|

市場調查報告書

商品編碼

1644443

印尼硬質塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Indonesia Rigid Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

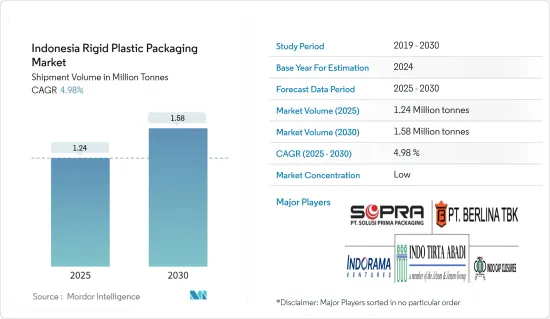

以出貨量為準,印尼硬質塑膠包裝市場規模預計將從 2025 年的 124 萬噸成長到 2030 年的 158 萬噸,預測期間(2025-2030 年)的複合年成長率為 4.98%。

由於塑膠包裝的演變和採用,印尼硬質塑膠包裝市場目前的表現有所不同。印尼下游硬質塑膠包裝市場高度發達,但由於依賴進口原料,成長潛力有限。

主要亮點

- 印尼的工業部門對於支撐該國的經濟成長至關重要。在過去幾年裡,該產業的產量和產值顯著成長。這背後的主要因素包括政府對投資者的激勵措施、友善的商業環境、技術進步和熟練的勞動力。在消費支出不斷成長的推動下,預計未來幾年印尼硬質塑膠包裝市場將繼續成長。

- 塑膠包裝重量輕、易於處理,比其他類型的包裝更受消費者歡迎。甚至大型製造商也因其生產成本低而更喜歡塑膠包裝解決方案。此外,聚對苯二甲酸乙二酯(PET)、高密度聚苯乙烯(HDPE)等聚合物的出現擴大了塑膠包裝的應用範圍。各行各業對寶特瓶的需求正在增加。

- 印尼在亞洲不斷擴大的消費市場中發揮關鍵作用,而包裝材料方面的投資穩步湧入也凸顯了這一作用,這與全部區域高階包裝日益成長的需求相一致。例如,2023年1月,BASF擴大了位於印尼Merak工廠的聚合物分散體生產能力。

- 印尼對硬質塑膠包裝的需求正在增加。硬質塑膠包裝應用於工業、零售和醫療保健等多個領域。由於其優異的阻隔性、較長的保存期限和耐用性,塑膠包裝在醫療保健領域正經歷顯著的成長。

- 全國各地的製造商都傾向於使用硬質塑膠包裝,因為它是一種經濟有效的解決方案,可以在從農場到餐桌的運輸過程中保護食品和飲料,並長期保存食品。這些包裝還支援各種形狀和形式的創新,並且重量輕。

- 然而,預測期內監管標準的變化、原料成本的波動、廢物量的增加以及環境廢棄物法規的日益嚴格預計將阻礙市場的成長。這也有望鼓勵企業開發具有顛覆性潛力的新產品,並降低當前市場的風險。

印尼硬質塑膠包裝市場的趨勢

聚對苯二甲酸乙二醇酯(PET)預計將出現強勁成長

- 印尼包裝產業對 PET 的需求正在增加。良好的阻隔性、高抗張強度、優異的表面光潔度和低成本使 PET 成為許多塑膠包裝應用的理想產品。

- 與玻璃相比,PET 的引入可節省高達 90% 的重量,使運輸過程更加經濟。 寶特瓶現在為礦泉水和其他飲料提供可重複使用的包裝,取代了沉重而易碎的玻璃瓶。

- 在硬質塑膠包裝市場,PET 用於製造微波食品托盤、軟性飲料、水、果汁、運動飲料、啤酒、漱口水、番茄醬、沙拉醬和食品罐的塑膠瓶。家庭護理、飲料和個人護理等各個終端用戶行業對寶特瓶的需求正在成長。這種成長是由消費者偏好和 PET 的特性(例如重量輕、可回收性高)所推動的。

- 為了符合要求並建立閉合迴路回收週期,當地市場供應商也致力於使 PET 一次性包裝更加可回收。隨著人們對 PET 一次性包裝回收的重視程度不斷提高,預計 PET 一次性包裝將迎來成長機會。

- 隨著牛奶飲料需求的不斷成長,製造商正在生產輕質、透明的塑膠瓶。這不僅提高了產品的知名度,而且解決了成本效益和永續性的擔憂。其中, 寶特瓶是牛奶的首選包裝,因為其重量輕,降低了運輸成本,而且易於消費者拿取。

- 根據印尼統計局 2023 年 6 月發布的資料,2022 年,印尼乳牛廠生產了約 1.3 億公升牛奶,比 2020 年有所成長。在研究期間,印尼這些產品的產量保持相對穩定。全國穩定的牛奶產量可能會在未來幾年增加牛奶包裝用寶特瓶的需求。

