|

市場調查報告書

商品編碼

1644431

美國OTT:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)US OTT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

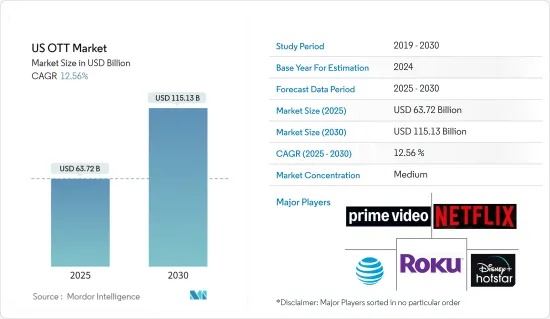

預計 2025 年美國OTT 市場規模為 637.2 億美元,到 2030 年將達到 1,151.3 億美元,預測期內(2025-2030 年)的複合年成長率為 12.56%。

美國是全球最大的OTT市場之一。智慧型電視和智慧型手機等智慧型裝置的高普及率、對 VOD 內容的不斷成長的需求以及每用戶的高付款率是推動該國 OTT 市場發展的主要因素。 Netflix 和亞馬遜等全球大多數頂級 OTT 供應商都位於美國,這使得他們在這個區域市場中具有優勢。

主要亮點

- 對 OTT 內容的日益關注將使美國公民擺脫有線電視、地理限制和廣播時間表的限制,從根本上改變影片的銷售、製作和消費方式。因此,由於類型客製化、包裝靈活性、可在多種設備上使用、網際網路普及率和低成本,採用率正在增加。 Netflix 和 Amazon 是全國訂閱量最大的 OTT 平台。

- 隨著收益的成長,OTT影片內容觀看時間佔有率的激增反映了串流媒體的成長,這正在改變該國的娛樂格局。據 Uscreen 稱,美國觀眾每周平均觀看 21 小時的內容,到 2024 年,這將相當於一份串流數位媒體的兼職工作。值得注意的是,65% 的內容是透過行動和電視應用程式而不是網路瀏覽器消費的。

- 然而,對於OTT提供者而言,消費量的增加也意味著成本的上升,並且根據所採用的內容傳遞網路模式,服務會受到不同程度的影響。 CDN 服務通常會對傳輸的內容收費,因此隨著 OTT 觀看次數的增加,OTT 提供者的傳輸成本也會增加。

- 此外,人們看電視的時間越來越長,並且已經習慣了在線觀看電視內容。因此,我們預計短期內將實現正成長。在供應商方面,提供直接面對消費者(D2C)服務並由美國免費串流服務Pluto TV支援的維亞康姆是重要的供應商。

美國OTT 市場趨勢

智慧型電視普及率高,成長顯著

- 該地區正看到越來越多的內容擁有者,如迪士尼、通訊業者(AT&T)和純 OTT 提供者(如亞馬遜)直接向消費者提供串流內容。同時,4K 串流媒體的出現也推動了 OTT 內容的成長,並使其能夠在智慧電視格式中提供。

- 串流媒體設備使用量的持續成長、網際網路普及率的提高以及對智慧型電視的需求,為媒體公司進入Over-The-Top(OTT) 行業提供了豐厚的機會。多家電視製造商正在推出創新的智慧電視。

- 例如,SONY電子在2023年3月發布了2023年BRAVIA XR電視陣容,搭載認知處理器XR,提供家庭娛樂體驗。該公司推出了其 BRAVIA XR 系列的幾款新產品:X95L、X93L Mini LED、X90L 全陣列 LED、A95L QD-OLED 和 A80L OLED。所有型號均整合技術,為觀看電影、玩遊戲、串流媒體應用等創造身臨其境的體驗。

- 在內容消費方面,消費者的觀看模式正在改變。網路消費的成長速度快於傳統電視觀看。推動市場發展的關鍵因素是可負擔價格的訂閱計劃的靈活性。消費者對家庭娛樂的興趣日益濃厚,他們在地下室使用智慧型電視來營造家庭劇院體驗。此外,內容類型的多樣性、舒適性、自由度和時間靈活性正在推動市場成長。

