|

市場調查報告書

商品編碼

1644463

亞太地區玻璃瓶和容器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Asia-Pacific Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

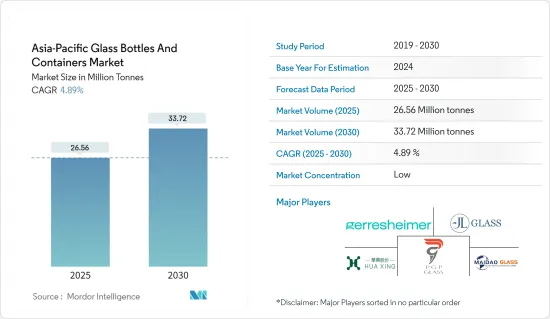

預計 2025 年亞太地區玻璃瓶和容器市場規模將達到 2,656 萬噸,預計到 2030 年將達到 3,372 萬噸,預測期內(2025-2030 年)的複合年成長率為 4.89%。

主要亮點

- 在亞太地區,食品飲料和製藥業正在推動玻璃包裝需求的快速成長。需求的成長主要歸功於全部區域的塑膠包裝禁令、永續性舉措和完善的回收基礎設施。

- 國際貿易中心的資料顯示,中國在亞洲玻璃包裝出口中佔據主導地位,2023 年出口量為 1,898,260 噸,其次是印度,出口量為 357,747 噸。隨著兩國擴大出口,也增加對尖端生產技術的投資。除了卓越的產品品質外,這種先進的包裝還能簡化流程、降低成本,使玻璃相對於其他包裝替代品更具競爭力。

- 在印度,由於人們對酒精飲料的偏好日益成長,玻璃包裝行業預計將擴張。玻璃酒瓶尤其受歡迎,因為它們可以防止葡萄酒因陽光照射而變質。加拿大農業和食品部預測,到 2025 年印度的葡萄酒消費量將達到 5,220 萬公升,這將進一步增加對玻璃包裝的需求。

- 對一次性塑膠的嚴厲打擊導致人們對玻璃等替代品的關注度增加。在日本,與其他包裝材料相比,回收玻璃瓶的財務支出非常經濟。日本容器包裝回收協會的資料顯示,2023年玻璃瓶的回收成本為琥珀色瓶每公斤約8.2日圓(0.058美元),無色透明瓶每公斤約6日圓(0.042美元)。這些成本效益促使製造商轉向玻璃包裝。

- 製造玻璃是一項能源密集產業,需要高溫來熔化原料。這種能源需求可能會推高營運成本,特別是在能源價格上漲和環境法規嚴格的地區。此外,矽石、堿灰和石灰石等主要原料價格波動可能會進一步增加生產成本。

亞太地區容器玻璃市場趨勢

飲料佔市場佔有率最大

- 在亞太包裝玻璃市場中,飲料業佔據約60%的市場佔有率,在推動市場成長方面發揮著舉足輕重的作用。

- 消費者越來越意識到使用玻璃容器而非塑膠容器對健康的益處,尤其是用於盛裝飲料。玻璃無毒,不會將化學物質滲入產品中,長期使用是安全的,尤其是盛裝酒精飲料時。預計消費者偏好的這些變化將推動容器玻璃市場的成長。

- 隨著經濟的不斷發展和中階的壯大以及購買力的提高,中國的包裝產業正在快速且穩定地成長。飲料市場的擴大推動了包裝需求的增加,尤其是玻璃容器領域。雖然每種飲料類別都有其獨特的挑戰和機遇,但中國消費者生活方式的新趨勢正在塑造對玻璃包裝的需求。

- 中國都市區的酒精和非酒精飲料消費量正在增加。具有古老根源的酒精飲料包括米酒、葡萄酒、啤酒、威士忌和各種蒸餾酒。白酒仍是中國消費量最大的蒸餾酒。

- 根據港交所披露,2021年濃香型白酒銷售額約2,860億元(404.2億美元),佔中國白酒銷售額的一半以上。預計到 2026 年濃香型白酒銷售額將達到 3,129 億元(442.2 億美元)。