食品領域可望佔據主要市場佔有率

- 硬質塑膠包裝,包括寶特瓶和容器,在食品包裝應用中仍然很受歡迎。容器用於包裝消費品,包裝用的是HDPE和LDPE。

- 印尼食品業採用各種硬質塑膠包裝。印尼人對食用有機食品的興趣越來越大,導致有機農產品的採購和出口增加。印尼包裝的主要最終用途之一是食品。然而,印尼長期以來一直進口大量加工食品和基本食品原料。

- 用於製造瓶子和容器產品的材料包括聚對苯二甲酸乙二酯(PET)和聚丙烯(PP)。 PP 經過吹塑成型可製成木箱、木瓶和木鍋。由PP製成的薄壁容器是印尼各地的標準,用於食品包裝。

- 印尼政府推出了新的食品接觸包裝法,以更新該國的包裝標準,並使其與美國FDA 和歐盟食品立法等國際標準保持一致。修訂後的法規涵蓋了五種包裝類別的國產和進口食品包裝,包括硬質塑膠。

- 隨著印尼食品產業的商機不斷成長,一些國際參與者不斷投資該市場,為硬質塑膠製造商創造更多創新和推出塑膠食品包裝選擇的途徑。根據印尼統計局2024年2月發布的報告,2023年印尼食品業的外國直接投資達到約22.6億美元,高於2020年的15.9億美元。

印尼硬質塑膠包裝產業概況

印尼硬質塑膠包裝市場比較分散。由於大量製造公司在該國營運,分散化現象正在加劇。市場參與者正在尋求透過投資研發、將新技術融入其產品以及提供改進的消費產品來保持優勢。策略聯盟、協議、合併和夥伴關係關係是所採用的一些策略。

- 2024 年 7 月,領先的塑膠薄片供應商 PT ALBA Tridi 宣佈建立最先進的 rPET 工廠,反映了政府促進平衡和支持綠色投資的政策。該工廠是中爪哇省第一家食品級 rPET 製造商,預計將增強當地經濟並促進當地中小微型企業的發展。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 貿易情景

- 貿易分析(前 5 名進出口國)

第5章 市場動態

- 市場促進因素

- 食品飲料包裝產業需求強勁

- 市場限制

- 與軟質塑膠包裝的競爭

第6章 市場細分

- 依樹脂類型

- 聚乙烯 (PE)

- 低密度聚乙烯 (LDPE) 和線型低密度聚乙烯(LLDPE)

- 高密度聚苯乙烯(HDPE)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 聚苯乙烯 (PS) 和發泡聚苯乙烯 (EPS)

- 聚氯乙烯(PVC)

- 其他樹脂類型

- 聚乙烯 (PE)

- 依產品類型

- 瓶子和罐子

- 托盤和容器

- 蓋子與封口裝置

- 中型散裝容器 (IBC)

- 鼓

- 調色盤

- 其他產品類型

- 按最終用途行業

- 食物

- 糖果零食

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾糧

- 肉類、家禽、魚貝類

- 寵物食品

- 其他食品

- 食品服務

- 飲料

- 衛生保健

- 化妝品和個人護理

- 工業

- 建築和施工

- 汽車

- 其他最終用戶產業

- 食物

第7章 競爭格局

- 公司簡介

- PT. Berlina Tbk

- PT Indo Tirta Abadi

- PT.Solusi Prima Packaging

- PT. Indorama Ventures Indonesia

- Indo Cap Closures

- PT. Hasil Raya Industries

- PT. Hokkan Deltapack Industri

- PT Rheem Indonesia

- PT. Neilsen

- PT. Namasindo Plus

- 熱圖分析

- 競爭分析:新興企業與現有公司

第 8 章回收與永續性展望

第9章:未來展望

The Indonesia Rigid Plastic Packaging Market size in terms of shipment volume is expected to grow from 1.24 million tonnes in 2025 to 1.58 million tonnes by 2030, at a CAGR of 4.98% during the forecast period (2025-2030).

The Indonesian rigid plastic packaging market now operates differently as a result of the evolution and adoption of plastic packaging. Although Indonesia's downstream rigid plastic packaging market is highly developed, its reliance on imported raw materials has limited its growth potential.

Key Highlights

- Indonesia's industrial sector has been pivotal in bolstering the nation's economic growth. Over the past few years, this sector has seen a notable uptick in both production volume and value. Key drivers of this include government incentives for investors, a business-friendly environment, technological advancements, and a skilled workforce. The rigid plastics packaging market in Indonesia is poised for continued growth in the coming years, fueled by surging consumer spending.