- 內容創作者與 Netflix 合作,將其內容獨家發佈在該平台上。例如,2023 年,佩里和 Netflix 達成創新夥伴關係關係,根據一份多年期協議,佩里將參與編寫、監督和製作長電影長片。據Netflix稱,2024年第一季,該串流平台在美國和加拿大的付費用戶群已達8,266萬,足見該平台的受歡迎程度。許多製作人正在與 Netflix 合作,利用我們的整合功能賺取更多收益。

SVoD 市場佔有主要市場佔有率

- 訂閱隨選視訊(SVoD)類似於傳統電視套餐,用戶只需支付固定費率即可觀看任意數量的內容。主要服務包括 Sky(及其子公司 Now TV)、Amazon Prime Video、Netflix 和 Hulu。

- 美國六大平台主導 SVoD:Netflix、亞馬遜、Disney+、Paramount+、Apple TV+ 和 HBO。 SVoD平台的出現也有助於吸引更多消費者。預計未來五年美國的 SVoD 訂閱數量將大幅增加。

- 美國OTT市場的SVoD部分是關鍵部分之一。到2025年,預計將有12個平台擁有超過500萬付費用戶,顯示美國市場領先世界其他地區。由於來自 Disney+、Peacock 和 CBS All Access 等年輕競爭對手的激烈競爭,亞馬遜、Netflix 和 Hulu 等現有參與者可能會面臨成長挑戰。

- 根據Media Play的資料,SVoD預計在2023年貢獻525億美元,到2029年達到546億美元。市場的主要企業正在提供更便宜的訂閱計劃以吸引更多的客戶。 OTT 平台具有內容多樣性、靈活性、身臨其境型體驗和提供本地內容的特點,是推動市場成長的主要因素。

美國OTT 產業概況

隨著越來越多的公司進入市場,美國OTT市場正在逐步整合,參與企業。主要市場參與者正在採取各種策略來擴大市場佔有率,包括併購。此外,電視廣播廣播公司也透過推出應用程式或投資替代 OTT 平台進入市場。最終,在未來幾年,預計大多數有線電視營運商都將投資這些經營模式,以確立其在該行業的地位。

- 2024 年 4 月:Roku 宣布與 The Trade Desk、iSpot 和 NBCUniversal 建立合作關係。此次合作旨在解決連網電視面臨的問題,例如程式化採購和易於測量等。此外,透過與 NBCUniversal 合作,2024 年巴黎奧運的精彩片段將在 Roku 平台上播出。與 The Trade Desk 的合作將允許獨立需求方平台 (DSP) 存取 Roku 庫存資料,從而使媒體購買者能夠更精準地定位受眾。

- 2024 年 3 月,華特迪士尼宣布將在美國向迪士尼捆綁用戶推出 Disney+ 上的 Hulu。這使得用戶可以探索數以千計的綜合娛樂節目,並在提供個人化體驗的同時享受 Hulu 和 Disney+ 內容。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 當前市場狀況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- COVID-19 對產業的影響

第5章 市場動態

- 市場促進因素

- 智慧型電視的高普及率和主要 OTT 供應商的存在將促進該地區 OTT 的普及

- 強調透過市場整合建立合作與夥伴關係

- 市場限制

- 資料隱私和安全問題

第6章 市場細分

- 按類型

- SVoD

- TVoD

- AVoD

第7章 OTT 播放市場類型

第8章 競爭格局

- 公司簡介

- Netflix

- Disney+

- Amazon Prime Video

- Roku

- HBO Max(AT&T Inc.)

- CBS All Acess(Viacomcbs Inc.)

- Sling TV LLC

- Apple Inc.

- YouTube(Google LLC)

第9章投資分析

第10章:市場的未來

The US OTT Market size is estimated at USD 63.72 billion in 2025, and is expected to reach USD 115.13 billion by 2030, at a CAGR of 12.56% during the forecast period (2025-2030).

The United States is one of the largest OTT markets in the world. The high penetration of smart devices, like smart TVs and smartphones, growing demand for VOD content, and a high rate of per-user payment are some of the major factors driving the country's OTT market. Most of the top global OTT vendors, like Netflix and Amazon, are US-based, providing an advantage to the regional market.