- 韓國飲酒文化不僅限於飲酒,也涵蓋傳統的搭配食物。韓國料理以其濃烈、辛辣的口味而聞名,常與酒搭配。從傳統的米酒到日益流行的日本燒酒,酒在韓國社會和文化中扮演著重要的角色。該市場的主要特徵是生產供大眾消費的低成本日本燒酒品牌。

- 玻璃包裝對於飲料儲存有幾個優點。它是永續的、可無限回收的、可重複使用的、可再填充的、不含合成化學物質且惰性。這些特性使玻璃成為安全包裝飲料的可行選擇。

- 日本可口可樂公司正在實施各種永續性,例如去除飲料上的塑膠標籤和降低自動販賣機的耗電量。這符合該公司在 2030 年全球回收 25% 的包裝並推出可重複使用的包裝(包括玻璃瓶)的承諾。這些努力正在促進該地區玻璃容器市場的成長。

- 消費者健康意識的不斷增強推動了對具有多種健康益處的機能飲料的需求。玻璃包裝符合這一趨勢,因為它被認為是一種安全衛生的選擇,可以保存飲料的營養價值,從而支持玻璃包裝市場的成長。

- 根據香港交易及結算所有限公司的資料,2019年中國機能飲料零售額達約158.2億美元,預計至2024年將達248.2億美元。

印度佔據了顯著的市場成長

- 對乳製品的需求不斷增加,推動了玻璃包裝設計的創新。製造商可能會投資研發來開發更方便、耐用和美觀的玻璃瓶和容器。預計此類技術創新將促進亞太地區玻璃包裝市場的成長。

- 乳製品行業對永續性和環保包裝解決方案的關注正在推動可回收並可多次重複使用的玻璃容器的進一步應用。

- 印度在全球牛奶生產中的主導地位進一步支持了這一趨勢。根據Invest India統計,印度的原乳產量居世界首位,佔世界牛奶產量的25%。 2014-15 年至 2022-23 年間,印度的原乳產量預計將增加 58%,達到 2.3058 億噸。牛奶產量的大幅成長導致對優質包裝解決方案的需求增加,玻璃瓶成為優質乳製品的首選包裝瓶。

- 軟性飲料製造商正在積極推廣使用玻璃瓶。 2023年3月,可口可樂印度公司 Thumbs Up 發起了一項名為「Toofan Glass Mein Nahin, Glass Se Peete Hain」的電視宣傳活動,鼓勵消費者體驗可回收玻璃瓶裝的飲料。該公司的目標是到 2030 年,全球銷售的飲料中至少有 25% 採用可重複使用或可回收的容器,包括汽水供應機和玻璃瓶裝飲料。

- 此項舉措不僅促進了永續性,而且還提升了消費者體驗,因為眾所周知,玻璃瓶比其他包裝材料更能保存飲料的碳酸化和風味。

- 非酒精飲料,尤其是軟性飲料的成長預計也將影響玻璃包裝的市場需求。隨著消費者健康意識的增強,天然和有機飲料的消費量也隨之增加,這些飲料通常採用玻璃瓶包裝以保持其純度和新鮮度。此外,精釀蘇打水和手工飲料等高階非酒精飲料通常選擇玻璃包裝來傳達品質和奢華感。

- 酒精飲料出口的增加推動了對玻璃瓶和容器的需求。玻璃包裝因能夠保持風味和品質而成為酒精飲料的首選。據APEDA稱,印度23會計年度的酒精飲料出口額預計將達3.16億美元,比上年度增加3,800萬美元。

- 由於國際市場通常對進口酒精飲料的品質和包裝有嚴格的要求,出口的成長導致對優質玻璃包裝的需求增加。此外,該地區精釀啤酒廠和釀酒廠的興起為特殊玻璃瓶和容器創造了一個利基市場,進一步推動了玻璃包裝行業的成長。

亞太地區容器玻璃產業概況

亞太地區容器玻璃市場較為分散,幾家主要參與者爭奪市場佔有率。這些公司不斷投資於策略夥伴關係和產品開發,以鞏固其市場地位。

市場的主要企業包括跨國公司和區域製造商。這些公司專注於擴大生產能力、加強分銷網路和開發創新包裝解決方案,以滿足客戶的多樣化需求。其他公司進行併購是為了加強其市場地位並獲得新技術或細分市場的機會。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 容器玻璃進出口資料