- Plastic packaging is more popular with consumers than other types of packaging because plastic is lightweight and easy to handle. Even large manufacturers prefer plastic packaging solutions due to their low production costs. In addition, the emergence of polymers such as polyethylene terephthalate (PET) and high-density polyethylene (HDPE) has expanded the applications of plastic packaging. The demand for PET bottles is increasing across various industries.

- Indonesia's pivotal role in Asia's expansive consumer market is underscored by a steady influx of investments in packaging materials, aligning with the rising demand for premium packaging across the region. For instance, in January 2023, BASF expanded its production capacity for polymer dispersions at its Merak facility in Indonesia.

- In Indonesia, the demand for rigid plastic packaging is on the rise. Rigid plastic packaging is used in various sectors, including industrial, retail, and healthcare. Due to its excellent barrier qualities, lengthy shelf life, and durability, plastic packaging has seen substantial growth in the healthcare sector.

- Various manufacturers in the country prefer rigid plastic packaging as it is a cost-effective solution to protect food and beverages during delivery from farm to table and preserve food over longer durations. These packages also support innovations through different forms and shapes and are lighter in weight.

- However, changing regulatory standards, fluctuating raw material costs, increasing waste volumes, and rising environmental waste regulations are expected to hinder market growth during the forecast period. This is also expected to encourage companies to develop new products that are potentially disruptive and reduce the current risks in the market.

Indonesia Rigid Plastic Packaging Market Trends

Polyethylene Terephthalate (PET) is Expected to Witness Significant Growth

- The demand for PET from the packaging industry is increasing in Indonesia. Superior barrier properties, high tensile strength, better surface finish, and low cost allow PET to be an ideal product for numerous plastic packaging applications.

- The introduction of PET allows weight reductions of up to 90% compared to glass, enabling a more economical transportation process. PET plastic bottles are now replacing heavy and fragile glass bottles to provide reusable packaging for mineral water and other beverages.

- In the rigid plastic packaging market, PET is used to manufacture microwavable food trays and plastic bottles for soft drinks, water, juices, sports drinks, beer, mouthwash, ketchup, salad dressings, and food jars. There is a growing demand for PET bottles from various end-user industries, such as home care, beverages, and personal care. The growth can be attributed to consumer preference and the properties of PET, such as its lightweight nature and high recycling rate.

- In order to comply with requirements and establish a closed-loop recycling cycle, regional market vendors are also concentrating on making PET single-use packaging more recyclable. Growth opportunities for PET single-use packaging are anticipated due to the growing emphasis on recycling these materials.

- Driven by rising demand for milk-based drinks, manufacturers are producing lightweight and transparent plastic bottles. This not only enhances product visibility but also addresses concerns about cost-effectiveness and sustainability. Notably, PET bottles, being lightweight, cut down transportation costs and are easier for consumers to handle, making them the preferred choice for milk packaging.

- As per Statistics Indonesia data published in June 2023, in 2022, Indonesian dairy cow establishments produced nearly 130 million liters of milk, marking an increase from 2020. During the study period, Indonesia's production volume for these products remained relatively stable. Consistent milk production across the country may increase the demand for PET bottles for milk packaging in the upcoming years.

The Food Segment is Expected to Hold a Significant Market Share

- Rigid plastic packaging, including plastic bottles and containers, continues to be popular in food packaging applications. Containers are used to pack consumer goods, and HDPE and LDPE are used for the packaging.

- Indonesia's food industry employs a range of rigid plastic packaging options. Indonesians are becoming more interested in eating organic food, leading to stores stocking and exporting more organic produce. One of the primary end uses of packaging in Indonesia is food. However, Indonesia has long imported many processed and essential food components.

- Some materials used for making bottles and container products include polyethylene terephthalate (PET) and polypropylene (PP). PP is blow-molded to produce crates, bottles, and pots. PP thin-walled containers are standard across the country and used for food packaging.

- The Indonesian government introduced a new food contact packaging legislation to update the domestic packaging standards and align them with international standards, such as those used by the US FDA (Food and Drug Association) and EU food legislation. The revised regulation covers domestic and imported food packaging across five packaging categories, including rigid plastics.

- Owing to the growing opportunities in the Indonesian food industry, several international players are constantly investing in the market, creating more avenues for rigid plastic manufacturers to innovate and launch plastic food packaging options. According to the Statistics Indonesia report published in February 2024, in 2023, foreign direct investment in Indonesia's food industry reached around USD 2.26 billion, marking an increase from USD 1.59 billion in 2020.

Indonesia Rigid Plastic Packaging Industry Overview

The rigid plastic packaging market in Indonesia is fragmented. Numerous manufacturing companies operate in the country, leading to high fragmentation. Market players are trying to maintain dominance by investing in R&D, incorporating new technology into their products, and delivering improved consumer products. Strategic alliances, agreements, mergers, and partnerships are a few of the strategies employed.

