術、終端用戶產業、地區和競爭格局分類,2020-2030 年預測) 無線連接晶片組市場-2025-2030年預測

無線連接晶片組市場-2025-2030年預測 無線物聯網連接晶片組市場:2025-2030

無線物聯網連接晶片組市場:2025-2030 無線連線的市場資料概要:2025年第3季

無線連線的市場資料概要:2025年第3季 2032 年橋接晶片市場預測:按類型、功能、配置、技術、應用、最終用戶和地區進行的全球分析

2032 年橋接晶片市場預測:按類型、功能、配置、技術、應用、最終用戶和地區進行的全球分析