- 容器玻璃市場的PESTEL分析

- 玻璃包裝行業標準和法規

- 包裝玻璃的原料分析及材料考量

- 玻璃包裝的永續性趨勢

- 亞太地區容器玻璃熔爐和位置

第5章 市場動態

- 市場促進因素

- 永續包裝解決方案需求不斷成長推動玻璃使用

- 製藥業對玻璃包裝的偏好日益增加

- 市場挑戰

- 高製造成本和能源成本限制了容器玻璃市場的成長

- 貿易概況 - 亞太地區容器玻璃產業進出口模式的歷史與現狀分析

第6章 市場細分

- 按最終用戶產業

- 飲料

- 酒精

- 啤酒和蘋果酒

- 葡萄酒和烈酒

- 非酒精性

- 碳酸飲料

- 汁

- 水

- 乳類飲料

- 調味飲料

- 食物

- 化妝品

- 藥品(不含管瓶和安瓿瓶)

- 其他最終用戶產業

- 飲料

- 按國家

- 中國

- 印度

- 日本

- 泰國

- 澳洲和紐西蘭

- 韓國

- 越南

第7章 競爭格局

- 公司簡介

- Gerresheimer AG

- Guangdong Huaxing Glass Co., LTD

- Maidao Industry Co. Ltd

- JL Glass Co., Ltd

- PGP Glass Private Limited

- KOA GLASS CO., LTD.

- AGI glaspac

- CANPACK GROUP

- Emerge Glass

- JAPAN SEIKO GLASS CO.,LTD.

第8章 補充資料:區域內主要容器玻璃廠主要窯爐供應商分析

第9章:未來市場展望

The Asia-Pacific Glass Bottles And Containers Market size is estimated at 26.56 million tonnes in 2025, and is expected to reach 33.72 million tonnes by 2030, at a CAGR of 4.89% during the forecast period (2025-2030).

Key Highlights

- In the Asia-Pacific region, the food, beverage, and pharmaceutical sectors are driving a surge in demand for glass containers. This uptick is largely attributed to bans on plastic packaging, a push for sustainability, and a well-established recycling infrastructure throughout the region.

- Data from the International Trade Centre highlights China's dominance in Asia's glass container exports, tallying 1,898,260 tons in 2023, with India trailing at 357,747 tons. As both nations ramp up their export activities, they're poised to channel investments into cutting-edge production technologies. Such advancements promise not only superior product quality but also streamlined processes, potentially slashing costs and bolstering the competitiveness of glass containers against other packaging alternatives.

- In India, the rising appetite for alcoholic beverages is set to propel the glass container industry's expansion. Glass bottles, especially for wine, are favored for their protective qualities against sunlight-induced spoilage. Agriculture and Agri-Food Canada forecasts India's wine consumption to hit 52.2 million liters by 2025, further amplifying the demand for glass packaging.

- With the crackdown on single-use plastics, there's been a notable pivot towards alternatives like glass. In Japan, the financial outlay for recycling glass bottles stands out as more economical compared to other packaging materials. Data from the Japan Containers and Packaging Recycling Association reveals that in 2023, recycling costs for amber and colorless glass bottles were about JPY 8.2 (USD 0.058) and JPY 6 (USD 0.042) per kilogram, respectively. Such cost benefits are nudging manufacturers towards glass packaging.

- Producing glass is an energy-intensive endeavor, demanding elevated temperatures to melt raw materials. This energy requirement can inflate operational costs, particularly in areas grappling with surging energy prices or stringent environmental mandates. Moreover, fluctuations in the prices of key raw materials like silica, soda ash, and limestone can further escalate production expenses.

Asia-Pacific Container Glass Market Trends

Beverage Occupies the Largest Market Share

- The beverage industry's dominance, accounting for approximately 60% of the market share in the Asia-Pacific container glass market, plays a pivotal role in driving the market's growth.