- July 2024: PT ALBA Tridi, a key plastic flakes supplier, announced the establishment of a cutting-edge rPET facility, echoing the government's push to balance and champion green investments. This facility, marking Central Java's inaugural food-grade rPET producer, is poised to bolster the regional economy and uplift local micro, small, and medium enterprises.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Trade Scenario

- 4.4.1 Trade Analysis (Top 5 Import-Export Countries)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Strong Demand From the Food and Beverage Packaging Industry

- 5.2 Market Restraints

- 5.2.1 Competition From Flexible Plastic Packaging

6 MARKET SEGMENTATION

- 6.1 By Resin Type

- 6.1.1 Polyethylene (PE)

- 6.1.1.1 Low-Density Polyethylene (LDPE) & Linear Low-Density Polyethylene (LLDPE)

- 6.1.1.2 High Density Polyethylene (HDPE)

- 6.1.2 Polyethylene terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Polystyrene (PS) and Expanded polystyrene (EPS)

- 6.1.5 Polyvinyl chloride (PVC)

- 6.1.6 Other Resin Types

- 6.1.1 Polyethylene (PE)

- 6.2 By Product Type

- 6.2.1 Bottles and Jars

- 6.2.2 Trays and Containers

- 6.2.3 Caps and Closures

- 6.2.4 Intermediate Bulk Containers (IBCs)

- 6.2.5 Drums

- 6.2.6 Pallets

- 6.2.7 Other Product Types

- 6.3 By End-use Industries

- 6.3.1 Food

- 6.3.1.1 Candy & Confectionery

- 6.3.1.2 Frozen Foods

- 6.3.1.3 Fresh Produce

- 6.3.1.4 Dairy Products

- 6.3.1.5 Dry Foods

- 6.3.1.6 Meat, Poultry, And Seafood

- 6.3.1.7 Pet Food

- 6.3.1.8 Other Food Products

- 6.3.2 Foodservice

- 6.3.3 Beverage

- 6.3.4 Healthcare

- 6.3.5 Cosmetics and Personal Care

- 6.3.6 Industrial

- 6.3.7 Building and Construction

- 6.3.8 Automotive

- 6.3.9 Other End User Industries

- 6.3.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 PT. Berlina Tbk

- 7.1.2 PT Indo Tirta Abadi

- 7.1.3 PT.Solusi Prima Packaging

- 7.1.4 PT. Indorama Ventures Indonesia

- 7.1.5 Indo Cap Closures

- 7.1.6 PT. Hasil Raya Industries

- 7.1.7 PT. Hokkan Deltapack Industri

- 7.1.8 PT Rheem Indonesia

- 7.1.9 PT. Neilsen

- 7.1.10 PT. Namasindo Plus

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging vs. Established Players

8 RECYCLING & SUSTAINABILITY LANDSCAPE

9 FUTURE OUTLOOK

2025 年硬質塑膠包裝全球市場報告

2025 年硬質塑膠包裝全球市場報告 硬質塑膠包裝市場規模、佔有率、成長分析、按產品類型、按原料、按生產過程、按最終用途、按地區 - 行業預測,2024-2031 年

硬質塑膠包裝市場規模、佔有率、成長分析、按產品類型、按原料、按生產過程、按最終用途、按地區 - 行業預測,2024-2031 年 硬質塑膠包裝市場:按原料、產品類型、製造流程和應用分類 - 2025-2030 年全球預測

硬質塑膠包裝市場:按原料、產品類型、製造流程和應用分類 - 2025-2030 年全球預測 硬質塑膠包裝市場:依原料、類型、應用、地區劃分,2024-20312024-2032 年按產品、材料(聚乙烯、聚丙烯、高密度聚丙烯等)、生產流程、最終用途產業和地區分類的硬塑膠包裝市場報告

硬質塑膠包裝市場:依原料、類型、應用、地區劃分,2024-20312024-2032 年按產品、材料(聚乙烯、聚丙烯、高密度聚丙烯等)、生產流程、最終用途產業和地區分類的硬塑膠包裝市場報告 2024-2028年全球硬質塑膠包裝市場

2024-2028年全球硬質塑膠包裝市場 硬質塑膠包裝市場,按產品類型、按應用、按材料、按配銷通路、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測硬質塑膠包裝市場報告:2030 年趨勢、預測與競爭分析

硬質塑膠包裝市場,按產品類型、按應用、按材料、按配銷通路、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測硬質塑膠包裝市場報告:2030 年趨勢、預測與競爭分析 硬質塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029 年硬質塑膠包裝市場:依材料、製造流程、最終用戶產業:2023-2032 年全球機會分析與產業預測

硬質塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029 年硬質塑膠包裝市場:依材料、製造流程、最終用戶產業:2023-2032 年全球機會分析與產業預測