Key Highlights

- The increasing gravitation toward OTT content allows US citizens to get rid of cables, geographic restrictions, and broadcast schedules and fundamentally changes how video is sold, produced, and consumed. Thus, increasing adoption has been attributable to customized genre choices, package flexibility, wider device availability, internet penetration, and lower costs. Netflix and Amazon are the most commonly subscribed OTT platforms in the country.

- With increasing revenue numbers, the surging percentage of viewing time going to OTT video content reflects the streaming growth and is changing the country's entertainment landscape. According to the Uscreen, viewers spend an average of 21 hours per week consuming content in the United States, equivalent to a part-time job streaming digital media in 2024. Notably, 65% of content is consumed via mobile or TV apps rather than web browsers.

- However, some costs for OTT providers also rise along with increased consumption, with services impacted by varying degrees depending on the content delivery network model employed. As the OTT viewing amount increases, so does the OTT provider's delivery cost since CDN services are usually charged for the content delivered.

- Moreover, the hours spent on TV have risen, and people are getting used to watching TV content online. This entails a positive growth outlook on a near-term basis. On the vendor front, Viacom is a significant vendor offering a direct-to-consumer (D2C) service on the back of Pluto TV, the free streaming service company in the United States.

US OTT Market Trends

High Penetration of Smart TV Witnesses Significant Growth

- Streaming content in the region has intensified as content owners like Disney go directly to consumers, telcos (AT&T), and OTT-only operators like Amazon, to name a few. Simultaneously, the emergence of 4K for streaming has propelled OTT content growth to be made available across smart TV formats.

- Consistent growth in streaming device usage, increasing internet penetration, and demand for smart TVs have provided lucrative opportunities for media companies to enter the over-the-top (OTT) industry. Several TV makers are introducing innovative smart TVs.

- For instance, in March 2023, Sony Electronics announced the 2023 BRAVIA XR TV Lineup, equipped with Cognitive Processor XR, for a home entertainment experience. The company launched a few new BRAVIA XR lines: X95L and X93L Mini LED, X90L Full Array LED, A95L QD-OLED, and A80L OLED. All models are integrated with technology to create an immersive experience for watching movies, gaming, streaming apps, and others.

- Consumer viewership is transforming in terms of content consumption. There is more growth in online consumption than traditional TV viewership. Major factors driving the market are the flexibility of subscription plans that are available at affordable prices. Consumers have grown their interest in home entertainment by using Smart TVs in their basement areas to create home theater experiences. Additionally, it allows a diversity of content genres, comfort, freedom, and time flexibility, propelling the market's growth.

- Content producers are partnering with Netflix to feature their content exclusively on the platform. For instance, in 2023, Perry and Netflix signed a creative partnership in which Perry contributed to writing, directing, and producing feature films under a multi-year deal. According to Netflix, the number of subscribers paying for streaming platforms in the United States and Canada accounted for 82.66 million in Q1 2024, which shows the popularity of the platform. Many producers are collaborating with Netflix to generate more revenue using integrated capabilities.

SVoD Segment to Hold Significant Market Share

- Subscription video-on-demand (SVoD) is similar to traditional TV packages, allowing users to consume as much content as they desire at a flat monthly rate. Major services include Sky (also its subsidiary Now TV), Amazon Prime Video, Netflix, and Hulu.

- Six major US-based platforms, namely Netflix, Amazon, Disney+, Paramount+, Apple TV+, and HBO, dominate the SVoD landscape. The emergence of SVoD platforms is also helping to attract more consumers. The number of SVoD subscriptions in the United States is projected to grow significantly in the next five years.

- The SVoD segment in the US OTT market is one of the significant segments. By 2025, the country is expected to witness a dozen platforms with more than 5 million paying subscribers, revealing just how ahead the US market is compared with the rest of the world. Growth for established players such as Amazon, Netflix, and Hulu will be affected due to intense competition from younger rivals such as Disney+, Peacock, and the augmented CBS All Access.

- As per the data by Media Play, SVoD contributed USD 52.5 billion in 2023, which is expected to reach USD 54.6 billion by 2029. Major market players are offering cheaper subscription plans to attract more customers. OTT platforms featuring content diversity, flexibility, immersive experiences, and regional content offered are the major drivers that foster the market's growth.