- Consumers are increasingly aware of the health benefits of using glass over plastic, particularly for beverages. Glass is non-toxic, does not leach chemicals into the product, and is considered safer for long-term use, especially in alcoholic beverages. This shift in consumer preference is expected to fuel growth in the container glass market.

- China's packaging industry is experiencing rapid and steady growth, fueled by the country's expanding economy and a growing middle class with increased purchasing power. The beverage market's expansion is driving a heightened demand for packaging, particularly in the glass container segment. While each beverage category presents unique challenges and opportunities, emerging trends in Chinese consumer lifestyles are shaping the demand for glass packaging.

- China's major urban areas have witnessed an increase in the consumption of both alcoholic and non-alcoholic beverages. Alcoholic beverages, with roots in ancient times, include rice wine, grape wine, beer, whiskey, and various spirits. Baijiu remains the most consumed distilled spirit in China.

- According to HKEXnews, in 2021, Nongxiang flavor baijiu generated revenue of approximately CNY 286 billion (USD 40.42 billion), accounting for over half of China's baijiu sales revenue. The revenue from Nongxiang flavor baijiu is projected to reach CNY 312.9 billion (USD 44.22 billion) by 2026.

- Korean drinking culture extends beyond alcohol consumption to include traditional accompanying foods. Korean cuisine, known for its intense and spicy flavors, often complements alcohol consumption. From traditional rice wines to the increasingly popular soju, alcohol plays a central role in Korean society and culture. The market is predominantly characterized by low-priced brands producing soju for mass consumption.

- Glass packaging offers several advantages for beverage storage. It is sustainable, infinitely recyclable, reusable, refillable, and inert, containing no synthetic chemicals. These properties make glass a viable option for packaging beverages safely.

- Coca-Cola Japan has implemented various sustainability initiatives, including removing plastic labels from drinks and reducing power consumption in vending machines. This aligns with the company's global commitment to recycle 25% of packaging worldwide by 2030 and implement reusable packaging, including glass bottles. Such initiatives are contributing to the growth of the glass container market in the region.

- Increasing health and wellness awareness among consumers is driving demand for functional beverages, which are perceived to offer various health benefits. Glass packaging aligns with this trend as it is considered a safe and hygienic option for preserving the nutritional integrity of beverages, thus supporting the growth of the glass containers market.

- According to Hong Kong Exchanges and Clearing Limited, the retail sales of functional beverages in China reached nearly USD 15.82 billion in 2019 and are projected to reach USD 24.82 billion by 2024.

India to Account for Significant Market Growth

- The increasing demand for dairy products is driving innovation in glass packaging design. Manufacturers are likely to invest in research and development to create glass bottles and containers that offer improved convenience, durability, and aesthetic appeal. This innovation is expected to contribute to the growth of the Asia-Pacific glass packaging market.

- The dairy industry's focus on sustainability and eco-friendly packaging solutions further propels the adoption of glass containers, as they are recyclable and can be reused multiple times.

- India's dominant position in global milk production further supports this trend. According to Invest India, the country leads worldwide milk production, contributing 25% of the global output. India's milk production increased by 58% between 2014-15 and 2022-23, reaching 230.58 million tonnes in 2022-23. This significant growth in milk production has led to an increased demand for high-quality packaging solutions, with glass bottles being a preferred choice for premium dairy products.

- Soft drink manufacturers are actively promoting the use of glass bottles. In March 2023, Coca-Cola India's Thumbs Up launched a television campaign, 'Toofan Glass Mein Nahin, Glass Se Peete Hain,' encouraging consumers to experience the beverage from returnable glass bottles. The company aims to sell at least 25% of its beverages globally in reusable or returnable containers by 2030, including drinks sold at soda fountains and in glass bottles.

- This initiative not only promotes sustainability but also enhances the consumer experience, as glass bottles are known to maintain the beverage's carbonation and flavor better than other packaging materials.

- The growth in non-alcoholic beverages, particularly soft drinks, is also expected to impact the market demand for glass packaging. The rising health consciousness among consumers has led to an increase in the consumption of natural and organic beverages, which are often packaged in glass bottles to maintain their purity and freshness. Additionally, the premium segment of non-alcoholic beverages, including craft sodas and artisanal drinks, often opts for glass packaging to convey a sense of quality and luxury.