US OTT Industry Overview

The US OTT market is witnessing increasing competitive rivalry as more companies enter, leading to the gradual consolidation of the market. The major market players are involved in various strategies to expand their market share, including mergers and acquisitions. Moreover, TV broadcasters are entering the market either by launching their app or investing in another OTT platform. Eventually, in the coming years, most TV cable operators are expected to invest in these business models to establish their presence in the industry.

- April 2024: Roku announced a partnership with Trade Desk, iSpot, and NBCUniversal. This alliance aims to solve the problem faced during connected television space, which includes ease of programmatic buying and measurement. Moreover, in collaboration with NBCUniversal, it will provide 2024 Paris Olympics highlights, featuring all available sports for Olympics coverage on the Roku platform. In partnership with the Trade Desk, it facilitates independent Demand Side Platform (DSP) to gain access to Roku data on Roku inventory, which will allow media buyers to target viewers with more precision.

- March 2024: Walt Disney announced the launch of Hulu on Disney+ in the United States for Disney Bundle subscribers, which brought a variety of genres with integrated content libraries. This allowed subscribers to explore thousands of general entertainment titles, bringing Hulu and Disney+ content together with a personalized experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market drivers

- 5.1.1 High Penetration of Smart TV and the Presence of Major OTT Providers have Contributed to the Growth of OTT Adoption in the Region

- 5.1.2 Market Consolidation to Result in Emphasis on Collaboration and Partnerships

- 5.2 Market Restraints

- 5.2.1 Data Privacy and Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 SVoD

- 6.1.2 TVoD

- 6.1.3 AVoD

7 OTT PLAYBACK MARKET - BY GENRE

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Netflix

- 8.1.2 Disney+

- 8.1.3 Amazon Prime Video

- 8.1.4 Roku

- 8.1.5 HBO Max (AT&T Inc.)

- 8.1.6 CBS All Acess (Viacomcbs Inc.)

- 8.1.7 Sling TV LLC

- 8.1.8 Apple Inc.

- 8.1.9 YouTube (Google LLC)

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

2026年全球OTT串流媒體市場報告2026年全球OTT設備與服務市場報告

2026年全球OTT串流媒體市場報告2026年全球OTT設備與服務市場報告 OTT內容市場分析及預測(至2035年):依類型、產品類型、服務、技術、設備、最終用戶、部署類型、應用程式和元件分類OTT( Over-The-Top)市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、設備、部署類型和最終用戶分類

OTT內容市場分析及預測(至2035年):依類型、產品類型、服務、技術、設備、最終用戶、部署類型、應用程式和元件分類OTT( Over-The-Top)市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、設備、部署類型和最終用戶分類 OTT內容市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

OTT內容市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 OTT( Over-the-Top)設備與服務市場-2026-2031年預測全球OTT市場-產業規模、佔有率、趨勢、機會和預測:按內容類型、平台、用戶類型、最終用戶、地區和競爭對手分類,2021-2031年

OTT( Over-the-Top)設備與服務市場-2026-2031年預測全球OTT市場-產業規模、佔有率、趨勢、機會和預測:按內容類型、平台、用戶類型、最終用戶、地區和競爭對手分類,2021-2031年 日本OTT平台市場規模、佔有率、趨勢及預測(依收入模式、內容類型、串流媒體設備、使用者類型、服務區域及地區分類),2026-2034年日本Over-The-Top市場報告:按組件、平台類型、部署模式、內容類型、收入模式、產業垂直領域和地區分類(2026-2034年)

日本OTT平台市場規模、佔有率、趨勢及預測(依收入模式、內容類型、串流媒體設備、使用者類型、服務區域及地區分類),2026-2034年日本Over-The-Top市場報告:按組件、平台類型、部署模式、內容類型、收入模式、產業垂直領域和地區分類(2026-2034年) OTT設備和服務市場按設備類型、服務類型、內容類型、收益來源和最終用戶分類-2025-2032年全球預測

OTT設備和服務市場按設備類型、服務類型、內容類型、收益來源和最終用戶分類-2025-2032年全球預測