- Increased exports of alcoholic beverages are driving demand for glass bottles and containers. Glass packaging is preferred for alcoholic beverages due to its ability to preserve flavor and quality. According to APEDA, in the financial year 2023, India's export value of alcoholic beverages reached USD 316 million, an increase of USD 38 million from the previous year.

- This growth in exports has led to a higher demand for premium glass packaging, as international markets often have stringent quality and packaging requirements for imported alcoholic beverages. Furthermore, the rise of craft breweries and distilleries in the region has created a niche market for specialized glass bottles and containers, further driving the growth of the glass packaging industry.

Asia-Pacific Container Glass Industry Overview

The Asia-Pacific container glass market is characterized by fragmented, with several major companies competing for market share. These companies consistently invest in strategic partnerships and product development initiatives to strengthen their positions in the market.

Key players in the market include multinational corporations and regional manufacturers. These companies often focus on expanding their production capacities, enhancing their distribution networks, and developing innovative packaging solutions to meet diverse customer needs. Some firms also engage in mergers and acquisitions to consolidate their market presence and gain access to new technologies or market segments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL Analysis of Container Glass Market

- 4.4 Industry Standard and Regulation for Container Glass Use for Packaging

- 4.5 Raw Material Analysis and Material Consideration for Packaging

- 4.6 Sustainability Trends for Glass Packaging

- 4.7 Container Glass Furnace and Location in Asia- Pacific Region

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Sustainable Packaging Solutions Boosting Glass Use

- 5.1.2 Growing Pharmaceutical Industry Preference for Glass Packaging

- 5.2 Market Challenge

- 5.2.1 High Manufacturing and Energy Costs Limiting Growth in the Container Glass Market

- 5.3 Trade Scenerio - Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in Asia-Pacific

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.2 Non-Alcoholic

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Juices

- 6.1.1.2.3 Water

- 6.1.1.2.4 Dairy Based Drinks

- 6.1.1.2.5 Flavored Drinks

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical (Excluding Vials and Ampoules)

- 6.1.5 Other End-User Vertical

- 6.1.1 Bevarages

- 6.2 By Country

- 6.2.1 China

- 6.2.2 India

- 6.2.3 Japan

- 6.2.4 Thailand

- 6.2.5 Australia and New Zealand

- 6.2.6 South Korea

- 6.2.7 Vietnam

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Gerresheimer AG

- 7.1.2 Guangdong Huaxing Glass Co., LTD

- 7.1.3 Maidao Industry Co. Ltd

- 7.1.4 JL Glass Co., Ltd

- 7.1.5 PGP Glass Private Limited

- 7.1.6 KOA GLASS CO., LTD.

- 7.1.7 AGI glaspac

- 7.1.8 CANPACK GROUP

- 7.1.9 Emerge Glass

- 7.1.10 JAPAN SEIKO GLASS CO.,LTD.

8 SUPPLEMENTARY COVERAGE - ANALYSIS OF MAJOR FURNACE SUPPLIERS TO MAJOR CONTAINER GLASS PLANTS IN THE REGION

9 FUTURE OUTLOOK OF THE MARKET

玻璃瓶和容器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)非洲玻璃瓶和容器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

玻璃瓶和容器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)非洲玻璃瓶和容器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 玻璃瓶和容器市場規模、佔有率和成長分析(按產品、應用、顏色、最終用途產業和地區分類)—產業預測(2026-2033 年)

玻璃瓶和容器市場規模、佔有率和成長分析(按產品、應用、顏色、最終用途產業和地區分類)—產業預測(2026-2033 年) 2025-2029年全球玻璃瓶與容器市場英國玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)中東和非洲玻璃瓶和容器市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)拉丁美洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)

2025-2029年全球玻璃瓶與容器市場英國玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)中東和非洲玻璃瓶和容器市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)拉丁美洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030) 玻璃瓶及容器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

玻璃瓶及容器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球玻璃瓶和容器市場

全球玻璃瓶和容器市場